Oregon Winery Insurance Quotes: How to Compare and Save

Oregon winery insurance quotes vary wildly depending on your operation’s size, location, and risk profile. At ISU Insurance Solutions Group, we’ve helped countless winery owners navigate these quotes and cut their premiums significantly.

The right coverage protects your vineyard, equipment, and products from real threats. This guide walks you through comparing quotes effectively and finding genuine savings.

What Coverage Do Oregon Wineries Actually Need

General Liability and Liquor Liability Protection

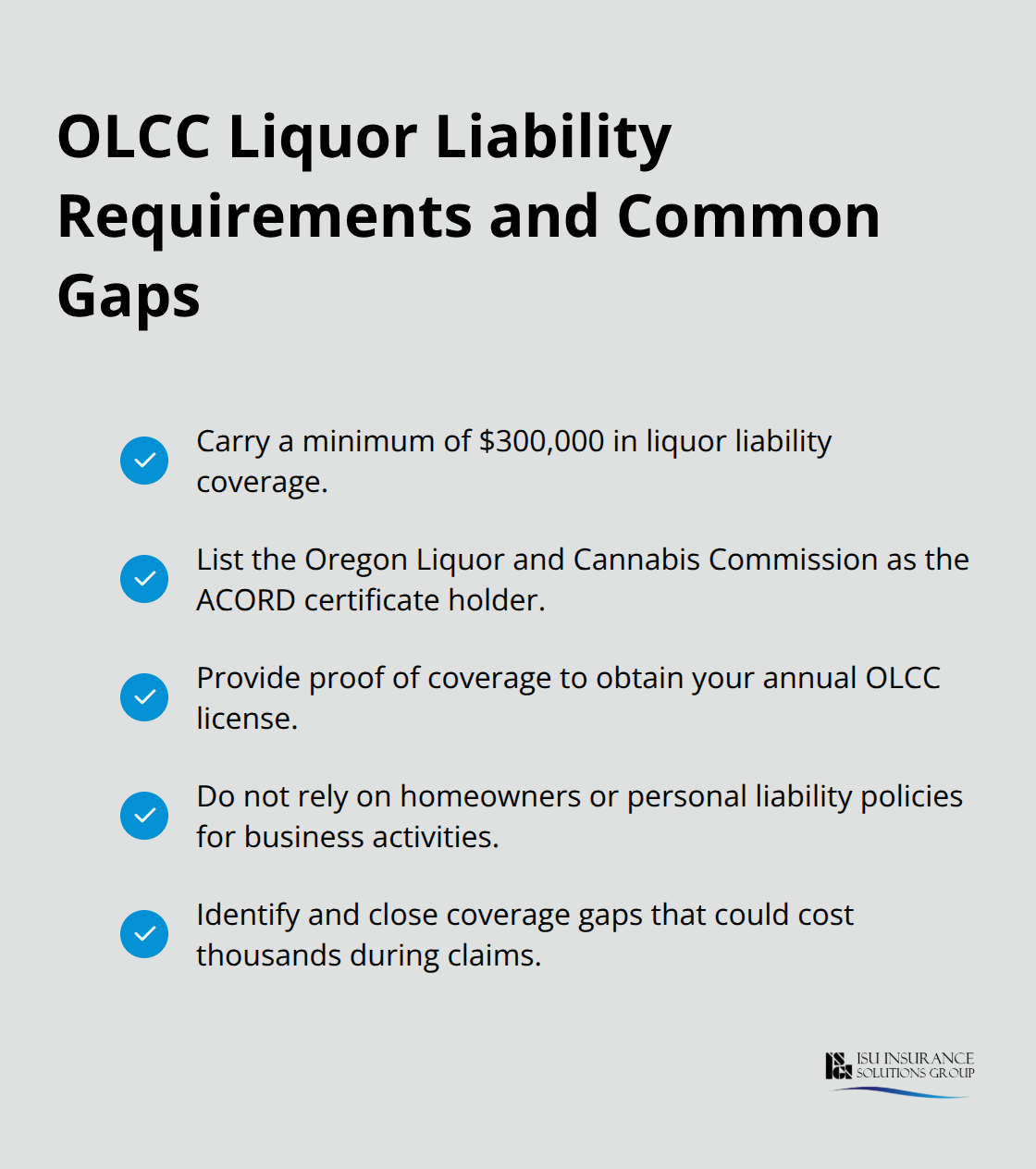

General liability protection stands as the non-negotiable foundation for any Oregon winery operation. If a customer suffers heat stroke during a vineyard tour or slips in your tasting room, general liability covers your legal defense and damages up to your policy limit. Oregon wineries with on-site tastings where consumption occurs must carry liquor liability insurance with a minimum of $300,000 in coverage, with the Oregon Liquor and Cannabis Commission named as the certificate holder on an ACORD form. This requirement appears in the OLCC licensing process, and you cannot obtain your annual license without proof of this coverage. Many winery owners mistakenly believe their homeowners or personal liability policies cover business activities-they do not.

The gap between what people think they have and what actually protects their winery operations costs owners thousands annually when claims arise.

Property and Equipment Coverage

Property and equipment coverage protects the assets that generate your revenue. Your processing buildings, fermentation tanks, bottling lines, and tasting room furniture all require commercial property insurance because standard homeowners policies exclude business property. Oregon wineries face specific threats: wildfire smoke exposure can spoil entire vintages, equipment breakdowns during harvest season can destroy crops worth hundreds of thousands of dollars, and wine stored off-site or in transit needs inland marine coverage to prevent gaps in protection.

Product Liability and Recall Insurance

Product liability and recall insurance address the reality that contaminated wine batches, labeling errors, or allergen issues can trigger lawsuits and force expensive recalls. A single recall can cost $50,000 to $500,000 depending on distribution scope, and product liability insurance covers legal fees, settlements, and recall expenses that would otherwise devastate cash flow. Oregon wineries that sell directly to consumers through tasting rooms or special event licenses face higher product liability exposure than those selling exclusively to distributors.

The coverage types that matter most depend entirely on how you operate-a vineyard selling grapes differs fundamentally from a producer hosting 15,000 annual visitors in a tasting room. Your operation’s structure, sales channels, and guest activities determine which protections you actually need. Once you understand your specific coverage requirements, the next step involves comparing quotes from multiple carriers to find the best rates and terms for your situation.

Comparing Quotes Side by Side

Gather Operational Details Before Requesting Quotes

Gathering detailed information about your winery before requesting quotes accelerates the entire process and produces more accurate comparisons. Insurance carriers need specifics: annual production volume in cases, number of employees, whether you operate a tasting room and how many visitors annually, if you host events or provide food service, what equipment you own, whether you store wine off-site, and your distribution channels (direct-to-consumer, wholesale, or both). The Oregon Liquor and Cannabis Commission requires this operational detail for licensing anyway, so you likely have most of it documented. When you request quotes, provide the same information to all carriers-inconsistent details create apples-to-oranges comparisons that waste your time.

Request Quotes from Multiple Carriers

Request quotes from at least three carriers; many Oregon wineries discover that premiums vary by $2,000 to $5,000 annually for identical coverage simply because carriers price risk differently. Contact each carrier with the same operational details to ensure fair comparison. As an independent agency serving Washington and Oregon since 1983, ISU Insurance Solutions Group works with 20+ carriers and can provide multi-carrier quotes through a single contact point, eliminating the legwork of reaching out to multiple agencies separately.

Evaluate Coverage Limits and Deductibles

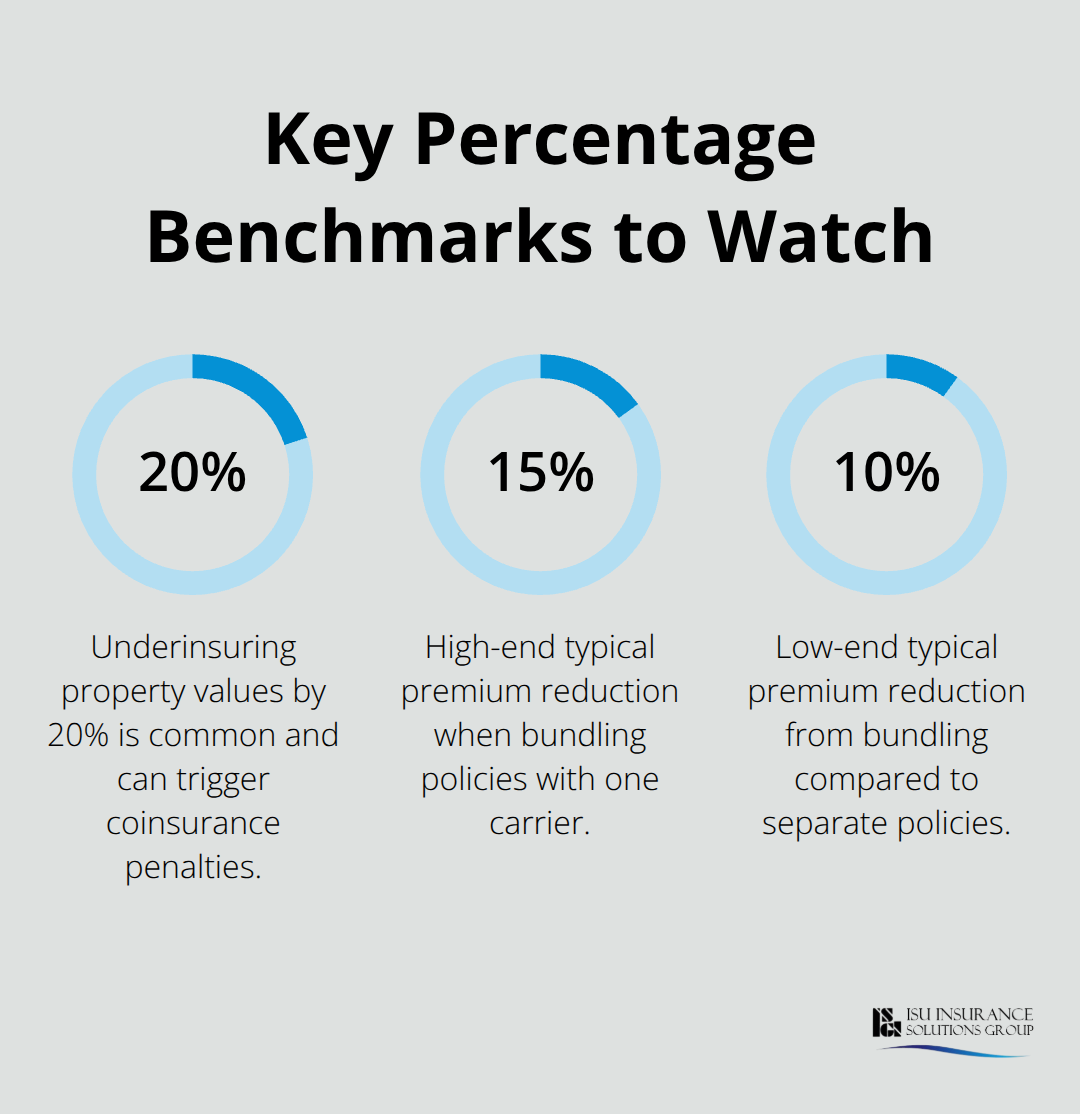

When evaluating quotes side by side, focus on three specific elements beyond premium price. First, verify that liquor liability meets the $300,000 OLCC minimum and that the policy actually covers your specific operations-some policies exclude special events or off-premises tastings, creating dangerous gaps. Second, compare property coverage limits against your actual equipment and building values; underinsuring by 20% is common, and it triggers coinsurance penalties when you file a claim, meaning the carrier pays less than you expect. Third, examine deductibles carefully: a $2,500 deductible saves perhaps $300 annually on premium but costs significantly more if you need coverage, so balance this based on your cash reserves and risk tolerance.

Verify Complete Coverage in Your Quotes

Check whether quotes include product liability and recall coverage, as many standard policies exclude these entirely-you must add them separately, and quotes that omit them appear cheaper but leave you exposed. Request ACORD certificates from carriers before committing; this verifies they can meet OLCC requirements in the format Oregon requires. Most carriers cannot bind or modify policies online, so speak with a licensed representative who can explain coverage gaps specific to your operation rather than relying on automated quote systems. Once you’ve selected the right coverage and carrier, the real opportunity to reduce costs emerges through strategic bundling and operational risk management practices.

How to Cut Your Winery Insurance Costs Without Sacrificing Coverage

Bundle Policies for Immediate Savings

Consolidating your general liability, property, and product liability policies with a single carrier typically reduces your annual premium by 10 to 15 percent compared to purchasing each policy separately. Oregon wineries that consolidate coverage often discover they can afford higher coverage limits at lower total cost than they paid for minimal coverage across multiple carriers. When you request quotes, ask each carrier for bundled pricing on general liability plus property plus liquor liability, then compare the total package price rather than individual policy costs. Some carriers offer additional discounts for bundling commercial auto insurance if your winery operates delivery vehicles. The real trap occurs when winery owners chase the cheapest individual quote without calculating the bundled total-you may select a carrier offering the lowest general liability rate only to discover their property coverage costs significantly more than a competitor’s bundled package.

Implement Risk Management Practices That Carriers Reward

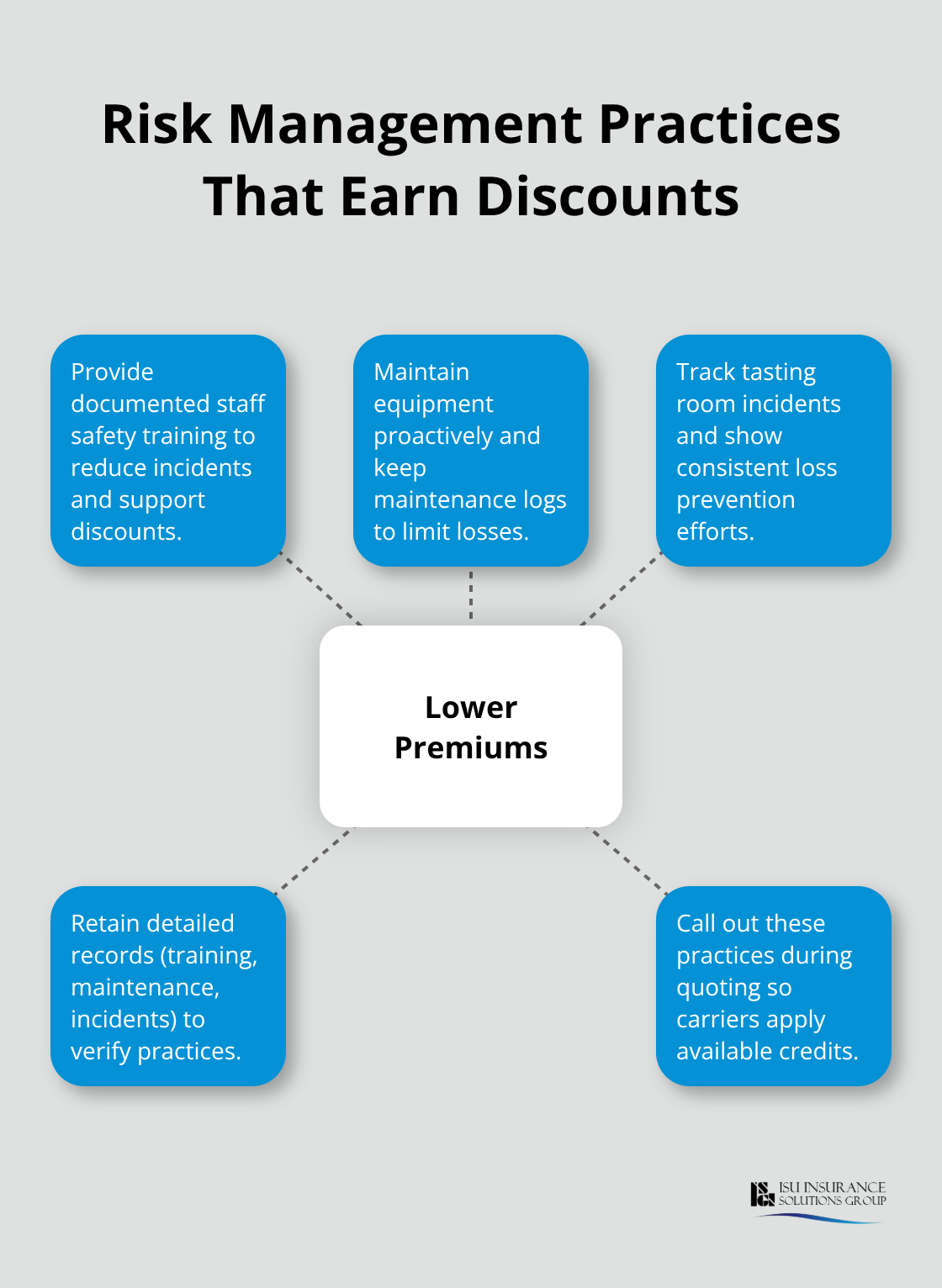

Risk management practices directly influence your insurance costs because carriers adjust premiums based on your operational safety record and loss history. Wineries that implement documented safety training for staff, maintain equipment regularly, and track visitor incidents typically qualify for safety discounts ranging from 5 to 20 percent depending on the carrier and your specific practices. Document everything: maintenance logs for fermentation tanks and bottling equipment, staff training records for food safety and alcohol service, incident reports from your tasting room, and any loss prevention improvements you’ve made. When requesting quotes, mention these practices explicitly because many carriers do not automatically apply discounts unless you highlight your risk management efforts.

Carriers want to see that you take safety seriously, and your documentation proves it.

Review and Adjust Coverage Annually

Review your coverage annually, particularly after operational changes like expanding your tasting room capacity, adding a special event license, increasing production volume, or hiring additional staff-each change shifts your risk profile and creates coverage gaps or opportunities for cost reduction. Oregon wineries that wait three to five years between policy reviews often discover they are either dramatically overinsured in areas where risk has decreased or dangerously underinsured in areas where operations have expanded. Request updated quotes every two years minimum, and request them immediately whenever your operation changes significantly. This approach (combined with the bundling and risk management strategies above) positions you to capture savings while maintaining the protection your winery actually needs.

Final Thoughts

Your winery’s insurance costs depend on five concrete factors: annual production volume, employee count, tasting room operations and annual visitor numbers, distribution channels, and documented safety practices. A small vineyard selling exclusively to distributors pays substantially less than a producer hosting 15,000 annual visitors with on-site consumption and special event licenses. Location matters too-Oregon wineries in wildfire-prone regions face higher property insurance costs due to smoke exposure and equipment loss risks.

Working with a local agent who understands Oregon’s specific regulatory environment transforms Oregon winery insurance quotes from confusing to actionable. An agent familiar with OLCC requirements verifies your liquor liability coverage meets the $300,000 minimum in the exact ACORD format Oregon requires, preventing licensing delays and coverage gaps. Local agents know which carriers price Oregon winery operations competitively and identify coverage gaps that online quote systems miss.

Your next step is straightforward: gather your operational details, request quotes from multiple carriers, and compare coverage limits and deductibles side by side rather than chasing the lowest premium. Contact ISU Insurance Solutions Group for a multi-carrier quote that eliminates the legwork of reaching out to separate agencies. A licensed representative will explain your specific coverage needs, identify cost-saving opportunities through bundling, and answer questions about OLCC requirements and Oregon-specific risks.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.