Commercial Auto Rates: How to Find the Best Value

Commercial auto rates vary wildly depending on your vehicle, drivers, and business type. Most business owners overpay because they don’t understand what actually moves the needle on their premiums.

We at ISU Insurance Solutions Group help companies cut through the noise and find real savings. This guide walks you through the factors that matter, how to compare quotes properly, and concrete tactics to lower what you pay.

What Actually Moves the Needle on Your Commercial Auto Rates

Vehicle Type and Usage Shape Your Baseline

Vehicle type sits at the top of the rate-setting pyramid, and insurers price it ruthlessly. A box truck carrying general cargo costs far less to insure than a food truck with specialized equipment, which can drive premiums up 20–30% according to industry data. Heavy-duty vehicles like dump trucks or cement mixers face even steeper costs because they operate in high-risk environments. How you use that vehicle matters just as much. Delivery fleets need higher liability limits because drivers spend more time on the road, exposing the business to greater accident risk. Transporting hazardous materials or passengers kicks rates even higher.

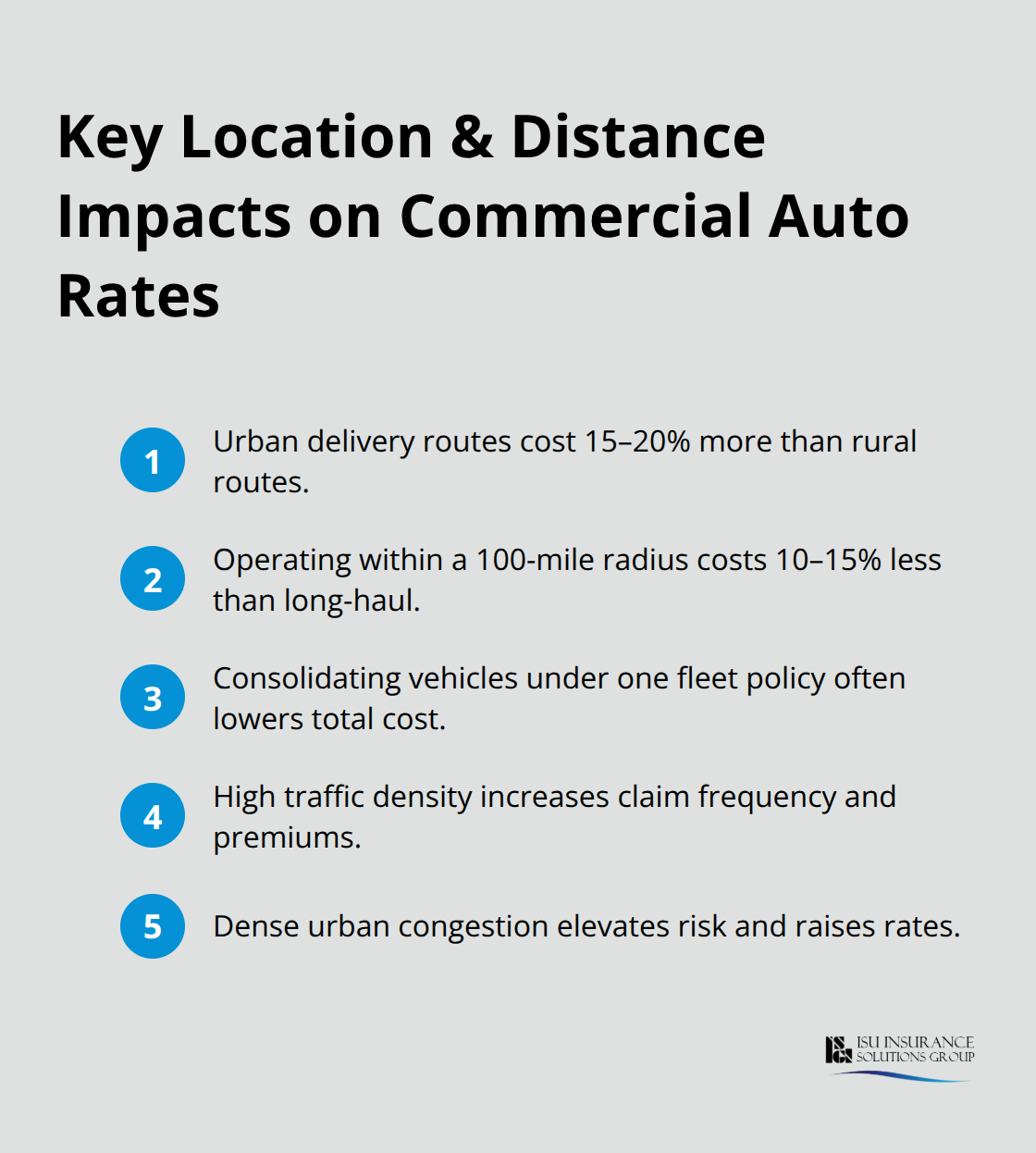

Location and distance traveled directly affect what you pay. Urban delivery operations pay 15–20% more than rural routes, simply because congestion and traffic density create more claim opportunities. A fleet running within a 100-mile radius pays 10–15% less than long-haul operations. If you operate two vehicles versus one, fleet insurance often beats buying two separate commercial auto policies, so consolidating under one carrier makes financial sense.

Driver History Determines Half Your Premium

Your worst drivers cost you the most. A single accident or violation can lock in higher rates for years, while clean driving records can reduce premiums compared to fleets with violations or claims. Industry data shows that having no insurance claims in the past three years saves up to 30% on premiums versus fleets with multiple claims. Younger drivers aged 18–25 carry higher crash risk and require targeted training to offset their premium impact.

Hire drivers with clean licenses and notify insurers immediately of any penalty points. Formal driver training programs reduce driver risk, and some insurers offer discounts when they recognize the training provider. Telematics devices that monitor driving behavior can cut premiums around 15%, giving you data-backed proof that your safety investments work. Dash cams and in-cab cameras defend against fraudulent claims and reveal dangerous behavior for coaching, making them worth the investment.

Industry Type and Mileage Create the Baseline

Construction and transportation sit at the high end-premiums run up to 30% higher than low-risk industries. According to Insureon data, industry monthly averages vary significantly: auto services average about $69, while construction and contracting average $173, and IT or technology services average $198. Your annual mileage directly correlates with claims frequency. More time on the road means more exposure to accidents and incidents.

Vehicle age influences your rate substantially. Vehicles with recent model years benefit from advanced safety features and better security systems, which can reduce premiums. Older vehicles, especially those without modern anti-lock brakes or airbags, cost more to insure. Maintenance habits matter too-well-maintained fleets avoid breakdowns that create incidents and raise premiums. Secure overnight parking at depots or with robust locking systems lowers theft risk and insurance costs.

Understanding these three factors gives you the foundation to shop effectively. The next step involves gathering quotes from multiple carriers and comparing them side by side to identify where real savings hide.

How to Compare Commercial Auto Quotes from Multiple Carriers

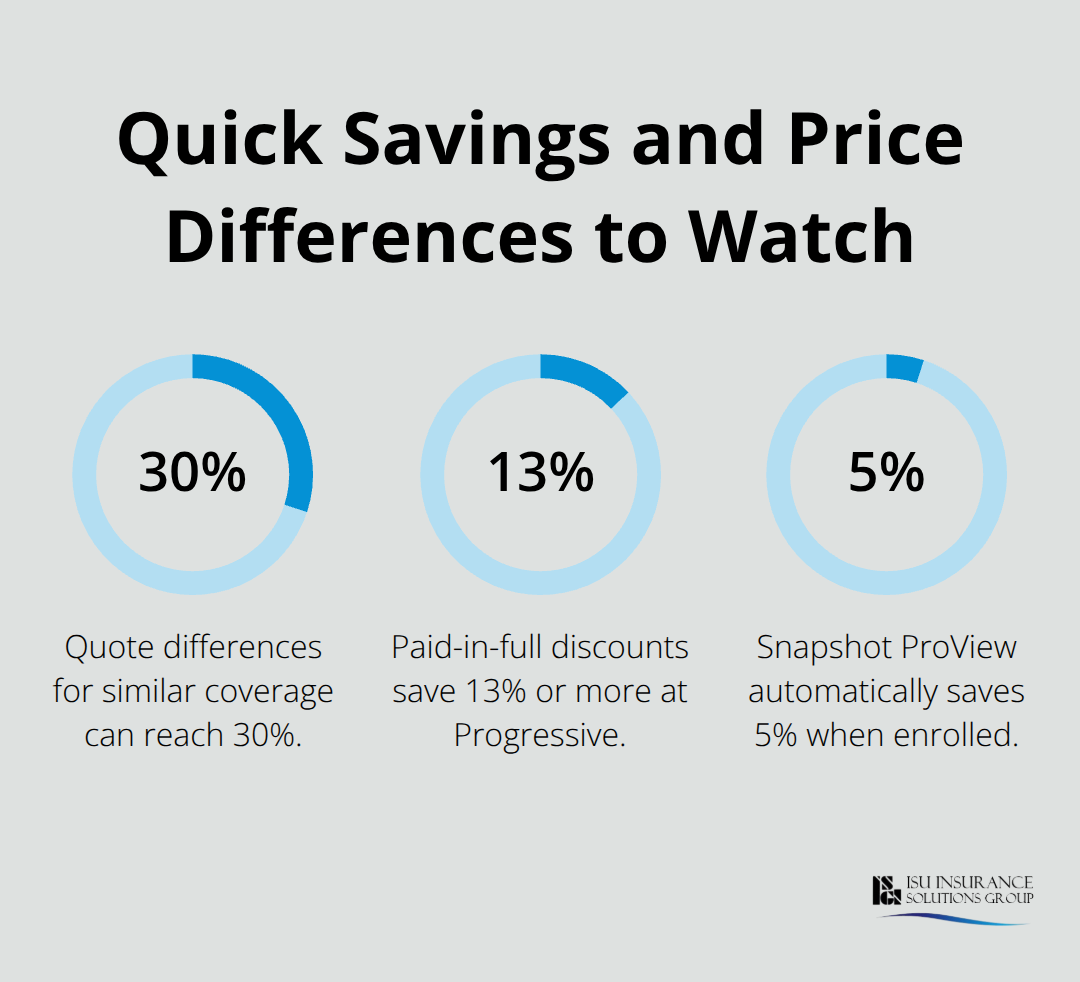

Collecting quotes from different insurers is non-negotiable if you want real savings. Quote differences for similar coverage can reach 30%, meaning the carrier you choose matters far more than the coverage level you select. Most business owners request one or two quotes and stop, leaving thousands of dollars on the table. You should request quotes from at least three to five carriers within 24 hours, which is the standard turnaround time. Progressive offers customized quotes online or by phone, while independent agencies access 20+ carriers through one application, eliminating the need to contact each insurer separately.

This matters because comparing quotes manually wastes time and guarantees you’ll miss options.

Focus on Coverage Differences, Not Just Price

When you evaluate quotes, focus on what changes between them rather than staring at the bottom-line premium. Two quotes at $150 and $180 per month look different until you realize one includes comprehensive and collision coverage while the other only covers liability. Liability limits vary too-one carrier might quote $100,000 per accident while another assumes $300,000, which shifts the entire risk picture. Delivery fleets need higher liability limits than construction crews, so you should align each quote’s coverage to your actual operation.

Bundling commercial auto with general liability or property insurance yields discounts, sometimes reaching significant savings on total costs. You should ask each carrier what bundling savings apply before comparing standalone auto rates. Higher deductibles reduce premiums by 10–20%, but only increase your deductible if you can actually cover that amount out-of-pocket after a claim. A $1,000 deductible saves money monthly but costs you significantly if you need to file a claim within weeks of switching.

Select Coverage That Matches Your Operation

Core coverages-liability, collision, comprehensive, uninsured motorist, and medical payments-form the foundation, but your industry dictates what matters most. Hazmat transporters need pollution liability that general cargo haulers skip entirely. Food delivery operations face different exposure than construction material haulers. You should avoid paying for coverage you’ll never use, but don’t strip coverage just to hit a lower premium. If your fleet includes older vehicles worth less than $5,000 each, dropping comprehensive coverage on those units saves money without meaningful risk.

Progressive’s Snapshot ProView program automatically saves 5% when enrolled, and fleets with three or more vehicles access free fleet management tools at no extra cost. This data-driven pricing means your actual driving behavior influences rates at renewal, so premiums can rise or fall based on telematics results.

Stack Discounts to Maximize Savings

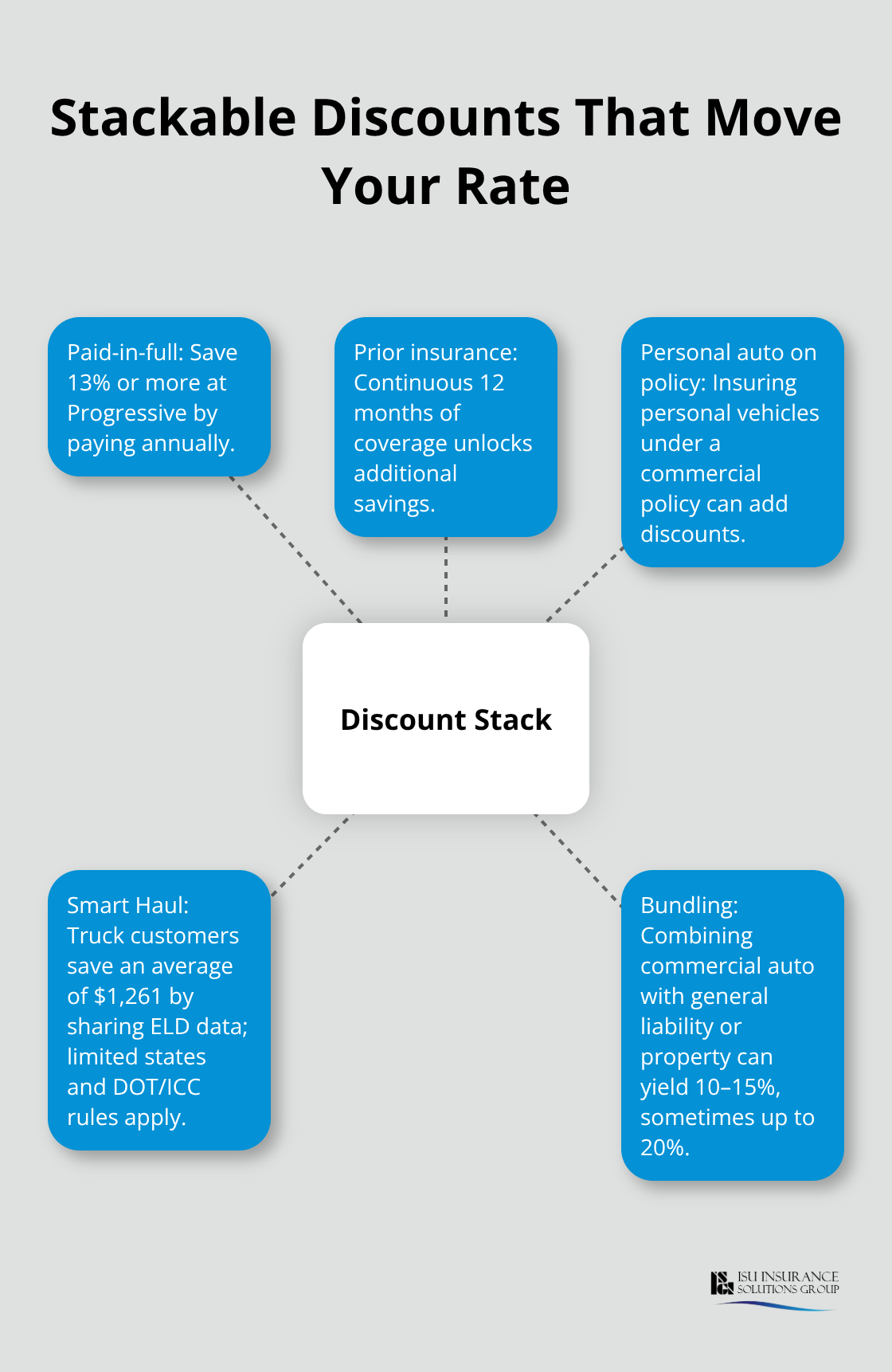

Paid-in-full discounts save 13% or more for most customers at Progressive, making annual payments smarter than monthly installments if your cash flow allows it. Prior insurance savings reward continuous coverage-maintaining insurance for the last 12 months qualifies you for additional discounts. Personal auto discounts apply if you insure your personal vehicles under a commercial policy. Smart Haul programs for truck customers save an average of $1,261 on premiums by sharing electronic logging device data, though this program doesn’t operate in all states and requires DOT filing with ICC.

These discounts compound when stacked, turning a $200 monthly quote into something far more competitive. Independent agents negotiate carrier-specific discounts you won’t find online, making professional guidance worth the conversation. Once you’ve identified your best quote and locked in discounts, the real work begins-implementing the safety and maintenance strategies that keep your rates from climbing at renewal.

How to Cut Your Premium Without Cutting Coverage

Safety Programs and Driver Training Deliver Real Returns

Safety programs and driver training produce measurable returns that most fleet operators overlook. A formal driver training program costs $200–$500 per driver annually, but insurers recognize these programs and offer discounts that recover that investment within months. Telematics devices that monitor driving behavior cut premiums around 15% on average, and dash cams provide fault evidence that defends against fraudulent claims while revealing dangerous driving patterns you can address through coaching.

Roughly 10–15% of any fleet drives recklessly and inflates your rates disproportionately. Identify your worst drivers through telematics data, then invest in targeted mentoring or consider separate policy options that contain their premium impact. Progressive’s Smart Haul program saves truck customers an average of $1,261 annually by sharing electronic logging device data, though this requires DOT filing with ICC and operates only in select states. Data-backed safety improvements aren’t optional expenses-they’re rate reductions disguised as operational costs.

Bundling and Payment Strategies Cut Costs Immediately

Bundling commercial auto with general liability or property insurance yields 10–15% discounts on total costs, sometimes reaching 20%, making this the fastest path to immediate savings. Paid-in-full discounts save 13% or more at Progressive when you pay your annual premium in one lump sum instead of monthly installments. Prior insurance savings reward continuous coverage over the past 12 months, which means switching carriers for a lower quote costs you this discount at your new insurer unless you maintain coverage without gaps.

Fleet Maintenance and Parking Lower Your Risk Profile

Fleet maintenance directly affects premiums because well-maintained vehicles avoid breakdowns that create incidents and trigger rate increases at renewal. Secure overnight parking at depots with robust locking systems lowers theft risk substantially, and insurers adjust rates downward for fleets that demonstrate this commitment. These operational practices signal to carriers that you manage risk seriously.

Deductibles and Policy Reviews Optimize Coverage

Higher deductibles reduce premiums by 10–20%, but only increase yours if you can actually cover that amount after a claim-a $1,000 deductible saves money monthly but becomes expensive if you file a claim within weeks. Schedule annual policy reviews to adjust coverage as your fleet and operations change, avoiding over-insurance on older vehicles while maintaining adequate protection on newer units. An independent agent provides access to multiple carriers through one application, eliminating the manual legwork of contacting each insurer separately while negotiating carrier-specific discounts you won’t find online.

Final Thoughts

Finding real value in commercial auto rates requires three concrete actions: understanding what moves your premiums, comparing quotes across multiple carriers, and implementing safety strategies that stick. Most business owners pay too much because they treat insurance as a one-time purchase rather than an ongoing negotiation. Your vehicle type, driver history, and industry baseline set the foundation, but bundling policies, raising deductibles strategically, and investing in telematics can cut your costs by thousands annually without sacrificing protection.

The gap between your current rate and what you should pay often reaches 30% or more. That difference disappears only when you request quotes from at least three to five carriers within 24 hours and compare coverage side by side rather than chasing the lowest number. Paid-in-full discounts, prior insurance savings, and multi-product bundling compound quickly when stacked together, and safety programs deliver measurable returns that offset their costs within months through premium reductions.

Contact ISU Insurance Solutions Group today to start comparing quotes and lock in real savings on your commercial auto rates. Our local agents understand Pacific Northwest risks and can secure quotes that reflect your actual exposure. Whether you run a construction fleet, delivery operation, or specialized transport business, we partner with 20+ carriers to deliver competitive rates tailored to your operation.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.