Professional Services Liability Insurance: Common Pitfalls and Protections

Professional service providers face real financial risks every day. A single mistake-missed deadline, miscommunication, or overlooked detail-can trigger a lawsuit that threatens your entire practice.

At ISU Insurance Solutions Group, we’ve seen how the right professional services liability insurance protects firms from these costly exposures. This guide walks you through the pitfalls that leave providers vulnerable and the protections that actually work.

Common Pitfalls That Expose Professional Service Providers

Documentation Failures Leave You Defenseless

Inadequate documentation creates the largest exposure most service providers never see coming. When you finish a project or complete work for a client, the details fade quickly-but if a dispute arises months or years later, your records become the only evidence of what you actually delivered. Courts and insurers don’t care about your memory; they care about what you can prove.

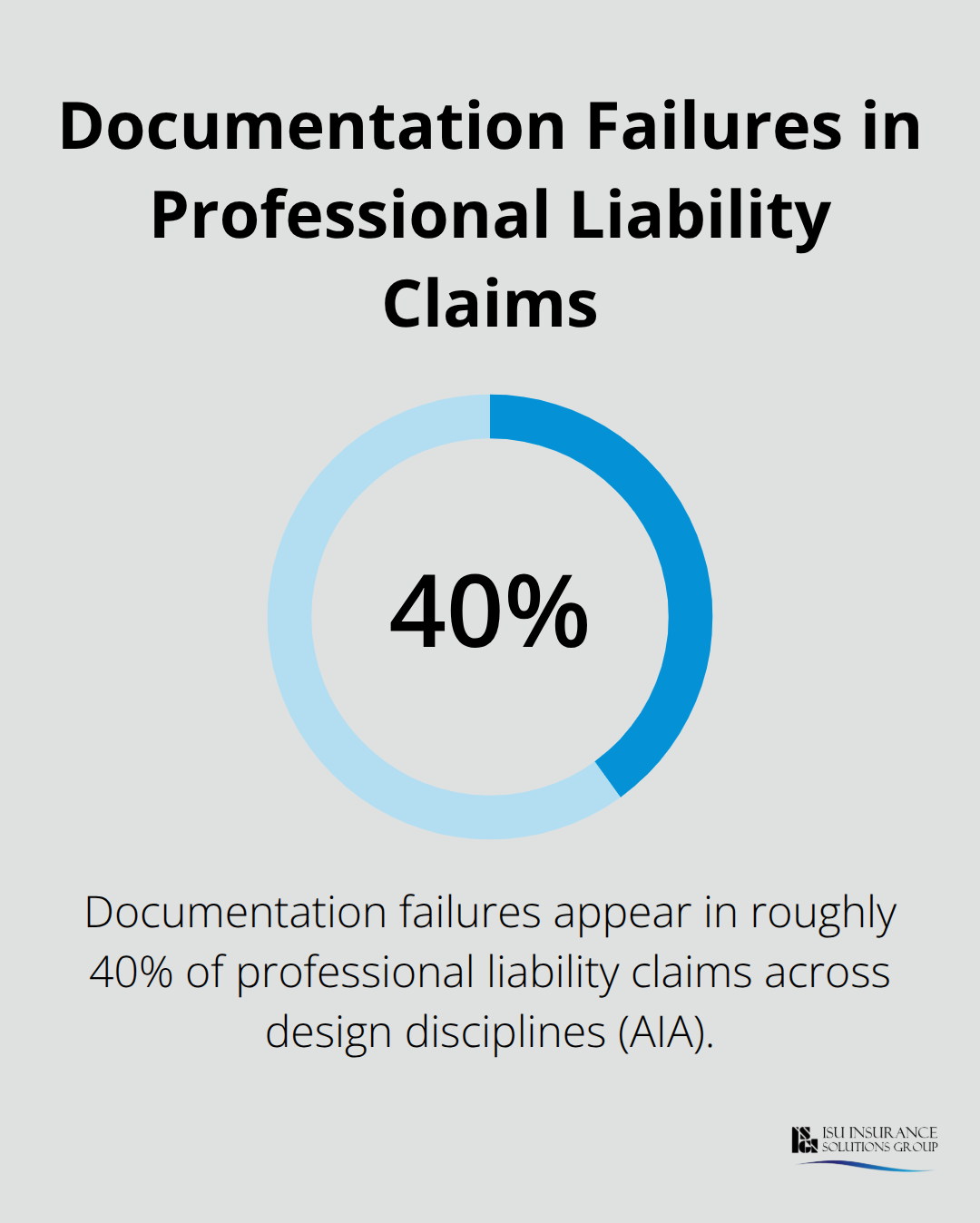

A consultant who fails to document scope changes in writing, an engineer who doesn’t keep detailed notes on design decisions, or an accountant who doesn’t record client instructions all face the same problem: when a claim lands, they have no way to demonstrate they met their obligations. The American Institute of Architects reports that documentation failures appear in roughly 40% of professional liability claims across design disciplines.

Start maintaining a system today that captures client instructions in writing, records project changes with client sign-off, and preserves communications showing what work was completed and when. Email confirmations, project logs, and signed scope documents cost nothing to create but become priceless if you ever need to defend yourself.

Scope Creep and Unmet Expectations Trigger Claims

Scope creep and undefined expectations destroy more professional relationships than actual mistakes do. A client requests one deliverable, but during the project they casually mention three additional tasks they assumed were included. You complete the work thinking you’ve done a solid job, but they feel shortchanged because their unstated expectations weren’t met. This gap between what you promised and what they thought they’d get becomes the foundation for a liability claim.

Set expectations in writing before work begins-specify exactly what services you’ll provide, what’s excluded, timelines, and revision limits. If a client requests additional work mid-project, document the change and confirm whether it’s included in the original fee or costs extra.

Coverage Limits Must Match Your Real Risk

Insurance coverage limits matter just as much as the coverage itself, yet many service providers choose limits based on affordability rather than actual risk. A $1 million per-claim limit sounds substantial until a single error costs $2 million. Review your client contracts carefully; many require minimum coverage limits before they’ll hire you.

If a $5 million project requires $2 million in coverage and you only carry $1 million, you’ve created an uninsurable gap. Evaluate what damages could realistically result from your work-consider lost client revenue, project delays, and legal defense costs-then set your limits accordingly. The right coverage protects both your finances and your ability to take on higher-value work, which leads directly to understanding what protections actually prevent these pitfalls from becoming expensive claims.

What Professional Liability Insurance Actually Covers

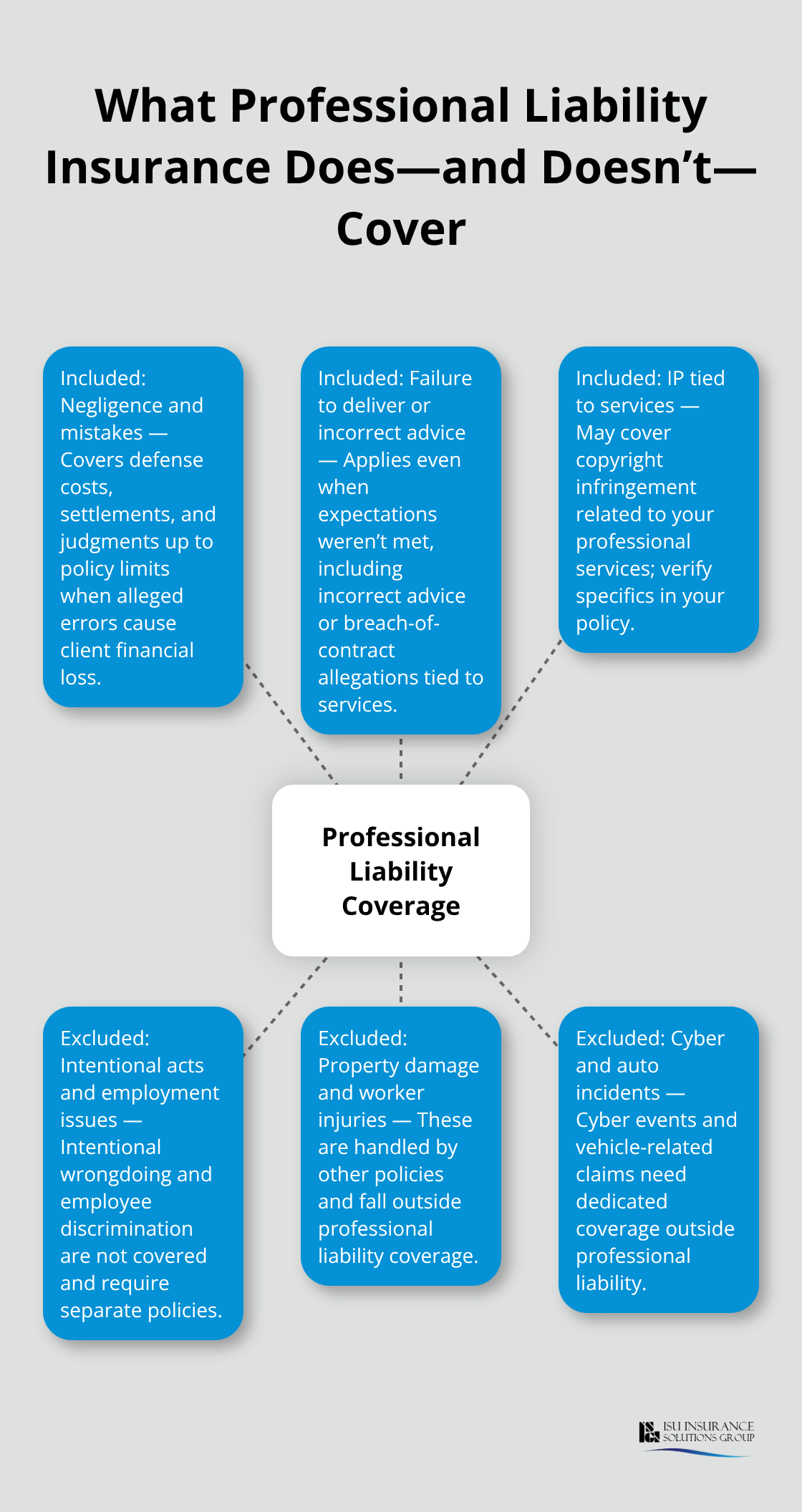

Professional liability insurance protects you when a client claims your work caused them financial loss through negligence, mistakes, or failure to deliver promised services. This coverage pays for legal defense costs, settlements, and court judgments up to your policy limits, which means you avoid personal liability for damages that could exceed your annual revenue. The protection applies whether you made an actual error or simply failed to meet unstated client expectations-a distinction that matters enormously when defending against a claim.

The coverage typically includes defense costs for allegations of negligence, incorrect advice, breach of contract, copyright infringement, and failure to deliver services as promised. What it doesn’t cover matters equally: intentional acts, employee discrimination, property damage, worker injuries, cyber incidents, and vehicle-related incidents all fall outside professional liability and require separate policies.

Claims-Made vs. Occurrence: Your Career Path Determines the Right Choice

Most professional liability policies operate on a claims-made basis, meaning coverage applies only to claims filed while your policy is active. This structure creates a critical vulnerability when you change jobs or retire-a claim filed after your policy expires won’t be covered unless you purchase tail coverage, an extended reporting period that costs up to twice your annual premium. An occurrence policy covers incidents that happen during the policy period regardless of when the claim is filed, offering better protection if you plan career transitions, but occurrence policies typically cost more upfront. If you stay with your current firm long-term, a claims-made policy with a retroactive date works fine and saves money. However, if you consider a job change within the next five years, calculate whether tail coverage costs make sense now or whether switching to an occurrence policy would be more economical. Maryland allows discovery periods extending up to five years after an incident is discovered, meaning claims can surface years later-another reason to verify your policy form matches your career stability.

Industry-Specific Coverage Gaps That Generic Policies Miss

Construction and engineering firms face distinct exposures that generic professional liability policies miss entirely. Environmental liability, pollution coverage, and care-custody-control exclusions create dangerous gaps on projects involving hazardous materials or site work. Software developers and IT consultants need coverage for client losses caused by code defects or faulty implementation advice, yet many standard policies exclude technology-related errors unless specifically endorsed. Healthcare providers often rely on employer-provided malpractice coverage that vanishes when you change positions or retire, leaving you exposed for claims arising from prior work. Verify what your employer actually covers before assuming you’re protected-many employer policies include restrictive language that excludes coverage once you’ve left the organization. The fastest-growing segment in professional liability claims involves surgical errors in healthcare, with surgical-specific endorsements becoming standard for operating physicians and surgical specialists. If your profession handles client funds, fiduciary liability coverage should supplement your professional liability policy to cover investment losses or mismanagement claims.

Finding an Agent Who Understands Your Discipline

Work with an insurance agent who understands your specific discipline rather than accepting a generic quote, because the difference between adequate and inadequate coverage often comes down to industry-specific endorsements that generic carriers miss entirely. An agent familiar with your profession identifies exposures you wouldn’t spot alone and recommends endorsements tailored to your actual work. This specialized knowledge becomes especially valuable when you operate across multiple states or handle complex client relationships, as coverage requirements and claim patterns vary significantly by jurisdiction and service type. The right agent also helps you navigate policy exclusions and confirms that your coverage aligns with what your clients require in their contracts-a mismatch that could disqualify you from bidding on projects or leave you uninsured for work you’ve already completed.

Selecting Coverage That Matches Your Actual Exposure

Review Client Contracts for Coverage Requirements

Pull your three largest client contracts and review their insurance requirements line by line. Most contracts specify minimum coverage limits, and if you fall short, you lose the work entirely-this isn’t negotiable. A construction firm bidding on a $10 million project typically faces a requirement for $2 million or $5 million in professional liability coverage, and submitting a bid without meeting that threshold wastes everyone’s time. Document these requirements across your client base to identify the highest limit you actually need to carry.

Many service providers set their limits based on what feels affordable rather than what their clients demand, which creates a predictable disaster: you win a contract, complete the work flawlessly, then discover the client’s claim exceeds your policy limit and you’re personally liable for the difference.

Understand How Industry Risk Affects Your Costs

Industry data shows that higher-risk professions like engineering and architecture typically pay $800 to $1,200 annually per employee for adequate coverage, while lower-risk consultants might spend $400 to $600. These figures mean nothing, however, if your limit is too low. Your actual costs depend on your discipline, location, years in business, prior claims history, and the coverage limits you select-not on what competitors in your field pay.

Compare Multiple Carriers and Policy Terms

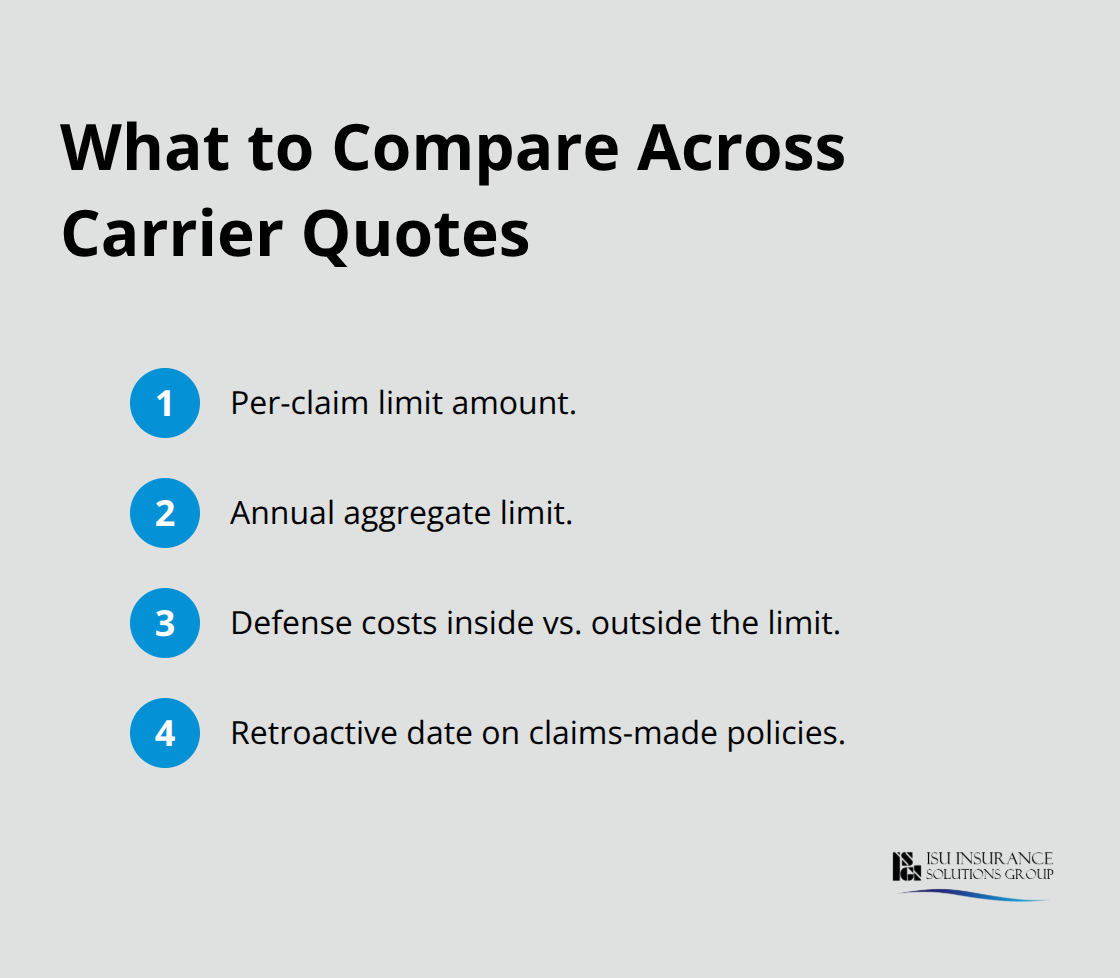

Compare quotes from at least three carriers rather than accepting the first proposal. Progressive reported a national median cost of $42 per month for professional liability insurance in 2024, but that average obscures massive variation by discipline and risk profile. Request quotes that specify per-claim limits, annual aggregate limits, whether defense costs are included within the limit or paid separately, and the retroactive date on claims-made policies.

A carrier offering $1 million coverage at $50 per month might include defense costs within the limit, meaning a $100,000 legal bill reduces your coverage to $900,000 for damages. Another carrier’s $65 monthly quote pays defense costs outside the limit, giving you the full $1 million for damages plus separate defense coverage. These differences dramatically affect your actual protection.

Ask Carriers About Industry Specialization

Ask each carrier directly whether their underwriters specialize in your discipline and what endorsements they recommend for your specific work. An agent who understands your industry spots these differences immediately and steers you toward carriers with favorable terms for your profession rather than pushing you toward the cheapest option. An independent agency with access to multiple carriers (such as ISU Insurance Solutions Group, which partners with 20+ carriers) can compare these policy details across different underwriters and identify which carriers offer the best terms for your specific discipline and risk profile.

Final Thoughts

Professional services liability insurance protects your practice from the financial devastation that follows a claim, whether the error was yours or simply a mismatch between what you delivered and what the client expected. The pitfalls we’ve covered-poor documentation, undefined scope, and inadequate limits-occur regularly across every discipline, and they cost providers thousands in legal fees and damages that proper coverage would have prevented. Your next step is straightforward: pull your client contracts to identify the highest coverage limit any client requires, calculate realistic damages from your work, and compare quotes from multiple carriers while focusing on policy terms rather than price alone.

If you’re changing jobs or retiring within five years, ask about tail coverage costs now rather than discovering them later when you’ve left your employer. Verify that your coverage includes industry-specific endorsements for your discipline and confirm whether your policy operates on a claims-made or occurrence basis. If your employer provides coverage, request written confirmation of what’s actually covered and whether protection extends after you leave the organization.

We at ISU Insurance Solutions Group have helped professional service providers across Washington and Oregon find professional services liability insurance that matches their actual risks since 1983. Our agents understand the exposures specific to your discipline and compare terms across 20+ carriers to identify the best fit for your practice. Contact us for a consultation and quotes tailored to your professional liability needs.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.