Auto Insurance for Homeowners: What You Need to Know

Homeowners often overlook the fact that their auto insurance needs differ significantly from those of other drivers. At ISU Insurance Solutions Group, we’ve seen countless homeowners make costly mistakes by assuming their current coverage is adequate.

Auto insurance for homeowners requires careful attention to liability limits, bundling opportunities, and protection gaps that renters or apartment dwellers might not face. The right policy can save you thousands while protecting your assets and finances.

Why Homeowners Actually Need Different Auto Coverage

Auto insurance and homeowners insurance serve completely separate functions, yet many homeowners treat them as interchangeable. Homeowners insurance protects your house structure, belongings, and liability if someone gets injured on your property. Auto insurance protects your vehicle, covers injuries you cause to others in a car accident, and shields your personal assets if you’re found liable for significant damages. The two policies operate in different legal jurisdictions and follow different state regulations.

How Your Home Changes Your Auto Insurance Needs

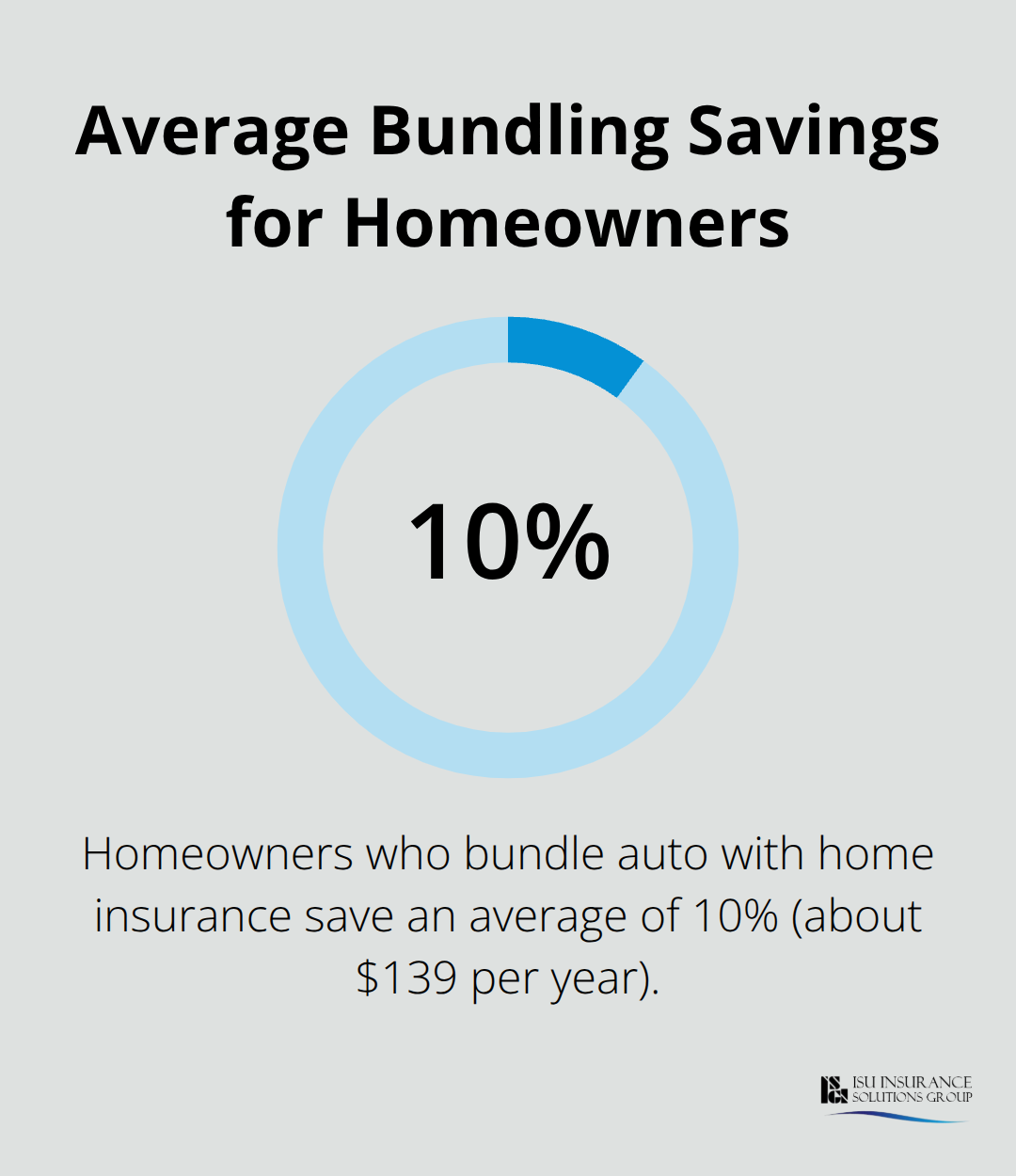

When you own a home, your financial exposure extends far beyond just protecting the vehicle itself. According to The Zebra’s analysis of 61 million rate quotes, homeowners who bundle auto with home insurance save an average of 10 percent (roughly $139 per year) because insurers recognize that homeowners represent lower-risk profiles than renters. However, this discount only materializes if you actually carry adequate auto coverage in the first place.

Many homeowners mistakenly believe their homeowners policy covers vehicle liability or that basic coverage is sufficient. The reality is stark: if you cause a serious accident and injure someone, your auto liability limits determine how much protection your personal assets receive. A single catastrophic accident can result in judgments exceeding $500,000, which is precisely why your auto policy limits matter far more than most homeowners realize.

Your Home as an Asset Requiring Stronger Auto Protection

Homeowners possess significant assets that renters typically don’t, which means your auto liability exposure carries higher stakes. If you’re found at fault in an accident that causes severe injuries or death, a judgment can attach to your home through a lien or forced sale in some circumstances. This is why collision and comprehensive coverage become more valuable when you own property.

Additionally, homeownership status actually affects your auto insurance rates in 46 states plus Washington D.C., according to The Zebra’s research. Homeowners pay approximately $35 less per year for the same auto coverage than renters, representing roughly a 2.4 percent lower rate nationally. This pricing advantage exists because insurers view homeowners as more responsible and stable, but you only benefit from this lower rate if you’re actually insured. The gap widens dramatically by state, with renters in New Jersey paying about 11.4 percent more than homeowners for identical coverage. These aren’t theoretical differences-they represent real money that compounds over years of policy ownership.

The Bundling Trap: Coverage First, Discounts Second

The misconception that bundling always saves money can actually work against you if it pushes you toward inadequate limits just to hit a price point. The correct approach involves selecting proper coverage first, then shopping bundled options to find the best rate on that same level of protection. Your liability limits should reflect your actual assets and income, not the discount available at a particular carrier.

When you move forward with your auto insurance search, understanding these coverage distinctions positions you to make decisions based on protection rather than price alone. The next section examines the specific coverage types that matter most for homeowners and how each one protects different aspects of your financial life.

Coverage That Actually Protects Your Homeowner Assets

Liability Coverage: The Real Protection Your Assets Need

Liability coverage is where homeowners most often expose themselves to financial ruin, yet it remains the easiest coverage to underestimate. Most states require minimum liability limits around $15,000 to $25,000 per person, but those minimums exist only to satisfy legal requirements-not to protect your actual wealth. If you own a home worth $400,000 or more, carrying only state minimum liability coverage leaves hundreds of thousands of dollars in personal assets vulnerable to a lawsuit.

A single at-fault accident causing serious injuries can generate judgments of $500,000 or higher, and your home can be attached through liens or forced sale in many states. Homeowners recognize this exposure differently than renters, which is why liability limits should scale with your net worth, not with what your state legally requires. Most homeowners should carry at least $100,000 in bodily injury liability per person and $300,000 per accident, then layer an umbrella policy on top for additional protection. This isn’t theoretical-it’s the baseline that protects the equity you’ve built.

Collision and Comprehensive: Protecting Your Vehicle Investment

Collision and comprehensive coverage determines whether a car accident or weather event depletes your emergency fund or gets handled by insurance. Collision pays for damage when you hit another vehicle or object, while comprehensive covers theft, weather, vandalism, and animal strikes. Homeowners often skip these coverages on older vehicles to save money, but that calculation fails when you need the car for commuting to work and cannot afford a replacement.

The gap between keeping an old car paid off versus carrying collision coverage is usually $200 to $400 annually, which means a single accident can cost ten times that amount out of pocket. If you have a mortgage, your lender requires comprehensive and collision anyway, so the decision is really about whether to keep them after the loan is paid off. This coverage becomes especially valuable when you own property, since you cannot easily absorb unexpected vehicle replacement costs without disrupting your household finances.

Uninsured and Underinsured Motorist Coverage: Closing the Gap

Uninsured and underinsured motorist coverage protects you when the other driver caused the accident but lacks adequate insurance-a scenario that happens in roughly one in eight accidents nationally. This coverage pays your medical bills and vehicle damage when the at-fault driver’s policy maxes out or they carry no insurance at all. Many homeowners treat this as optional, but uninsured motorist coverage costs roughly $50 to $100 annually and covers gaps that your health insurance will not touch, making it essential protection for anyone with significant assets to lose.

When you own a home, this protection becomes even more valuable because you have more to protect. The cost is minimal compared to the financial exposure you face if an uninsured driver causes serious damage. Your next step involves assessing your specific driving habits and risk factors to determine which coverage levels make sense for your household situation.

How to Choose the Right Auto Policy as a Homeowner

Match Coverage to Your Actual Driving Patterns

Your driving habits determine which coverage types matter most and which ones you can safely skip. A homeowner who commutes 45 minutes each way on highways faces different risks than someone working from home who drives occasionally for errands. Track your annual mileage and identify whether you drive during rush hour, in weather-prone areas, or on rural roads where uninsured motorists are more common. According to The Zebra’s analysis, homeowners who assess their risk profile accurately and match coverage to actual exposure patterns save significantly more than those who simply bundle everything together.

If you drive fewer than 5,000 miles annually, you might qualify for low-mileage discounts that some carriers offer, which can reduce your premium by 10 to 15 percent. Conversely, if you drive 25,000 miles yearly in heavy urban traffic, collision and comprehensive coverage becomes non-negotiable regardless of your vehicle’s age, because accident probability climbs substantially. Document whether you have a garage, driveway, or street parking, since theft and weather damage rates vary dramatically by storage location. Homeowners with garage parking often qualify for lower comprehensive rates because the vehicle spends protected time off the street.

Age matters too-if you’re over 50 and have a clean driving record, many insurers offer mature driver discounts ranging from 5 to 15 percent, which stack on top of bundling discounts.

Evaluate Bundling Against Separate Quotes

Bundling auto with homeowners insurance typically saves homeowners about 10 percent on their auto premium. However, this discount only works if you compare actual bundled quotes against separate quotes from multiple carriers rather than assuming your current insurer offers the best bundled rate. The bundling trap occurs when homeowners accept a bundled discount that’s smaller than the difference between their current separate policies and what competitors offer unbundled.

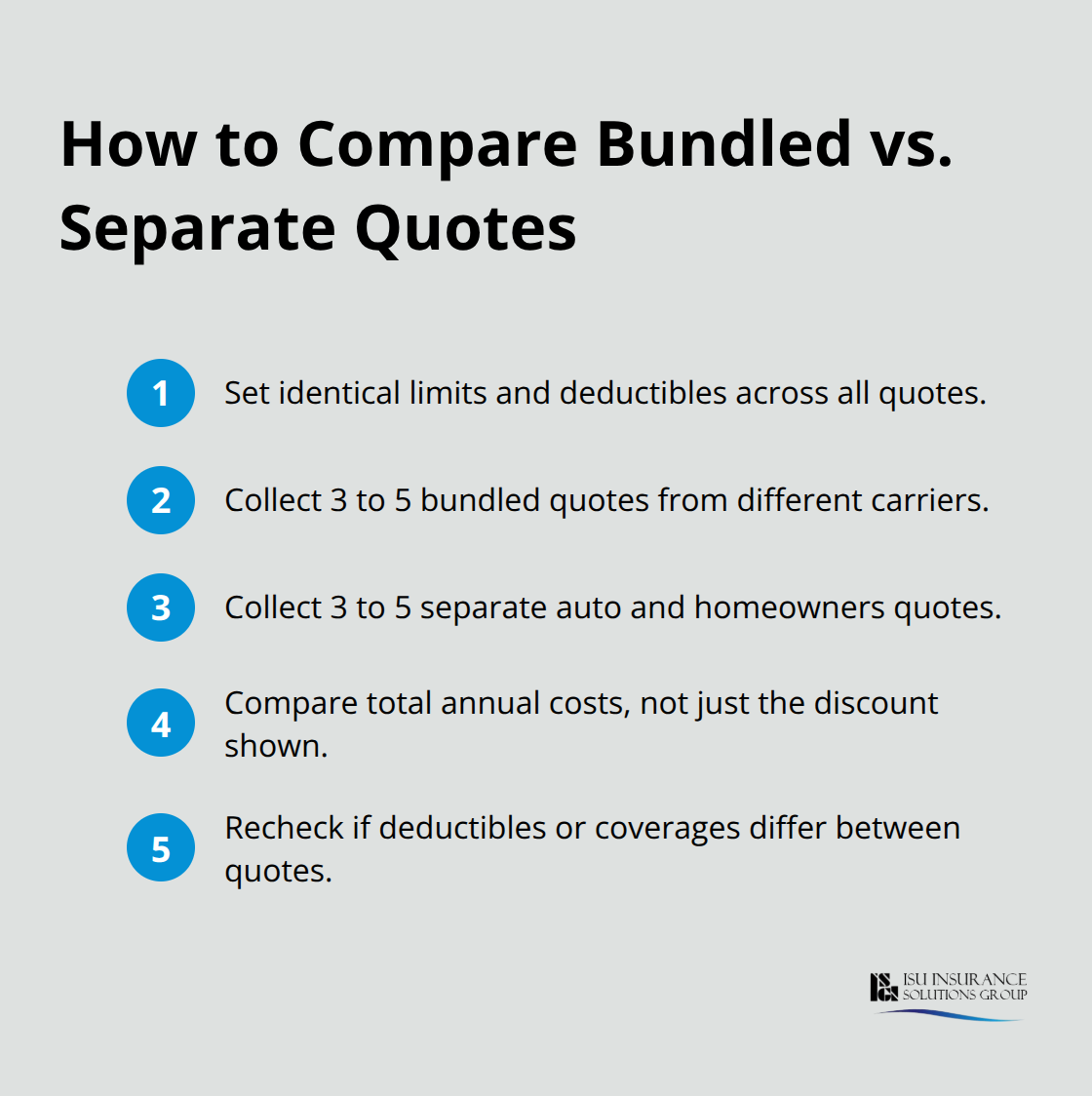

For example, if your current auto premium is $1,400 annually and your homeowners is $1,200, a 10 percent bundling discount saves $260 total. But if another carrier quotes $1,100 for auto and $1,050 for homeowners separately, you save $350 without bundling. The only way to know is to collect three to five bundled quotes and three to five sets of separate quotes, then compare total annual costs. When gathering quotes, ensure you compare identical coverage limits and deductibles across all options, since a $500 deductible versus $1,000 deductible creates apples-to-oranges comparisons that hide the actual price difference.

Track Discounts and Align Policy Dates

Track which discounts you qualify for at each carrier-multi-policy, multi-vehicle, safety features, paperless billing, automatic payment-because these discounts vary widely and often don’t appear unless you ask. A local independent agent can help align your policy start dates so your auto and homeowners coverage renew together, which simplifies management and ensures you don’t accidentally let coverage lapse when switching between carriers.

This coordination prevents gaps in protection and reduces the administrative burden of managing multiple renewal dates throughout the year.

Final Thoughts

Auto insurance for homeowners demands regular attention rather than a single decision made years ago. Your coverage needs shift as your home equity grows, your driving patterns change, or your household circumstances evolve. Start by reviewing your current policy declarations page to confirm your liability limits, deductibles, and which coverages you actually carry-many homeowners discover they’re either over-insured on older vehicles or under-insured on liability.

Gather fresh quotes from at least three carriers using identical coverage limits and deductibles, requesting both bundled and separate quotes so you can calculate which approach delivers the lowest total cost for your household. This comparison takes roughly 30 minutes but often reveals $300 to $500 in annual savings that homeowners leave on the table by never shopping around. When you receive quotes, ask specifically about discounts you qualify for (safety features in your vehicle, bundling, low mileage, mature driver status, or paperless billing) since these discounts vary dramatically between carriers.

An independent agent can simplify this process considerably. We at ISU Insurance Solutions Group work with multiple carriers to find auto insurance for homeowners that matches your actual needs and budget, rather than pushing you toward a single company’s bundled package. Contact us at https://isgwoodinville.com to discuss your auto insurance needs with a local agent who understands your community and can deliver personalized solutions.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.