Auto Insurance for Businesses: Protecting Assets and People

Your business vehicles are more than just transportation-they’re assets that need protection. Auto insurance for businesses isn’t optional; it’s a legal requirement in every state, and it shields your company from devastating financial losses.

At ISU Insurance Solutions Group, we help business owners understand what coverage actually matters. The right policy protects your employees, your vehicles, and your bottom line when accidents happen.

Why Your Business Needs Commercial Auto Insurance

Every state requires commercial auto insurance if your business operates vehicles, and this isn’t just a legal checkbox. Most states mandate liability coverage for bodily injury and property damage when vehicles are used for business purposes. The financial exposure from a single accident can be catastrophic-without proper coverage, your business faces unlimited liability for injuries, medical bills, lost wages, and property damage claims. A serious collision involving an employee could result in settlement costs exceeding $100,000 or more, and without commercial auto insurance, that liability falls directly on your business. Personal auto policies explicitly exclude business use, which means your employees’ personal insurance won’t cover accidents that occur while conducting company business. If an employee uses their personal vehicle for work-related tasks and causes an accident, your business could face negligent entrustment liability-the legal consequence of allowing someone to operate a vehicle for business when you haven’t verified their qualifications or driving history.

What Commercial Auto Insurance Actually Covers

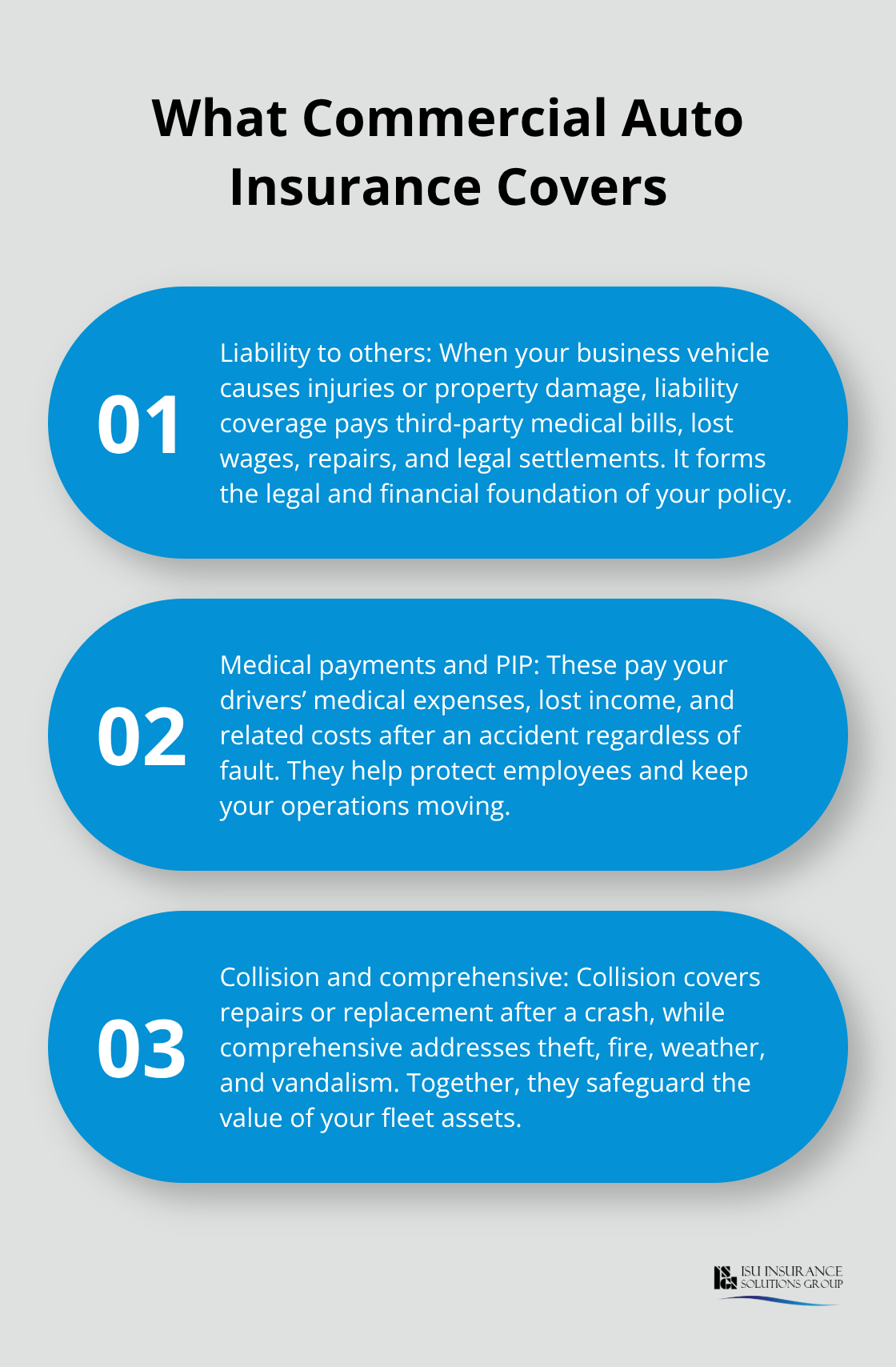

Commercial auto insurance covers bodily injury and property damage that your business causes to others, but it also protects your employees and your assets. Medical payments coverage and personal injury protection pay for your drivers’ medical expenses, lost wages, and even funeral costs after an accident, regardless of who was at fault.

Uninsured and underinsured motorist coverage has become increasingly important-the Transportation and Logistics industry, which represents the largest vertical needing commercial auto coverage, faces significant risk from uninsured drivers on the road. Collision coverage repairs or replaces your company vehicles after accidents, while comprehensive coverage protects against theft, fire, weather damage, and other non-collision losses.

Why Asset Protection Matters More Than Ever

For vehicles used for both business and personal purposes, the correct insured must be listed on the policy declarations to avoid claim denials-this detail matters more than most business owners realize. If your employees occasionally use personal vehicles for business errands, hired and non-owned auto coverage fills the gap that personal policies leave open, protecting your company when those accidents happen. The right coverage strategy (one that matches your actual fleet and operations) prevents costly gaps that could expose your business to unexpected expenses.

What Coverage Types Actually Protect Your Fleet

Liability Coverage Forms Your Foundation

Liability coverage forms the foundation of commercial auto insurance, and most states legally require it. When your business vehicle causes bodily injury or property damage to someone else, liability coverage pays for their medical bills, lost wages, property repairs, and legal settlements up to your policy limits. Carriers commonly use a Combined Single Limit approach, typically offering $500,000 or $1,000,000 in coverage for both bodily injury and property damage combined. The reality is that $500,000 limits expose mid-sized businesses to significant risk-a single serious accident involving multiple vehicles or pedestrians can easily exceed this threshold.

Most business owners underestimate their exposure because they focus on the vehicle’s value rather than the potential liability from injuries. If your company operates in transportation or logistics, where the industry faces the largest share of commercial auto claims, you need higher limits. The difference between $500,000 and $1,000,000 in coverage costs far less than the gap between what a major accident costs and what your policy actually pays.

Collision and Comprehensive Coverage Protect Your Assets

Collision and comprehensive coverage protect your actual fleet assets, and these matter differently depending on your vehicle values and usage patterns. Collision coverage pays for repairs or replacement after accidents, while comprehensive handles theft, fire, weather damage, and vandalism. The critical decision here involves your deductible-choosing a $1,000 deductible instead of $500 can lower your annual premium significantly, but only if your business can absorb that cost without strain.

For vehicles worth less than $5,000, comprehensive coverage often costs more than the vehicle’s value, making self-insurance the smarter choice. You should evaluate each vehicle individually rather than applying one deductible across your entire fleet. This approach prevents you from overpaying for protection on older or lower-value vehicles.

Uninsured and Underinsured Motorist Coverage Protects Your Drivers

Uninsured and underinsured motorist coverage protects your drivers when the other party lacks sufficient insurance, and this has become non-negotiable. According to the Insurance Research Council, 15.4% of motorists were uninsured in 2023, meaning your employees face genuine risk from drivers who cannot pay for injuries they cause. This coverage pays your drivers’ medical expenses, lost wages, and damages when an uninsured driver hits them, protecting both your people and your payroll continuity when accidents happen.

Your drivers encounter this risk every time they operate a company vehicle, which makes this coverage essential rather than optional. Without it, your employees absorb the financial consequences of someone else’s lack of insurance. The cost of this protection remains minimal compared to the exposure your team faces on the road.

Matching Coverage to Your Actual Operations

The coverage you select should align with how your business actually uses vehicles. A delivery service operates under different risk conditions than a consulting firm with occasional client visits, and your policy should reflect that distinction. Transportation and logistics operations face higher frequency claims, while construction companies encounter different hazards entirely. Your coverage strategy must account for your specific industry, vehicle types, and how often employees drive for business purposes.

What Actually Drives Your Commercial Auto Premiums

Driver Records and Vehicle Types Set Your Base Rate

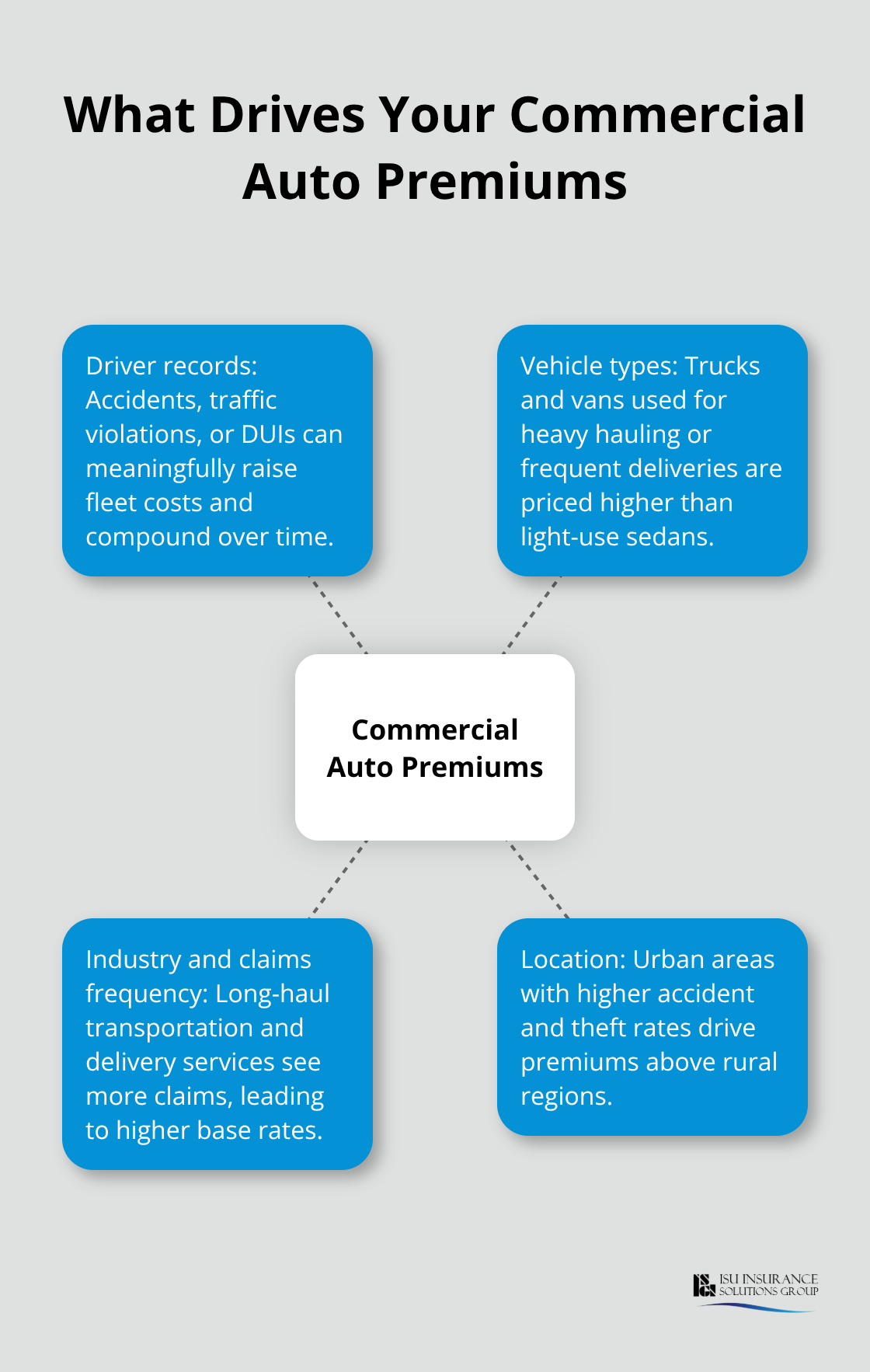

Your driver records and vehicle types are the two largest factors determining what you pay for commercial auto insurance, and understanding this reality helps you make smarter decisions about where to invest in risk reduction. A single driver with a history of accidents, traffic violations, or DUI convictions can increase your entire fleet’s premiums by 20 to 40 percent, which means one bad hire creates ongoing costs that compound across years. Vehicle type matters equally-trucks and vans used for heavy hauling or frequent deliveries generate higher claims than sedans used for occasional client visits, so carriers price them accordingly. The industry data shows that long-haul transportation and delivery services face the highest frequency of claims, which directly translates to higher base rates for those operations.

Your location also influences costs significantly; businesses operating in urban areas with higher accident rates and theft risk pay more than those in rural regions, and this geographic factor sits outside your immediate control but should inform your coverage strategy.

Safety practices and driver training Lower Your Costs

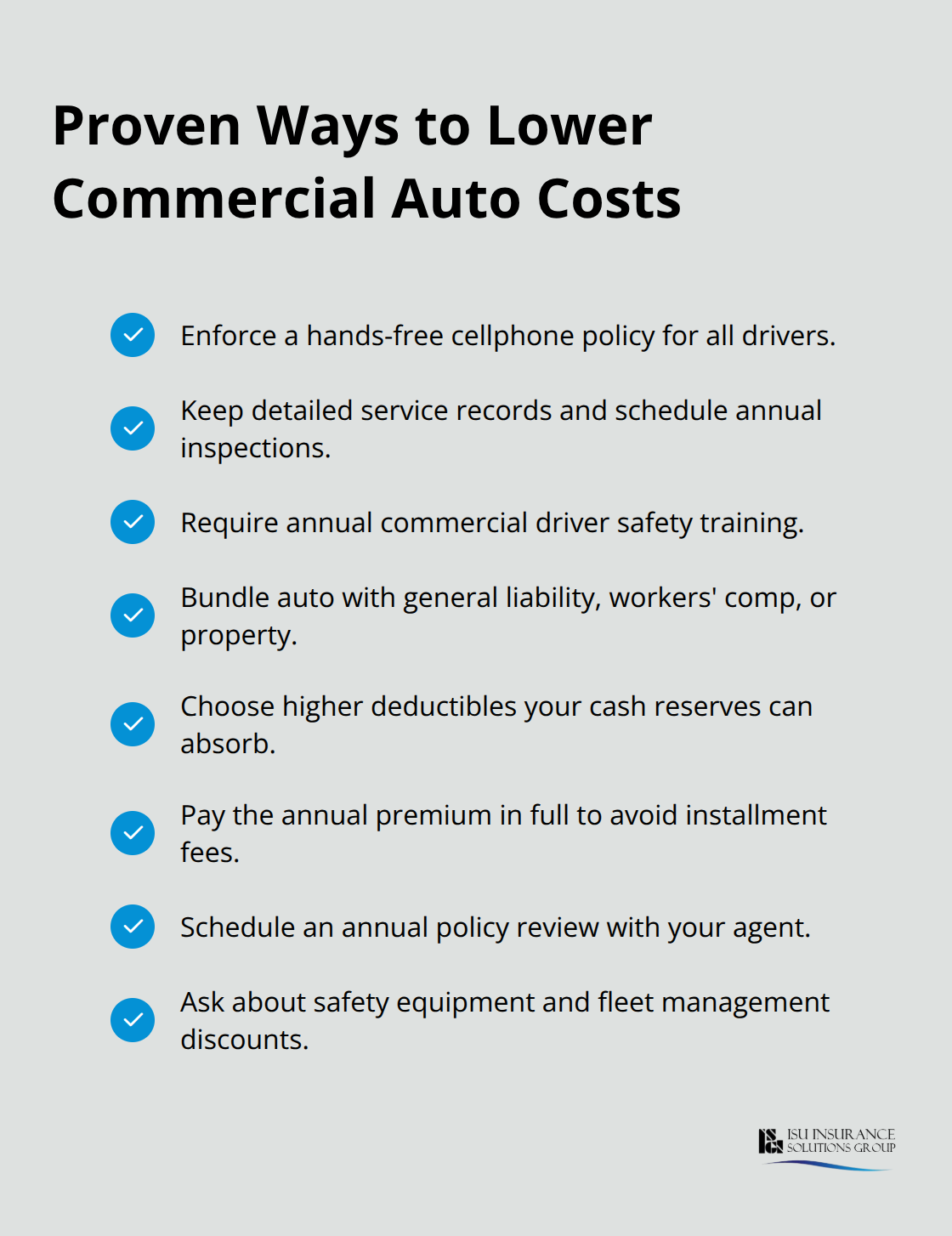

The practical path to lower premiums focuses on controllable factors that directly reduce your risk profile. A documented cellphone and texting policy requiring hands-free operation for all drivers demonstrates risk awareness to carriers and qualifies your business for safety-focused discounts that typically save 10 to 15 percent annually. Detailed vehicle service records and annual inspections show carriers that your fleet receives professional upkeep, which reduces mechanical failure claims and demonstrates operational discipline. Driver training programs specifically addressing commercial driving hazards create another discount opportunity; many carriers offer reductions when drivers complete approved safety courses annually.

Policy Bundling and Deductible Choices Reduce Expenses

Bundling your commercial auto policy with general liability, workers’ compensation, or property coverage through the same carrier generates substantial savings-bundled policies typically cost 15 to 25 percent less than purchasing coverage separately from multiple insurers. Higher deductibles directly lower premiums, and choosing a $2,500 deductible instead of $500 can reduce your annual costs by 20 to 30 percent if your business maintains adequate cash reserves to absorb that expense. Paying your annual premium in full rather than monthly installments eliminates installment fees and often qualifies you for an additional 5 to 10 percent paid-in-full discount that compounds your savings.

Annual Policy Reviews Uncover Hidden Savings

Rate changes happen constantly, and carriers frequently apply discounts retroactively when you request policy reviews. Schedule an annual conversation with your agent rather than waiting for renewal notices-this proactive approach catches rate reductions and new discount programs that you might otherwise miss. The most overlooked strategy involves asking your agent about discounts you haven’t yet qualified for; many carriers offer reductions for safety equipment, driver certifications, or fleet management practices that your business may already have in place.

Final Thoughts

Commercial auto insurance for businesses protects far more than vehicles-it safeguards your employees, your assets, and your company’s financial stability when accidents happen. The coverage you select directly determines whether a single collision becomes a manageable claim or a catastrophic expense that threatens your operations. Liability protection covers the injuries and property damage your business causes to others, while collision and comprehensive coverage preserve your fleet’s value, and uninsured motorist protection shields your drivers from the financial consequences of someone else’s lack of insurance.

Choosing the right coverage means matching your policy to how your business actually operates. A delivery service faces different risks than a consulting firm, and your coverage should reflect that reality rather than following a generic template. Your driver records, vehicle types, location, and industry all influence both your risk profile and your premiums, which means understanding these factors helps you make smarter decisions about where to invest in protection.

We at ISU Insurance Solutions Group have served Washington and Oregon businesses since 1983, helping owners navigate the complexity of auto insurance for businesses through personalized guidance and competitive rates. Our independent agency partners with multiple carriers, which means we can compare coverage options and pricing across different insurers rather than limiting you to a single company’s offerings. Contact us today to review your current coverage or get quotes for your fleet.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.