Washington Winery Insurance Quotes: Compare Local Coverage

Washington winery insurance quotes require specialized knowledge that most standard business agents simply don’t have. Wine production involves unique risks-from fermentation hazards to inventory spoilage to liquor liability-that generic policies won’t cover properly.

We at ISU Insurance Solutions Group work with Washington wineries regularly, and we’ve seen too many owners settle for inadequate coverage. This guide walks you through exactly what coverage you need and how to compare quotes from carriers who actually understand Pacific Northwest operations.

Why Standard Business Policies Miss Winery Risks

A standard commercial general liability policy treats your winery like a typical retail business. That’s the problem. When Washington State Wine Commission data shows the state produces over 17 million cases annually across 60,000+ vineyard acres, and Cabernet Sauvignon vines alone carry a value around $13,000 per planted acre, your insurance needs to reflect agricultural production complexity plus hospitality exposure plus manufacturing hazards all at once.

Standard policies ignore fermentation tank ruptures, wine oxidation from cork failure, contamination from cleaning solvents left in barrels, and the specific liability exposure when someone gets injured at your tasting room. A generic business package won’t cover a 5,000-gallon tank failure that costs roughly $600,000 in lost revenue, nor will it protect you when a guest claims they were over-served. Washington’s modified dram-shop rule creates real legal exposure-your winery faces liability claims even when a third party bears some responsibility. Your property coverage must account for crush pads, catwalks, climate-controlled aging rooms, and temperature-sensitive equipment like glycol chillers that cost tens of thousands to replace. Skagit County’s 2023 rebuild index shows insulated steel structures jumped 19% year over year, meaning replacement costs for winery buildings have climbed sharply. Standard policies also miss wine-specific inventory valuation. You need options to value finished stock at selling price minus discounts, irreplaceable wines at market value on the loss date, or stock in process based on the previous three years for that varietal. Equipment breakdown coverage protects high-cost fermentation tanks and bottling machinery, but only if your policy specifically includes it-standard packages skip this entirely.

Liquor Liability Exposure That Generic Policies Exclude

Liquor liability is non-negotiable in Washington. Your tasting room pours create exposure that a typical retail general liability policy excludes completely. Product liability goes beyond standard coverage too-wine contamination claims, cork taint affecting entire vintages, or oxidation from synthetic closures require specific product liability language that addresses the realities of wine production. Spoilage coverage protects perishable inventory from equipment failure, power outages, or mechanical breakdown, protecting up to $25,000 per occurrence in specialized winery programs. Wine leakage coverage addresses valve failures and tank ruptures that standard property policies treat as maintenance issues rather than covered losses.

Inventory Valuation and Equipment Protection Gaps

Your aging inventory represents months or years of work. Standard business property coverage values stock at cost, not at selling price. Specialized winery programs recognize that a barrel of premium Pinot Noir isn’t worth its production cost-it’s worth what a customer pays. Contingent transit coverage protects wine you’ve sold when a carrier causes loss during shipment, covering up to $50,000 per shipment in standard winery packages. Equipment coverage must extend to vineyard-specific assets: grape vines, stakes, trellises, harvested grapes, and the specialized storage structures like wine caves and cellars. A vineyard-specific cap of $1,000 per grape vine acknowledges replanting costs after frost or disease. Tank collapse and implosion coverage addresses a physical risk unique to winemaking-fermentation vessels can fail under pressure or structural stress.

Mobile Operations and Distribution Risks

Washington wineries that handle their own distribution face additional exposure. Mobile bottling equipment and harvest logistics introduce inland-marine exposures that require dedicated commercial auto and cargo coverage. Box trucks and mobile operations need protection that standard policies treat as secondary risks rather than core business assets. These distribution channels create gaps that generic coverage simply doesn’t address, which is why comparing quotes from carriers who understand winery operations becomes essential when you’re ready to move forward with actual coverage options.

Getting Your Winery Quote Right

Document Your Operation With Precision

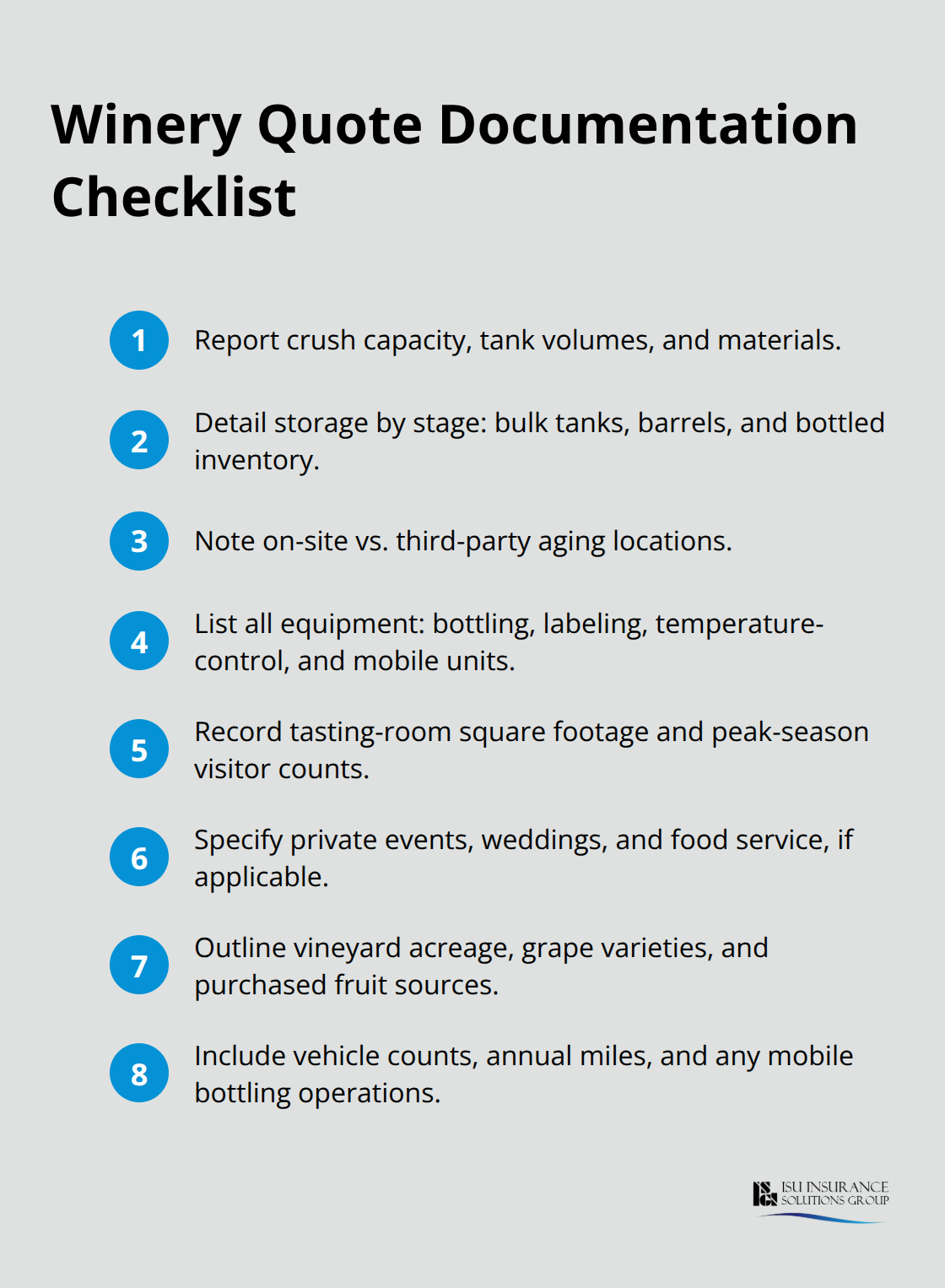

Accuracy in winery insurance quotes starts with honest documentation of what you actually operate. Most agents request basic business information, but winery quotes demand specifics that generic intake forms miss entirely. You need to document your crush capacity in tons per year, fermentation tank volumes and materials, storage methods across different wine stages, and whether you age wine on-site or use third-party facilities.

List every piece of equipment that touches your product: bottling lines, labeling machines, temperature-control systems, mobile equipment for harvest. Note your tasting-room square footage, average daily visitors during peak season, and whether you host private events or weddings. Include details about your vineyard acreage, grape varieties, and whether you purchase additional grapes from other Washington producers. If you operate your own distribution or use mobile bottling, specify vehicle counts and annual miles.

Value Your Inventory at Market Price, Not Production Cost

Washington wineries often underestimate their inventory value because they think in production costs rather than market value. A 5,000-case inventory of premium Pinot Noir at $35 retail represents $175,000 in finished goods value, not the $8,000 production cost. Carriers need exact numbers for wine stored in different conditions: bulk tanks, barrels, bottles in climate-controlled cellars, and any wine caves.

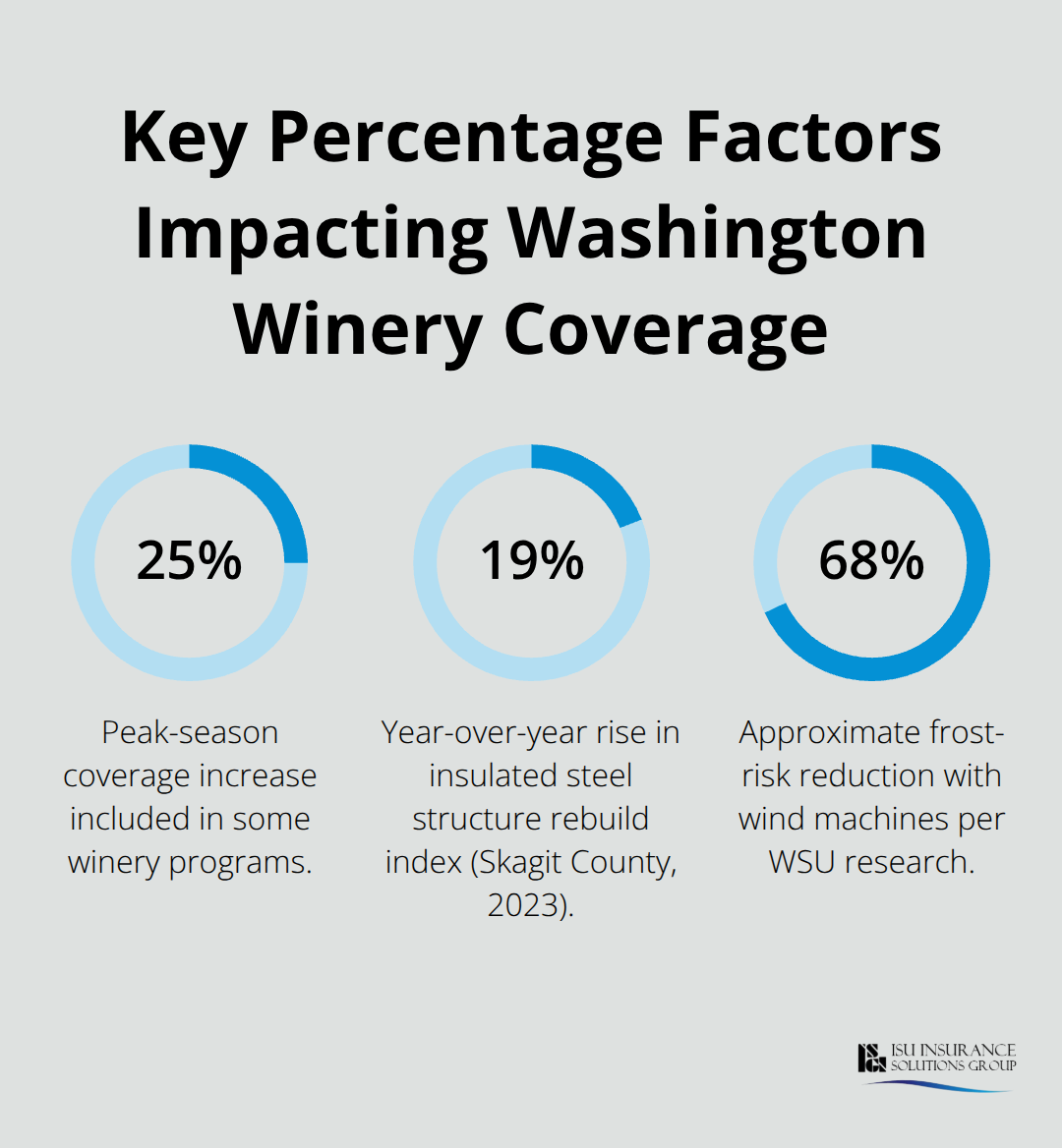

Winery inventory valuation uses methods including first-in, first-out (FIFO), specific identification, average cost and last-in first-out (LIFO). Skagit County’s 2023 rebuild index showed insulated steel structures increased 19% year over year, so provide current replacement-cost estimates for your buildings and specialized structures like crush pads and catwalks. This data helps carriers calculate accurate property limits that reflect actual rebuilding expenses.

Select an Agent With Winery-Specific Expertise

The agent you choose shapes your quote quality fundamentally. An agent unfamiliar with Pacific Northwest agriculture will miss frost-damage risks that Washington State University research shows wind machines reduce by about 68% in late-spring freezes, potentially lowering your property premiums if you operate these protections. Carriers specializing in agribusiness and beverage operations understand that Washington produces over 17 million cases annually across 19 AVAs with distinct risk profiles.

When evaluating agents, ask specifically whether they’ve quoted wineries in your county and what carriers they work with for wine-specific programs. A quality independent agency accesses multiple carriers rather than pushing one standard template. Request quotes that itemize coverage for wine leakage, oxidation, contamination from cleaning solvents, and valuation methods so you can compare apples to apples across proposals.

Compare Coverage Details Across Proposals

Some carriers offer blanket limits with no co-insurance clauses that simplify budgeting, while others use per-occurrence caps that create hidden gaps. Ask whether peak-season coverage automatically increases by 25% to reflect your highest inventory levels, as some winery programs include this adjustment. Request specific dollar limits for spoilage coverage, contingent transit protection, and processors’ liability if you send grapes to contract crushers.

The Washington State Liquor and Cannabis Board and federal Alcohol and Tobacco Tax and Trade Bureau impose specific regulatory requirements that affect your coverage design, so confirm your agent understands compliance obligations beyond insurance. When you receive quotes, compare them side by side using a spreadsheet that lists deductibles, limits, exclusions, and premium costs for each coverage type. A $2,000 deductible with a $500,000 limit at a lower premium might expose you to more risk than a $1,000 deductible with the same limit at higher cost, depending on your loss history and risk tolerance.

With your quotes in hand and coverage details clearly mapped, you’re ready to evaluate the specific protection types that separate adequate winery insurance from policies that leave you exposed.

Key Coverage Types Washington Wineries Need

General Liability Protects Your Tasting Room and Vineyard Operations

General liability covers bodily injury and property damage claims that occur when guests visit your property. A slip on wet tasting-room floors, a guest struck by equipment during harvest, or damage to a visitor’s vehicle parked on your grounds all trigger general liability exposure. Washington wineries face a specific risk that most other businesses don’t: your tasting room operates under modified dram-shop liability rules, meaning your winery can face legal claims if you serve alcohol to intoxicated customers who then cause harm.

Your general liability limit should reflect both your tasting-room traffic and your vineyard size. A small boutique operation with 50 visitors weekly faces different exposure than a facility drawing 500 visitors daily during peak season. Most carriers recommend minimum limits of $1 million per occurrence and $2 million aggregate for Washington wineries, though larger operations or those hosting frequent events should carry $3 million or higher.

Wine Inventory and Spoilage Protection Covers Your Most Valuable Assets

Your stock represents months or years of production cost plus market value waiting to be realized. Equipment breakdown coverage specifically protects fermentation tanks, glycol chillers, bottling lines, and temperature-control systems from mechanical failure, power outages, and electrical damage. A single power outage lasting 48 hours in your climate-controlled barrel room can spoil thousands of gallons of aging wine.

Spoilage coverage reimburses up to $25,000 per occurrence in most winery programs, though you should verify this limit matches your actual inventory value at risk. Wine leakage coverage addresses tank ruptures, valve failures, and barrel seepage that standard property policies treat as maintenance rather than insured losses. A 5,000-gallon tank failure costs approximately $600,000 in lost revenue when you factor in the wine itself plus the production time invested.

Liquor Liability Creates Mandatory Coverage Requirements in Washington

Liquor liability insurance is mandatory in Washington because your tasting-room pours create exposure that general liability excludes entirely. Unlike a retail store selling sealed bottles, your staff serves alcohol directly to guests, creating legal liability if someone over-served claims injury or property damage after leaving your property. Washington’s modified dram-shop rule means your winery can face liability if you serve alcohol to intoxicated customers who then cause harm.

Liquor liability premiums vary based on your tasting-room volume, number of events hosted, and whether you serve food alongside wine. A high-volume tasting room with frequent private events and weddings pays significantly more than a production-focused winery with minimal hospitality. Carriers examine your pour counts, event frequency, and staff training records when calculating premiums.

Some policies include product liability within liquor liability coverage, protecting you against claims that your wine caused harm, though you should confirm this explicitly because wine contamination, cork taint, or oxidation defects can trigger expensive recalls and customer claims. Request quotes that specify coverage limits of at least $1 million per occurrence for liquor liability, with defense costs included outside your limit rather than reducing your coverage when legal costs mount.

Final Thoughts

Your winery’s protection depends on coverage that reflects your actual operation, not a generic business template. Washington winery insurance quotes must include general liability with adequate tasting-room limits, liquor liability meeting Washington’s dram-shop requirements, equipment breakdown protection for fermentation tanks and chillers, spoilage coverage for inventory at risk, wine leakage and contamination protection, and property insurance covering crush pads and climate-controlled storage. Verify that your agent quotes wine-specific valuation methods-selling price for finished stock, market value for irreplaceable wines, and three-year averages for stock in process.

Local expertise matters because Washington winery risks differ fundamentally from operations in other regions. Frost damage patterns, wildfire smoke taint exposure, and the specific liability landscape under Washington’s modified dram-shop rule require agents who understand Pacific Northwest agriculture and hospitality combined. An agent unfamiliar with your county’s rebuild costs, frost-protection practices, or local carrier preferences will miss opportunities to lower premiums through risk-management credits.

Contact ISU Insurance Solutions Group to request quotes that itemize wine leakage, oxidation, contamination, valuation methods, and blanket limits so you can compare protection levels across carriers. Our Woodinville location puts us directly in the heart of Washington wine country, with local agents who understand the specific coverage gaps that generic policies create. The difference between adequate coverage and exposure that costs thousands in uninsured losses often comes down to working with agents who actually understand winery operations.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.