Washington Brewery Liability Coverage: What It Means for Craft Brewers

Washington brewery liability coverage isn’t optional-it’s a business necessity. Standard commercial insurance policies leave craft brewers exposed to risks that come with serving alcohol and operating a production facility.

At ISU Insurance Solutions Group, we’ve seen breweries face claims they never anticipated. The right coverage protects your taproom, your product, and your bottom line.

Why Brewery Operations Face Risks Standard Policies Won’t Cover

Equipment Failures Trigger Losses Standard Coverage Excludes

Brewing isn’t like running a typical retail business, and your insurance needs to reflect that reality. A standard commercial general liability policy treats your brewery the same way it treats an office or retail shop-which means massive coverage gaps the moment fermentation starts. Equipment breakdown claims rank among the costliest losses breweries face, yet general liability policies exclude mechanical and electrical failures entirely. When a glycol system fails and destroys thousands of dollars in inventory, or a boiler malfunction shuts down production for weeks, standard coverage leaves you exposed.

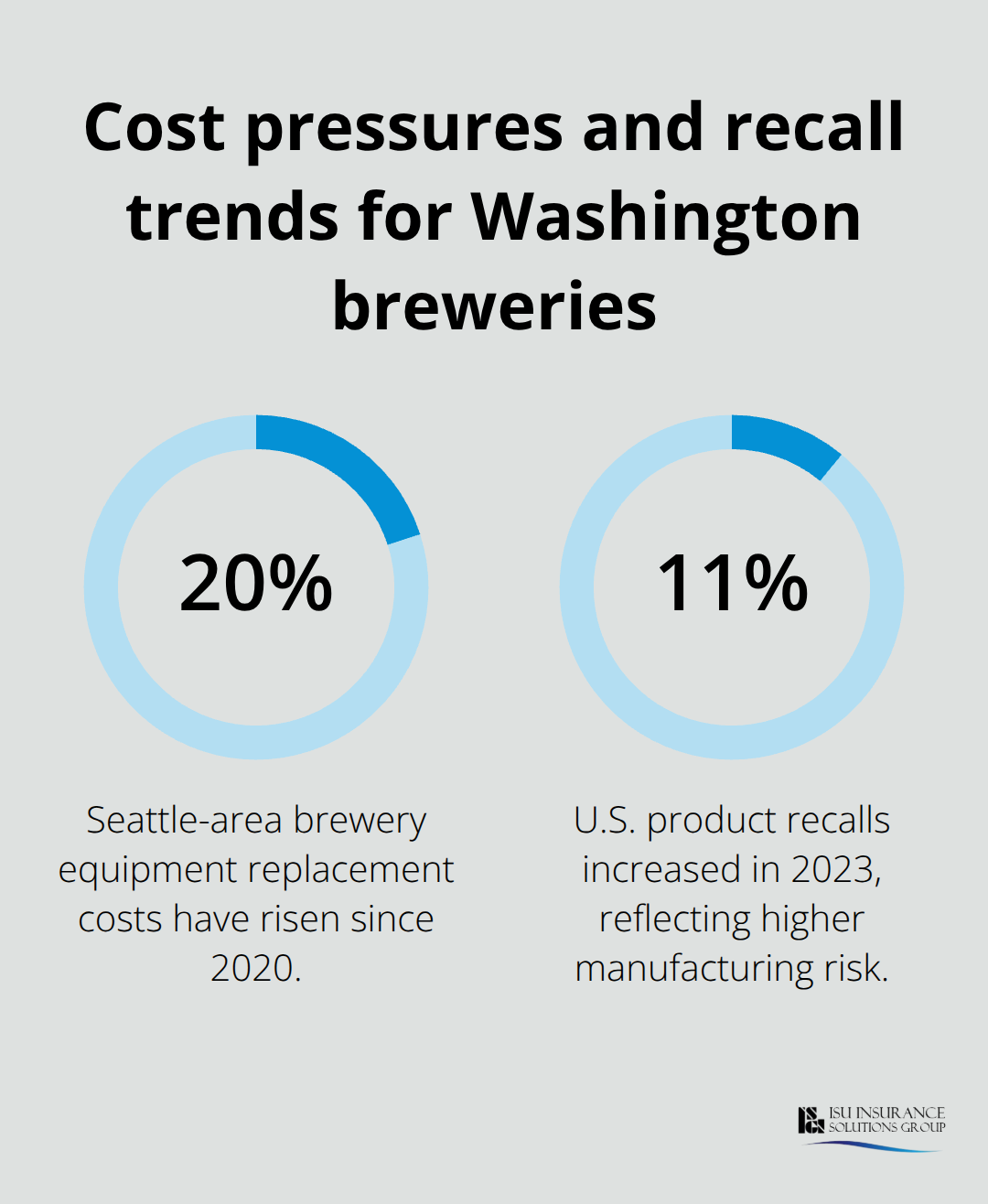

Replacement costs in the Seattle area have risen roughly 20% since 2020, so a tank or chiller that cost $50,000 five years ago now costs $60,000 to replace. Temperature control failures are relentless in Washington’s climate. One power outage or refrigeration breakdown can spoil entire batches of finished beer or raw ingredients. Spoilage coverage isn’t standard-it’s a specialized endorsement that reimburses destroyed inventory, disposal fees, and lost production time.

Without it, a single incident wipes out months of profit.

Alcohol Service Creates Legal Exposures Standard Policies Exclude

Washington’s Liquor and Cannabis Board requires minimum $1,000,000 in Commercial General Liability coverage for licensing, but that’s just the baseline. The real exposure comes from alcohol-related incidents, which standard policies explicitly exclude. If a customer suffers injury at your taproom after consuming alcohol, or if someone leaves your premises intoxicated and causes harm to a third party, your general liability policy won’t cover it. That’s where liquor liability and dram shop coverage becomes non-negotiable. These policies protect against assault-and-battery claims, over-service incidents, and third-party bodily injury claims tied to alcohol consumption.

Many brokers recommend at least $2 million in combined single limits for breweries hosting tours or events. Tasting rooms that function as event spaces for festivals, weddings, or concerts face even higher exposure. Each event multiplies your liability footprint. Assault-and-battery sublimits are critical for on-premises incidents. If a customer suffers injury in an altercation at your taproom, your standard general liability won’t touch it.

Product Liability and Recalls Demand Specialized Protection

Product liability and recall protection rounds out the picture. The Brewers Association reported that US product recalls rose 11% in 2023, the largest jump in seven years. If contamination or foreign material reaches market, recall costs-product destruction, freight, retailer chargebacks, and legal defense-can exceed six figures. Standard policies don’t cover any of it. Multi-state distribution under the Three-Tier System amplifies this risk. One contaminated batch shipped across state lines turns a local incident into a multi-state nightmare.

These three coverage gaps-equipment breakdown, alcohol-related liability, and product recall exposure-form the foundation of what separates brewery insurance from standard commercial policies. The next section examines each coverage type breweries actually need and how they work together to protect your operation.

The Three Coverage Pillars Every Washington Brewery Needs

General Liability Forms Your Foundation-But It’s Not Enough

General liability forms the foundation, but it’s insufficient on its own. Washington’s Liquor and Cannabis Board mandates minimum $1,000,000 in Commercial General Liability coverage before you receive a license, yet this baseline covers only bodily injury and property damage from standard premises incidents. The moment alcohol enters the equation or equipment malfunctions occur, gaps emerge. Industry brokers familiar with Washington operations recommend $2 million in combined single limits for breweries hosting tours or events. Your general liability policy protects against slip-and-fall injuries in your taproom or brewery, customer property damage, and advertising injury claims. However, it explicitly excludes mechanical failures, alcohol-related bodily injury, and product contamination.

Liquor Liability Protects Against Alcohol-Service Claims

Liquor liability and dram shop coverage fills the alcohol gap by protecting against claims arising from over-service, assault-and-battery incidents at your taproom, and third-party injuries caused by intoxicated customers who left your premises. This coverage is separate and essential because standard policies treat alcohol service as an excluded peril. If a customer suffers assault at your taproom or leaves intoxicated and causes a car accident, your general liability won’t respond. Assault-and-battery sublimits within your liquor policy should align with your taproom’s capacity and event frequency.

Product Liability and Recall Protection Address Manufacturing Risks

Product liability and recall protection addresses contamination, foreign material, and multi-state distribution risks. A single contaminated batch can trigger recall costs exceeding $100,000 when you factor in product destruction, freight, retailer chargebacks, and legal defense. This coverage reimburses those direct costs plus business interruption losses during the recall period. For breweries distributing across state lines under the Three-Tier System, recall protection isn’t optional-it’s essential insurance against a scenario that could disable your operation for months.

How These Three Pillars Work Together

These three coverage types work together because each addresses a distinct exposure. General liability handles premises incidents and basic operational claims. Liquor liability protects against alcohol-service-specific bodily injury and property damage. Product liability and recall protection cover manufacturing defects and contamination. Microbreweries typically spend $500 to $1,500 monthly on comprehensive coverage spanning all three areas, with larger operations or those hosting frequent events paying significantly more. The cost reflects real claims data from Washington breweries. Equipment breakdown coverage layers on top because spoilage from temperature failures, glycol system leaks, or boiler malfunctions represents a separate class of loss. Replacement costs in the Seattle area have risen 20% since 2020, making adequate property valuations critical.

Building Your Customized Coverage Program

Work with a broker who understands brewing operations and can document your specific exposures-tank capacity, fermentation processes, taproom guest count, and distribution geography. An independent agency serving Washington and Oregon can partner with multiple carriers to build customized brewery packages that address these three pillars plus equipment and spoilage coverage in one coordinated program. Your next step involves identifying which additional endorsements and limits match your specific operation-a decision that depends on your production volume, event frequency, and distribution footprint.

What Happens When Claims Hit Your Brewery

Slip-and-Fall Injuries Expose Coverage Gaps at Taprooms

Slip-and-fall injuries at your taproom represent one of the most common claim scenarios across Washington breweries. A customer trips on wet brewery flooring, suffers a fracture, and files suit. Your general liability policy responds to the slip-and-fall claim itself, covering medical expenses and legal defense. However, if that same customer consumed alcohol at your taproom before the fall, the claim narrative shifts. Now the plaintiff’s attorney argues over-service contributed to the injury. Your general liability explicitly excludes alcohol-related bodily injury claims, leaving you exposed for defense costs and any settlement.

Taproom staff need clear protocols on how many drinks constitute over-service, documented last-call procedures, and responsible alcohol service training on recognizing impairment. Breweries face slip hazards from wet floors near coolers, burn risks from hot wort transfer, and repetitive strain from lifting heavy ingredient bags. Your coverage should include business interruption protection because a serious injury claim can trigger weeks of legal proceedings and operational disruption.

Product Contamination Claims Escalate Faster and Cost More

Product contamination claims escalate faster and cost more than premises injuries. Foreign material, bacterial contamination, or yeast cross-contamination in finished beer triggers recalls that ripple across multiple retailers and distributors. A single contaminated batch distributed across Washington and Oregon generates recall logistics costs (freight, storage, destruction), retailer chargebacks, and third-party liability exposure if a customer suffers illness.

Recall protection reimburses product destruction, freight costs, lost revenue during the recall period, and legal defense if a consumer lawsuit follows. Quality control becomes your first line of defense. Implement microbiological testing, pH monitoring, temperature logging, and sensory analysis of finished product before shipment. Many Washington breweries now conduct ingredient inspection, monitor fermentation temperature continuously, and maintain documented batch records that defend against contamination claims.

Your product liability limit should align with your distribution footprint. A 15-barrel brewery distributing to five counties faces lower exposure than a 30-barrel operation shipping statewide.

Third-Party Alcohol-Related Incidents Create Off-Premises Liability

Third-party alcohol-related incidents occur when your customer leaves intoxicated and causes injury or property damage to someone else. A customer drinks at your taproom, drives away, and causes a motor vehicle accident injuring another driver. The injured third party sues your brewery for over-service and negligent alcohol service. Your general liability won’t cover this scenario because the injury occurred off-premises and involves alcohol. Your liquor liability policy responds because it covers third-party bodily injury claims arising from alcohol service at your licensed premises.

This exposure intensifies if your taproom hosts events. Festivals, live music nights, and special releases draw larger crowds and increase the statistical probability of over-service incidents. Peak-season endorsements automatically raise your liquor liability limits during high-volume periods when event activity peaks. This prevents underinsurance during your riskiest operating periods. Work with your broker to model claims scenarios specific to your operation. If you host 40 events annually with 200 guests each, your exposure differs significantly from a brewery hosting four annual tastings. Your liquor liability sublimits should reflect this reality.

Building Defenses Against Over-Service Claims

Document your staff training on responsible service, maintain pour records if you track consumption, and implement last-call procedures that demonstrate reasonable care against over-service claims. An independent agency serving Washington and Oregon can partner with multiple carriers to build customized brewery packages that address your specific event frequency and guest capacity. Your broker should document your taproom’s operational realities-how many events you host annually, typical guest counts, and whether you serve food alongside alcohol. This documentation strengthens your defense if a claim arises and demonstrates that your coverage limits match your actual exposure.

Final Thoughts

Standard commercial policies treat breweries like retail shops, which is why they fail when fermentation starts. Equipment breakdown, alcohol-service claims, and product recalls fall outside typical coverage because insurers designed those policies for businesses that don’t manufacture beverages or serve alcohol. A slip-and-fall claim becomes an over-service claim the moment alcohol enters the narrative, a temperature failure becomes a six-figure loss when spoilage coverage is missing, and a contaminated batch becomes a multi-state nightmare without recall protection.

Finding the right coverage requires working with specialists who understand brewing operations, not generalists who quote standard business packages. Your broker needs to know the difference between a 10-barrel system and a 30-barrel system, why glycol system failures matter, and how event frequency affects your liquor liability exposure. They need to understand Washington’s Liquor and Cannabis Board requirements, local fire marshal expectations, and how replacement costs in the Seattle area have risen 20% since 2020.

At ISU Insurance Solutions Group, we partner with multiple carriers to build customized Washington brewery liability coverage that addresses your actual exposures rather than forcing you into generic templates. We handle certificate turnaround for licensing, support you during recalls, and adjust your coverage as your operation scales. Contact us to discuss how tailored brewery liability coverage protects your operation and your bottom line.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.