Fleet Auto Insurance: Eight Ways to Protect Your Vehicle Fleet

Fleet auto insurance protects your business, but only if you have the right strategy in place. Most fleet managers focus solely on finding cheap premiums and miss the bigger picture of risk management.

At ISU Insurance Solutions Group, we’ve seen firsthand how companies that combine strong safety practices with solid coverage avoid costly accidents and claims. This guide walks you through eight concrete steps to strengthen your fleet’s protection.

1. Build a Driver Safety Program That Actually Works

A comprehensive driver safety program isn’t about creating a binder of policies that nobody reads. It’s about establishing measurable expectations and holding drivers accountable. Write safety guidelines that cover specific behaviors: speed limits on different road types, following distance requirements, phone use restrictions, and how to handle adverse weather. These aren’t suggestions-they’re non-negotiables that every driver signs off on. Defensive driving training offers measurable returns that directly impact your bottom line.

Annual Motor Vehicle Record reviews catch violations early, and responding immediately to infractions prevents repeat offenses. Drivers who know their records are monitored change their behavior. Incentive programs work because they reward the behavior you want to see-offer bonuses, gift cards, or extra time off for drivers who complete a full year without accidents or violations. This approach shifts the culture from compliance-only to safety-first. High-risk drivers identified through violations or near-misses need targeted retraining on defensive techniques and vehicle-specific operations rather than generic safety lectures.

When you combine clear policies, regular training, consistent monitoring, and positive reinforcement, you create an environment where safe driving becomes the norm. This foundation makes everything else in your fleet protection strategy more effective. The next step involves adding technology that tracks driver behavior in real time and identifies patterns before they cause accidents.

2. Install Telematics and GPS Tracking Systems

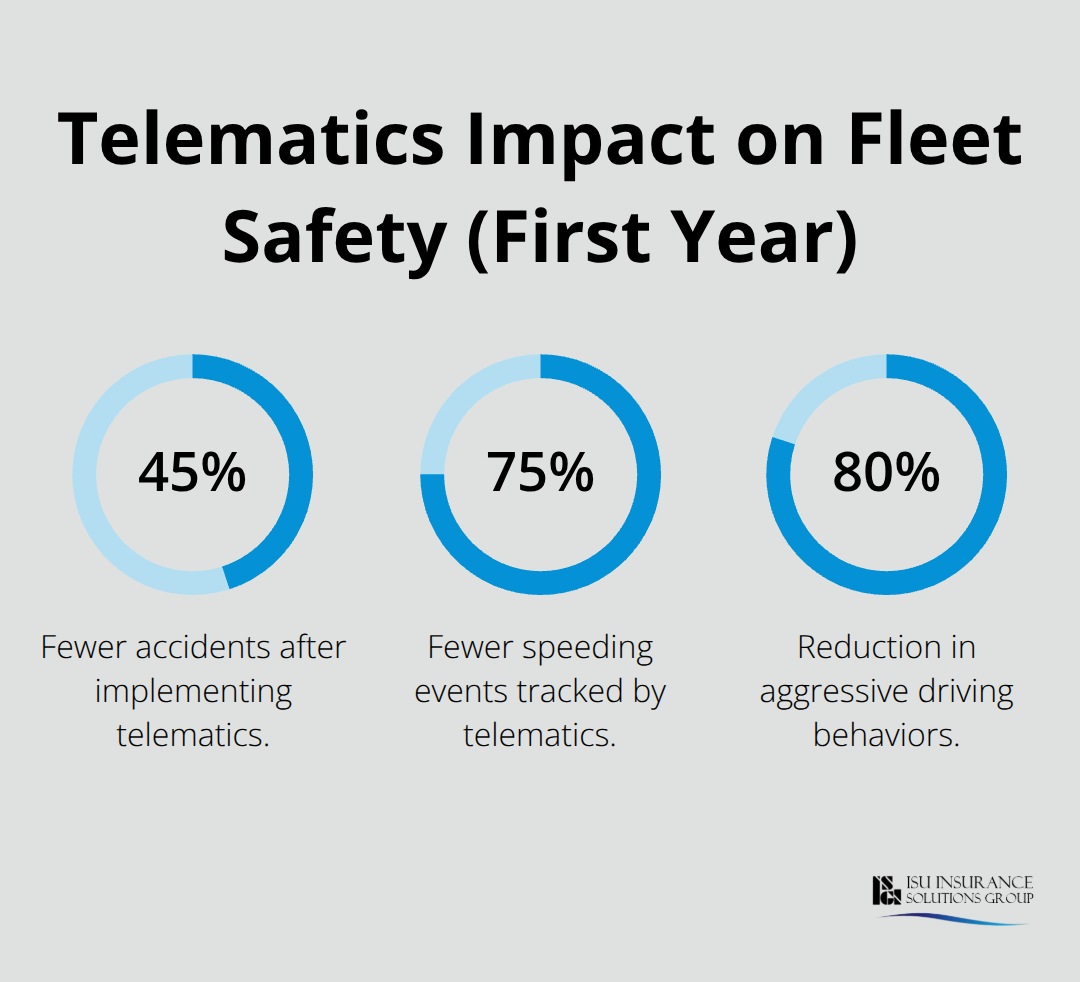

Telematics technology transforms fleet management from reactive to proactive by capturing real-time data on driver behavior, vehicle performance, and operational efficiency. Systems that monitor speeding, harsh braking, rapid acceleration, and idling patterns give you actionable insights into which drivers need coaching and which routes generate the most risk. Real-time GPS tracking and in-cab alerts prevent accidents by providing immediate feedback to drivers when they exceed safe thresholds. When you share this data with insurance carriers that offer usage-based discounts, you move beyond standard commercial auto rates and access pricing tied to actual performance rather than industry averages. Fleets that implement telematics typically see 45% fewer accidents, 75% fewer speeding events, and 80% reduction in aggressive driving within the first year.

Beyond safety, telematics delivers measurable cost reductions that justify the investment immediately. Idle-time monitoring eliminates unnecessary fuel waste and has saved fleets up to $3 million annually, while route optimization and fuel analytics reduce overall spend by identifying inefficient patterns and driver habits. Real-time vehicle diagnostics catch mechanical problems before they cause breakdowns, preventing costly repairs and reducing liability exposure from equipment failure. Documented case studies show $2.5 million in fuel savings, $1.1 million in maintenance cost reductions, and 23% improvement in vehicle utilization across customer fleets. The IDC study documents 8 times return on investment, meaning a $50,000 telematics deployment across a mid-sized fleet typically recovers costs within months and continues generating savings through reduced claims and operational efficiency.

With visibility into driver behavior and vehicle performance, you now need to protect that investment through consistent maintenance. The next step focuses on establishing a regular vehicle maintenance schedule that prevents breakdowns and catches safety issues before they escalate into claims.

3. Maintain a Maintenance Schedule That Prevents Claims

Preventive maintenance separates fleets that run smoothly from those that generate expensive insurance claims. Most fleet managers wait until something breaks, but that approach costs thousands in emergency repairs, downtime, and accident liability. Create a maintenance schedule tied directly to manufacturer recommendations and vehicle mileage intervals, then execute it without exception. Document every oil change, tire rotation, brake inspection, and fluid check in a centralized system so you have proof of compliance when an insurer reviews your risk management practices. Detailed service records signal to insurers that you take fleet protection seriously and often result in better rates or faster claims processing.

Safety recalls demand immediate action because ignoring them creates coverage gaps that can deny claims. If a vehicle fails due to a known defect that you neglected to address, your insurer may refuse to cover the resulting accident or injury claim. Check the National Highway Traffic Safety Administration website monthly for recalls affecting your vehicles and complete repairs within 30 days. Catching mechanical problems early through regular inspections prevents breakdowns that lead to accidents on the road. A transmission that slips slightly during routine maintenance is a minor repair; that same transmission failing at highway speed becomes a catastrophic collision with potential fatalities and six-figure liability exposure.

With your vehicles properly maintained and your drivers trained, the next critical step involves defining clear policies about who drives your fleet and under what circumstances they operate company vehicles.

4. Set Clear Vehicle Use and Assignment Policies

Vague vehicle policies create liability gaps that insurance companies exploit when claims arise. Define exactly who can operate company vehicles-not just job title, but specific names and driver qualifications-and document that authorization in writing. Establish non-negotiable rules about personal use, passenger policies, after-hours operation, and geographic boundaries that drivers cannot exceed. A driver using a company truck to move personal furniture on weekends or transporting unauthorized passengers creates exposure your insurer may refuse to cover if an accident occurs. Geographic restrictions matter because a regional delivery fleet operating within 50 miles of your base has fundamentally different risk than vehicles traveling across state lines, and your coverage must align with actual usage patterns.

Require drivers to report every accident and incident immediately, regardless of perceived severity. A minor fender-bender that goes unreported for weeks damages your credibility with insurers and complicates claims investigation when damage worsens or injuries surface later. Assign specific vehicles to individual drivers whenever possible because accountability eliminates the finger-pointing that delays incident response and claims resolution. When Driver A knows he operates Vehicle 5 every shift, he takes ownership of pre-trip inspections, maintenance needs, and safe operation in ways that shared vehicle fleets never achieve. Document all assignments in a simple spreadsheet that tracks which driver operated which vehicle on which dates-this becomes critical evidence if disputes arise about who caused damage or liability.

Clear, accessible policies reduce liability and boost accountability across departments. Your insurer can defend claims more effectively and you can demonstrate the risk controls that qualify for better rates. The next step involves screening the people who operate your vehicles before they ever get behind the wheel.

5. Screen Drivers Before and After You Hire Them

Most fleet accidents involve drivers with prior violations or suspended licenses that should have disqualified them from the job. Before hiring anyone to operate company vehicles, pull a comprehensive driving record check through the Department of Licensing to verify license validity, accident history, and outstanding violations. Your insurance policy sets minimum age and experience requirements-typically 21 years old with at least two years of driving history-and hiring drivers below those thresholds voids coverage on claims. Drug and alcohol testing during the hiring process isn’t optional if you want insurers to take your risk management seriously; random testing throughout employment catches substance abuse issues before they cause catastrophic accidents. A single DUI or reckless driving conviction increases accident likelihood dramatically, and documenting your screening process proves to insurers that you exercise reasonable care in driver selection.

Screen drivers before and after you hire them to reduce risks related to accidents and liability. Re-screen all drivers annually or whenever your insurance policy renews to catch license suspensions, new violations, or conviction records that emerged after employment began. A driver with a clean record at hire might accumulate three speeding tickets and a suspended license within 12 months, and failing to catch that creates massive liability exposure. Set a specific date each year-perhaps tied to your insurance renewal-and run fresh records on every driver in your fleet without exception. Drivers who accumulate violations should face retraining, reassignment to non-driving roles, or termination depending on severity. This systematic approach demonstrates to your insurer that you maintain active oversight of driver qualifications, which directly supports your case for competitive rates and faster claims processing. With your drivers properly vetted and monitored, the next step involves selecting coverage levels and policy structures that actually protect your fleet when accidents happen.

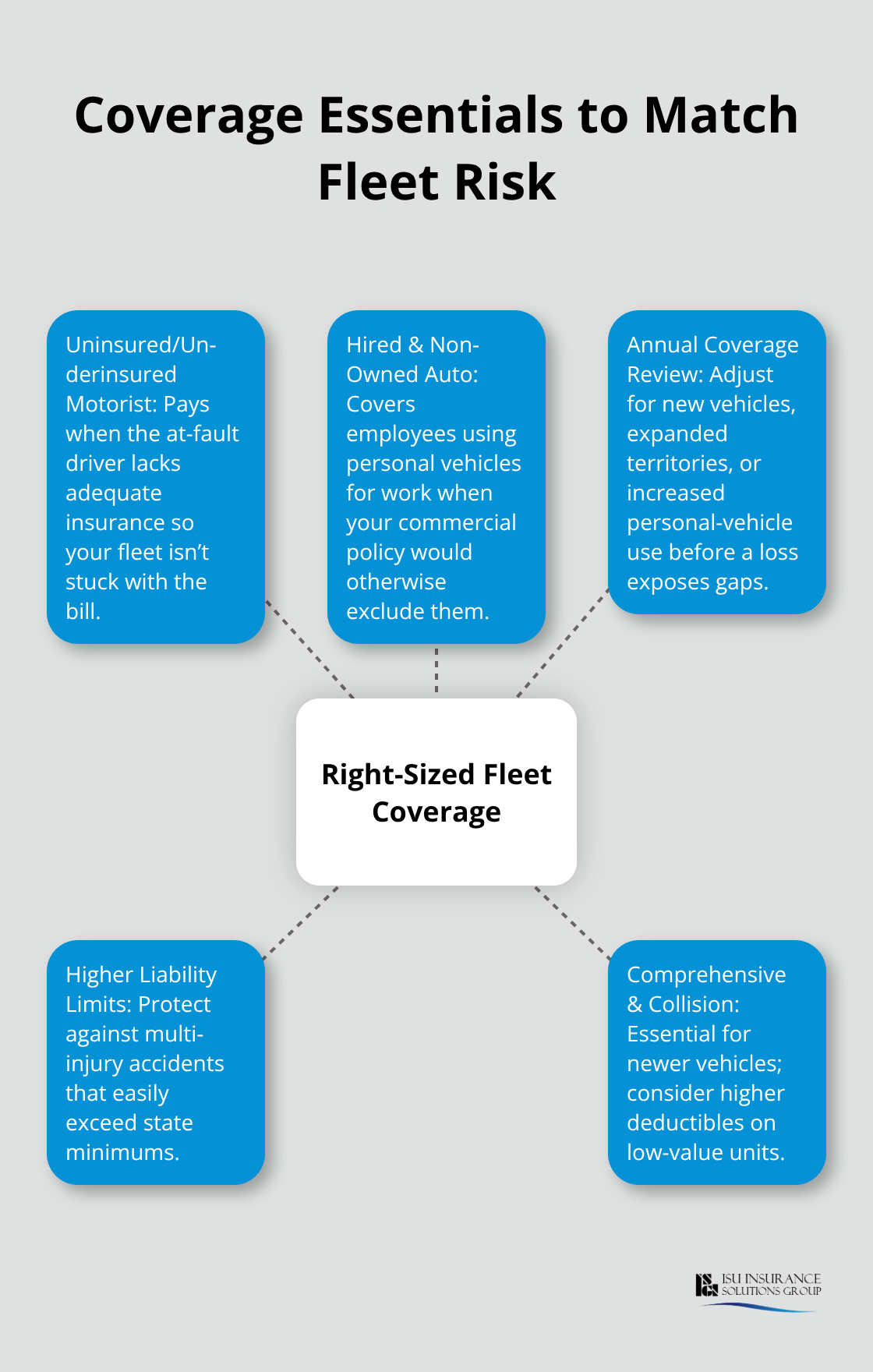

6. Select Coverage That Matches Your Fleet’s Actual Risk

State minimum liability limits exist as legal baselines, not as adequate protection for fleet operations. Most states require $15,000 to $25,000 in bodily injury liability per person, but a single serious accident involving multiple injured parties generates $200,000 to $500,000 in medical costs, lost wages, and pain-and-suffering claims that exceed those minimums by tenfold. Regional fleets should carry liability limits of at least $100,000 per person and $300,000 per accident, while vehicles traveling across state lines or operating in high-density urban areas need $250,000 per person and $500,000 per accident. The additional premium for higher limits costs roughly $400 to $800 annually per vehicle but protects your company from catastrophic judgments that force bankruptcy. Comprehensive and collision coverage becomes essential for vehicles newer than five years old, where replacement cost justifies the protection; for older units with market values under $5,000, raising deductibles to $1,000 or $2,500 reduces premiums while keeping coverage intact for major losses.

Uninsured and underinsured motorist coverage addresses the reality that approximately 13% of drivers nationwide carry no insurance, and many carry limits far below what they actually owe after causing serious injury. This coverage pays your claims when an at-fault driver cannot, preventing your fleet from absorbing losses caused by someone else’s negligence. If your drivers operate personal vehicles for work purposes (making client visits, attending meetings, or running errands), hired and non-owned auto coverage becomes mandatory because your commercial policy excludes those vehicles unless explicitly added.

Review your actual fleet operations annually to identify coverage gaps: new vehicles added, expanded geographic territory, or increased employee use of personal vehicles all demand policy adjustments before accidents expose those gaps. With your coverage structure locked in place, the next step involves creating a detailed accident response protocol that minimizes damage and protects your company when incidents occur.

7. Create an Accident Response Protocol That Protects Your Fleet

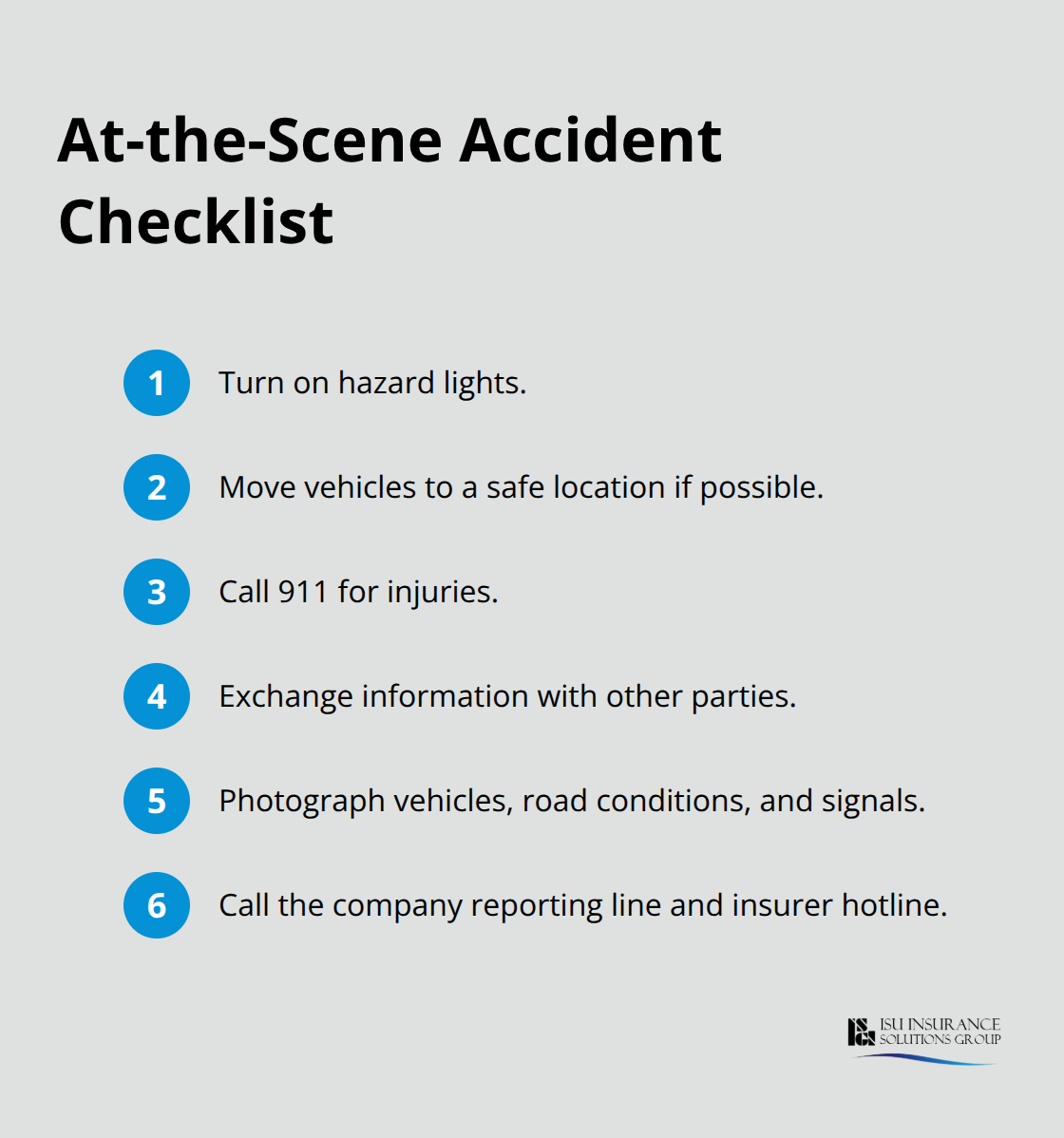

Accidents happen regardless of prevention efforts, but how your fleet responds determines whether claims get paid quickly or become disputed nightmares that drag on for months. Equip every driver with a laminated accident instruction card listing the exact steps to take at the scene: turn on hazard lights, move vehicles to a safe location if possible, call 911 for injuries, exchange information with other parties, and photograph everything before anyone moves vehicles. The card should include your direct reporting hotline number and your insurer’s claims hotline so drivers know exactly who to call without guessing or delays. Photographs must capture vehicle damage from multiple angles, road conditions, traffic signals, weather, and the other party’s vehicle and license plate.

Drivers who document scenes thoroughly give adjusters and defense attorneys clear evidence to support your claim, while poor documentation creates gaps that opposing counsel exploits to deny liability or reduce your recovery.

Require drivers to file reports within two hours of an accident, not the next day or whenever they remember-time delays allow witnesses to disappear and memories to fade. Review every accident within 48 hours to identify root causes and determine whether additional driver training or policy changes could prevent similar incidents. A driver rear-ending another vehicle at a traffic light signals need for defensive driving training focused on following distance and anticipating stops. A vehicle leaving the roadway on a curve at night suggests the driver was speeding or distracted, requiring targeted retraining or reassignment to lower-risk routes. Track patterns across your entire fleet: if three drivers have accidents during rain within a six-month period, implement inclement weather training for all operators. Document your accident reviews in writing and share findings with your insurer because demonstrating continuous improvement strengthens your case for competitive renewal rates. This systematic approach transforms accidents from isolated incidents into learning opportunities that strengthen your entire fleet’s safety culture and position you to work with an independent agent who specializes in commercial fleet coverage.

8. Partner with an Independent Agent Who Understands Fleet Operations

Most fleet managers shop for insurance the way they buy gas-finding the cheapest price and moving on. That approach costs thousands annually in missed discounts, inadequate coverage, and claims that get denied because policies don’t match actual operations. An independent agent with commercial fleet expertise accesses multiple carriers simultaneously and runs quotes from insurers that specialize in your specific industry, whether that’s construction, delivery, service calls, or regional transportation. Carriers that focus on fleet operations understand nuances that generalist insurers miss: they know how telematics investments lower claims, they recognize the value of formal driver training programs, and they reward documented safety practices with tangible premium reductions. A good agent compares not just price but coverage structures, deductibles, and policy limits across five to eight carriers, identifying which combination actually protects your fleet instead of creating gaps when accidents happen.

An independent agent serves as your advocate during claims disputes and policy reviews. When a driver causes a serious accident, your agent manages communication between your company, the insurer, and legal counsel to protect your interests and accelerate resolution. As your fleet grows-new vehicles added, operations expanded, or service territories changed-your agent adjusts coverage proactively rather than discovering gaps after incidents occur. They can manage multiple policies through multiple carriers for you, so you can get the best prices for the right coverage. Having a single point of contact who knows your fleet, your drivers, and your coverage eliminates the frustration of juggling multiple insurers and ensures consistency across renewals and claims, positioning you to implement the final protective layer that ties everything together.

Final Thoughts

The eight strategies outlined in this guide work together to create a comprehensive fleet auto insurance protection system that reduces accidents, lowers premiums, and keeps your drivers safe. Strong risk management practices alone won’t protect you if your coverage has gaps, and comprehensive coverage alone won’t prevent accidents if your drivers lack training and accountability. Fleet auto insurance delivers maximum value when you combine documented safety programs, technology investments, maintenance discipline, and policy structures that match your actual operations.

Lower accident frequency directly decreases claims and renewal premiums, while documented safety practices qualify you for carrier discounts ranging from 10% to 25% depending on your telematics data and driver training investments. Fewer breakdowns mean less downtime and reduced liability exposure from equipment failures. When you implement these eight steps systematically, your total cost of fleet operations drops significantly while your protection strengthens.

We at ISU Insurance Solutions Group have served Washington and Oregon businesses since 1983, building deep expertise in Pacific Northwest fleet operations across construction, delivery, service, and transportation sectors. Our independent agency accesses 20+ carriers simultaneously, comparing coverage and pricing to find solutions tailored to your specific fleet and regional exposure. Contact us now to review your current fleet auto insurance and identify which strategies need attention before the next accident exposes coverage gaps.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.