Architect Professional Liability Insurance: From Design to Defense

One mistake in your building plans can cost thousands in repairs and legal fees. Architect professional liability insurance protects your firm when design errors, missed site details, or project delays lead to client claims.

We at ISU Insurance Solutions Group know that most architects operate without understanding their actual exposure. The right coverage isn’t optional-it’s the difference between staying in business and facing financial ruin.

What Your Professional Liability Policy Actually Covers

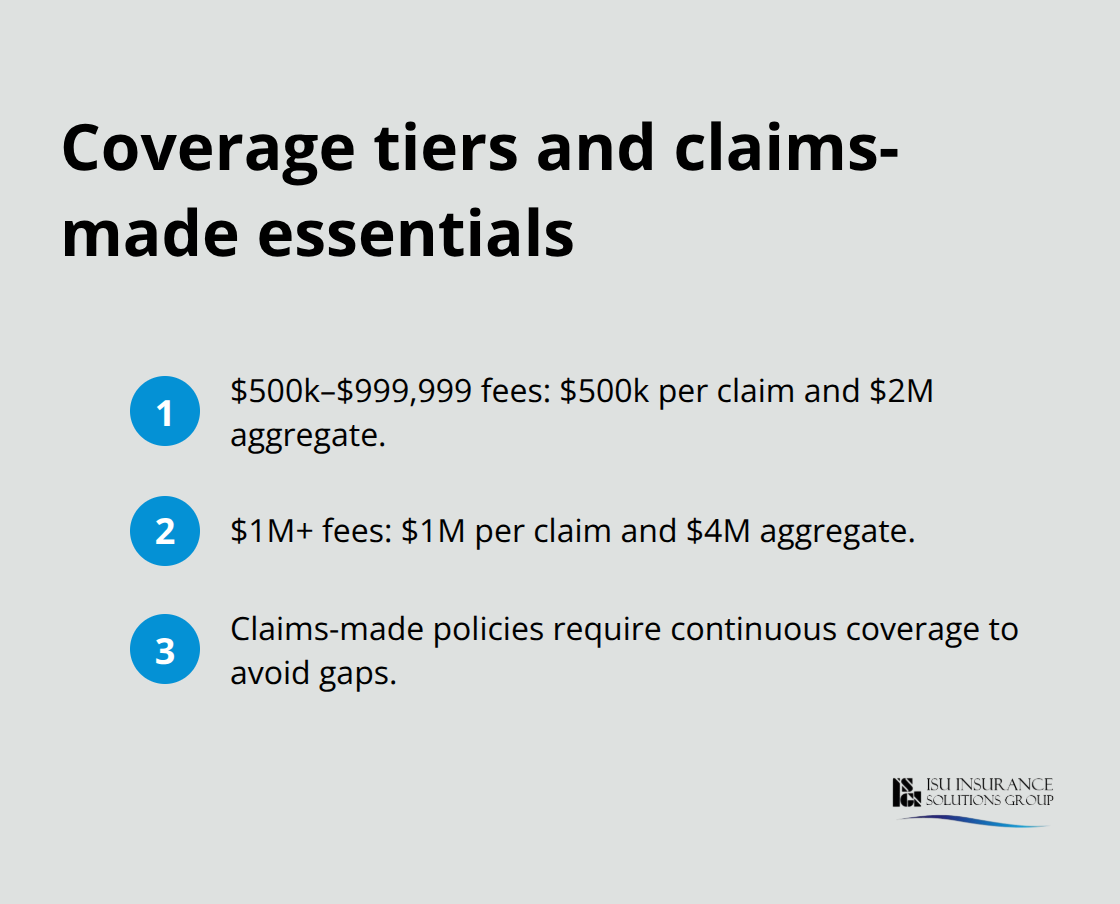

Architect professional liability insurance protects your firm when design errors, omissions, or negligent advice result in client claims. The coverage pays for legal defense costs, settlements, and judgments-typically in addition to damages under most policy structures. If a client alleges that your blueprints contained calculation errors, that you failed to verify building code compliance, or that inadequate site supervision led to construction defects, this insurance activates to defend your firm and cover the financial fallout. The policy applies to professional services spanning from initial design conception through construction administration, meaning claims can arise years after project completion. Typical annual premiums range from $300 to $4,000 depending on your firm’s size, claims history, years in business, and location. Firms with $500,000 to $999,999 in annual gross fees generally face claim limits of $500,000 per claim and $2,000,000 aggregate, while larger practices with $1,000,000+ in fees carry $1,000,000 per claim and $4,000,000 aggregate limits. The policy operates on a claims-made basis, meaning the claim must be reported during your active policy period-gaps in coverage can severely restrict your ability to defend against future allegations tied to past work.

Design Errors Stop Claims Before They Start

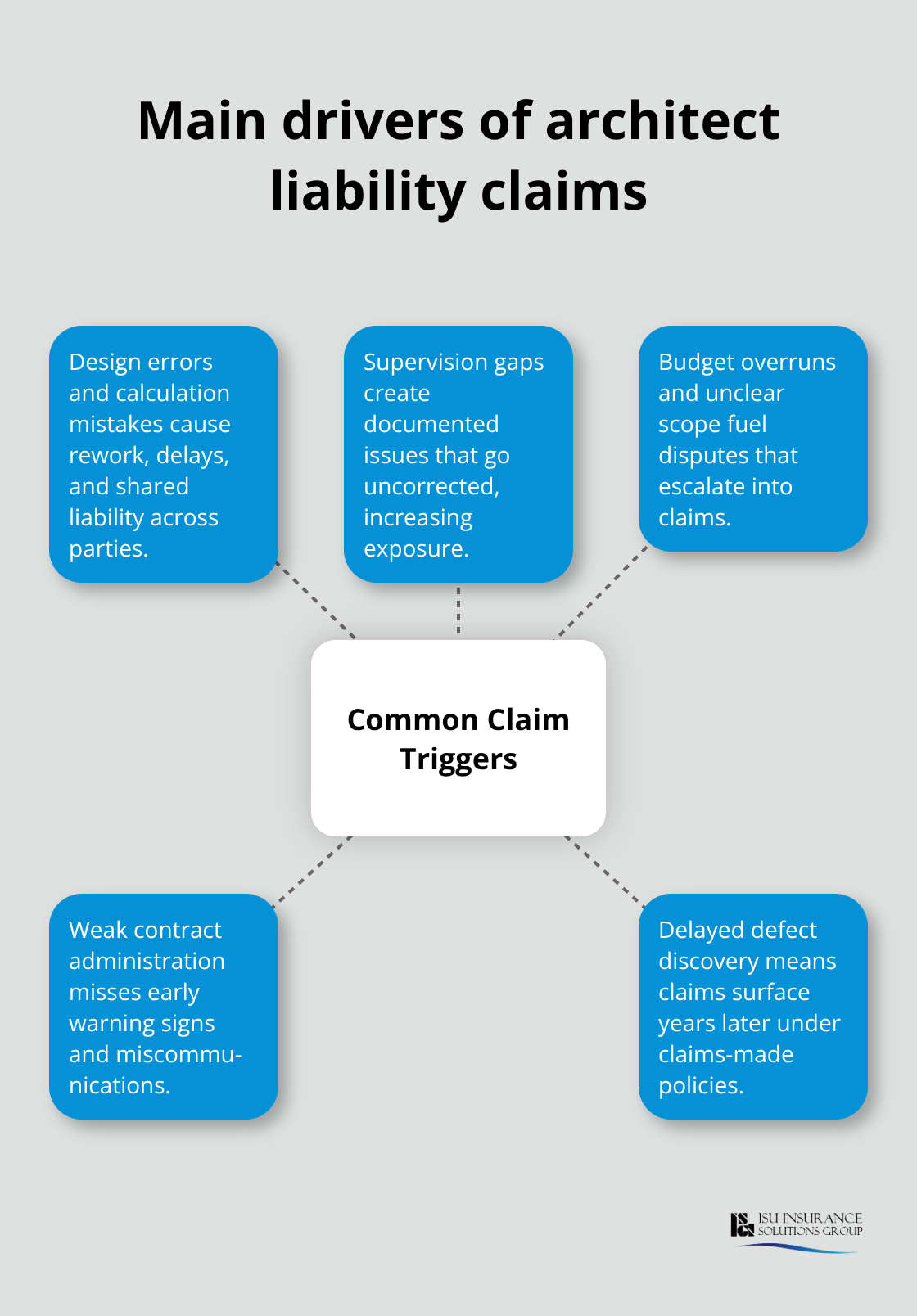

Most architect claims stem directly from design errors and calculation mistakes. A roof design error that miscalculates water runoff creates interior leakage and structural damage; a column spacing change that bypasses established engineering standards forces costly rebuilds; dimension conversion errors render components unusable and trigger multi-faceted losses (including site rework and shared liability exposure). The best defense involves preventing these errors through rigorous cross-checking procedures, especially on high-stakes structural elements, and validating designs against credible standards like Post-Tension Institute guidelines. Your professional liability policy covers the defense costs and damages when these errors slip through, but prevention reduces claims frequency and keeps your premiums lower over time.

Supervision Gaps Create Liability Exposure

Inadequate on-site supervision exposes architects to significant liability because you have a duty to monitor contractor adherence to plans and safety requirements. If your daily site logs document problems-water intrusion, material substitutions, code violations-but your team fails to report these issues to the contractor or owner, you’ve created a liability trail that insurers scrutinize closely. Architects who conduct minimal site visits or rely on passive observation without documented corrective action face higher claim risk. Your professional liability coverage protects you when supervision disputes arise, but clear contractual language limiting your duties to defined scope and explicit documentation of site communications strengthen your defense position substantially.

Why Claims Arise Years Later

Claims can surface long after project completion because construction defects often remain hidden until occupancy or seasonal weather stress reveals them. A design flaw in waterproofing details may not manifest until the second winter of building operation; structural miscalculations might only become apparent when the structure bears full load. This delayed discovery means your firm needs continuous coverage (not gaps) to defend against allegations tied to work completed years earlier. The claims-made structure of professional liability policies makes this timing critical-you must maintain active coverage when the claim is reported, not when the work occurred.

Coverage Limits Match Your Firm’s Scale

Your policy limits should reflect both your firm’s revenue and the complexity of projects you undertake. Smaller practices handling residential or light commercial work typically operate with lower limits, while firms managing large institutional or mixed-use projects require higher protection. The standard tiering system ties limits directly to annual gross fees, which means your coverage grows as your practice expands. Understanding these limits (claim limit, project limit, and aggregate limit) helps you plan for risk exposure and identify whether additional coverage or risk management strategies are necessary for larger or higher-risk engagements.

The specific risks your firm faces depend heavily on project type, client relationships, and how your team manages design changes and site coordination. Understanding these exposure points prepares you to select the right policy and implement the risk controls that keep claims from materializing in the first place.

What Claims Actually Cost Your Firm

Structural Design Flaws Drive the Highest Claim Costs

Structural design flaws represent the costliest claims architects face, and they’re entirely preventable through disciplined verification processes. A column spacing error that contradicts established engineering standards forces contractors to halt work, rebuild structural elements, and absorb cascading delays across the entire project timeline. Material specification failures-such as failing to verify that fire-retardant materials meet local building codes before approval-trigger remediation costs that can reach tens of thousands of dollars, plus project delays measured in months. One calculation error in scale conversion or dimension verification renders components unusable and creates shared liability exposure across multiple parties on site. Your professional liability insurance covers defense costs and damages when these errors surface in claims, but the real financial damage extends beyond insurance: reputation harm, project delays that strain client relationships, and the internal costs of rework that insurance doesn’t cover. The Post-Tension Institute and similar authoritative design references exist specifically to prevent these errors, yet architects who skip validation against credible standards face substantially higher claim frequency and premium costs over time.

How Budget Overruns Escalate Into Claims

Budget overruns and project delays stem almost entirely from poor site analysis, unclear scope definition, and inadequate contract administration. Architects who underestimate costs to satisfy clients early in the process create financial strain that inevitably surfaces in disputes later, and these disputes frequently escalate into claims alleging negligent cost projections or scope mismanagement. Inadequate site analysis-missing soil conditions, drainage challenges, or access constraints-leads to design changes mid-construction that force cost increases and timeline extensions. Your professional liability policy protects you when clients sue over these cost and delay issues, but prevention requires upfront investment in thorough site investigation, explicit scope documentation in contracts that clearly defines what your firm will and won’t do, and rigorous contract administration by qualified personnel trained to catch scope creep before it becomes a liability exposure.

Why Contract Administration Determines Claim Frequency

Firms that assign contract administration to junior staff without ongoing training consistently experience higher claim rates than those with designated, experienced administrators managing client communication and change order documentation. The difference in claim frequency directly impacts your insurance premiums and your firm’s financial stability. Qualified administrators catch problems early, document decisions thoroughly, and prevent the miscommunication that triggers disputes. This single operational choice-investing in experienced contract administration-reduces your exposure more effectively than any other risk control measure available to architectural practices.

The specific risks your firm faces depend heavily on project type, client relationships, and how your team manages design changes and site coordination. Understanding these essential protections prepares you to select the right policy and implement the risk controls that keep claims from materializing in the first place. The next section examines how to assess your firm’s actual risk exposure and match it to the right coverage limits and policy structure.

Matching Your Coverage to Your Firm’s Actual Risk Profile

Your firm’s risk exposure isn’t generic-it depends on project type, client expectations, employee experience, and how tightly you manage scope creep. A five-person residential design practice faces fundamentally different exposures than a twenty-person firm handling institutional projects, yet many architects select coverage limits based on what competitors carry rather than what their specific work demands.

Categorize Your Projects and Identify Your Highest-Risk Work

Start with your project portfolio over the past three years: residential, commercial, institutional, or mixed-use. Identify which category generates the highest revenue and carries the greatest complexity. Institutional and mixed-use projects typically trigger higher claim frequency because they involve more stakeholders, longer timelines, and stricter building codes. Your firm’s claims history matters significantly-if you’ve had zero claims in five years, you’ll qualify for better rates than a firm with two claims in the same period. Underwriters also consider near-misses and complaints that didn’t formally materialize into claims.

Align Your Limits to Revenue and Project Scope

The standard tiering system ties your claim limits directly to annual gross fees. Firms earning $500,000 to $999,999 annually typically carry $500,000 per claim and $2,000,000 aggregate limits, while those exceeding $1,000,000 in fees require $1,000,000 per claim and $4,000,000 aggregate. However, these minimums don’t account for project-specific risk. A residential firm with $600,000 in annual revenue handling a single large institutional project may need temporary higher limits for that engagement, which you can address through project-specific endorsements rather than permanently increasing your base policy.

Choose Your Deductible Based on Cash Flow and Claims History

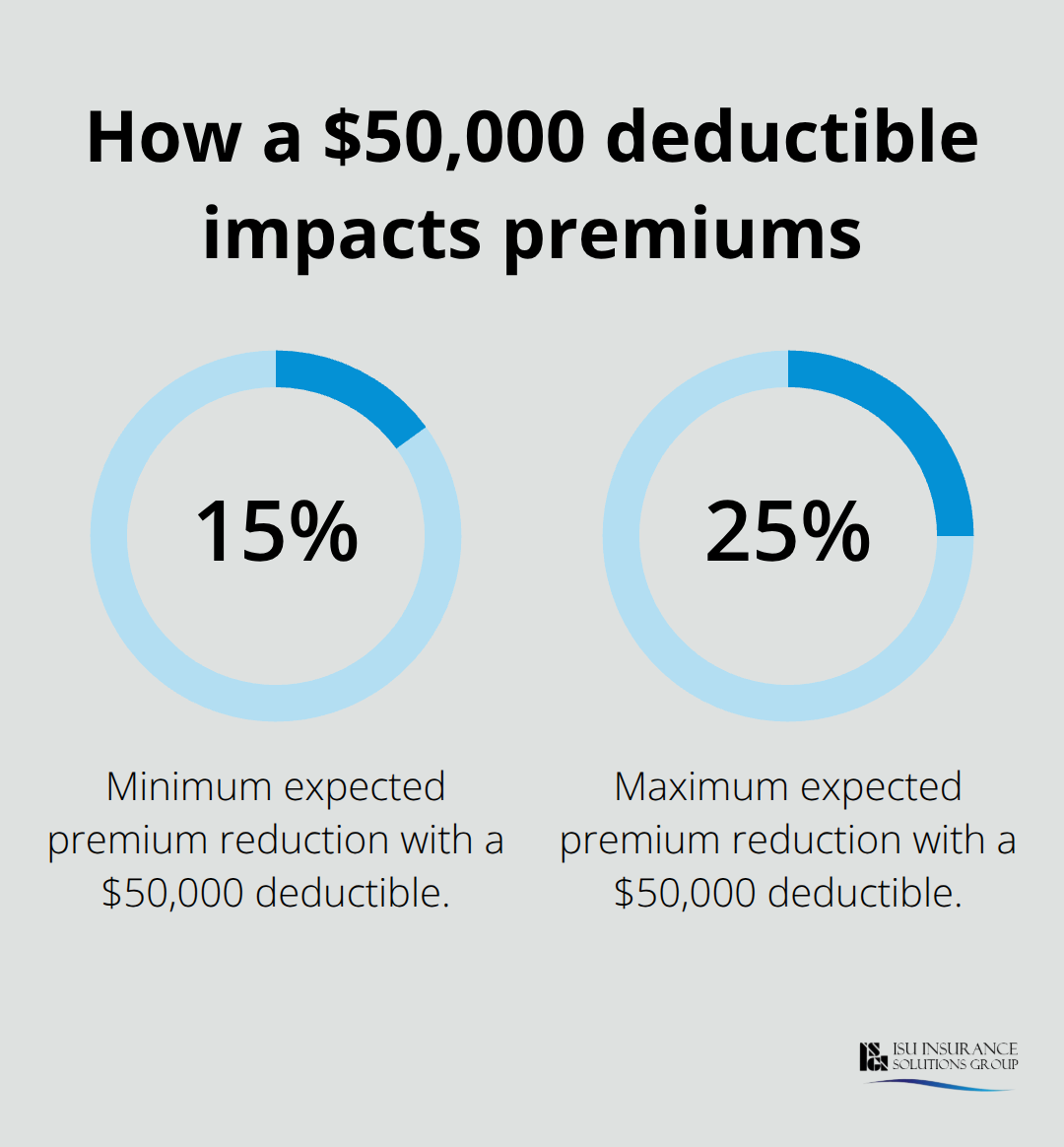

Your deductible choice directly impacts your annual premium and your out-of-pocket exposure when claims arise. Most architects select $25,000 deductibles as a middle ground, but firms with strong cash reserves and consistent project success can justify $50,000 deductibles to reduce annual premiums by 15 to 25 percent. Conversely, firms with tight cash flow or higher historical claims should stay with lower deductibles even if premiums cost more annually-the financial stability matters more than premium savings when a claim surfaces.

Verify Coverage for Exclusions and Special Risks

Policy exclusions deserve serious attention because water ingress claims are typically excluded unless your designs meet specific technical requirements schedules that your carrier publishes. If your firm designs projects in wet climates or handles substantial waterproofing work, verify whether your carrier offers a path to coverage for water-related claims through technical compliance rather than accepting blanket exclusion. Cyber and data breach coverage isn’t mandatory but becomes relevant if your firm stores client information, project files, or financial data electronically. General liability coverage complements your professional liability policy by protecting against third-party bodily injury or property damage claims unrelated to design services, and workers’ compensation is non-negotiable in every state where you employ staff.

Request Complete Documentation Before Committing

Request a complete declarations page and policy summary from any carrier you’re considering, then have your agent walk through exclusions, limits, and how defense costs apply to your specific situation before committing to any policy. This step prevents surprises when claims arise and confirms that your coverage actually matches your firm’s risk profile.

Final Thoughts

Architect professional liability insurance separates firms that survive claims from those that face financial devastation. Without coverage, a single design error or supervision dispute forces your firm to pay tens of thousands in legal fees and damages directly from operating capital, while coverage allows your practice to continue serving clients without interruption. The right policy protects your reputation and financial stability when claims arise.

Three actions move you forward immediately. Audit your current coverage against your actual project portfolio and revenue to confirm you carry adequate limits for the work you perform. Document your firm’s risk controls-rigorous design verification, qualified contract administrators, thorough site analysis-because these operational practices directly reduce your premiums and claim frequency over time. Schedule a conversation with an agent who understands architectural practice and can walk through your specific exposures rather than offering generic quotes.

We at ISU Insurance Solutions Group work with 20+ carriers to find architect professional liability insurance policies that match your firm’s size, project type, and risk profile. Contact us today for a multi-carrier quote that reflects your actual exposure. Your firm’s protection starts with one conversation.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.