Distillery Property Coverage: Guarding Distilling Equipment and Inventory

Distilleries face unique risks that standard business insurance simply doesn’t cover. Your equipment, inventory, and buildings need protection specifically designed for spirits production.

We at ISU Insurance Solutions Group help distillery owners understand what distillery property coverage actually protects and how to choose the right limits for your operation.

What Your Distillery Property Coverage Actually Protects

Equipment and Machinery Coverage

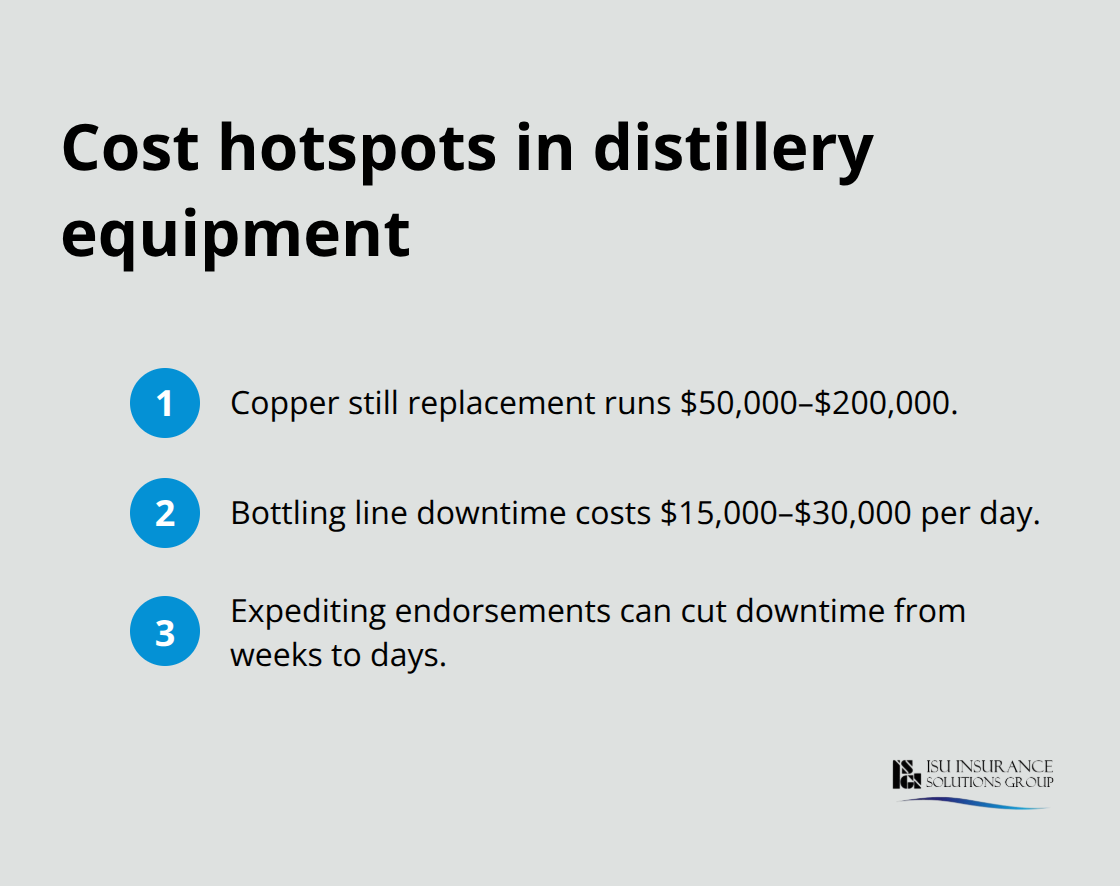

Distillery property coverage protects three critical areas of your operation, and understanding exactly what falls under each category prevents costly gaps when something goes wrong. Equipment and machinery coverage reimburses you for production assets like copper stills, fermentation tanks, bottling lines, and control systems when fire, explosion, equipment breakdown, or other covered perils damage them. A single copper still costs $50,000 to $200,000 to replace, and a bottling line failure costs $15,000 to $30,000 per day in lost production. Most distilleries underestimate equipment value or overlook specialized gear like temperature-control systems, so you should inventory your equipment carefully and include expediting expense endorsements that cover rush repairs. These endorsements can reduce downtime from weeks to days by paying for overnight parts shipment or emergency technicians.

Inventory and Product Protection

Inventory and product protection covers your raw materials, work-in-progress spirits, and finished goods stored in barrels or bottles. Aging spirits require valuation as stock-in-process, not raw materials, because a five-year-old bourbon barrel represents years of production cost plus significant aging value. Washington construction costs rose roughly 19 percent between 2021 and 2023, so inflation guard endorsements protect against replacement-cost inflation that erodes your coverage over time. You should confirm your total asset values match your coverage ceiling before a loss occurs, since property coverage limits typically cap combined building and inventory at around $5 million with most carriers.

Building and Structure Coverage

Building and structure coverage protects your production facility, barrel warehouses, tasting room, and related structures against fire, weather damage, and other perils. Fire and explosion hazards dominate distillery losses because ethanol vapor ignites at concentrations that pose significant fire hazards-even a small spark in an inadequately ventilated barrel room can trigger catastrophic damage. Sprinkler systems significantly improve your insurability and lower property rates; unsprinkled buildings face substantially higher premiums and deductibles. An experienced distillery agent will schedule all equipment and inventory properly, since generic property policies often exclude production equipment or age-restricted goods that require specific endorsements. This foundation of proper coverage sets the stage for evaluating the specific risks your distillery faces and determining whether your current limits adequately protect your assets.

Common Risks Facing Distilleries

Fire and Explosion Hazards

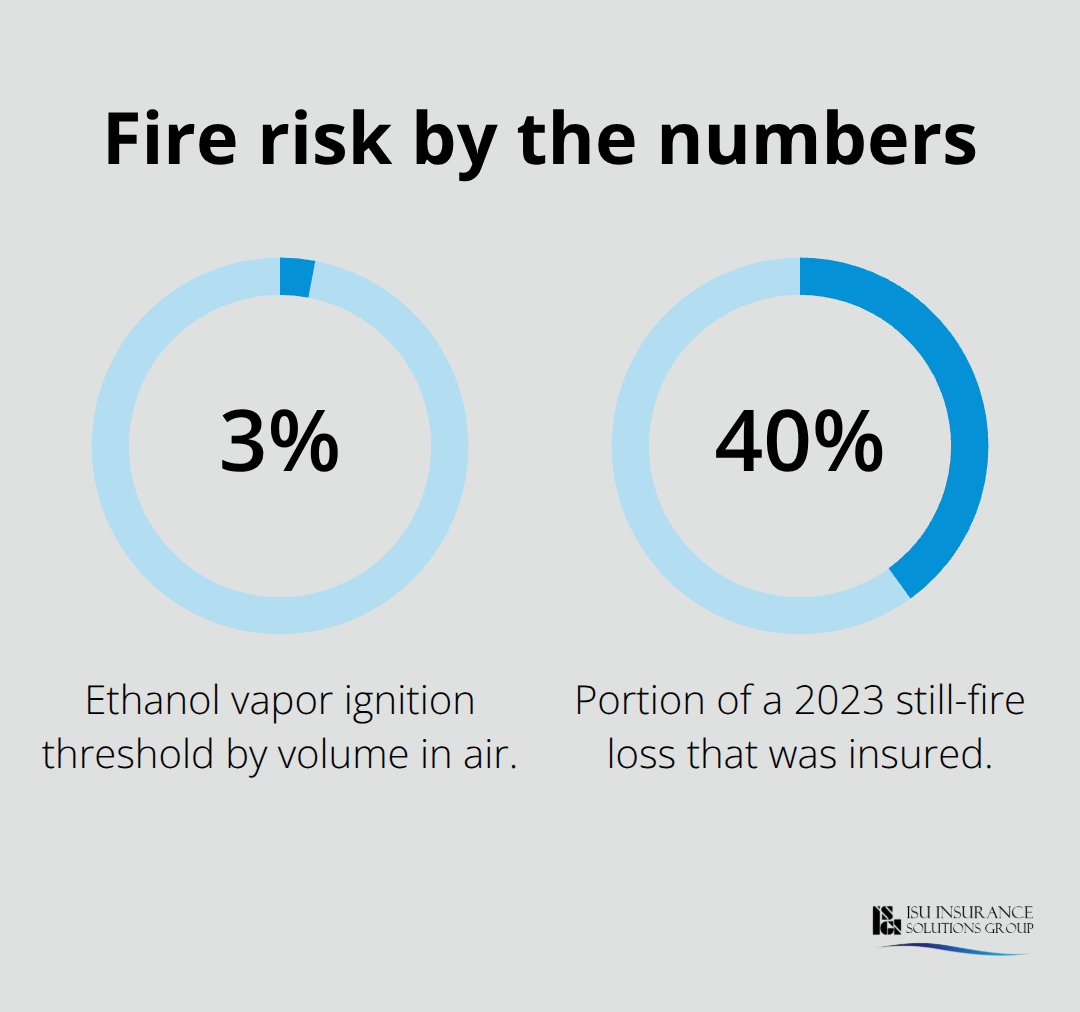

Fire and explosion remain the dominant threats to distillery operations, and the numbers prove why this risk demands serious attention. Ethanol vapor ignites at just 3 percent by volume in air, meaning even a small spark in an inadequately ventilated barrel room or still area can trigger catastrophic damage. A Kentucky facility suffered approximately $2.4 million in property damage from a still-fire event in 2023, yet only 40 percent of that loss was insured, leaving the owner with a $1.44 million gap. Washington distilleries face extended rebuild timelines averaging around 11 months after major fires, which means your business interruption coverage must reflect months of lost revenue, not weeks.

The American Craft Spirits Association reports that Washington’s independent distilleries generated over $650 million in direct sales last year while supporting roughly 4,700 jobs, so a single fire can devastate not just your operation but your employees’ livelihoods. Proper ventilation, explosion-proof design in still rooms, and sprinkler systems following NFPA 30 and NFPA 13 guidelines significantly reduce both the likelihood of fire and the severity of damage. Many distilleries install foam extinguishers specifically because they excel at suppressing Class A and Class B fires common in spirits production. Pairing detection systems (ionization detectors for fast-flaming fires and photoelectric detectors for smoldering fires) with automatic alarms catches problems early.

Theft and Break-Ins

Theft and break-ins pose a different but equally serious threat, particularly for distilleries holding high-value aged inventory and finished products. A barrel of premium whiskey worth $3,000 to $10,000 or more becomes an attractive target, especially in rural warehouse settings where monitoring is challenging. Installing security cameras with cloud backup, motion-activated lighting, and alarm systems connected directly to local law enforcement creates genuine deterrence rather than relying on hope.

Water Damage and Environmental Exposure

Water damage from burst pipes, roof leaks, or flooding destroys inventory rapidly and can contaminate entire batches stored in warehouses. Washington’s flooding patterns and seasonal rainfall mean property coverage must explicitly address weather-related water intrusion, and in flood-prone areas, separate flood insurance is non-negotiable since standard policies exclude flood damage. Environmental exposure includes temperature fluctuations that spoil aging spirits, power outages that disable climate controls, and chemical spills that contaminate product or soil.

Equipment breakdown coverage with spoilage protection reimburses product loss when refrigeration or climate systems fail, a scenario that costs thousands per day for large aging warehouses. Your property policy should cover contamination cleanup, disposal costs, and regulatory fines from environmental agencies if hazardous materials escape containment. Understanding these specific threats allows you to evaluate whether your current coverage limits actually match the real exposures your distillery faces.

How to Select the Right Distillery Property Coverage

Document Your Equipment and Inventory with Precision

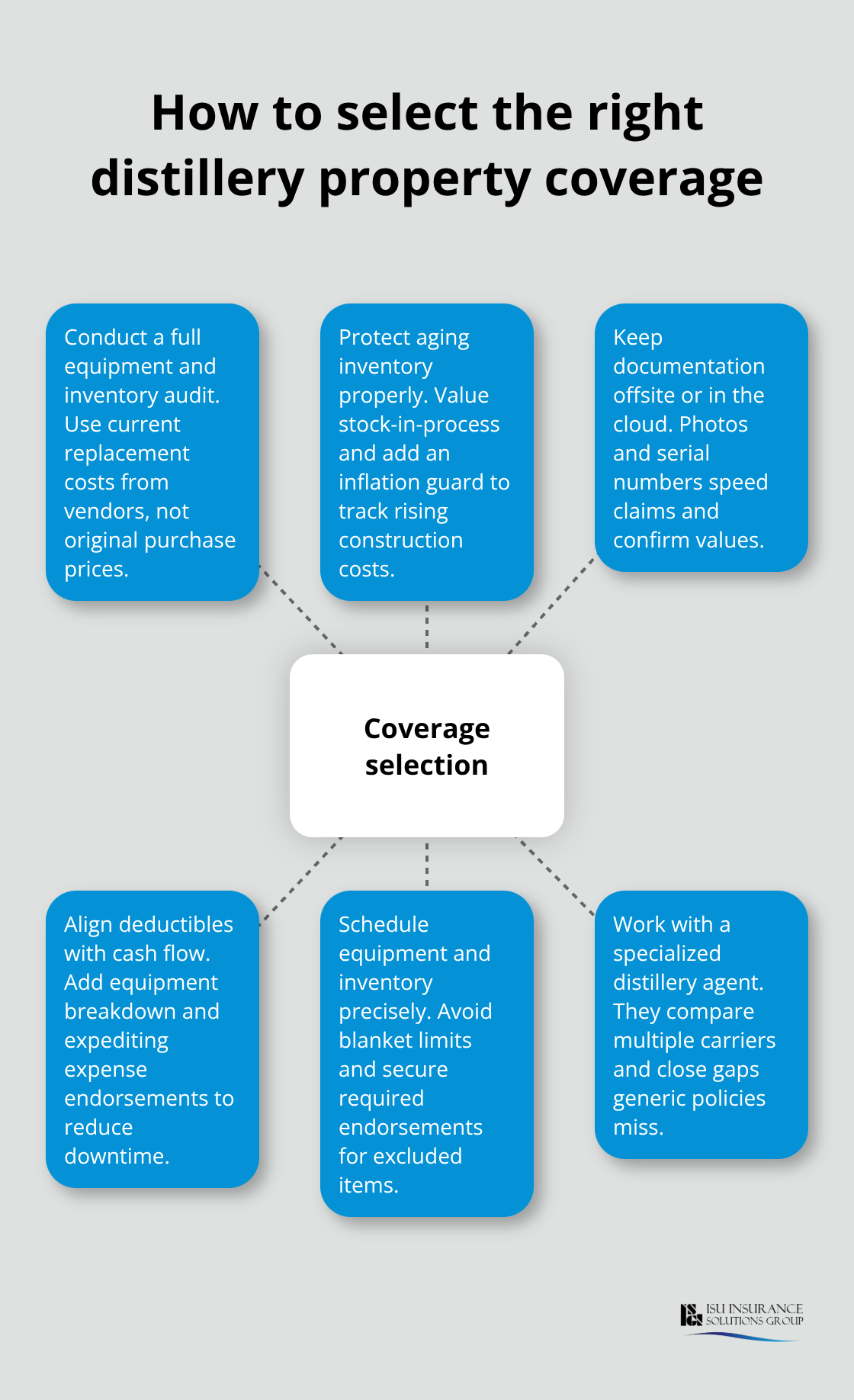

Start with a complete equipment and inventory audit, not a rough estimate. Walk through your distillery with a spreadsheet and record every production asset: copper stills, fermentation tanks, bottling equipment, control systems, pumps, hoses, and temperature monitors. Obtain replacement costs from vendors or recent quotes, not decade-old purchase prices. A single copper still costs $50,000 to $200,000 to replace, and bottling line failures cost $15,000 to $30,000 daily in lost production, so undervaluing equipment directly reduces your claim recovery.

For aging inventory, value spirits as stock-in-process rather than raw materials because a five-year-old bourbon barrel represents years of production costs plus significant aging value. Add an inflation guard endorsement to your property policy to protect against replacement-cost inflation that erodes coverage over time. Most carriers cap combined building and inventory coverage at around $5 million, so verify your total asset values fit within your coverage ceiling before a loss occurs.

Store Documentation Safely and Accessibly

Document your inventory with photos and serial numbers stored separately from your facility-cloud backup works best-since you’ll need proof during claims settlement. This separation protects your records if fire or water damage destroys your physical location. Organized documentation speeds the claims process and ensures you recover the full value of your assets.

Align Coverage Limits with Your Cash Flow

Evaluate your coverage limits and deductibles against your actual cash flow and risk tolerance. A $2,500 deductible sounds reasonable until you face three weather-related losses in a year and realize you’re paying $7,500 out of pocket across multiple claims. Most distilleries should carry deductibles between $1,000 and $2,500 depending on cash reserves, then add equipment breakdown coverage with expediting expense endorsements that cover rush repairs and overnight parts shipment. These endorsements reduce downtime from weeks to days and often cost less than a single day of lost production revenue.

Schedule Equipment and Inventory Properly

For property coverage, demand that your agent schedules all equipment and inventory properly rather than using blanket limits, because generic policies often exclude production equipment or age-restricted goods requiring specific endorsements. A specialized distillery agent understands that sprinkler systems significantly reduce property rates and that unsprinkled wooden warehouses face substantially higher premiums and deductibles-sometimes 25 to 40 percent more depending on your carrier.

Partner with an Agent Who Understands Distillery Operations

When comparing quotes, ignore the lowest price and instead compare what each carrier actually covers, what exclusions apply, and whether the agent truly understands still types, fermentation equipment, and barrel aging logistics. An independent agent with distillery experience can access multiple carriers and identify coverage gaps that generic business policies miss. This expertise protects your operation far more effectively than chasing the cheapest premium.

Final Thoughts

Distillery property coverage protects your entire operation from the specific threats that can shut you down for months-fire and explosion hazards, theft, water damage, and environmental exposure all demand coverage designed specifically for spirits production. Your copper stills, fermentation tanks, aging barrels, and bottling lines represent years of investment and production capacity, and a single fire can cost $2.4 million or more with Washington’s 11-month average rebuild timeline meaning your business interruption coverage must reflect months of lost revenue. Sprinkler systems, proper ventilation, and equipment breakdown endorsements with expediting expenses reduce both the likelihood of catastrophic loss and the financial damage when something goes wrong.

The most important step is partnering with an agent who understands distillery operations rather than treating your business like a generic manufacturing facility. An experienced distillery agent knows that unsprinkled wooden warehouses face substantially higher premiums, that aging spirits require valuation as stock-in-process, and that inflation guard endorsements protect your coverage as construction costs rise. They access multiple carriers and identify coverage gaps that would otherwise leave you exposed.

Contact ISU Insurance Solutions Group for a personalized distillery property coverage review that reflects your actual equipment, inventory, and business interruption needs.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.