Brewery Bonds and Insurance: Meeting Bond Requirements and Protecting Growth

Running a brewery means navigating a complex web of federal permits, state regulations, and insurance requirements. Brewery bonds and insurance aren’t optional extras-they’re foundational to legal operation and financial stability.

At ISU Insurance Solutions Group, we’ve helped dozens of breweries understand what coverage they actually need versus what’s just noise. This guide walks you through the bonds required by law, the insurance that protects your operation, and how to identify gaps before they cost you.

Federal and State Brewery Bond Requirements

What Federal Regulations Require

The federal government requires breweries to post a Brewer’s Bond if their beer tax liability under a single EIN exceeds $50,000 in a calendar year-either this year or last year. This threshold comes from the PATH Act of 2015 and is enforced by the Alcohol and Tobacco Tax and Trade Bureau (TTB). The bond itself guarantees payment of federal excise taxes, penalties, and interest, acting as security for your tax obligations. If your liability stays under $50,000, you avoid federal bonding requirements, but you still need a TTB Brewer’s Notice to operate legally.

The TTB requires two bond forms depending on your situation: Form 5130.22 for a standard Brewer’s Bond or Form 5130.25 for a Brewer’s Collateral Bond. Minimum federal bond amounts are $1,000 for breweries and $500 for pilot brewing plants, though larger operations need significantly higher coverage. Bond terms last four years and can be renewed with a continuation certificate.

Federal Bond Costs and Timeline

Pricing typically runs about $12 per $1,000 of coverage for the first $25,000, $8 per $1,000 for the next $25,000, and $3.75 per $1,000 for amounts above $50,000 up to $400,000. You can purchase federal bonds instantly online for coverage up to $50,000. The TTB National Revenue Center at 877-882-3277 provides guidance on exact amounts and bond documentation.

State Bonds Add Substantial Costs

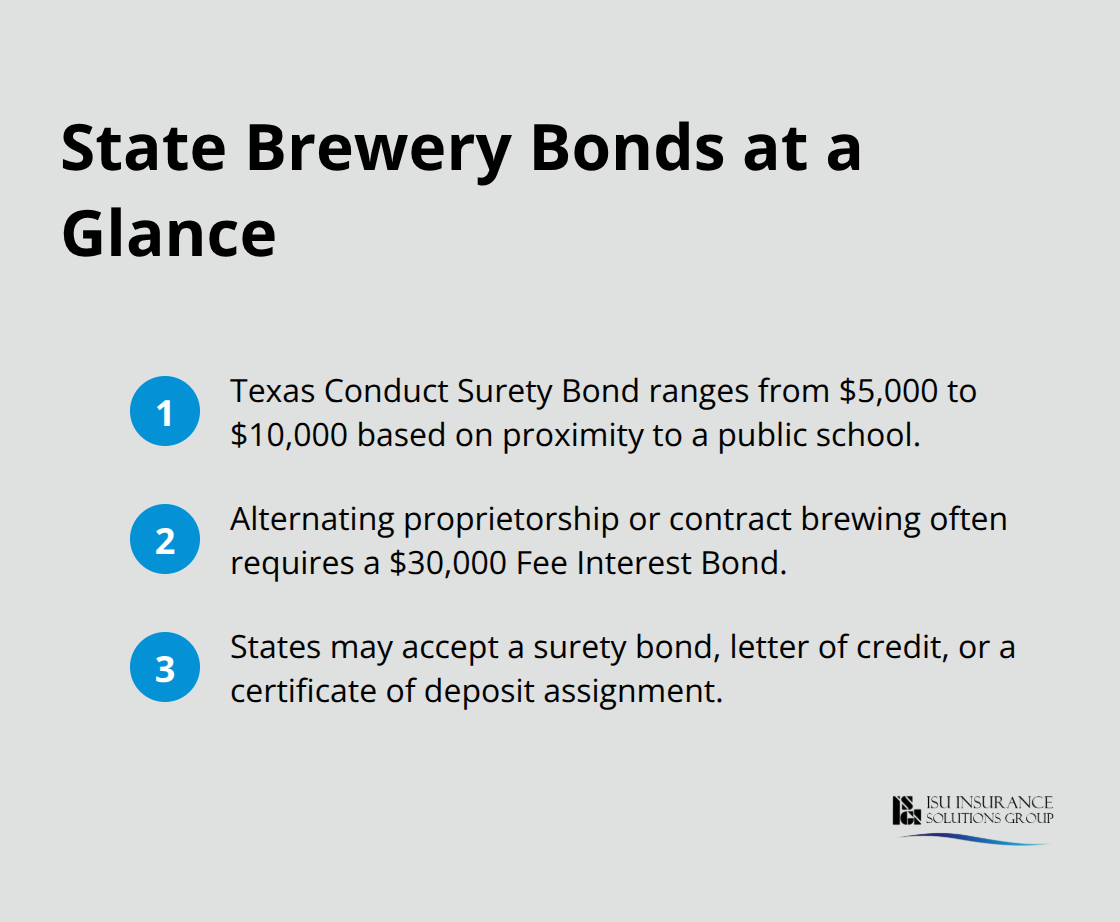

Most states require additional bonds separate from federal requirements. In Texas, for example, the TABC requires a Conduct Surety Bond ranging from $5,000 to $10,000 depending on your distance from a public school-a factor many breweries overlook during site selection. If you operate an alternating proprietorship or contract brewing arrangement, you’ll need a Fee Interest Bond of $30,000.

Washington and Oregon have their own licensing frameworks, and bonds can be satisfied as a traditional surety bond, a letter of credit, or an assignment of a certificate of deposit.

Common Submission Mistakes

The critical mistake breweries make is underestimating state bond costs during their financial planning phase. These bonds protect regulators and the public, not your business, so they’re non-negotiable for licensure. Processing delays happen when bonds aren’t submitted through the right channel-many states now require digital submission through their licensing systems rather than paper forms, which can add weeks to your permit timeline. Understanding your state’s specific submission requirements upfront prevents costly delays as you move toward opening.

What Insurance Do Breweries Actually Need

Coverage That Protects Beyond Legal Requirements

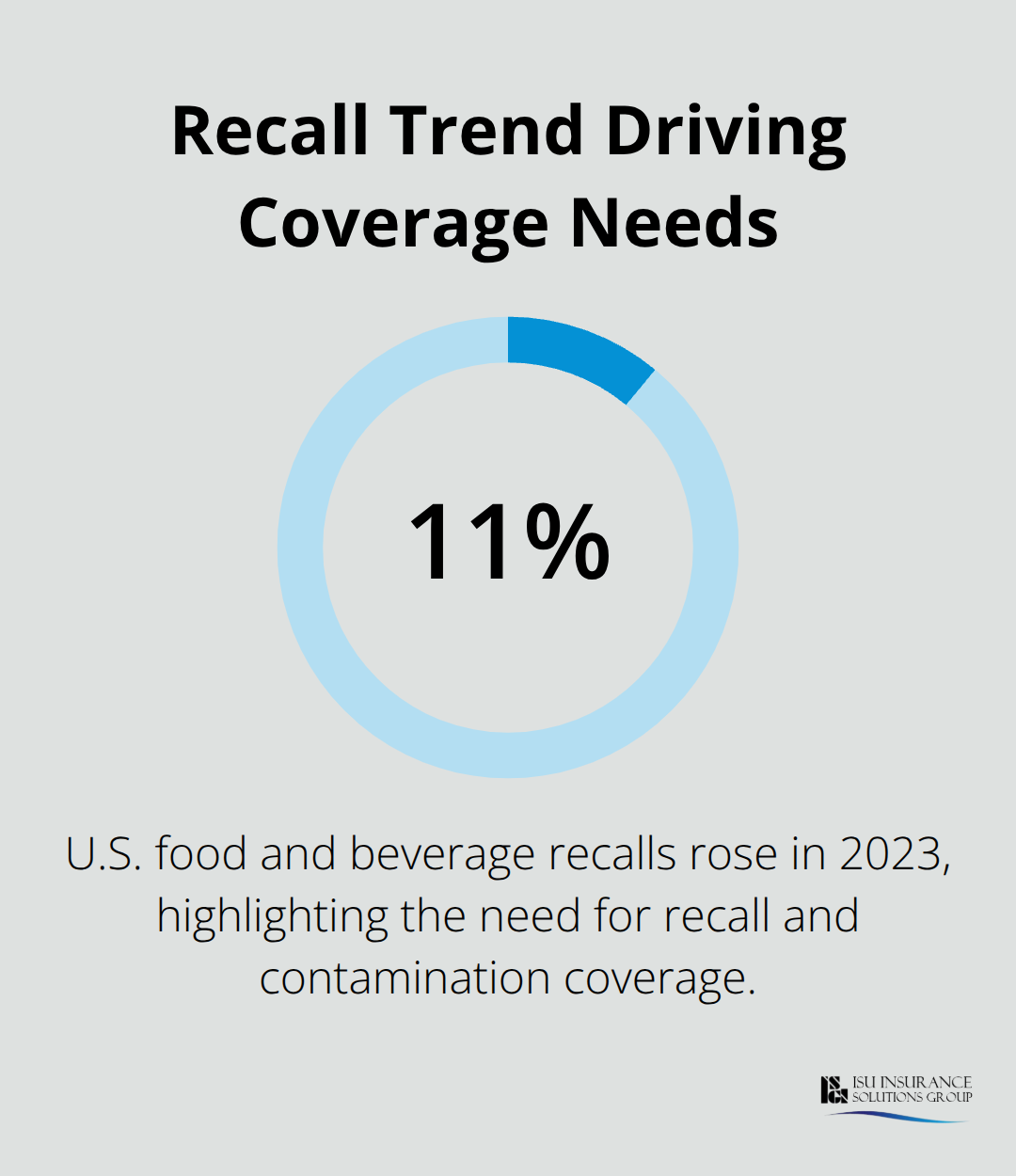

Federal bonds and state licensing requirements keep your brewery legal, but insurance protects your business from the financial devastation that bonds don’t cover. A U.S. food and beverage recall rose 11 percent in 2023 according to PR Newswire, and a single product recall can cost a microbrewery between $50,000 and $500,000 depending on distribution scope and contamination severity. Property coverage protects your fermentation tanks, brewing equipment, and facility against fire, weather damage, and theft-but standard commercial policies often exclude brewery-specific risks like yeast contamination, leakage from fermentation vessels, and the extra costs of keeping fermentation systems running after equipment failure.

You need coverage that includes specialized equipment endorsements, spoilage protection, and business income loss if your production shuts down for weeks.

Liability Coverage for Tours, Tastings, and Distribution

General liability and liquor liability work together to cover bodily injury or property damage claims from brewery tours, tastings, and off-site consumption at bars and restaurants. A single slip-and-fall during a tour or an alcohol-related incident at an event can trigger lawsuits exceeding $100,000 in legal defense alone. Workers compensation is mandatory in every state and covers medical care and wage replacement when your brewing staff gets injured-but brewery environments carry elevated slip-and-fall risks from wet floors, equipment operation, and heavy lifting.

Product Recall and Manufacturing Risk Protection

Product liability coverage specifically covers the costs of removing contaminated or mislabeled beer from shelves, notifying distributors and retailers, and replacing inventory. Without this coverage, a recall eats directly into your cash reserves and can force operational cutbacks. Manufacturers errors and omissions insurance fills gaps that general and product liability policies miss, protecting against manufacturing defects, formula changes, or labeling errors that cause customer harm. As your brewery scales production and distribution, umbrella or excess liability coverage becomes essential-it extends protection above your primary policy limits when a major incident occurs.

Calculating Your Coverage Investment

Microbreweries typically spend $500 to $1,500 monthly on comprehensive coverage depending on facility size, production volume, and distribution range. A risk assessment identifies your specific exposure: what equipment could fail, where customers visit your facility, how far your products travel, and what contamination scenarios keep you awake at night. That assessment drives your coverage choices far better than a generic package, and it positions your brewery to scale without coverage gaps that emerge only after growth happens. Understanding your actual risk profile also matters when you move toward expansion-growth introduces new liability exposures and property values that your current policies may not address.

Protecting Your Brewery Before Growth Happens

Expansion exposes gaps you didn’t know existed. A brewery operating at 5,000 barrels annually faces different property, liability, and supply chain risks than one scaling to 15,000 barrels. The insurance that protects your current operation often falls short when you add production lines, hire more staff, expand distribution territory, or open a taproom. A formal risk assessment before any major growth move identifies specific exposures that your existing policies don’t address.

Equipment and Facility Risk

Your fermentation tanks, chillers, grain mills, and packaging equipment represent your largest asset base, yet standard commercial property policies exclude brewery-specific losses. Equipment failure during fermentation destroys batch inventory, forces production shutdowns, and creates extra costs to restart fermentation systems. As you scale, your equipment value climbs, and your dependency on continuous operation intensifies. A risk assessment quantifies your actual replacement costs for specialized brewing equipment and determines whether your current property coverage includes spoilage protection, equipment breakdown endorsements, and business income coverage for lost production days. Many breweries discover their policies cap spoilage losses at $10,000 when a single contaminated batch costs $50,000 to replace. Growth amplifies this gap. If you expand production capacity, your insurer needs updated equipment schedules and facility diagrams before claims happen. Waiting until after a loss to discover coverage shortfalls proves expensive.

Liability Exposure and Distribution Changes

Adding a taproom, expanding to new states, or hiring delivery drivers introduces liability scenarios your current general and liquor liability policies may not fully address. A delivery vehicle accident in a new state can trigger workers compensation and auto liability claims outside your current coverage territory. Hiring seasonal staff during peak production means more people work around fermentation vessels, pressurized tanks, and heavy equipment-environments with genuine slip-and-fall and equipment-related injury risk. Your workers compensation coverage must reflect your actual payroll and the physical demands of brewery work. Umbrella liability becomes essential once your distribution reaches multiple states or once your taproom draws significant foot traffic. A single serious injury claim can exceed your primary liability limits quickly. Growth also increases product liability exposure. Distributing to 20 bars across two states multiplies the scenarios where contamination, labeling errors, or allergenic ingredients trigger recalls or injuries. Product recall coverage becomes non-negotiable at this scale. Breweries face genuine contamination risks, and product recall coverage protects against the financial impact of recalls and injuries.

Supply Chain Vulnerabilities and Coverage Gaps

Scaling production depends on reliable suppliers-grain sources, yeast cultures, packaging materials, and equipment maintenance. A disruption in any of these areas can halt production for weeks. Inland marine coverage protects your beer and ingredients while in transit from suppliers or to distributors, covering loss from theft, weather, or vehicle damage. Ocean marine coverage applies if you ship products across water. These aren’t standard coverages; they require specific endorsements tailored to your supply chain routes and product values. Your risk assessment should identify your critical suppliers and the financial impact if they become unavailable. If a single grain supplier provides 70 percent of your malt, what happens to production if that supplier’s facility burns down? That scenario is rare but catastrophic.

Contingency planning and appropriate coverage matter more as your operation becomes more complex. Your assessment also reveals whether cyber insurance makes sense. As breweries adopt digital systems for inventory management, recipe tracking, and distribution logistics, data breaches and malware attacks become real operational threats. A ransomware attack on your production scheduling system can force manual operations and production delays.

Final Thoughts

Brewery bonds and insurance form the backbone of a sustainable operation. Federal bonds keep you compliant with the TTB, state bonds satisfy licensing requirements, and comprehensive insurance protects the assets and revenue that bonds don’t cover. Most breweries treat these as separate concerns rather than interconnected safeguards that work together to support growth.

Your current coverage likely has gaps you haven’t discovered yet. A formal risk assessment identifies what your policies actually protect and where exposure exists. That assessment should examine your equipment replacement costs, your liability scenarios across all customer touchpoints, your supply chain dependencies, and the financial impact of production shutdowns or recalls. Growth amplifies every gap, and your insurance must evolve with your operation.

We at ISU Insurance Solutions Group work with breweries across Washington and Oregon to build coverage that matches their operations. Our agents understand brewery-specific risks, from fermentation equipment to distribution logistics, and we quote across multiple carriers to find competitive rates without coverage gaps. If you’re uncertain whether your current policies protect your growth plans, contact our team to discuss your brewery’s coverage needs.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.