Small Winery Insurance: Scalable Coverage for Growing Wineries

Small winery insurance isn’t a luxury-it’s a necessity. Wine production carries distinct risks that standard business policies simply don’t cover, leaving your operation exposed.

At ISU Insurance Solutions Group, we’ve seen too many growing wineries operate with gaps in their protection. The right coverage strategy grows with your business, protecting your vineyard, equipment, inventory, and liability exposure at every stage.

Why Your Winery Faces Risks Standard Policies Won’t Cover

Wine production creates exposures that generic business insurance simply ignores. A guest gets sick after your tasting event, and your standard general liability policy denies the claim because it excludes alcohol service. Your fermentation tanks rupture, contaminating soil and groundwater, but your property policy has no pollution coverage. Your bottled inventory spoils during a temperature fluctuation, yet your standard commercial property coverage doesn’t account for wine-specific losses. These aren’t hypothetical scenarios-they reflect real gaps that leave growing wineries financially exposed.

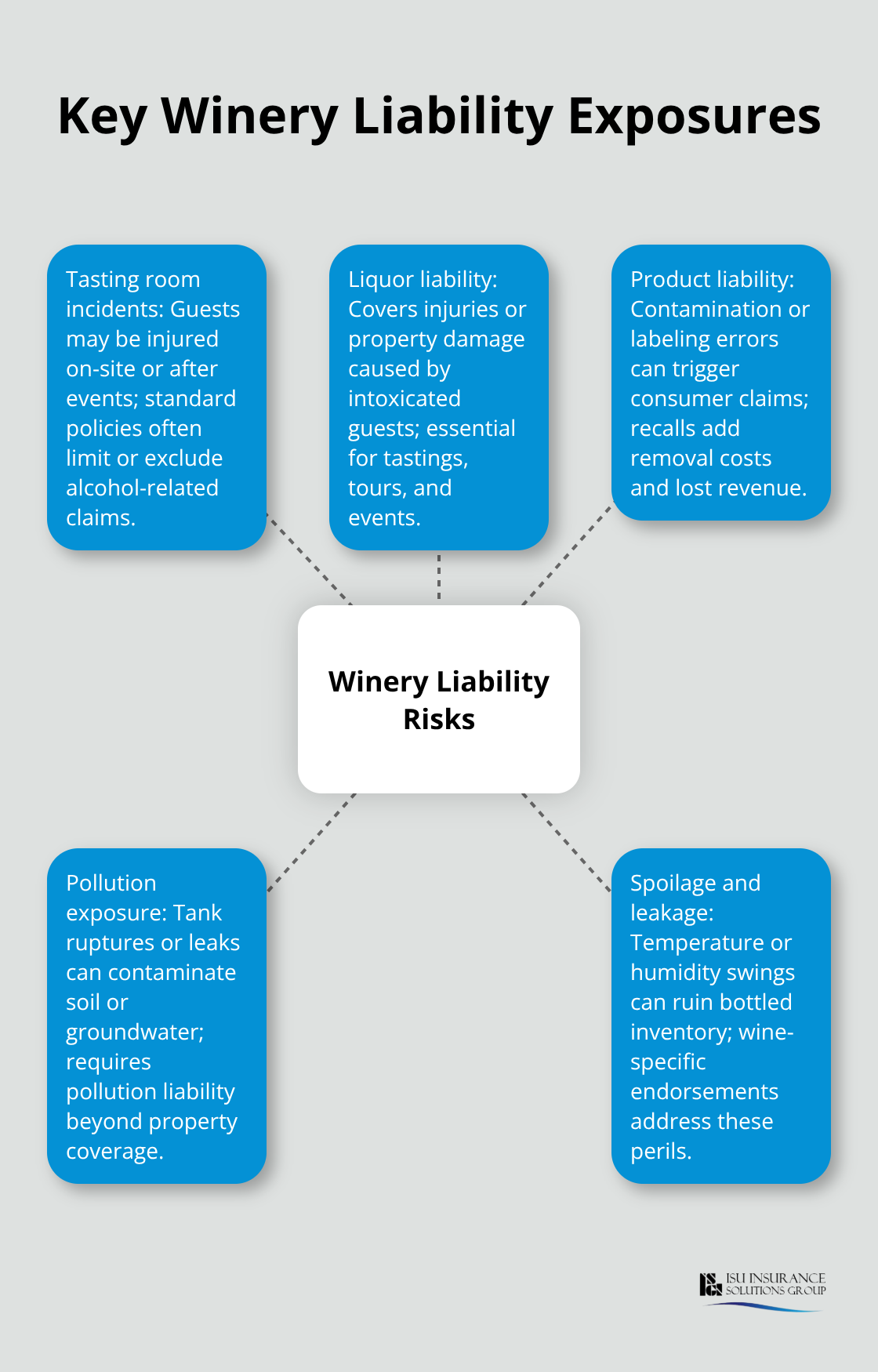

Wine Production Introduces Specific Liability Exposures

The U.S. Bureau of Labor Statistics reported 1,600 nonfatal injuries and illnesses in wineries during 2023, with approximately 900 resulting in missed workdays or job transfers. Your tasting room and events create third-party liability risks that standard policies exclude or severely limit.

Liquor liability coverage protects against claims from guests who consume your wine and suffer injury or property damage afterward-this protection is non-negotiable. Product liability becomes critical when you consider that wine contamination, labeling errors, or allergenic ingredients can trigger consumer claims. A single product recall costs thousands in removal expenses and lost revenue, which standard property policies won’t cover. Wine-specific endorsements address contamination, leakage, and spoilage from temperature or humidity fluctuations because standard coverage treats wine as generic inventory and excludes these wine-specific perils.

Equipment and Vineyard Assets Require Tailored Protection

Your crushers, destemmers, fermentation tanks, bottling lines, and aging barrels represent significant capital investment. Standard commercial property policies cover buildings and equipment, but they often exclude or undervalue wine production equipment because underwriters lack agricultural expertise. Newly acquired or replacement vineyard equipment receives automatic coverage up to $100,000 for 60 days under specialized winery programs, but once that grace period expires, gaps emerge if your policy wasn’t specifically designed for viticulture operations. Vineyard land itself varies dramatically in value-Napa land ranges from $150,000 to $500,000 per hectare depending on location and reputation-making accurate property valuation critical for replacement cost coverage. Your wine inventory also requires specialized handling because market price volatility affects asset values significantly.

Why General Agents Miss Wine-Specific Needs

A general commercial agent often defaults to undervalued or misaligned limits because they lack winery expertise. Specialized insurance partners understand that wine production equipment operates differently than standard manufacturing equipment and that vineyard operations face unique seasonal and environmental risks. An independent agency with deep experience in wine industry coverage (like ISU Insurance Solutions Group, which serves Washington and Oregon wineries through partnerships with multiple carriers) structures protection that aligns with your actual exposures rather than generic assumptions. This expertise becomes increasingly important as your winery scales and adds new facilities, distribution channels, or event operations-each expansion introduces exposures that require thoughtful coverage adjustments.

What Coverage Do Growing Wineries Actually Need

General Liability and Product Liability Protection

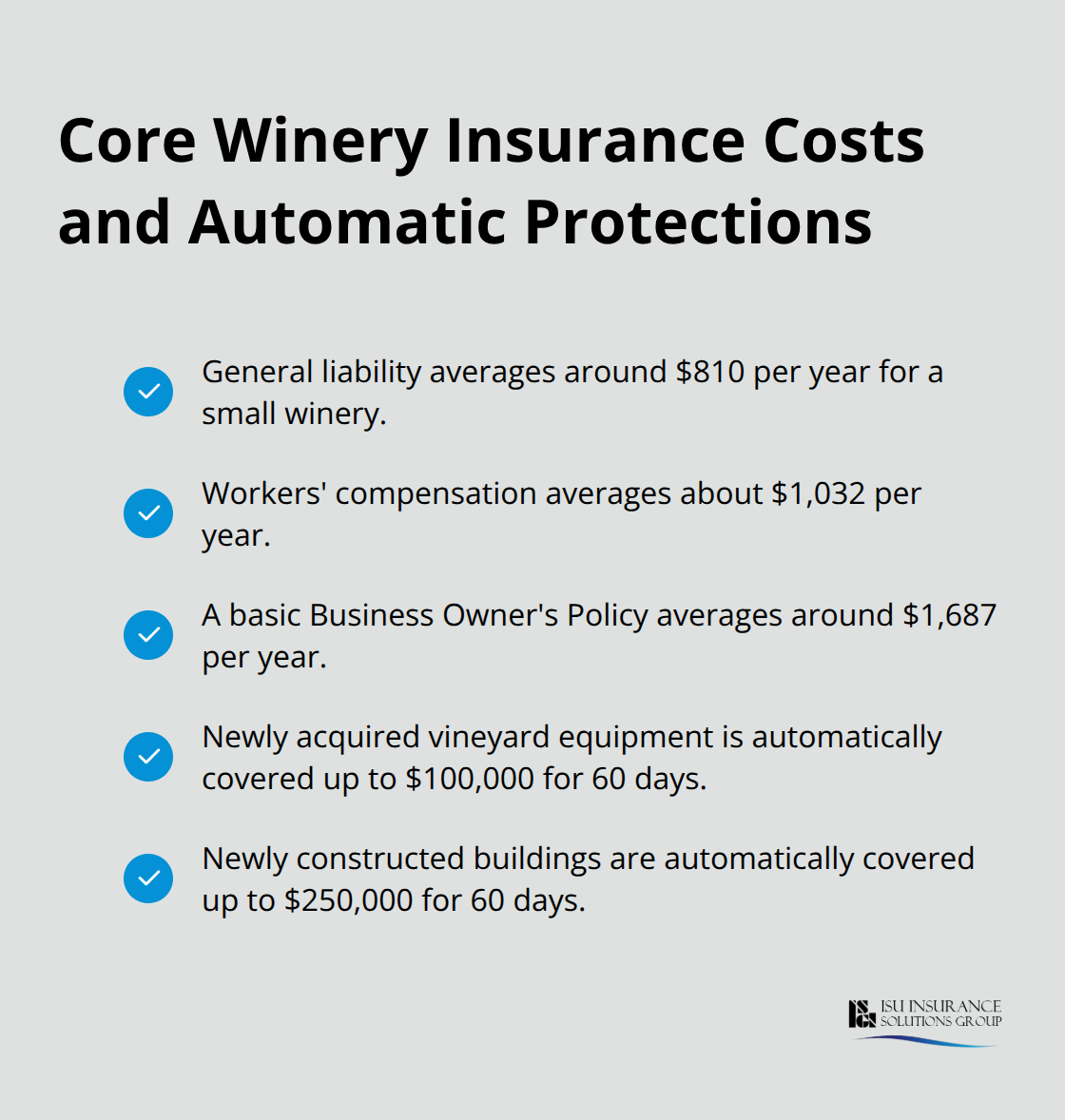

General liability protects your tasting room guests and event attendees, covering bodily injury or property damage claims that arise from your operations. The Hartford’s estimates suggest standalone general liability runs around $810 per year for a small winery, though your actual cost depends on employee count, location, and claims history.

Product liability becomes essential the moment you sell bottled wine because failure to warn or labeling errors trigger consumer lawsuits and product recalls. A single recall costs thousands in removal expenses and lost revenue that standard property policies won’t cover.

Liquor Liability and Workers’ Compensation

Liquor liability is non-negotiable if you host tastings, tours, or events where guests consume your wine. This coverage protects you when someone drinks your wine at your facility and later claims injury or property damage. Without it, your standard general liability explicitly excludes alcohol-related claims, leaving you exposed. Workers’ compensation protects your team when they suffer work-related injuries or illnesses. The Hartford’s estimates place workers’ compensation around $1,032 annually, reflecting the reality that the U.S. Bureau of Labor Statistics documented 1,600 nonfatal winery injuries in 2023, with roughly 900 causing missed workdays.

Equipment and Inventory Coverage for Wine Production

Your crushers, destemmers, fermentation tanks, bottling lines, and aging barrels require commercial property coverage specifically designed for wine production equipment. Standard policies undervalue or misclassify wine equipment because general underwriters lack agricultural expertise. Specialized winery programs automatically cover newly acquired vineyard equipment up to $100,000 for 60 days, giving you a grace period before renewal. Wine inventory coverage must account for temperature fluctuations, contamination, and leakage because standard commercial property treats wine as generic inventory and excludes these wine-specific perils.

Buildings and Business Income Protection

Your buildings, including processing facilities, warehousing, offices, and tasting rooms, receive automatic protection for newly constructed buildings up to $250,000 for 60 days under winery-specific programs. Business income coverage helps replace lost revenue after covered property damage, protecting ongoing costs like payroll and utilities during downtime. The Hartford estimates a basic Business Owner’s Policy around $1,687 annually, bundling general liability, property, and business income coverage. This bundled approach costs less than purchasing each coverage separately and eliminates gaps between policies.

Scaling Coverage as Your Winery Expands

As your winery expands, your coverage limits must increase proportionally to protect your growing assets and inventory values. An independent agency with deep winery expertise structures protection that aligns with your actual exposures rather than generic assumptions. An agent who understands Pacific Northwest winery operations can adjust your program as production increases and new facilities come online. Your next step involves working with a partner who recognizes how your coverage needs shift with each stage of growth.

How Your Coverage Limits Must Change as Production Grows

Calculate Coverage Limits Based on Production Volume

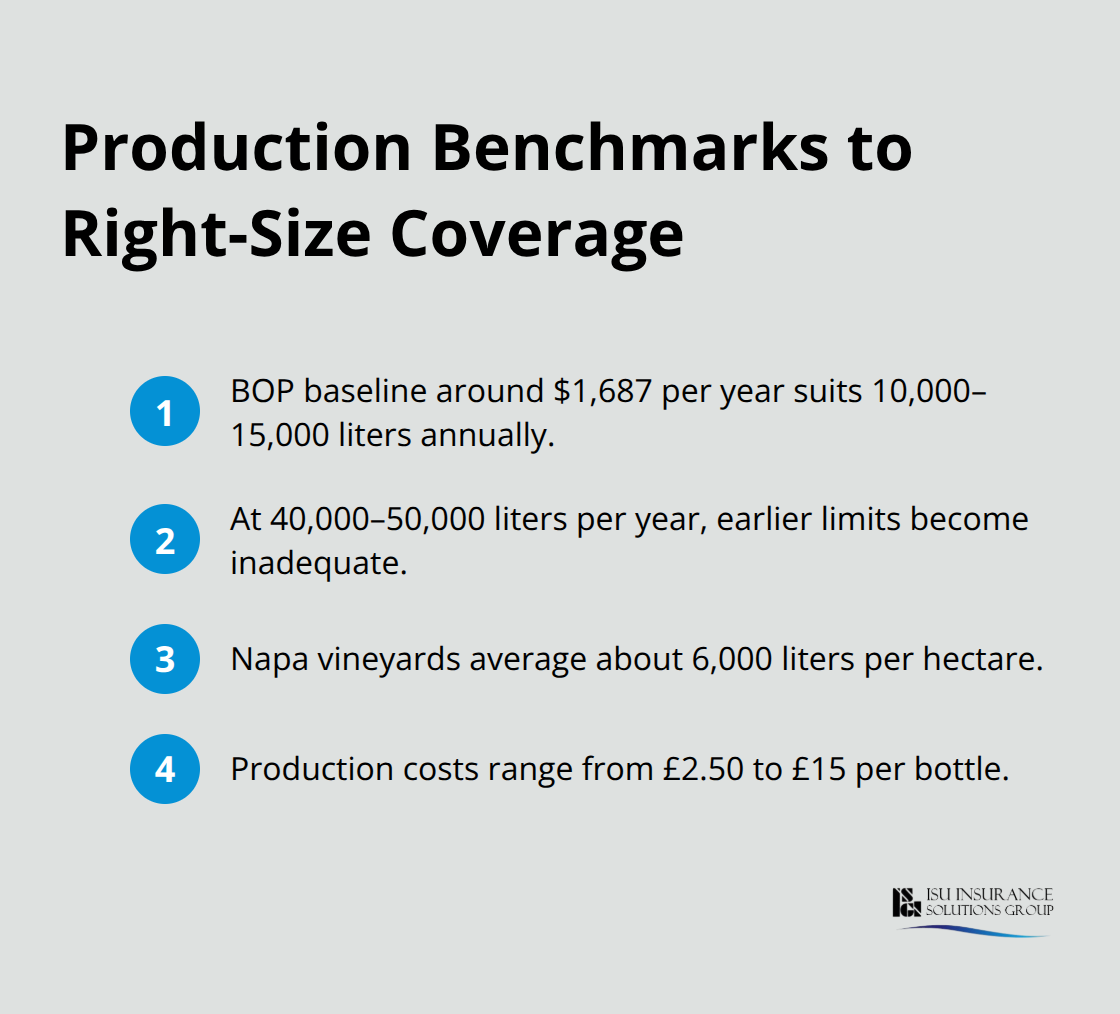

Your production volume directly determines your coverage limits, and misaligning them creates serious financial exposure. If you produce 50,000 liters annually but your property coverage only protects $150,000 in inventory, a fermentation tank failure or temperature-control malfunction wipes out uninsured wine worth tens of thousands. The Hartford’s Business Owner’s Policy baseline around $1,687 annually works for startups producing 10,000 to 15,000 liters yearly, but once you scale to 40,000 or 50,000 liters per year, those limits become dangerously inadequate.

Production yield benchmarks help calibrate realistic coverage: Napa vineyards average around 6,000 liters per hectare, and production costs range from £2.50 to £15 per bottle depending on quality tier. Use these metrics to calculate your actual inventory value at any production stage.

If you produce premium wine at the higher end of that cost range, your inventory replacement value climbs rapidly, requiring corresponding coverage increases.

Adjust Liability Limits for Tasting Room and Event Growth

General liability limits must scale with your production volume and event frequency. A tasting room hosting 20 guests monthly operates at different risk than one hosting 500 guests, and your policy limits need to reflect that exposure expansion. Equipment coverage becomes critical when you add new crushers, destemmers, or bottling lines; specialized winery programs automatically cover newly acquired vineyard equipment up to $100,000 for 60 days, but you must formalize that coverage in your renewal before that grace period expires.

Many growing wineries make the mistake of renewing policies on the same limits year after year, assuming their agent tracks production growth. That assumption costs money. Schedule a coverage review with your agent every time you add significant equipment or increase production by 25% or more.

Add Coverage for New Facilities and Distribution Channels

New facilities and distribution channels introduce exposures that standard policies do not anticipate, requiring deliberate coverage additions rather than hoping your existing policy stretches to cover them. Opening a second tasting location, launching a wine club with direct-to-consumer shipping, or adding event space for weddings and corporate tastings each triggers distinct liability and property risks.

Commercial auto coverage becomes mandatory if you operate vehicles for distribution or guest shuttles; without it, your general liability explicitly excludes vehicle-related claims. Pollution liability protection is essential if your fermentation processes, cleaning chemicals, or waste handling create environmental exposure, especially in regions with strict groundwater protection regulations.

Protect Digital Operations and Revenue Streams

Cyber liability protection becomes urgent the moment you collect customer data through online orders, reservations, or point-of-sale systems; a data breach affecting wine club members or tasting event attendees exposes you to notification costs, regulatory fines, and customer lawsuits that standard policies ignore entirely. Business interruption coverage becomes increasingly valuable as your revenue scales; if a fire or equipment failure forces a production shutdown, this coverage replaces lost income during downtime, protecting payroll and fixed costs like utilities and lease payments.

Structure a Scalable Insurance Framework

Rather than waiting for each new exposure to emerge, structure your policy around a scalable framework: start with General Liability and Property as your foundation, layer in a Package Policy that includes Business Interruption and Equipment Breakdown as production increases, then add specialized protections like Pollution Liability, Cyber Liability, and Commercial Auto as your operations expand into those areas. An independent agency with deep winery expertise structures this progression intentionally rather than reactively, adjusting your program at each growth stage so you remain properly protected without overpaying for coverage you do not yet need.

Final Thoughts

Your winery’s success depends on protecting what you’ve built at every growth stage. Small winery insurance isn’t a one-time purchase-it’s a living strategy that evolves as your production volume, facilities, and revenue streams expand. The coverage priorities remain consistent: general and product liability protect your guests and customers, property and equipment protection safeguards your physical assets, and business interruption coverage maintains cash flow when unexpected losses occur.

Working with specialists who understand wine industry risks transforms insurance from a compliance checkbox into a competitive advantage. A general commercial agent applies standard business templates that miss wine-specific exposures like fermentation contamination, temperature-controlled inventory loss, or liquor liability exclusions. Specialists recognize that your crushers and fermentation tanks operate differently than standard manufacturing equipment, that your vineyard land carries unique valuation challenges, and that your revenue streams span direct sales, distribution, events, and wine tourism-each requiring distinct coverage considerations.

At ISU Insurance Solutions Group, we’ve served Washington and Oregon wineries since 1983, building deep expertise in the exposures your operation faces. Our independent agency partnerships with multiple carriers mean we can deliver tailored quotes aligned to your specific production volume, facilities, and growth trajectory. Contact ISU Insurance Solutions Group to discuss how scalable small winery insurance protects your vineyard, equipment, inventory, and revenue as you grow.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.