Commercial Auto Insurance: A Smart Move for Your Fleet

Fleet owners face a constant challenge: protecting their vehicles and drivers while managing costs. Commercial auto insurance isn’t optional-it’s a legal requirement that shields your business from financial disaster.

We at ISU Insurance Solutions Group know that the right coverage strategy makes all the difference. This guide walks you through what you need to know to protect your fleet properly.

Understanding Your Fleet’s Coverage Options

Liability coverage forms the foundation of every commercial fleet policy, and the numbers prove why this matters. Most states require minimum liability limits for commercial auto insurance, but those minimums fall dangerously short for business operations. A single accident involving bodily injury to multiple people or property damage to expensive equipment can easily exceed state minimum requirements by hundreds of thousands of dollars. Liability coverage splits into two components: bodily injury liability pays medical expenses and lost wages for injured parties, while property damage liability covers damage to other people’s vehicles, buildings, or infrastructure. Fleet operators who visit job sites or transport goods face rapid accumulation of property damage claims. Many fleet operators carry only baseline coverage when they should pursue higher limits instead. Over 1 million small businesses trust commercial auto programs that emphasize higher liability limits, particularly contractors and service businesses that face third-party exposure when working on customer properties or near their assets.

Collision and Comprehensive Protection for Physical Damage

Physical damage coverage protects your actual vehicles when accidents occur. Collision coverage pays for repairs or replacement after crashes, rollovers, or impact incidents, regardless of fault. Comprehensive coverage handles everything else: theft, vandalism, weather damage, fires, and wildlife strikes. Collision and comprehensive coverage protect your actual fleet assets, and these matter differently depending on your vehicle values and usage patterns. Fleet operations require comprehensive coverage as a practical necessity, not a luxury. A single theft or weather event affecting multiple vehicles can cripple your business operations. Rental reimbursement endorsements keep your fleet operational while damaged vehicles sit in the shop. Gap coverage protects you if a financed vehicle is totaled and the loan balance exceeds the vehicle’s actual value. These endorsements prevent cash flow disasters that threaten your ability to serve customers and maintain operations.

Uninsured and Underinsured Motorist Coverage Fills Critical Gaps

This coverage protects your drivers and business when accidents involve uninsured or underinsured drivers. Roughly 13% of drivers nationwide carry no insurance, and many others carry limits far below what they actually owe after causing serious accidents. Your fleet absorbs the financial impact without this protection.

Uninsured motorist coverage pays for medical expenses and lost wages for your drivers, while underinsured motorist coverage activates when the at-fault driver’s policy limits fall short of actual damages. Fleet operators face repeated traffic exposure, making this protection essential. The cost to add these coverages remains minimal compared to the protection they provide, yet many business owners skip them. Liability coverage covers damage your fleet causes to others, not damage others cause to your fleet-a critical distinction that many fleet owners misunderstand.

Understanding these three coverage pillars positions your fleet to handle the real-world risks you face daily. The next step involves examining why commercial auto insurance matters beyond just coverage types, and how legal requirements and financial protection work together to safeguard your entire operation.

Why Your Fleet Needs Commercial Auto Insurance

Every state mandates commercial auto insurance for fleet operations, but legal compliance represents only the baseline. Fleet owners who treat commercial auto insurance as merely a checkbox miss the financial reality: one serious accident can bankrupt a business without proper coverage. State laws generally require commercial auto insurance requirements with statutory minimums such as $25,000 or $50,000 for basic vehicle registration. Your actual exposure far exceeds these minimums. A contractor’s van striking a utility pole or commercial building creates liability claims reaching hundreds of thousands of dollars. Without adequate coverage, you personally absorb costs that dwarf your annual insurance premiums. Interstate operations add complexity-federal regulations impose higher liability standards for vehicles crossing state lines, particularly when transporting goods or people. The financial exposure alone justifies carrying limits substantially above state minimums, yet many fleet operators skip this critical step.

Accidents Expose Your Business to Devastating Financial Loss

Financial protection extends beyond liability claims to the physical assets you depend on daily. A single vehicle loss disrupts your entire operation-jobs delay, customers lose confidence, and revenue stops flowing while you scramble to replace equipment or arrange temporary transportation. Collision and comprehensive coverage eliminate this operational vulnerability. Rental reimbursement endorsements keep you operational during repairs, preventing the costly downtime that compounds damage beyond repair costs. Gap coverage protects financed vehicles when total loss occurs, preventing loan deficits that drain cash reserves. Fleet operators managing five or more vehicles face compounding risks; a weather event damages multiple vehicles simultaneously and cripples operations for weeks without proper comprehensive coverage and rental support. The cost difference between basic coverage and comprehensive protection remains negligible when compared to business interruption losses.

Multiple Vehicles Require Coordinated Coverage Structures

Managing drivers across multiple vehicles demands coverage structures that personal auto policies explicitly exclude. Commercial auto policies cover owned vehicles, leased vehicles, hired vehicles, borrowed vehicles, and non-owned vehicles-the full spectrum of fleet operations. Employee-driven personal vehicles used for business purposes need coverage clarification; many businesses face unexpected claim denials because personal policies excluded business use. A single employee using a personal vehicle for business deliveries without proper commercial coverage creates liability exposure that falls on your business. Commercial fleet policies consolidate this complexity under one policy structure with consistent coverage across all vehicles and drivers. Five or more vehicles typically qualify for fleet policies, which simplify administration and often reduce per-vehicle costs compared to individual policies.

Coverage Gaps Between Vehicles Create Hidden Exposure

Uninsured motorist coverage protects your drivers and business when accidents involve uninsured or underinsured drivers. Roughly 13% of drivers nationwide carry no insurance, and many others carry limits far below what they actually owe after causing serious accidents. Your fleet absorbs the financial impact without this protection. Uninsured motorist coverage pays for medical expenses and lost wages for your drivers, while underinsured motorist coverage activates when the at-fault driver’s policy limits fall short of actual damages. Fleet operators face repeated traffic exposure, making this protection essential. The cost to add these coverages remains minimal compared to the protection they provide, yet many business owners skip them. Liability coverage covers damage your fleet causes to others, not damage others cause to your fleet-a critical distinction that many fleet owners misunderstand.

Understanding these financial realities positions your fleet to move beyond basic compliance and toward genuine protection. The next step involves examining specific cost-saving strategies that allow you to maintain comprehensive coverage without straining your budget.

How to Cut Fleet Insurance Costs Without Cutting Coverage

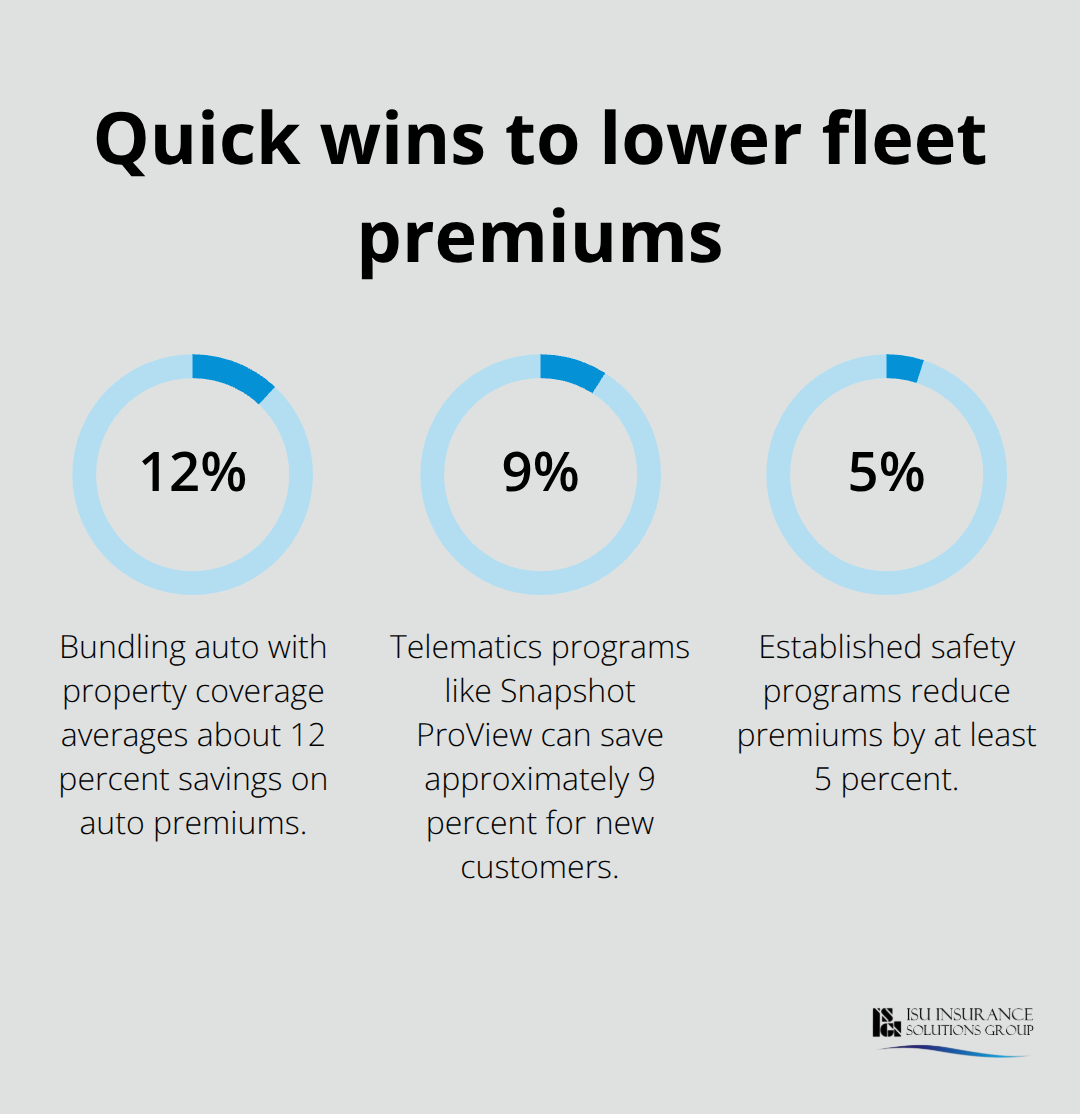

Driver behavior directly determines your insurance costs, and this is where most fleet operators leave money on the table. Progressive reports that established safety programs reduce premiums by at least 5 percent, yet many small fleet owners operate without formal driver training or safety protocols. Safety programs document defensive driving practices, accident prevention, and vehicle maintenance routines that insurers reward with meaningful discounts. Telematics programs like Snapshot ProView can save new customers approximately 9 percent on premiums by tracking actual driving patterns rather than relying on historical data alone. If your fleet operates with minimal accidents and traffic violations, this data proves your drivers deserve lower rates.

Driver training programs that focus on real-world hazards specific to your business-tight parking lots, delivery routes, or job site navigation-cost far less than the premium reductions they generate. Document these safety investments when shopping for quotes, as some carriers weight safety initiatives more heavily than others.

Bundling Coverage Types Delivers Immediate Savings

Combining commercial auto coverage with property insurance delivers substantial savings that most fleet operators never pursue. Progressive reports that bundling auto with property coverage generates approximately 12 percent average savings on auto premiums alone. A business owner’s policy covering your office, equipment, and liability paired with fleet auto insurance creates a complete risk picture that carriers reward with multi-product discounts.

This strategy works particularly well for contractors, service businesses, and small manufacturers who already carry general liability and property coverage. The bundle discount often exceeds the cost of adding coverage you were missing, turning protection gaps into savings opportunities. Paying your premium in full upfront rather than monthly installments generates additional discounts with most carriers. Some insurers reduce rates further for customers maintaining continuous coverage without gaps, incentivizing loyalty and stability.

These stacked discounts compound quickly-a 12 percent bundle discount plus a 5 percent continuous coverage discount plus a 9 percent safety program discount creates meaningful annual savings that justify investing time in proper policy structure.

Shopping Annually Exposes Hidden Pricing Differences

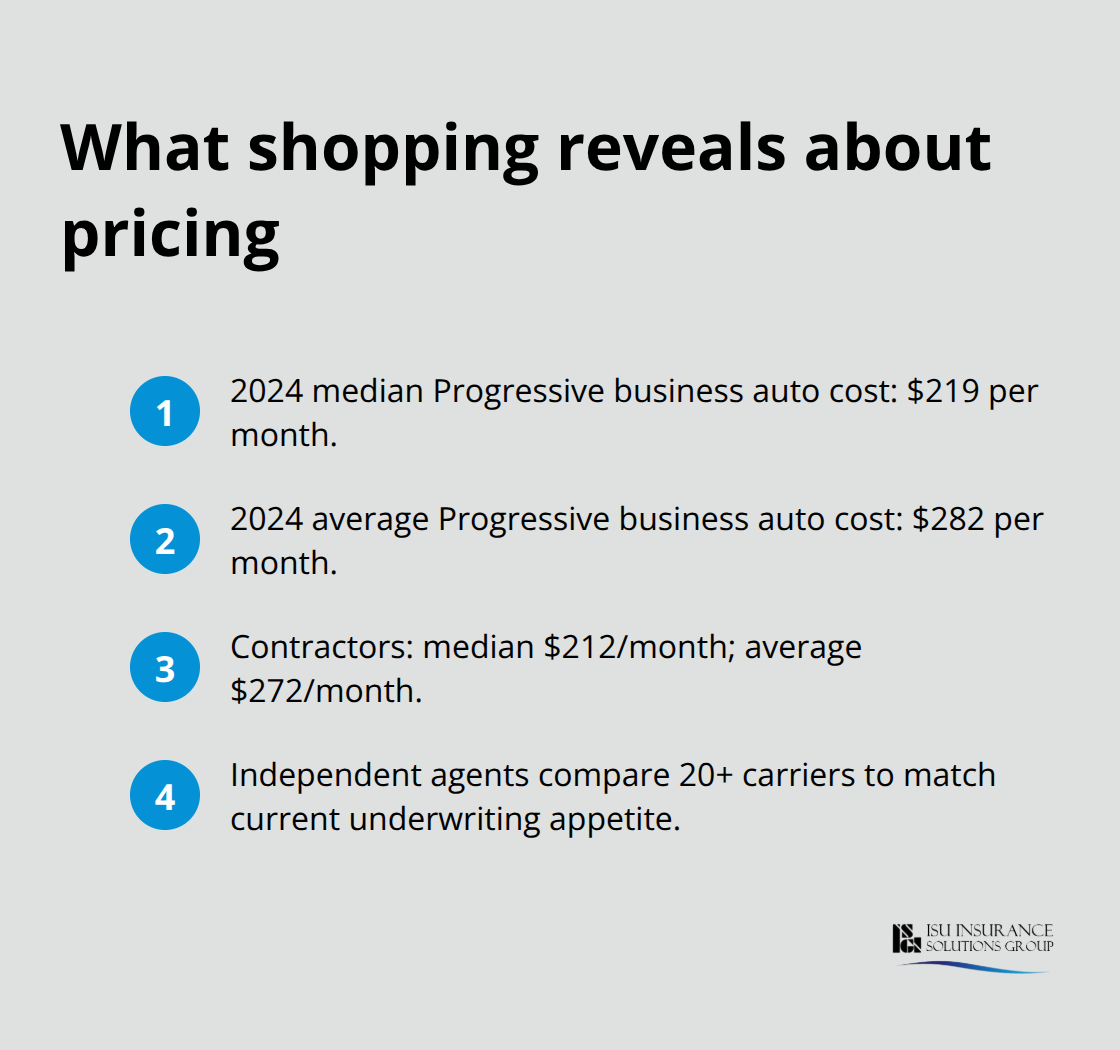

Carrier pricing for identical coverage varies dramatically, and this variation shifts annually based on each insurer’s claims experience and underwriting priorities. The 2024 median cost for business auto coverage through Progressive was approximately 219 dollars monthly, while the average reached 282 dollars-a significant spread that reflects how individual business factors affect pricing. Contractors faced median costs around 212 dollars monthly versus averages of 272 dollars, indicating that some carriers price contractor exposure more aggressively than others.

These variations mean your current premium may represent terrible value compared to competing quotes. Independent insurance agents can access multiple carriers simultaneously and identify which insurers currently favor your business profile. This matters because carrier appetite shifts quarterly as their claims data changes. An insurer offering aggressive pricing this year may pull back next year, while a previously expensive option becomes competitive.

Annual shopping prevents you from paying premium rates during years when your carrier has reduced appetite for your business type. As an independent agency serving Washington and Oregon since 1983, ISU Insurance Solutions Group provides access to 20 plus carriers through one call, eliminating the tedious process of contacting multiple insurers individually.

Conclusion

Commercial auto insurance protects your fleet from financial devastation, legal liability, and operational disruption that accidents create. Liability coverage, collision protection, comprehensive coverage, and uninsured motorist protection work together to address the real risks your business faces daily. State minimums provide baseline compliance, but they leave your business dangerously exposed to losses that exceed your annual insurance premiums many times over.

Cost-saving strategies prove that comprehensive protection does not require excessive spending. Safety programs reduce premiums by at least 5 percent, bundled coverage generates approximately 12 percent average savings on auto premiums, and annual shopping prevents you from overpaying when your current carrier reduces appetite for your business profile. Driver training and telematics programs lower costs while improving safety outcomes simultaneously.

We at ISU Insurance Solutions Group have served Washington and Oregon businesses since 1983, providing access to 20 plus carriers through one conversation. Contact us for a multi-carrier quote that reveals your actual options and structures coverage that protects your fleet while controlling costs.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.