Medium Business Auto Insurance: Scalable Coverage for Growing Companies

Medium business auto insurance doesn’t work the same way as coverage for small startups or large enterprises. As your fleet grows, your risks change, your costs climb, and standard policies often leave gaps that can hurt your bottom line.

We at ISU Insurance Solutions Group help growing companies find coverage that actually matches where they are today and where they’re heading tomorrow. This guide walks you through what matters most when scaling your fleet.

The Real Cost of Growth

Commercial Auto Premiums Rise Faster Than Your Fleet

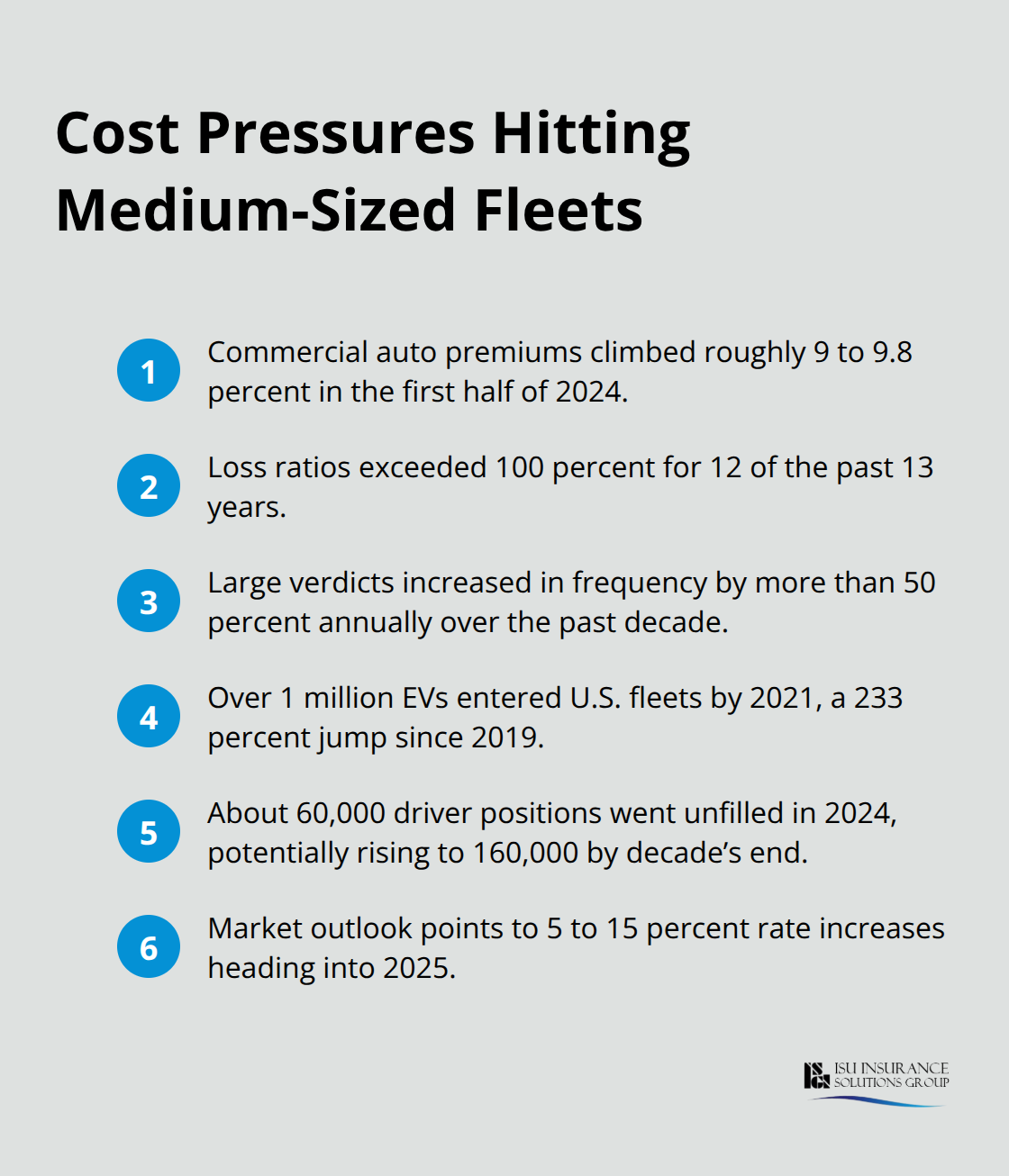

Commercial auto premiums climbed roughly 9 to 9.8 percent in the first half of 2024, according to industry loss data. Carriers reported loss ratios above 100 percent for 12 of the past 13 years, meaning insurers paid out more in claims than they collected in premiums. This tighter capacity and higher scrutiny hit your renewal hard when you expand your fleet.

Nuclear verdicts and social inflation have accelerated the problem. Large verdicts increased in frequency by more than 50 percent annually over the past decade, pushing commercial auto claims up roughly 30 billion dollars since 2012. Medium-sized fleets sit in a difficult position: you’re too large for startup-friendly policies, yet you lack the negotiating power of major enterprises.

Why Standard Policies Fail Growing Operations

Standard policies designed for small operations don’t account for the complexity of managing multiple drivers, diverse vehicle types, or the liability exposure that comes with scaling. Repair costs have surged due to supply chain delays and advanced driver-assistance systems (ADAS-enabled repairs can cost twice as much as traditional repairs, according to the American Automobile Association). The total cost of risk becomes impossible to ignore when you factor in longer downtime and higher salvage values.

The Driver Shortage Pushes Your Rates Higher

The trucking industry faces a severe driver shortage. Roughly 60,000 positions went unfilled in 2024, with potential openings rising to 160,000 by decade’s end. This shortage forces companies to hire less experienced drivers or retain drivers longer despite higher loss history, both of which spike your rates. Experienced driver retention becomes a competitive advantage when loss history directly impacts your premiums.

Electric Vehicles Add New Risk Layers

Over 1 million electric vehicles entered U.S. fleets by 2021, a 233 percent jump since 2019. While initial EV insurance premiums run higher, the real risk lies in cyber threats from connected charging systems and lithium-ion battery fire hazards that traditional repair networks aren’t equipped to handle. Your fleet composition now determines not just your coverage needs but also your exposure to emerging technologies.

Growth Creates Coverage Gaps Mid-Year

As you add vehicles and drivers, your coverage needs shift, but most policies lock you into fixed terms that don’t flex when your operation changes. You end up either over-insured and overpaying, or under-insured and exposed. The market outlook suggests 5 to 15 percent rate increases heading into 2025, making it critical to lock in scalable coverage now rather than scrambling for options when renewal hits. Understanding how your specific growth trajectory affects your coverage requirements separates companies that control costs from those that get blindsided by renewal.

How Your Fleet Composition Shapes Coverage and Cost

Vehicle Types Drive Your Risk Profile and Premium

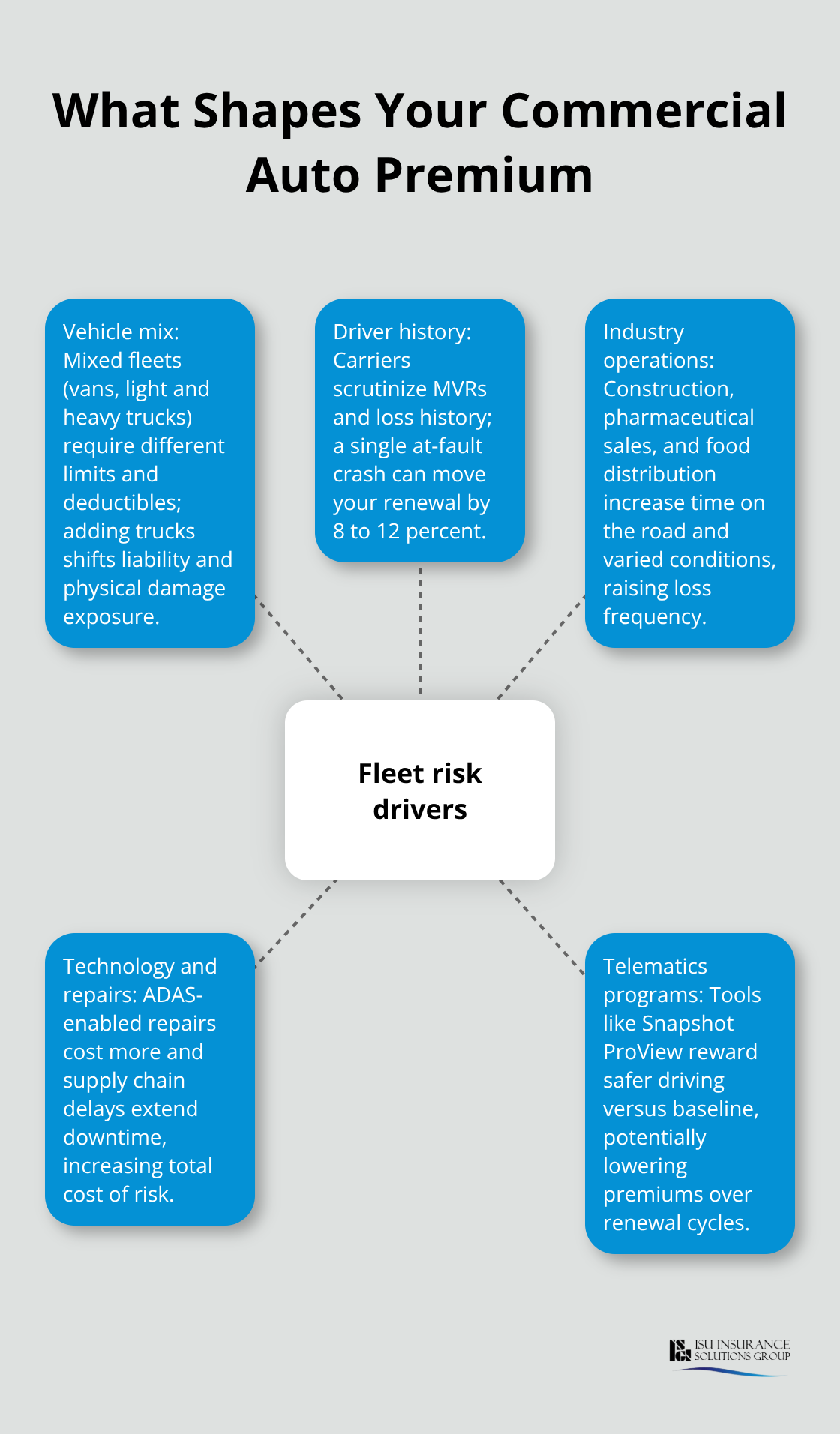

Most medium-sized businesses treat their fleet as a single unit rather than recognizing that each vehicle type, driver profile, and operational pattern creates distinct risk exposure. Your coverage structure must reflect what you actually operate, not what worked for your competitor down the street. A mixed fleet of passenger vans, light trucks, and heavy trucks demands different liability limits, collision deductibles, and hired-auto coverage than a uniform fleet of sedans.

When you add a box truck to your operation, your premium doesn’t just tick up slightly-your entire risk profile shifts. Repair costs for commercial trucks run significantly higher than passenger vehicles, and the liability exposure from carrying cargo or equipment introduces new claims scenarios that standard coverage wasn’t designed to handle. Map your current vehicles against your growth plan now. If you’re planning to add specialty vehicles-refrigerated units, lift gates, or equipment carriers-those need endorsements and higher physical damage limits before you put them on the road, not after your first accident reveals the gap.

Driver History and Loss Patterns Control Your Renewal Rate

Driver history and loss patterns matter far more than most business owners realize, and this is where medium-sized fleets face real pressure. Carriers scrutinize your motor vehicle records and loss history more closely than they did five years ago because claim costs have spiraled. A single at-fault accident on one driver’s record can push your entire fleet’s renewal rate up 8 to 12 percent, according to industry underwriting standards.

Your driver qualification standards become a cost-control tool. Establish minimum MVR requirements before hiring, conduct regular motor vehicle record reviews at renewal, and document your driver safety training programs. Carriers reward companies that demonstrate loss-control discipline with better rates. This investment in driver vetting and training directly lowers what you pay at renewal.

Industry-Specific Operations Amplify Your Exposure

Industry-specific factors amplify pressure on your rates further. If you operate in construction, pharmaceutical sales, or food distribution, your drivers spend more time on the road in varied conditions, increasing frequency of loss. Construction contractors face higher exposure from job-site vehicle use and equipment theft, while delivery operations accumulate more mileage and weather-related incidents.

The solution isn’t to accept higher rates as inevitable. Work with an agent who understands your specific industry’s risk profile and can structure your coverage, deductibles, and loss-control programs to reflect your actual operations. Bundling commercial auto with general liability or property coverage can yield savings on the auto line itself. Telematics programs like Progressive’s Snapshot ProView monitor real driving behavior, potentially lowering premiums if your fleet performs better than baseline assumptions.

Structuring Coverage to Match Your Actual Operations

The math is straightforward: a company that invests in driver training, maintains clean MVRs, and structures coverage to match its specific risk profile pays significantly less at renewal than one hoping general coverage will suffice. Your fleet composition determines not just what you need to buy today, but also how your coverage must adapt as you add vehicles and drivers. This flexibility in your policy structure-the ability to add vehicles mid-term without penalty, adjust liability limits as your operation expands, and layer endorsements for specialty equipment-separates scalable coverage from policies that force you to choose between overpaying for protection you don’t need or gambling on gaps that could devastate your business.

Cutting Costs Without Sacrificing Protection

Bundle Coverage to Lock in Immediate Savings

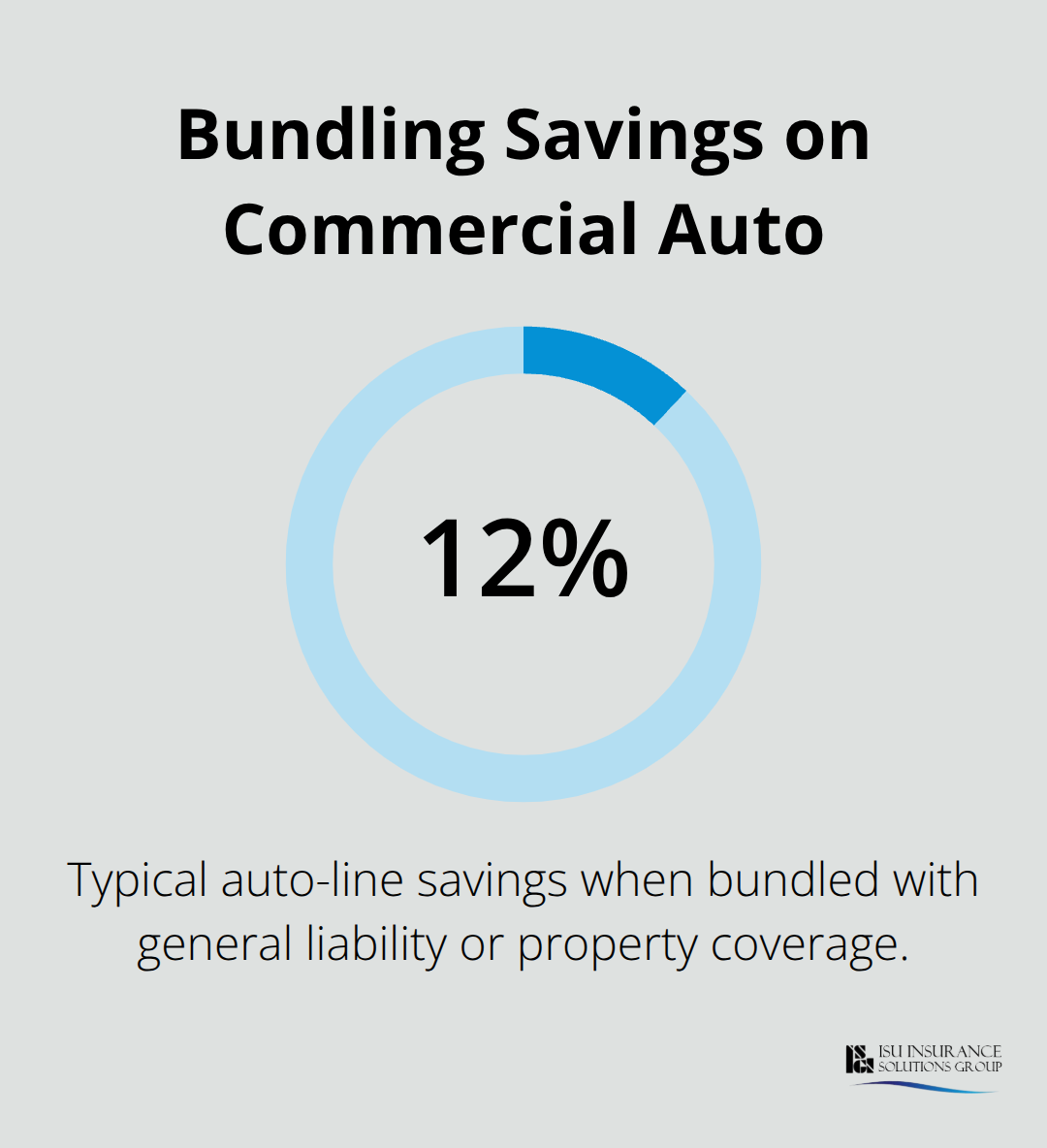

Bundling commercial auto with other business coverages delivers real savings that add up fast. When you pair auto insurance with general liability or property coverage, you typically save around 12 percent on the auto line itself, according to industry bundling data. For a medium-sized fleet paying $3,000 to $5,000 monthly in auto premiums, that’s $360 to $600 annually just from consolidating policies with one carrier. More importantly, bundling forces you to work with a single agent who understands your entire risk picture, not fragmented coverage across multiple insurers who don’t communicate.

Leverage Multi-Vehicle Discounts as Your Fleet Grows

Multi-vehicle discounts tier upward as your fleet grows, rewarding you for consolidation rather than penalizing you for expansion. Some carriers offer 5 to 10 percent reductions when you hit specific vehicle thresholds, typically at 5, 10, or 25 vehicles. The math matters: a fleet of 12 vehicles at a baseline $250 monthly per vehicle costs $36,000 annually. A 7 percent multi-vehicle discount saves $2,520 per year. Telematics programs add another layer of cost control by monitoring actual driver behavior rather than relying on historical loss data alone. If your fleet demonstrates safer driving patterns than baseline assumptions, you unlock additional premium reductions that compound over multiple renewal cycles.

Use Loss Control Programs to Reduce Claims and Premiums

Claims management and loss control directly shape what you pay at renewal, yet most medium-sized businesses treat claims as inevitable rather than preventable. Carriers now expect documented driver safety programs, regular motor vehicle record reviews, and clear qualification standards before hiring. Companies that implement these programs see 8 to 15 percent premium reductions at renewal compared to those with passive loss histories. This means establishing a baseline: pull MVRs on every driver before they touch a company vehicle, repeat the process annually, and document training attendance.

When an accident happens, your response matters as much as the incident itself. Carriers distinguish between companies that investigate losses thoroughly and implement corrective measures versus those that simply pay claims and move on. A single at-fault accident can trigger an 8 to 12 percent rate increase across your entire fleet at renewal, but that damage multiplies if you fail to demonstrate you’ve addressed the underlying cause.

Work with an Agent Who Coordinates Your Risk Management

Your agent should review your motor vehicle records quarterly, help you implement telematics where it makes sense, and coordinate with carriers on loss-control initiatives that reduce claims frequency. This relationship-centered approach separates companies that control costs from those that watch premiums climb unpredictably at each renewal cycle. An agent who coordinates claims management and loss control keeps your exposure visible and actionable, ensuring coverage adjusts as you add vehicles and drivers without forcing you into renewal surprises.

Final Thoughts

Medium business auto insurance works best when it scales with your operation rather than forcing you to choose between overpaying for static coverage or gambling on gaps that could derail your growth. Premiums are climbing, carriers are tightening capacity, and standard policies designed for smaller operations leave you exposed. Your competitive advantage comes from locking in scalable coverage now that adjusts as you add vehicles and drivers, rather than scrambling for options when renewal hits with rate increases of 5 to 15 percent.

Map your current fleet composition against your growth plan for the next 12 to 24 months, identify which vehicle types you’ll add, and determine how many drivers you’ll hire. Implement driver safety programs and motor vehicle record reviews before expansion accelerates-companies that document loss-control discipline see 8 to 15 percent premium reductions at renewal compared to those with passive loss histories. Work with an agent who coordinates across multiple carriers and understands how bundling, multi-vehicle discounts, and telematics programs reduce your total cost of risk.

Contact ISU Insurance Solutions Group to discuss how your fleet composition and growth trajectory shape your coverage needs and costs. We help growing companies in Washington and Oregon structure coverage that matches where you are today and where you’re heading tomorrow. Rather than accepting renewal surprises, you can lock in competitive rates and scalable protection that grows with your operation.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.