Professional Liability Insurance Washington: Reducing Risk for Your Practice

One lawsuit can devastate your practice financially. Professional liability insurance in Washington protects you from the costs of client claims, legal defense, and settlements that could otherwise force you to close your doors.

We at ISU Insurance Solutions Group help Washington professionals understand their coverage options so they can focus on their work with confidence. The right policy matches your specific risks and keeps your practice secure.

Why Professional Liability Insurance Matters for Washington Practices

The Real Cost of Client Claims

Washington professionals face genuine financial exposure when clients file claims. A single lawsuit costs thousands in legal defense alone, even if you win. Average defense costs for professional liability claims in Washington average $87,338. For consultants, architects, and medical professionals, these numbers climb higher. Many practices close not because they were negligent, but because they could not absorb the financial hit of defending themselves in court.

Why the Absence of a Legal Requirement Misleads You

Washington law does not mandate professional liability insurance for most professions, but that absence of a legal requirement creates a false sense of security. Many contracts, licenses, and client relationships now require proof of coverage. Real estate professionals, consultants, and building designers frequently discover that lenders, franchises, or major clients will not work with them without a Certificate of Insurance showing active coverage.

Coverage Requirements That Block Your Growth

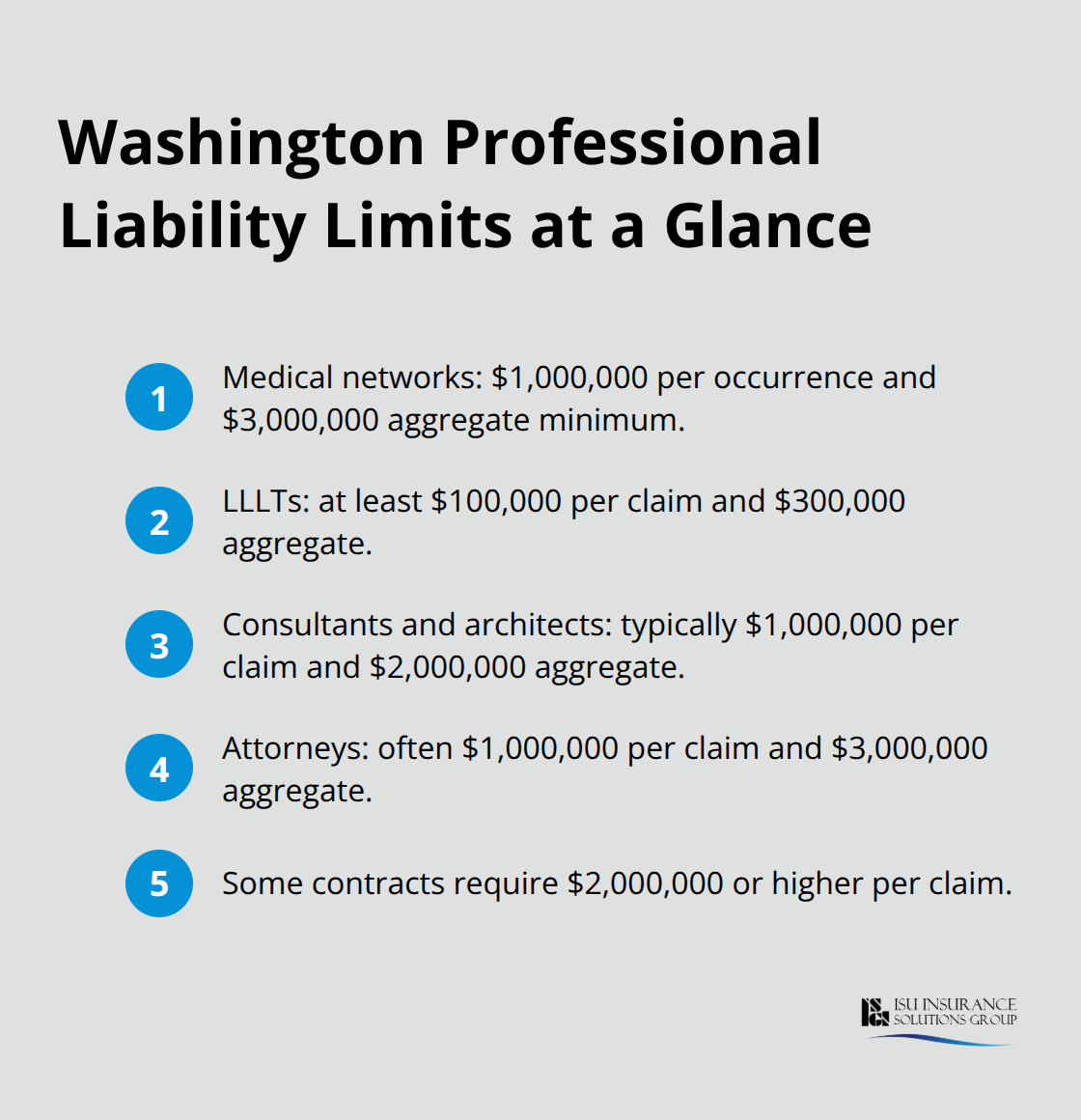

Medical professionals enrolling in insurance networks must carry minimum coverage of $1,000,000 per occurrence and $3,000,000 annual aggregate to participate. Limited License Legal Technicians must maintain at least $100,000 per claim and $300,000 annual aggregate. These are not suggestions-they are enrollment barriers that block your ability to serve clients and grow revenue.

Attorneys in Washington must report their insurance status annually to the Washington State Bar Association, though coverage remains optional. The WSBA does not independently verify that reported coverage is current or adequate, so clients often ask for direct proof. A Certificate of Insurance demonstrates you take risk seriously and protects your reputation when prospects ask about your coverage. Without it, you signal either that you are uninsured or that you are hiding your coverage status, both of which damage client confidence.

The Affordability Factor

The cost of professional liability insurance in Washington is affordable, making it one of the least expensive ways to protect your practice from catastrophic loss. That monthly premium is far cheaper than the legal fees you would pay defending a single claim, and it covers your defense costs, settlements, and judgments up to your policy limits. Understanding what different policy types actually cover-and how they differ-helps you select the right protection for your specific practice.

How Professional Liability Policies Actually Work

Claims-Made Coverage and Your Reporting Window

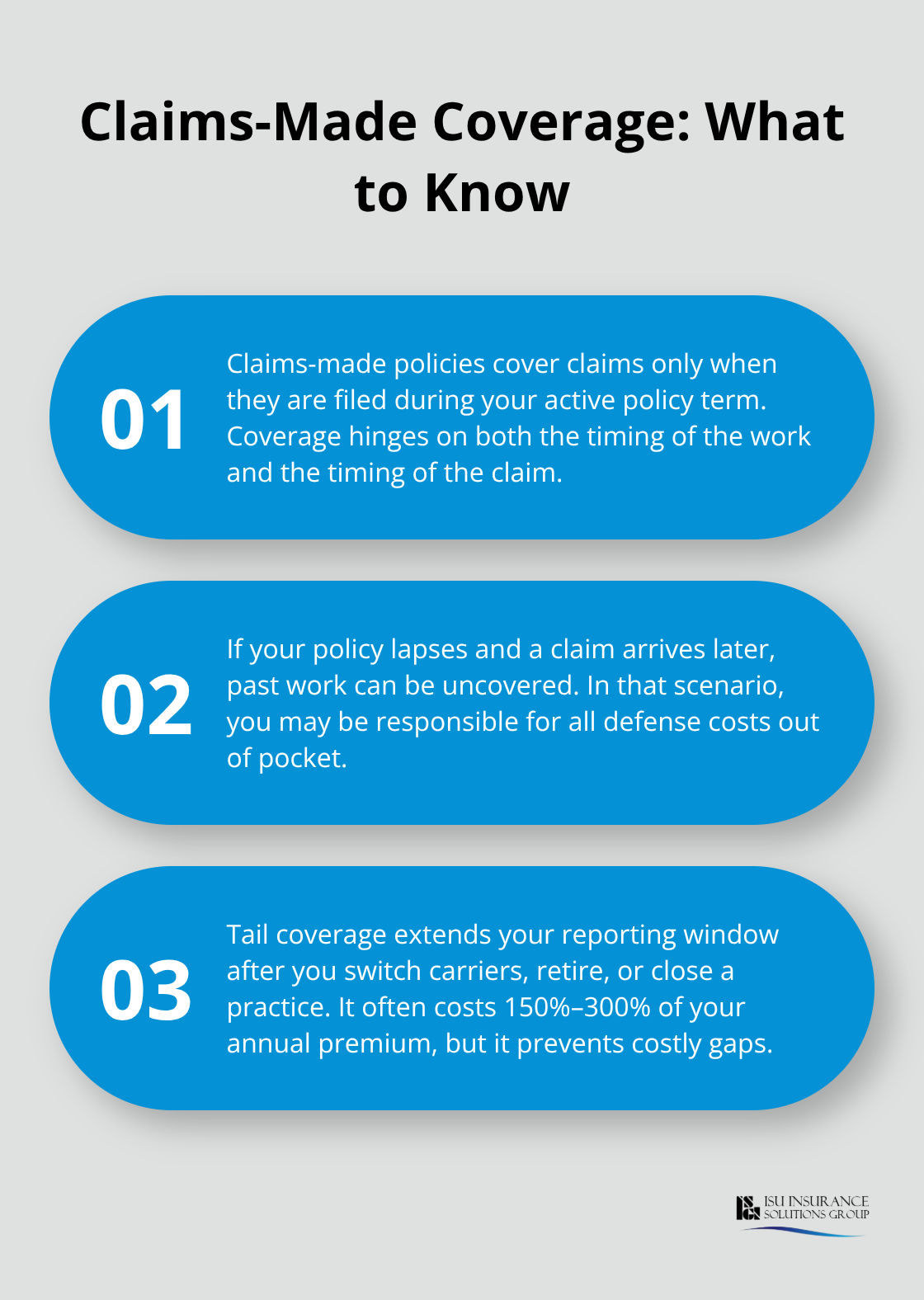

Most professional liability policies in Washington operate on a claims-made basis, which means coverage applies only to claims filed during your active policy term. This distinction matters more than you might think. If you stop your policy and a client files a claim two years later for work you performed while insured, that claim falls outside your coverage window and you pay for defense entirely out of pocket.

Tail Coverage Protects Your Transition

Tail coverage extends your reporting period after you leave a practice, retire, or switch carriers. Without tail coverage, you face years of unprotected exposure. The cost of tail coverage typically runs 150 to 300 percent of your annual premium-a significant but necessary expense when you transition practices. Some carriers include a limited tail period automatically, so verify what your current policy offers before assuming you need to purchase extended reporting separately.

Coverage Limits Match Your Risk Exposure

The coverage limits you select directly determine your financial protection in a claim. Washington medical professionals must maintain $1,000,000 per occurrence and $3,000,000 annual aggregate to enroll in insurance networks, but your actual needs depend on your specific risk exposure and contract requirements. Consultants and architects typically carry $1,000,000 per claim with $2,000,000 aggregate, while attorneys often select $1,000,000 per claim with $3,000,000 aggregate based on case complexity and client base.

Deductibles Shape Your Premium and Out-of-Pocket Costs

Your deductible affects both your premium and your out-of-pocket responsibility when a claim occurs. A $2,500 deductible costs less monthly than a $1,000 deductible, but you absorb the first $2,500 of defense costs in any claim. Industry-specific risks shape what coverage you truly need-medical professionals handling complex surgeries face higher exposure than solo practitioners in lower-risk specialties, and this difference should reflect in your policy selection.

Matching Coverage to Your Practice Reality

Your specific practice determines which limits actually protect you. Medical professionals, attorneys, consultants, and architects each face distinct claim patterns and defense costs that demand different coverage strategies. The next section walks you through how to assess your own risk exposure and select limits that match your actual practice rather than simply meeting minimum enrollment requirements.

Matching Your Coverage to Your Practice Risk

Assess Your Specific Services and Client Exposure

Start by listing the specific services you provide and the client relationships that create exposure. An architect designing commercial buildings faces different claim patterns than a solo consultant advising on business strategy. A surgeon performing complex procedures carries higher risk than a family medicine doctor. Medical professionals in Washington enrolling in insurance networks must carry $1,000,000 per occurrence and $3,000,000 annual aggregate minimum, but that floor does not account for your actual practice complexity.

Review your contracts and client agreements to identify any coverage requirements your clients impose. Many hospitals, school districts, and corporate clients demand $2,000,000 or higher per claim before they hire you. Your policy must meet or exceed these contractual minimums, or you cannot accept the work. If you serve multiple client types, your highest requirement becomes your policy floor.

Evaluate Your Claims History and Financial Exposure

Your claims history shapes your risk profile. Attorneys with complex litigation practices face higher defense costs than those handling simple estate planning. Consultants working with startups on financial projections face different exposure than those advising established corporations. If you have never faced a claim, your risk profile still depends on the complexity of your work and the financial stakes your clients hold.

A $500,000 error in a client transaction creates exposure that demands robust coverage. A missed deadline costing a client millions in lost opportunity demands coverage that matches that potential loss. Your actual practice complexity, not minimum enrollment requirements, should drive your coverage selection.

Choose Your Deductible Based on Cash Flow and Risk Tolerance

Your deductible choice directly affects your monthly premium and your financial exposure when a claim occurs. A $2,500 deductible typically costs 20 to 30 percent less monthly than a $1,000 deductible, but you absorb the first $2,500 of defense costs out of pocket in any claim. For practices with strong cash reserves and clean claims histories, higher deductibles reduce premiums significantly. For practices operating on tighter margins or in higher-risk specialties, lower deductibles provide peace of mind even if premiums climb.

Partner with Local Agents Who Know Your Profession

Work with a Washington-licensed agent who understands your specific profession, not a national carrier with generic underwriting. Independent agents access quotes from multiple carriers and match your practice profile to carriers that specialize in your profession. They identify coverage gaps you might miss and explain exclusions that matter to your work.

Many policies exclude coverage for illegal conduct, intentional harm, or discrimination claims, so understand what falls outside your protection. Get multiple quotes and request a Certificate of Insurance within 24 hours of application to compare how quickly each carrier processes your request. Your coverage becomes active only after you receive that certificate, so speed matters when you need protection immediately.

Final Thoughts

Professional liability insurance in Washington protects your ability to serve clients and build your practice without fear that one claim destroys everything you have built. List the specific services you provide, review any coverage requirements your clients impose, and identify your actual financial exposure if a claim occurs. Medical professionals need $1,000,000 per occurrence and $3,000,000 aggregate minimum to enroll in insurance networks, while attorneys must report their coverage status to the Washington State Bar Association.

Contact a Washington-licensed agent who understands your profession and accesses quotes from multiple carriers in a single conversation. Request a Certificate of Insurance within 24 hours of application so you can verify coverage is active before you take on new clients. Compare not just premiums but also what each policy covers, what it excludes, and how quickly the carrier processes claims.

We at ISU Insurance Solutions Group have served Washington and Oregon professionals since 1983, helping them select professional liability insurance that matches their specific risks rather than settling for generic policies. Our independent agency partners with 20+ carriers to deliver personalized quotes and hands-on support from local agents who understand Pacific Northwest practices. One call gets you multiple quotes and honest guidance on what coverage actually protects your work.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.