Independent Agent Professional Liability: Insurance That Grows With Your Practice

Independent agents face a unique set of risks that standard business insurance simply doesn’t cover. A single mistake in policy recommendations or client communication can trigger claims that threaten your practice and reputation.

At ISU Insurance Solutions Group, we’ve seen how the right professional liability coverage protects agents at every stage of growth. This guide walks you through the coverage options and strategies that keep your agency secure as you scale.

What Independent Agents Actually Need to Know About Professional Liability

The Coverage Gap That Exposes Your Practice

Standard commercial policies leave independent agents dangerously exposed. General liability covers third-party bodily injury and property damage-someone slips in your office or you damage a client’s property. Professional liability covers something entirely different: negligent advice, errors in policy placement, misrepresentation, or failure to deliver promised services. When you recommend a coverage option that turns out to be inadequate, or you miss a deadline that costs a client thousands in uninsured losses, general liability won’t help you. The gap between these two types of coverage is where most independent agents encounter serious trouble.

What the Data Reveals About E&O Claims

A 2025 Best Practices Study analyzing over 3,000 data points across agencies of all sizes found that governance practices and structured risk controls directly correlate with lower E&O claim frequency. Agencies without documented processes for client communication, policy review protocols, and staff training experience significantly higher liability exposure. Real claims against independent agents include misquoting premium amounts, failing to add required coverages, missing policy renewal deadlines, providing incorrect underwriting information to carriers, and giving advice outside their licensing scope. Each of these scenarios can result in client financial losses ranging from thousands to hundreds of thousands of dollars, and your agency bears the liability.

Why Your Advice Requires Specific Protection

Your errors and omissions insurance create exposures that general liability, property insurance, and workers’ compensation simply don’t address. A client who claims you misrepresented coverage terms, failed to explain policy exclusions, or recommended inadequate limits will pursue you directly. Defense costs alone can exceed $50,000 before any settlement or judgment. Professional liability policies cover defense expenses outside the policy limit in most quality plans, meaning your legal costs don’t reduce your available coverage for damages.

Cyber liability has become inseparable from professional liability for independent agents. As you move client data online and rely on digital communications, first-party breach costs and third-party liability from data mishandling require specific coverage. Standard policies exclude cyber incidents entirely.

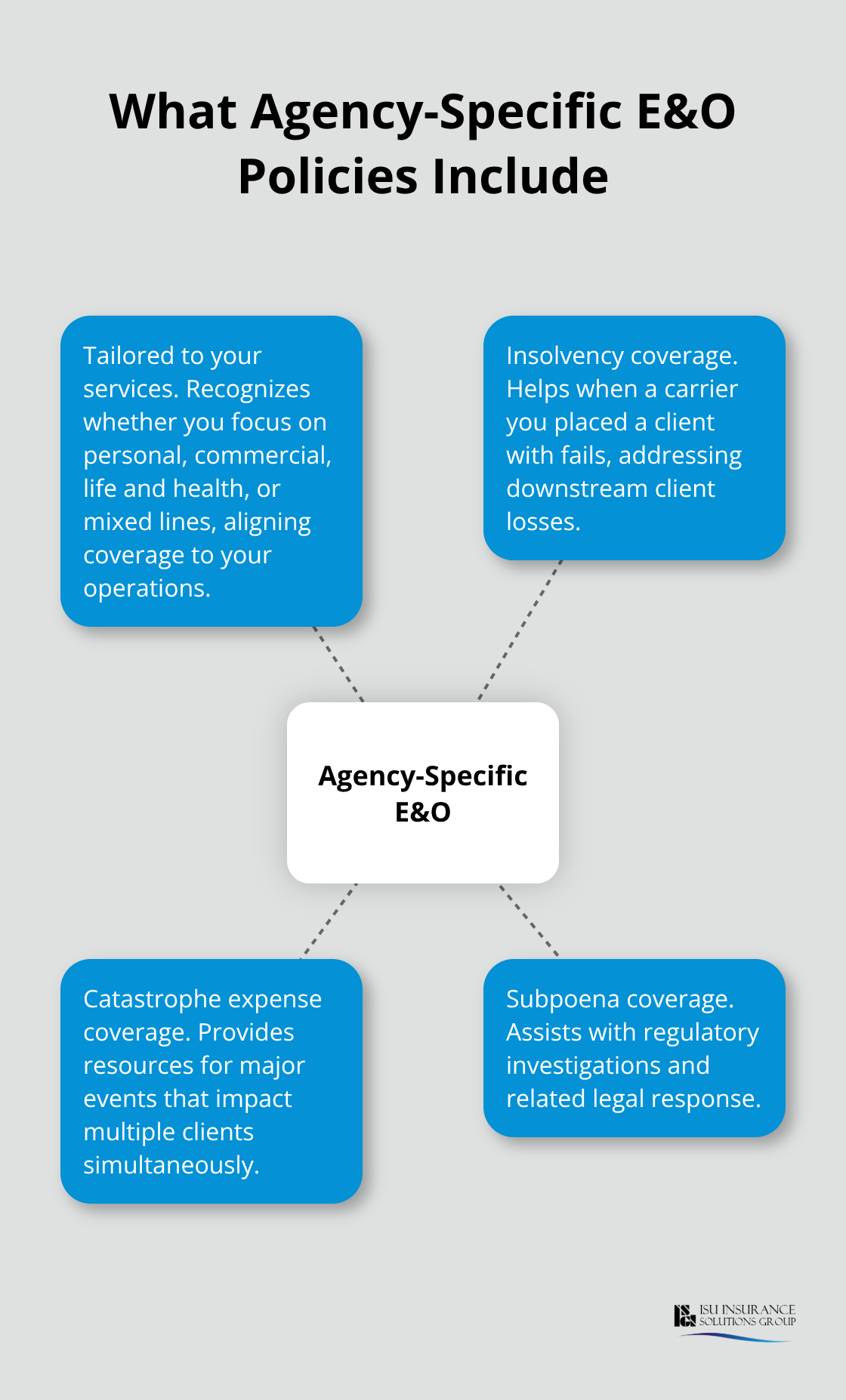

Agency-Specific Policies Address Your Real Operations

Agency-specific professional liability policies recognize the exact services you provide-whether you specialize in personal lines, commercial, life and health, or a combination-and tailor coverage accordingly. They include provisions for insolvency coverage if a carrier you placed a client with fails, catastrophe expense coverage for major events affecting multiple clients, and subpoena coverage for regulatory investigations. These aren’t add-ons; they’re built into policies designed specifically for how independent agents operate.

The market has shifted from soft to hard in recent years, meaning broader coverage is harder to find and rates have increased. This shift makes it critical to secure agency-specific protection rather than hoping general business insurance will suffice. Your next step involves understanding what coverage limits actually protect your practice as it grows.

Coverage Limits That Protect Growing Agencies

Matching Coverage to Your Agency Size

Professional liability policies for independent agents vary significantly based on your agency size and service mix. A solo agent handling personal lines needs different protection than a 20-person shop writing commercial accounts across multiple states. The 2025 Best Practices Study tracking over 3,000 data points across seven revenue bands shows that agencies under $1.25 million annual revenue typically carry $1 million per claim limits, while agencies between $10 million and $25 million in revenue average $5 million per claim. This pattern reflects reality: higher revenue means more clients, more transactions, and statistically higher exposure to larger claims.

How Risk Controls Lower Your Costs

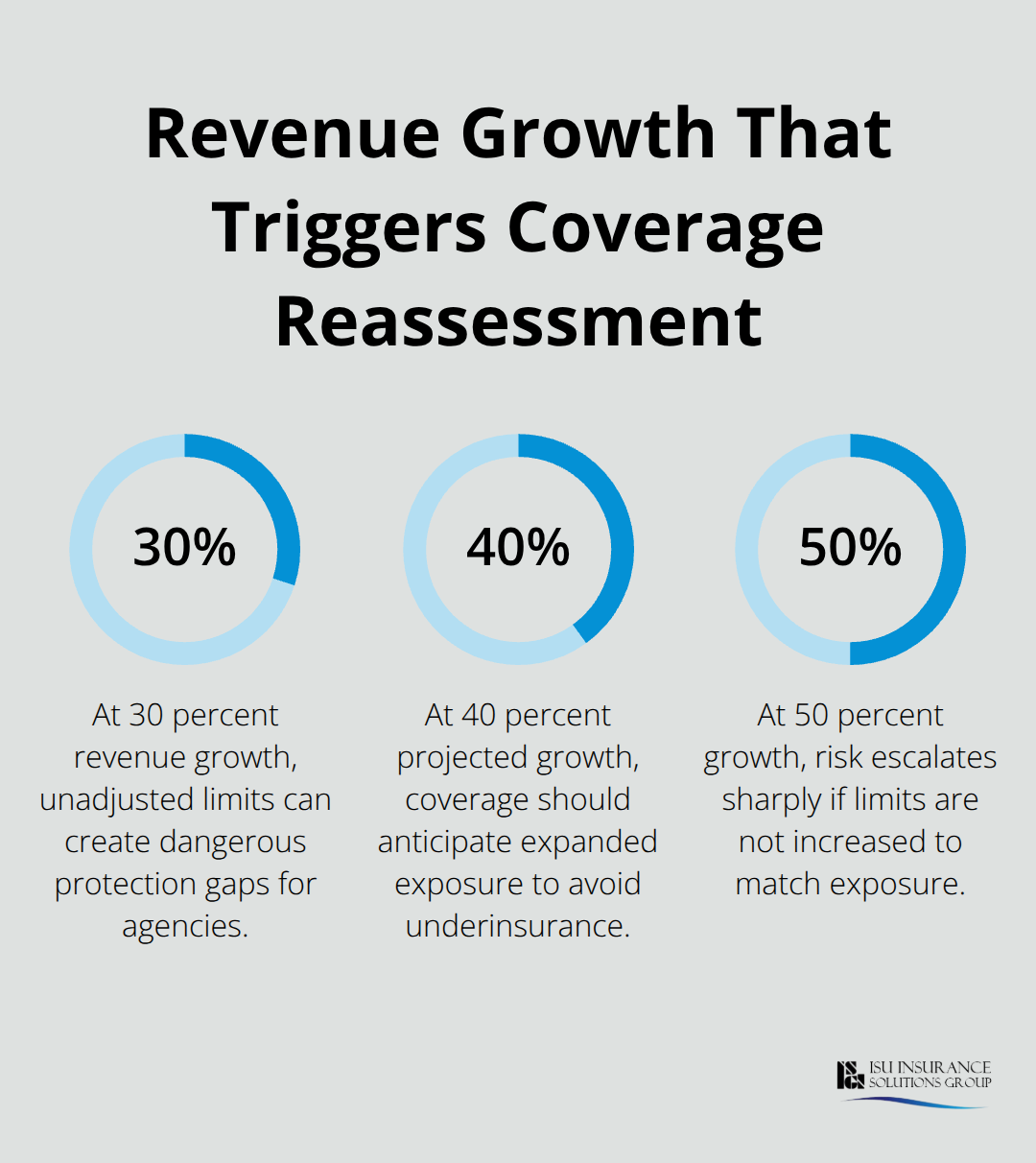

The same study reveals that agencies with documented risk controls and governance practices-client communication protocols, policy review checklists, staff training records-secure better rates and lower deductibles than those operating without structure. Your policy limits should reflect not just your current size but your growth trajectory over the next three years. If you project 40 percent revenue growth, your coverage should anticipate that expanded exposure now rather than leaving you underinsured during your growth phase.

Defense Costs Outside Your Limit

A single E&O claim generates legal bills that start accumulating before any settlement discussion begins. Quality professional liability policies place defense costs outside the policy limit, meaning your $2 million coverage for damages remains intact while defense expenses-expert witnesses, depositions, discovery, trial preparation-stack up separately. This structure matters enormously. If your policy lumps defense costs inside your limit, a $150,000 legal defense consumes 7.5 percent of your available coverage before you’ve resolved the claim. The Big I Professional Liability Program includes defense costs outside limits as standard, along with catastrophe expense coverage of $25,000 per policy period for events affecting multiple clients simultaneously.

Cyber Coverage as a Core Component

Cyber liability has shifted from optional to essential. As your agency digitizes client files and communication, your exposure to data breach costs and third-party liability from mishandled information increases dramatically. Cyber coverage under professional liability policies typically covers first-party breach costs-forensics, notification, credit monitoring-plus third-party liability if your systems fail and damage client data. The Big I program includes $25,000 in first-party cyber costs and $1 million in third-party cyber liability as standard components. This coverage protects you when ransomware hits your systems or a hacked email account sends fraudulent policy cancellations to clients. Without it, you absorb breach notification costs, regulatory fines, and client lawsuits directly.

Scaling Your Protection as Revenue Grows

Your coverage limits today won’t match your needs in two years. Agencies that grow their revenue by 30 to 50 percent without adjusting their professional liability limits create dangerous gaps in protection. The next step involves assessing your actual risk exposure and determining which coverage adjustments align with your specific growth plans.

How to Assess and Adjust Your Professional Liability Coverage as You Scale

Start With Your Current Numbers

Most independent agents wait until a claim hits to realize their coverage limits no longer match their practice. The 2025 Best Practices Study tracked over 3,000 data points across agencies of varying sizes and found that agencies reviewing their professional liability coverage annually experience significantly fewer coverage gaps than those reviewing every two to three years. Your assessment starts with three specific metrics: your current annual gross revenue, your projected revenue for the next 24 months, and the number of active clients you service. Agencies under $1.25 million in annual revenue typically carry $1 million per claim limits, while those between $10 million and $25 million average $5 million per claim. This pattern reflects actual claim patterns across the industry, not arbitrary scaling.

If you project 35 to 50 percent revenue growth, your current limits are already insufficient. Calculate your growth trajectory honestly and adjust your coverage accordingly. A solo agent expanding to a three-person team fundamentally changes your exposure profile-more staff means more transactions, more client interactions, and statistically higher probability of errors reaching clients.

Document Your Exact Service Mix

Document the specific services you provide right now: personal lines, commercial, life and health, specialty classes like contractors or wineries. Your coverage should match exactly what you sell, not what you might sell someday. Agencies that misalign their coverage with their actual service mix pay unnecessarily high premiums or carry gaps they don’t realize exist. When you approach your carrier or broker about increasing limits as you grow, accuracy in your service description prevents both overpricing and underinsurance.

Leverage Your Risk Controls for Better Rates

Your risk controls directly impact both your rates and your ability to secure higher limits. Agencies with documented client communication protocols, policy review checklists, and staff training records consistently receive better pricing than those operating informally. The data supports this: governance practices correlate directly with lower E&O claim frequency. Present your risk controls as evidence of your commitment to accuracy and client service when you request higher limits.

Prioritize Defense Costs Outside Your Limit

Defense costs outside your policy limit matter more as your revenue grows. A $2 million limit with defense costs inside the limit looks adequate until a single claim generates $250,000 in legal expenses, instantly consuming 12.5 percent of your coverage. Quality policies place defense costs outside limits, meaning your damage coverage remains intact regardless of legal costs. This structure protects your available coverage for actual damages and settlements.

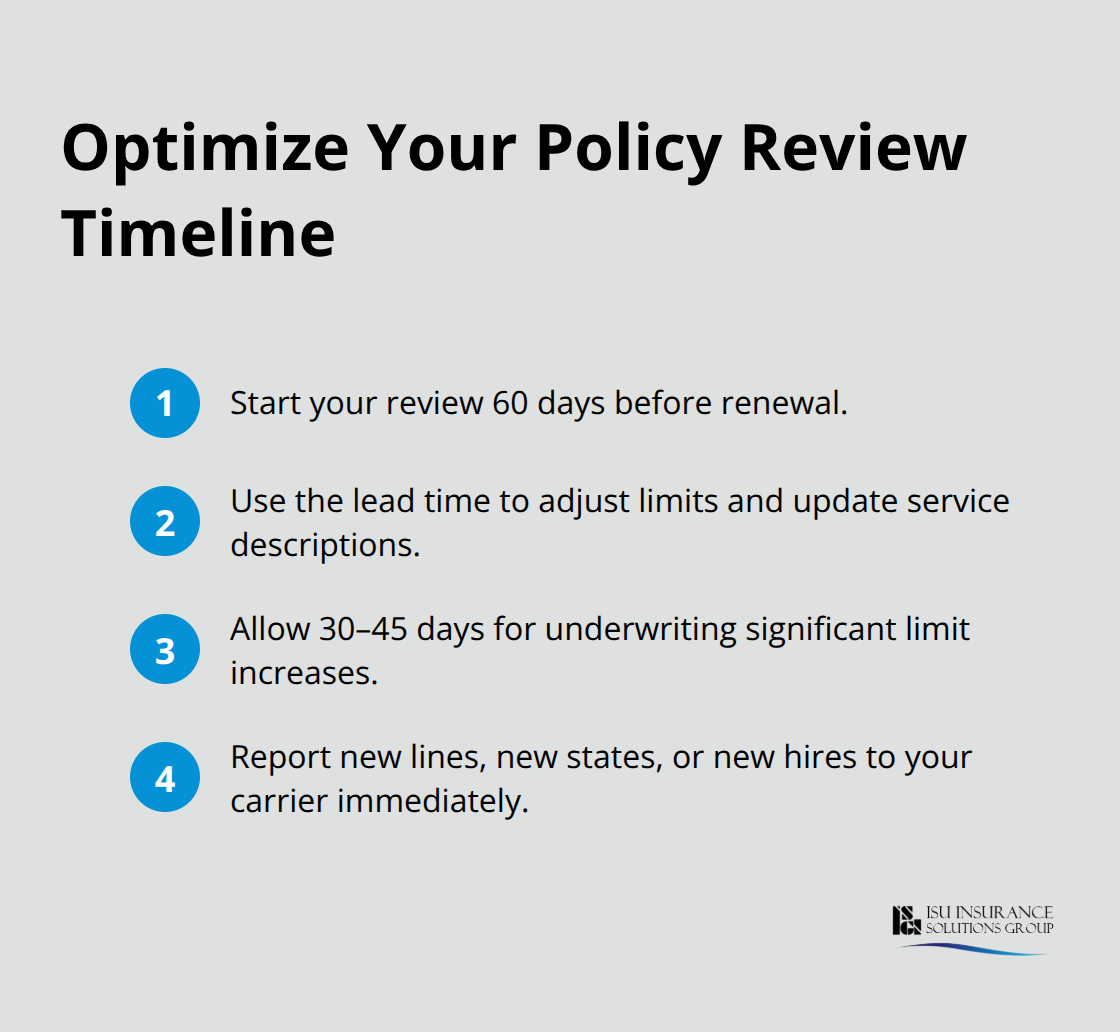

Time Your Policy Review Strategically

Schedule your policy review 60 days before renewal, not at renewal itself. This timing gives you room to adjust limits, update your service descriptions, and make coverage changes without rushing. Carriers need 30 to 45 days to underwrite significant limit increases, so starting early prevents coverage gaps when your policy renews. If you’ve added new service lines, expanded into new states, or hired staff, communicate these changes to your carrier immediately rather than waiting for renewal.

Mid-term endorsements cost less than repricing at renewal, and they prevent you from unknowingly operating outside your coverage scope.

Final Thoughts

Professional liability coverage for independent agents is not optional in today’s market. Hard market conditions, rising claim frequency, and regulatory scrutiny mean that agencies without proper coverage face serious financial and reputational risk. A single claim can drain your reserves, damage your reputation, and force closure-but agencies with documented risk controls and appropriate independent agent professional liability coverage experience significantly fewer claims and recover faster when issues arise.

Taking action means moving beyond general business insurance and securing coverage tailored to your specific operations. Your coverage needs change as your agency grows, your service mix expands, and your client base increases, so schedule a policy review now and document your current revenue alongside your projected growth. Defense costs outside your policy limit, cyber liability protection, and catastrophe expense coverage should form the foundation of your plan.

We at ISU Insurance Solutions Group understand the specific risks you face as an independent agent. Our team works with multiple carriers to deliver personalized solutions that grow with your practice, and we can help you assess your current exposure and build a professional liability strategy that protects both your agency and your clients. Contact us today to discuss your coverage needs.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.