Commercial Vehicle Insurance Oregon: Coverage That Scales

Growing your business means your insurance needs change fast. At ISU Insurance Solutions Group, we help Oregon businesses find commercial vehicle insurance that actually fits where you are today and where you’re heading tomorrow.

Your fleet might be three vehicles now and thirty next year. The right coverage scales with you, and the right rates reward your growth.

What Oregon Actually Requires for Commercial Vehicle Insurance

Oregon’s Mandatory Coverage Minimums

Oregon law is strict about commercial vehicle insurance, and the penalties for falling short are real. Every business operating a vehicle on Oregon’s public highways must carry liability insurance with proof filed to the Oregon Department of Transportation’s Commercial Carrier Section within 60 days of vehicle registration.

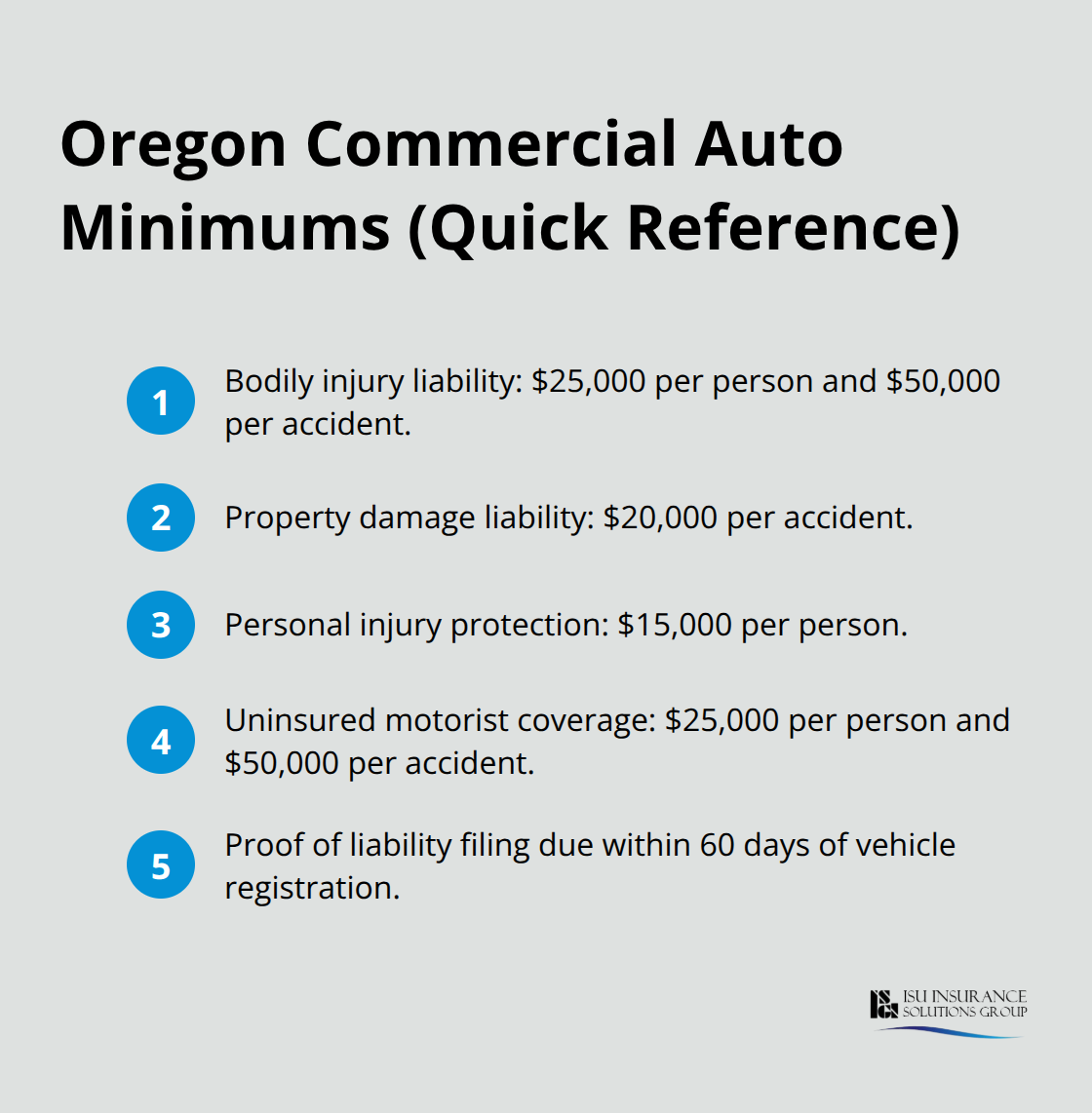

The baseline requirements from the Oregon DMV are bodily injury liability of $25,000 per person and $50,000 per accident, property damage liability of $20,000 per accident, personal injury protection of $15,000 per person, and uninsured motorist coverage of $25,000 per person and $50,000 per accident. Operating without filed proof is a Class B traffic violation that costs between $135 and $1,000 in fines, plus potential suspension of driving privileges.

Federal Requirements for Larger Vehicles

For larger vehicles over 10,000 pounds, federal FMCSA requirements add another layer-the liability minimums jump significantly based on vehicle weight, whether you operate interstate, passenger capacity, and whether you transport hazardous materials. Oregon’s baseline minimums are genuinely low compared to what your actual exposure demands, especially if you haul freight or passengers. A single accident with significant injuries can easily exceed $750,000 in damages, which is why most Oregon fleets should carry higher limits than the legal minimum.

Filing Requirements and Deadlines

If you operate intrastate only, you file using Form E (liability) and Form H (cargo, if applicable) with the CCD, and your insurer or agent handles the filing-not you. Interstate carriers satisfy Oregon’s requirement by filing with FMCSA instead, which automatically covers state obligations. Cargo insurance is mandatory for for-hire shipments and requires a minimum of $10,000 coverage. The 60-day filing deadline is a compliance checkpoint that catches many operators off guard; miss it and your operating authority gets suspended. Unlike some states that allow online self-certification, Oregon demands actual certificates filed by your insurer, which means you cannot just purchase a policy and assume you are legal.

Coverage Types That Protect Your Operation

Different coverage types protect different pieces of your operation, and Oregon’s minimum requirements cover only third-party liability and uninsured motorist scenarios. Liability protects you when you damage someone else’s vehicle, property, or injure a person-it forms the foundation of any commercial policy. Physical damage coverage (collision and comprehensive) protects your own vehicles from accidents, theft, vandalism, weather, and fire, and while not legally required, it becomes essential if you financed or leased the vehicle. Medical payments coverage pays medical expenses for your employees and passengers regardless of fault, which keeps your crew whole and morale intact after minor incidents. Uninsured and underinsured motorist coverage fills the gap when the at-fault driver’s insurance is insufficient or nonexistent-Oregon requires this, but most businesses underestimate how often they need it.

Specialized Coverage for Your Fleet

For specialized operations, loading and unloading coverage protects equipment and cargo during transport, bobtail coverage handles tractors running without trailers, and hired and non-owned auto liability covers accidents involving employee personal vehicles used for work. Towing and roadside assistance keeps your fleet moving when breakdowns happen on the road. Oregon’s minimums do not account for the reality that your business assets face exposure every day-a single serious accident can wipe out months of profit, which is why physical damage and higher liability limits matter far more than the state’s floor suggests.

As your fleet grows, the coverage types you select today determine how well you protect tomorrow’s larger operation. The next section shows how to structure liability and physical damage protection across multiple vehicles and drivers without overpaying for redundant coverage.

How Liability Coverage Scales as Your Fleet Grows

Starting With Realistic Liability Limits

Your liability limits today will not protect your fleet tomorrow. Most Oregon businesses start with the state minimum of $750,000 combined single limit, which covers the legal floor but leaves serious exposure. A single accident involving multiple vehicles, injuries, or significant property damage routinely exceeds $750,000-trucking industry data shows average settlement for serious injury claims in commercial operations runs between $1 million and $3 million depending on severity and jurisdiction. As you add vehicles and drivers, your exposure compounds because each additional driver increases the statistical likelihood of an accident.

Consolidating Coverage Across Multiple Vehicles

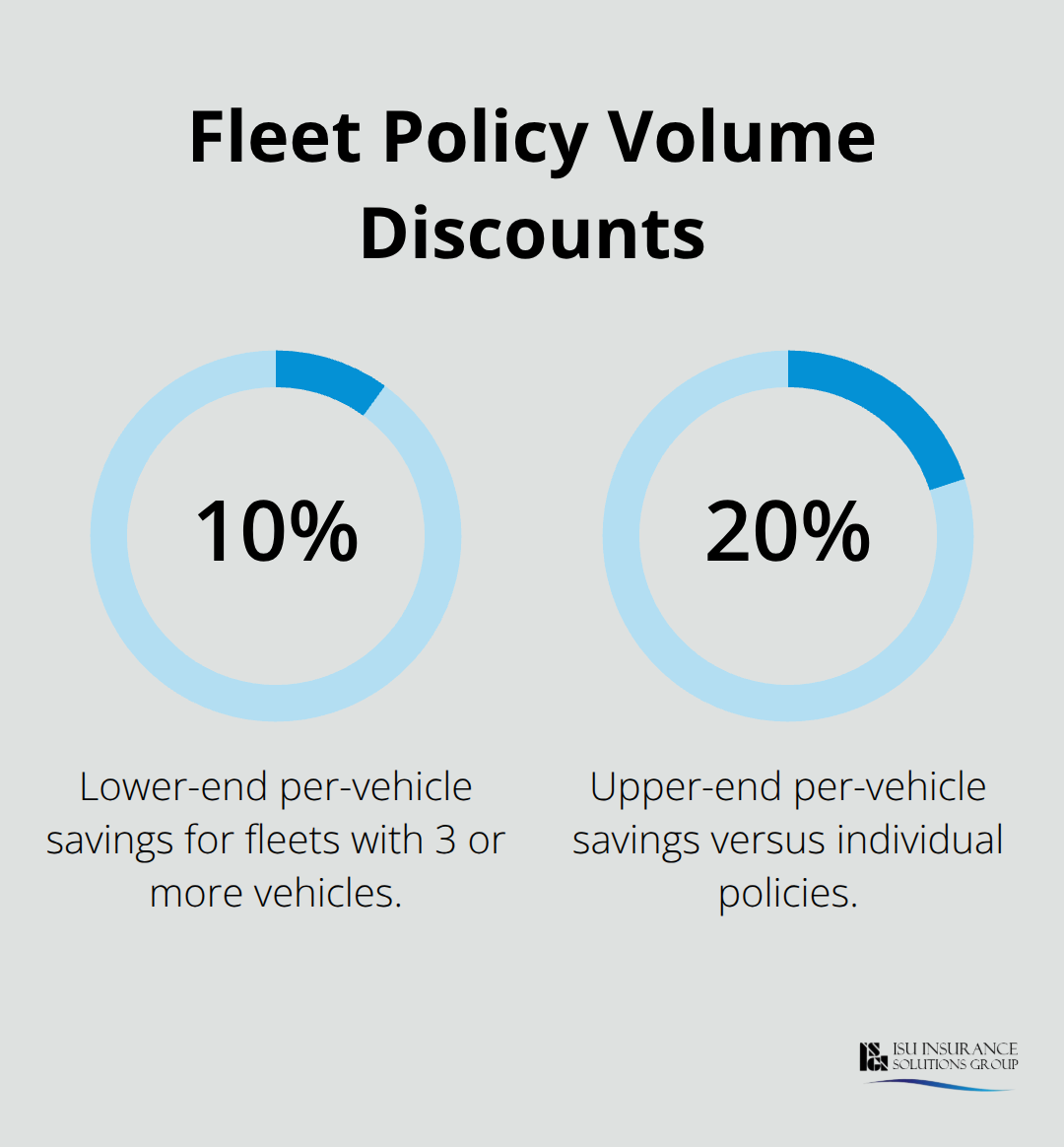

The solution is not to buy the same $750,000 policy three times; instead, you consolidate under one fleet policy with a higher aggregate limit that covers all vehicles and drivers under a single umbrella. This approach costs less than multiple single-vehicle policies and eliminates gaps where an accident on one vehicle exhausts the limit while others sit unprotected. When comparing quotes across carriers, ask specifically about fleet rates-Liberty Mutual, Nationwide, Travelers, and Progressive all offer volume discounts for Oregon fleets with three or more vehicles, typically reducing your per-vehicle cost by 10 to 20 percent compared to individual policies.

Physical Damage and Deductible Strategy

Physical damage coverage protects what you own, but the coverage structure matters more than the limit amount. Collision and comprehensive coverage (non-collision damage like theft, vandalism, weather) are optional under Oregon law, yet financially essential if your vehicles are financed or leased-lenders require them anyway. The real decision is your deductible: a $500 deductible costs roughly 15 to 25 percent more in premium than a $1,000 deductible, depending on vehicle value and type. For growing fleets, a $1,000 deductible typically makes financial sense because the annual premium savings across five vehicles can exceed $3,000 to $5,000, which covers several deductible payments.

Specialized Coverage for Unique Operations

Specialized coverage fills critical gaps: loading and unloading coverage protects cargo and equipment during transport (essential if you haul freight), bobtail coverage covers tractors operating without trailers (many carriers overlook this), and hired and non-owned auto liability protects you when employees use personal vehicles for business. The Oregon Department of Consumer and Business Services data shows that 35 to 40 percent of small fleet accidents involve employee personal vehicles, yet most businesses skip hired and non-owned coverage until they face a claim.

Federal Requirements for Larger Vehicles

For any vehicle over 10,000 pounds, verify federal FMCSA requirements using your vehicle’s USDOT number-these may demand higher liability limits than Oregon’s state minimum, which your agent can confirm and build into your policy structure. The next section examines how to identify which coverage options your specific operation actually needs and how to avoid paying for protection you will never use.

What Actually Drives Your Premium

Vehicle Type, Age, and Fleet Size Set Your Baseline

Fleet size, vehicle type, and driver history dominate your premium calculation, but the specifics matter far more than general rules suggest. A five-vehicle fleet with newer trucks and experienced drivers costs dramatically less per vehicle than a three-vehicle fleet with older vehicles and drivers under 25. The Oregon Department of Consumer and Business Services data shows commercial auto insurance for small Oregon businesses averages around $107 per month per vehicle, but roughly 37 percent of small businesses pay under $100 monthly while others exceed $200 depending on their risk profile. Vehicle weight and age matter enormously: a 2022 pickup costs roughly 30 to 40 percent less to insure than a 2015 model of the same make because newer vehicles have better safety technology and lower repair costs.

Hazardous materials transport and geographic factors reshape your costs significantly. If you transport hazardous materials, your premium jumps 20 to 35 percent above standard rates regardless of your safety record. Daily mileage and route patterns affect cost too-a fleet that stays within Portland’s metro area faces lower premiums than one covering rural eastern Oregon because accident frequency and theft risk differ significantly by geography.

Deductibles and Claims History Control Costs

Your deductible choice directly controls premium: moving from a $500 to $1,000 deductible typically saves 15 to 25 percent annually, which on a five-vehicle fleet translates to $3,000 to $5,000 in savings that offset several deductible payments. Claims history is the single largest premium driver after vehicle type-a single at-fault accident can raise rates 20 to 40 percent for three years, making accident prevention genuinely cheaper than claiming minor damage.

Compare Quotes Across Multiple Carriers

Rates vary wildly across carriers for identical coverage because each insurer weights risk factors differently. Liberty Mutual, Nationwide, Travelers, and Progressive all offer Oregon commercial fleet coverage, but one carrier’s quote for your operation might be 25 to 40 percent higher or lower than another’s depending on their underwriting appetite for your specific vehicle types and business model. An independent agent can pull quotes from multiple carriers simultaneously rather than forcing you to contact each one separately, which saves time and surfaces discounts you would miss calling carriers individually.

Safety Programs and Loss Prevention Reduce Rates

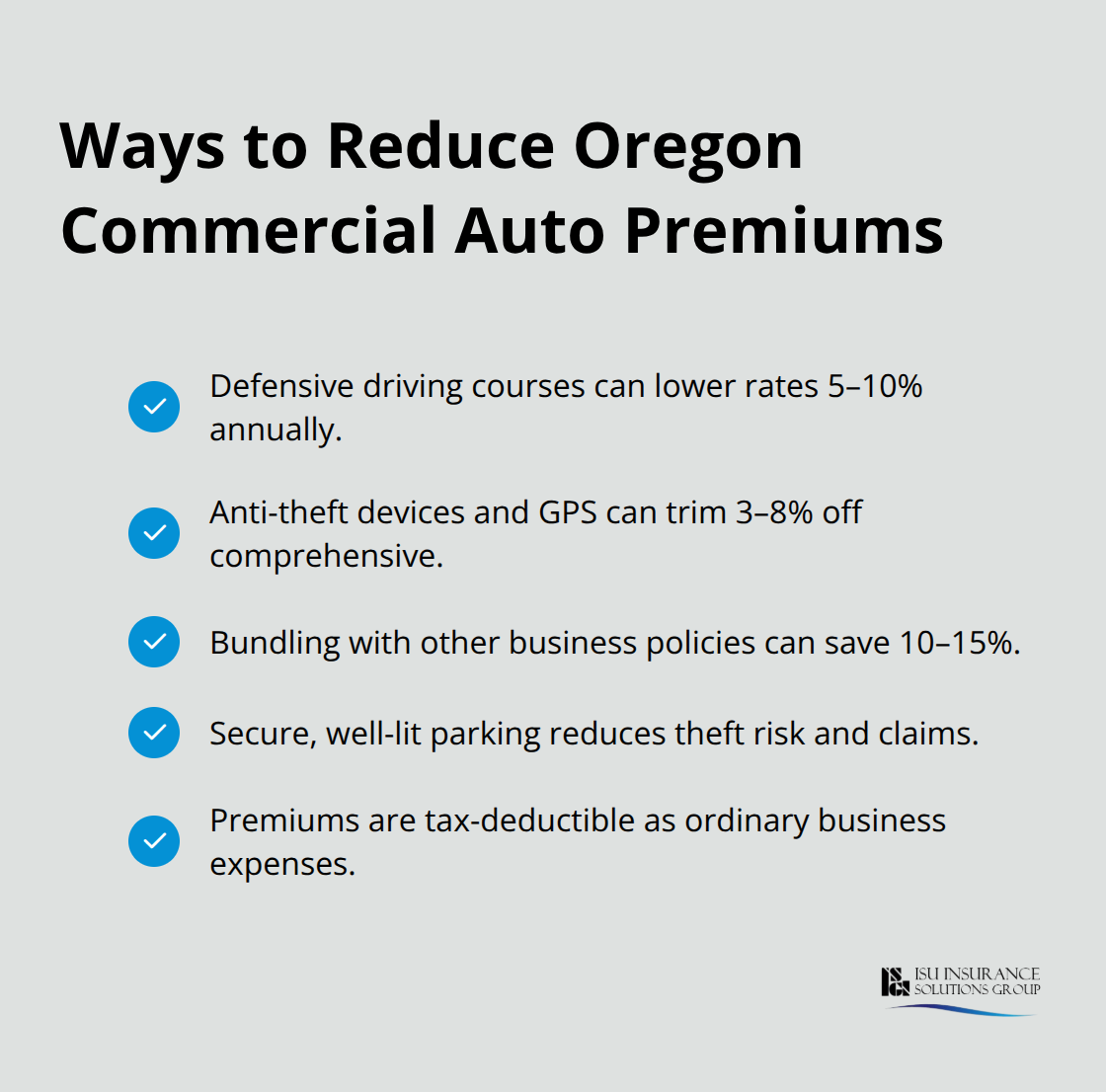

Safety training programs, clean driving records, and vehicle maintenance reduce premiums because insurers reward behaviors that prevent claims-enrolling your drivers in defensive driving courses through organizations like the National Safety Council can lower rates 5 to 10 percent annually. Anti-theft devices, GPS tracking, and parking vehicles in secured lots also reduce theft risk and can trim 3 to 8 percent off comprehensive coverage costs. Bundling commercial auto with other business coverage like general liability or property insurance often yields 10 to 15 percent discounts across the board.

Oregon tax law allows you to deduct all commercial vehicle insurance premiums as ordinary business expenses, which reduces your actual cost basis compared to the stated premium.

Final Thoughts

Your commercial vehicle insurance in Oregon must scale as your business expands. The state minimums-$25,000 bodily injury per person, $50,000 per accident, $20,000 property damage-protect you legally but leave you exposed when serious accidents happen. Most claims exceed these limits by hundreds of thousands of dollars, so your actual coverage should reflect your real exposure, not just what Oregon demands.

Consolidate liability across multiple vehicles under one fleet policy rather than buying separate coverage for each truck. Choose deductibles strategically so your annual savings offset the higher out-of-pocket cost when claims occur, and add specialized coverage like hired and non-owned auto liability before an employee’s personal vehicle causes an accident on company business. These decisions compound over time-a fleet that starts with realistic limits costs far less per vehicle than one that scrambles to add protection after exposure becomes obvious.

Local agents understand Oregon’s filing deadlines, federal FMCSA requirements for larger vehicles, and which carriers compete on your type of operation. We at ISU Insurance Solutions Group have served Oregon and Washington businesses since 1983, helping fleets scale coverage as they grow. Start by requesting quotes that reflect your actual fleet size and growth plans, then review your current policy against the coverage types outlined here.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.