Commercial Auto Insurance Washington: Rates, Regulations, and Coverage

Running a business in Washington means understanding your commercial auto insurance obligations. The state has specific requirements that differ from other regions, and getting them wrong can cost you thousands in fines or leave your company exposed.

We at ISU Insurance Solutions Group help Washington business owners navigate these rules while finding coverage that actually fits their needs. This guide breaks down rates, regulations, and the protection your fleet requires.

What Determines Your Commercial Auto Insurance Costs in Washington

Washington commercial auto insurance averages about $206 per month or $2,469 annually according to Insureon data, but this number tells only part of the story. Your actual premium depends on factors specific to your operation, and understanding them gives you real leverage to control costs.

How Your Fleet Characteristics Shape Your Rate

The number of vehicles you own directly impacts your rate because insurers view fleet size as a risk indicator. A single delivery van costs far less to insure than five service trucks. Vehicle type and value matter significantly too-a heavy-duty truck rated for cargo transport carries different risk than a standard pickup used occasionally for business. How you use these vehicles shapes your premium more than most owners realize. A contractor who hauls equipment daily faces steeper rates than one who primarily drives to job sites. Your location within Washington also influences pricing; urban areas with higher accident rates and theft typically cost more than rural regions.

The Role of Driver Records and Claims History

Claims history and driver records are non-negotiable factors that insurers scrutinize closely. One at-fault accident or a driver with traffic violations can spike your premium by hundreds annually. Your chosen deductibles and coverage limits directly affect what you pay monthly-higher deductibles lower premiums but increase out-of-pocket costs when claims happen.

Understanding Washington’s Rate Landscape

Washington’s insurance market operates differently than most states because the Office of the Insurance Commissioner reviews and approves all rate filings before insurers can implement them. This regulatory oversight means rates here stay relatively competitive compared to national averages. However, this does not mean all insurers price identically. Rates vary substantially between carriers, which is why shopping multiple quotes matters far more than accepting the first offer.

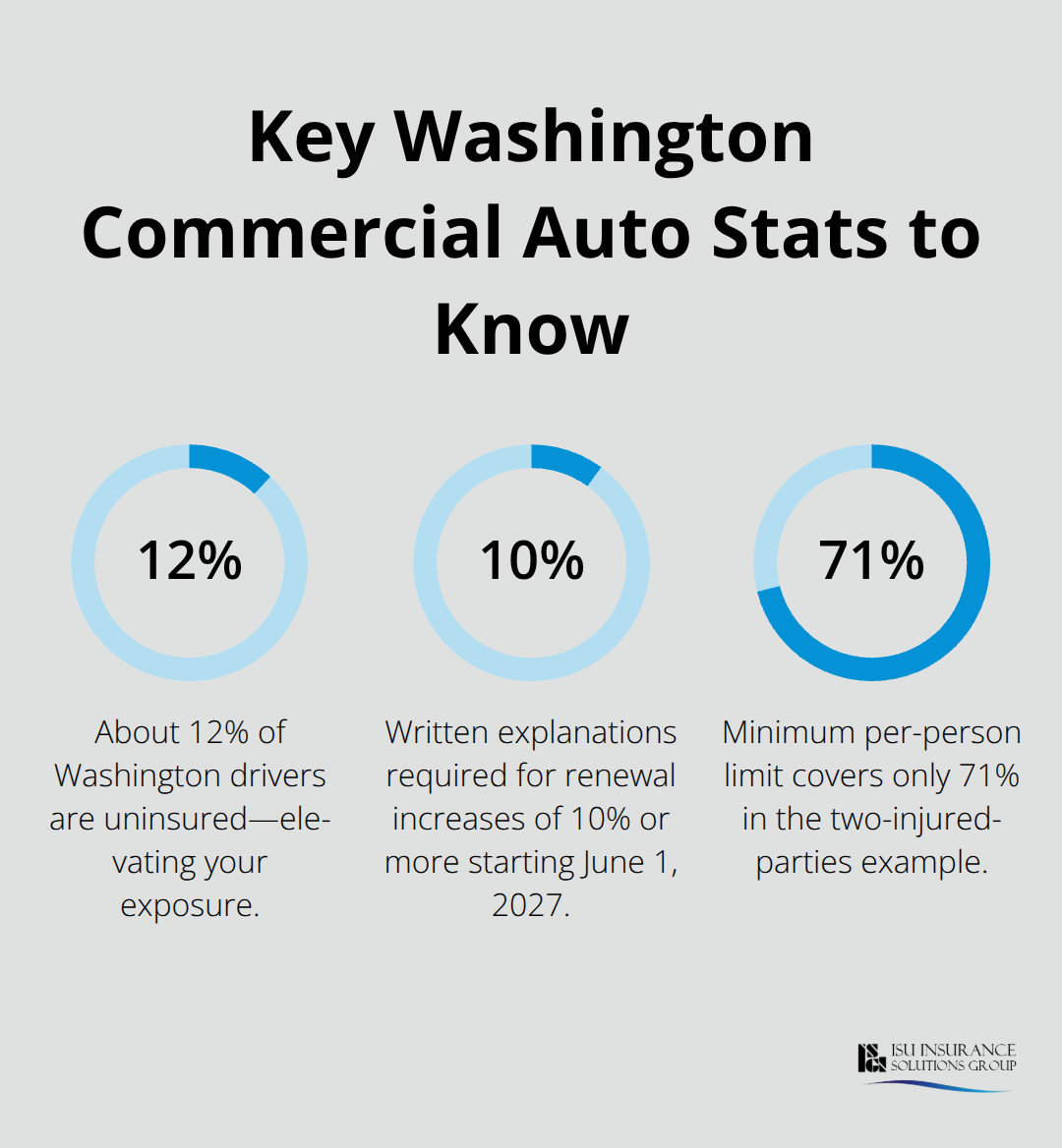

Some insurers specialize in specific industries like landscaping or construction and offer better pricing than generalists. Your best strategy involves requesting quotes from multiple carriers to identify which one values your particular risk profile most favorably. Request written explanations when comparing quotes so you understand exactly what drives price differences. Starting June 1, 2027, insurers must provide written explanations when your renewal premium increases by 10 percent or more, showing you the main reasons for the jump. This transparency requirement gives you concrete data to challenge unjustified increases or shop competitively. If you disagree with a rate increase, contact the Washington Office of the Insurance Commissioner’s Consumer Advocacy line at 800-562-6900 during business hours Monday through Friday, or use their online Ask an Insurance Expert form for assistance.

Practical Steps to Reduce Your Premium

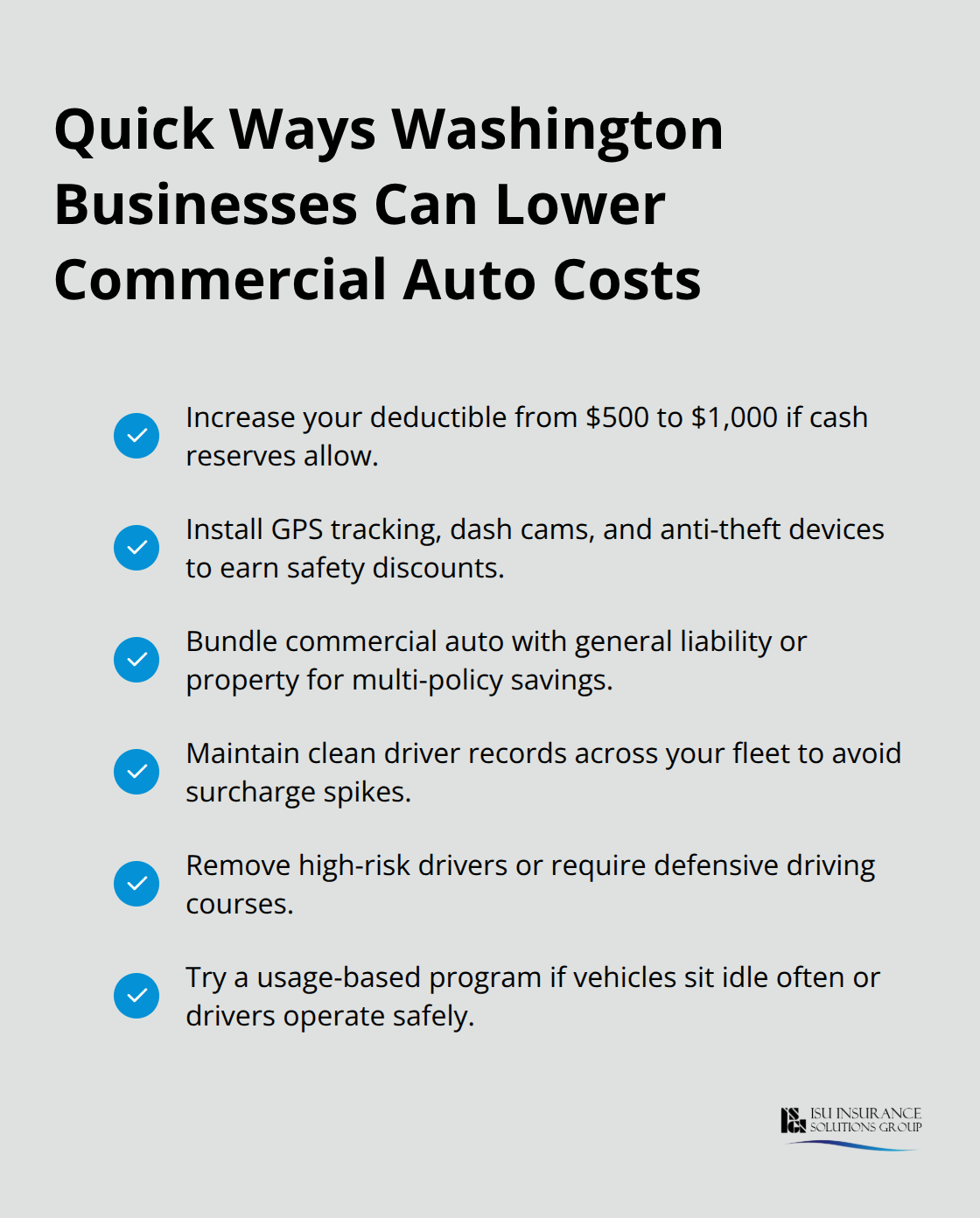

Increasing your deductible from $500 to $1,000 typically reduces your premium by 10 to 15 percent, making this the fastest way to lower costs if you have adequate cash reserves for claims. Installing safety devices like GPS tracking, dash cameras, or anti-theft systems on your vehicles qualifies you for discounts with many carriers because these reduce claim frequency. Bundling your commercial auto policy with other business coverage like general liability or property insurance often yields 10 to 20 percent discounts across your entire account.

Maintain clean driver records across your entire fleet because one driver’s violations can increase rates for your entire operation. Remove drivers with poor records from your policy or require them to complete defensive driving courses to demonstrate risk management to insurers. Usage-based insurance programs that track actual mileage and driving behavior can save money if your vehicles sit idle frequently or drivers operate safely. The key is finding an insurer willing to credit your specific operational practices rather than applying generic rates.

Now that you understand what shapes your costs, the next section covers the specific liability requirements Washington imposes on all commercial operators and how these regulations directly impact what coverage you must carry.

Washington’s Minimum Coverage Requirements and What They Actually Mean

Washington imposes non-negotiable minimum liability coverage that every commercial vehicle must carry: $25,000 per person and $50,000 per accident for bodily injury liability, plus $10,000 per accident for property damage liability. These minimums apply whether you operate a single service vehicle or manage a fleet of twenty trucks. Many business owners believe these minimums sufficiently protect them, but this assumption exposes your company to substantial financial risk. If your driver causes an accident injuring two people with $35,000 in damages each, your $25,000 per-person limit covers only 71 percent of actual costs. The injured parties can pursue your business assets for the remaining $45,000, which is why higher limits than Washington’s legal minimum make financial sense. A $100,000 per-person limit costs only marginally more than the minimum but shields your business from catastrophic liability claims that could force bankruptcy.

How Washington’s Regulatory Framework Differs from Other States

Washington’s regulatory environment differs sharply from other states because the Office of the Insurance Commissioner mandates that insurers must carry primary coverage during any period your driver is logged into a commercial transportation platform or actively provides a prearranged ride. This means your commercial auto policy must provide continuous protection, not just during active customer service periods. If you operate a rideshare or delivery service, your primary policy must include combined single limit liability of $1,000,000 during prearranged rides, plus underinsured motorist coverage of $100,000 per person and $300,000 per accident. These requirements exist because Washington law places the burden of claims directly on your business if your insurance lapses at any moment during commercial service.

Coverage Beyond the Minimum That Protects Your Operation

Washington does not require Personal Injury Protection or uninsured motorist coverage for standard commercial operations, but adding these protections is strategically sound. PIP coverage covers your employees’ medical expenses regardless of fault, preventing workers compensation claims from mounting, while underinsured motorist protection safeguards your operation when at-fault drivers carry insufficient insurance. These optional coverages function as financial buffers that absorb costs your minimum liability limits cannot reach. The difference between carrying only minimums and adding these protections often amounts to just $50 to $100 monthly-a small price against exposure that could devastate your business.

Deductible Selection and Its Impact on Your Budget

Your chosen deductible directly impacts your operational budget because you pay this amount out-of-pocket before insurance begins coverage. Selecting a $2,500 deductible instead of $500 can reduce your annual premium by 15 to 25 percent, but only if your cash reserves can absorb unexpected repair costs without disrupting operations. Lower deductibles ($500–$1,000) suit businesses with tight cash flow or those operating high-value vehicles, while higher deductibles work for established operations with substantial reserves. Test your deductible choice against your worst-case scenario: if a vehicle suffers major damage, can your business cover that deductible and still meet payroll and vendor obligations?

Understanding these regulatory requirements and coverage options positions you to make informed decisions about protection levels. The next section examines the specific types of commercial auto coverage available and which ones your particular business actually needs.

What Coverage Your Washington Business Actually Needs

Understanding Liability Coverage and Its Real Limits

Liability coverage forms the legal foundation of your commercial auto policy, but most Washington business owners misunderstand what it actually protects. Your liability coverage pays for injuries and property damage your driver causes to others-not damage to your own vehicle or injuries to your employees. Washington requires minimum liability coverage of at least $50,000 per person for bodily injury and $100,000 per accident. The injured party sues your business directly, and your liability limit becomes the financial ceiling of protection your company receives. If you cause an accident with $150,000 in damages but carry only the minimum, your business pays the remaining amount from operating capital or faces asset seizure.

Carrying limits of at least $100,000 per person and $300,000 per accident makes financial sense-the premium difference between minimums and these higher limits typically runs $30 to $60 monthly. This modest increase shields your business from catastrophic claims that could force bankruptcy.

Collision and Comprehensive Coverage for Vehicle Protection

Collision coverage pays to repair or replace your vehicles after accidents regardless of fault, while comprehensive coverage handles theft, vandalism, weather damage, and fire. These coverages are optional in Washington but essential if your vehicles have financed loans or lease obligations-lenders require them. The deductible you select for collision and comprehensive directly affects your monthly cost; a $1,000 deductible costs substantially less than $250, but you absorb that $1,000 out-of-pocket when damage occurs.

For vehicles worth less than $8,000, collision and comprehensive often cost more annually than the vehicle’s replacement value, making these coverages uneconomical unless financing requires them. Calculate your vehicle’s actual value before committing to these optional protections.

Medical Payments and Motorist Coverage for Accident Protection

Medical payments coverage covers employee and passenger medical expenses after an accident regardless of fault, protecting your business from workers compensation claims escalating when employees suffer injuries in company vehicles. Uninsured motorist coverage protects your operation when at-fault drivers carry no insurance-a reality affecting roughly 12 percent of Washington drivers according to insurance industry data. Underinsured motorist protection covers damages exceeding the at-fault driver’s policy limits, preventing your business from absorbing shortfalls when settlements fall short of actual costs.

These optional coverages function as financial buffers that absorb costs your minimum liability limits cannot reach. The difference between carrying only minimums and adding these protections often amounts to just $50 to $100 monthly.

Specialized Coverage for Specific Business Operations

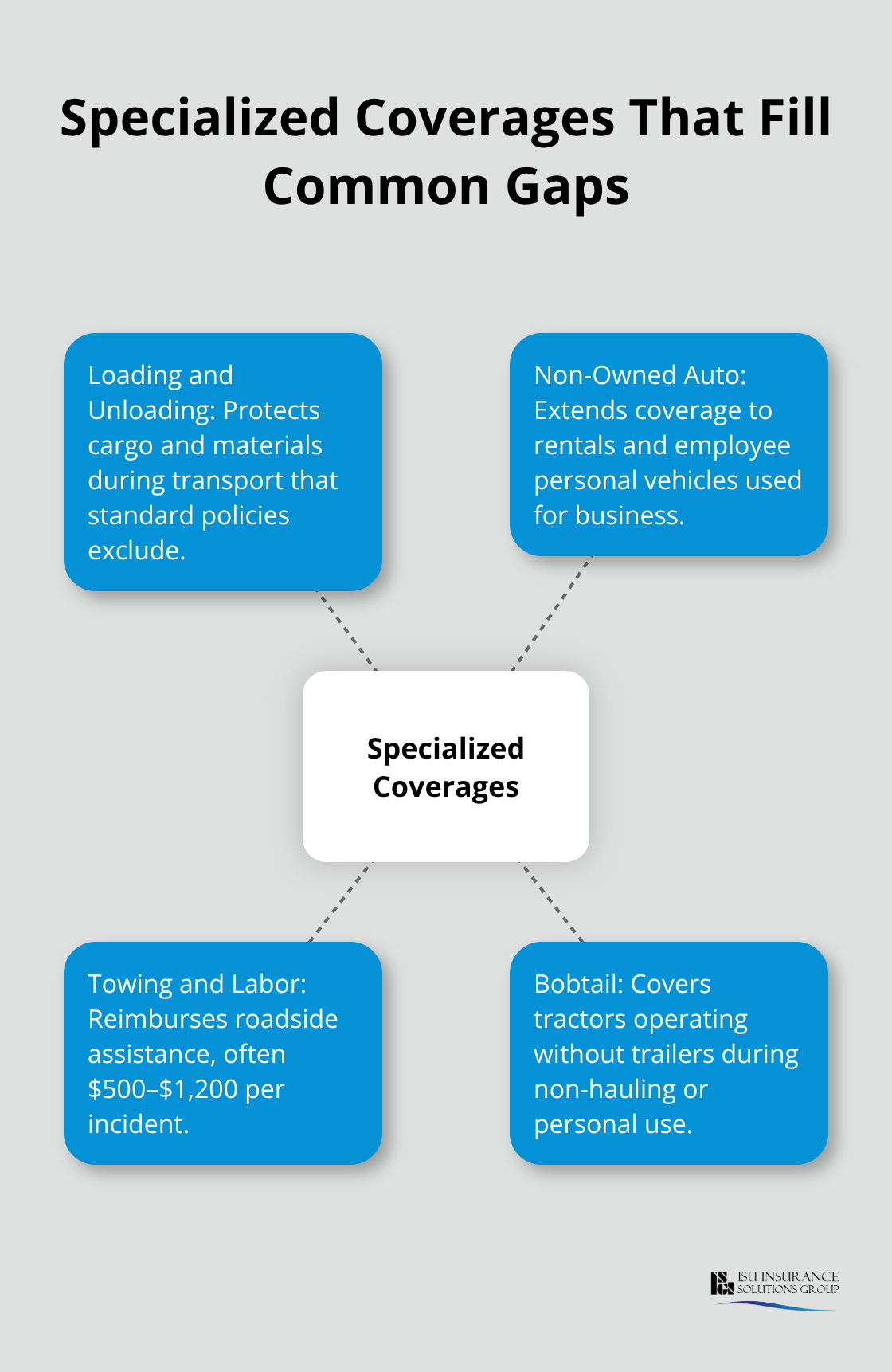

Loading and unloading coverage protects cargo and materials during transport, which standard policies explicitly exclude; contractors and delivery services absolutely need this if cargo damage represents a financial threat. Non-owned vehicle coverage extends protection to rental vehicles or employee personal vehicles used for business purposes, eliminating coverage gaps when your fleet cannot handle all business transportation needs. Towing and labor coverage reimburses roadside assistance costs, which matters for service businesses operating vehicles in remote areas where professional towing reaches $500 to $1,200 per incident.

Bobtail coverage insures tractors operating without trailers during non-hauling periods, critical for owner-operators who occasionally drive for personal use. The coverage combination that protects your business depends entirely on your operation’s specific risks, which is why generic policies from online quotes often miss critical gaps. An independent agent can identify which specialized coverages align with your actual operational risks rather than applying standard bundles that include unnecessary protection while leaving dangerous gaps.

Final Thoughts

Commercial auto insurance in Washington requires you to balance regulatory compliance with practical protection that matches your actual business risks. The minimum liability limits Washington mandates-$25,000 per person and $50,000 per accident for bodily injury-leave your business financially exposed when accidents exceed these thresholds, yet higher limits cost only marginally more and prevent catastrophic claims from forcing you to liquidate business assets. Your deductible selection, vehicle characteristics, driver records, and operational practices directly determine what you pay annually, giving you concrete levers to control costs without sacrificing protection.

The regulatory framework Washington enforces through the Office of the Insurance Commissioner creates transparency requirements that benefit your business. Starting June 1, 2027, insurers must explain premium increases of 10 percent or more in writing, giving you documented reasons to challenge unjustified hikes or shop competitively. Request quotes from multiple carriers because rates vary substantially between insurers, and some specialize in your specific industry and risk profile.

Getting the right commercial auto insurance Washington coverage means moving beyond generic online quotes that apply standard bundles missing your actual operational risks. Specialized coverages like loading and unloading protection, non-owned vehicle coverage, or bobtail insurance address specific business needs that standard policies explicitly exclude. ISU Insurance Solutions Group serves Washington and Oregon businesses since 1983, offering one-call multi-carrier quotes through partnerships with 20+ carriers, and their local agents understand Pacific Northwest operations to deliver personalized coverage that adapts to your specific risks and budget constraints.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.