Restaurant Insurance Coverage: Custom Fit for Your Eatery

Running a restaurant means juggling dozens of moving parts every single day. One mistake-a customer’s slip on a wet floor, a kitchen fire, a foodborne illness outbreak-can shut you down financially.

At ISU Insurance Solutions Group, we’ve seen restaurants lose everything because they didn’t have the right restaurant insurance coverage in place. The good news is that protecting your eatery doesn’t have to be complicated.

What Coverage Do Restaurants Actually Need?

General Liability and Property Protection

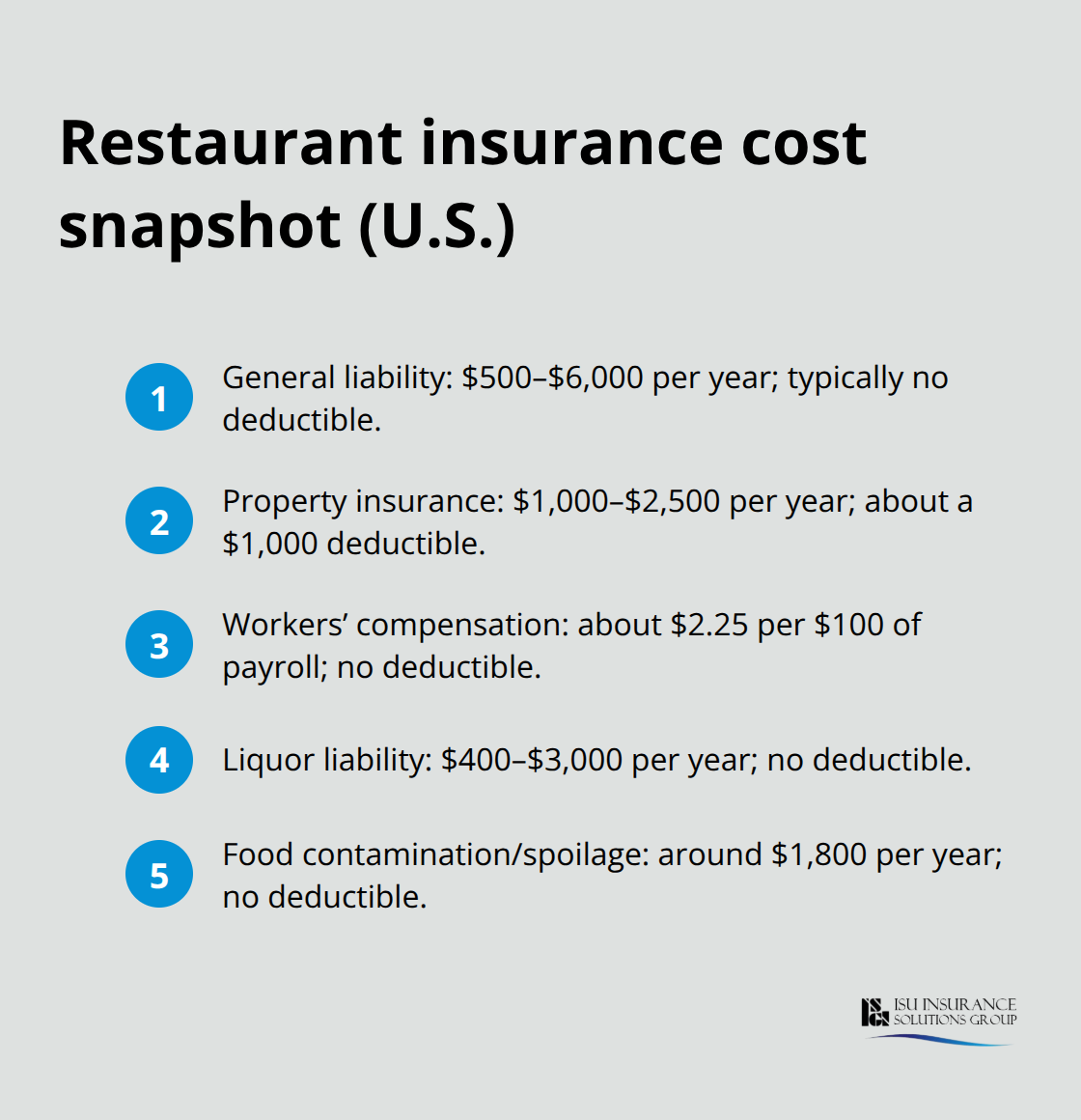

General liability insurance protects you when a customer slips on a wet floor or claims your food made them sick. Most restaurants pay between $500 and $6,000 annually for this coverage with no deductible. This policy covers medical bills, legal defense costs, and settlements-expenses that can bankrupt a restaurant without protection.

Property insurance stands equally vital. It covers your kitchen equipment, furniture, inventory, and the building itself if you own it. Annual costs typically run $1,000 to $2,500 with a $1,000 deductible. When a fire damages your commercial oven or a power outage spoils your walk-in cooler full of inventory, property insurance helps you recover without depleting your cash reserves.

Workers Compensation and Liquor Liability

Workers compensation is legally required in most states if you have employees. Premiums average about $2.25 per $100 of payroll with no deductible. This coverage pays medical expenses and lost wages when staff members get injured on the job-whether that’s a burn from hot oil or a slip in the kitchen.

If you serve alcohol, liquor liability insurance is non-negotiable. This coverage costs between $400 and $3,000 per year with no deductible and protects you when an intoxicated customer causes injury or property damage. Many jurisdictions legally require this if you have a liquor license, but more importantly, liability can extend beyond your doors. An overserved customer who leaves your restaurant and causes an accident can still trigger claims against your business.

Matching Coverage to Your Restaurant’s Real Risks

Most restaurants buy the cheapest policies available rather than matching coverage to their actual risks. A restaurant with $800,000 in annual revenue and 12 employees faces completely different exposures than a small 50-seat café. Your coverage limits should reflect your sales volume, the value of your equipment and inventory, and the number of people working in your kitchen.

A $1 million general liability limit might prove insufficient if you operate a high-volume establishment. Many successful restaurants layer an umbrella policy on top of their standard coverage to protect against claims exceeding their base limits. This additional protection costs far less than the financial devastation of a major lawsuit.

Food Contamination Coverage Protects Your Inventory

Food contamination and spoilage coverage deserves special attention. Equipment failure or power outages destroy thousands of dollars in inventory. This coverage typically costs around $1,800 per year with no deductible and reimburses you when food becomes unsafe to serve.

A single refrigerator breakdown during summer heat creates financial stress that takes months to recover from without this protection. The real question isn’t whether your equipment will fail-it’s whether you can afford to replace spoiled inventory when it does. Understanding these coverage gaps helps you move forward with confidence into selecting the right policy for your operation.

Real Restaurant Risks That Insurance Must Cover

Kitchen Fires Demand More Than Property Coverage

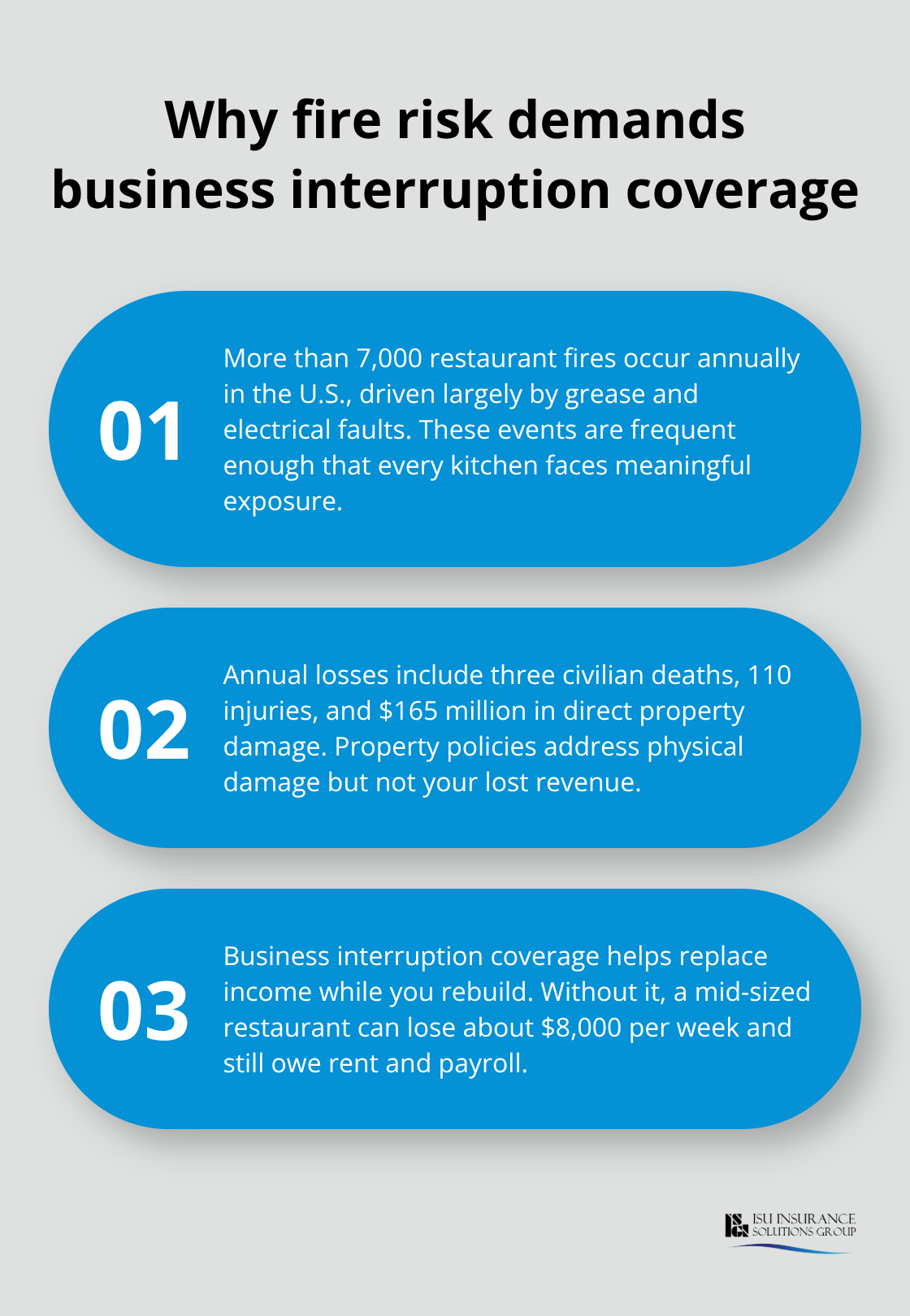

Fire remains the most devastating threat restaurants face. The National Fire Protection Association reports over 7,000 restaurant fires annually, with grease and electrical faults driving the majority. These fires cause average annual losses of three civilian deaths, 110 civilian injuries, and $165 million in direct property damage. Property insurance covers the direct damage, but business interruption coverage reimburses your lost income while you rebuild. Without it, you pay rent and payroll from depleted savings while your kitchen sits idle. A mid-sized restaurant losing $8,000 weekly in sales quickly realizes that property coverage alone leaves a dangerous gap.

Foodborne Illness Outbreaks Destroy More Than Revenue

Foodborne illness outbreaks create financial and reputational damage that spreads faster than traditional liability claims. When customers report illness linked to your food, medical costs mount immediately, but the real cost comes from closure orders, lost revenue, and destroyed customer trust. Food contamination coverage specifically addresses inventory losses from equipment failures, power outages, or actual contamination events. A summer power outage lasting just 12 hours can spoil $15,000 to $25,000 in inventory depending on your walk-in cooler contents. This coverage typically costs around $1,800 annually and prevents that single equipment failure from forcing you to choose between replacing spoiled stock and making payroll.

Customer Injuries Exceed Standard Liability Limits

Customer injuries happen constantly in restaurants. Slip-and-fall incidents, burns from hot plates, and allergic reactions to undisclosed ingredients all generate liability claims. General liability insurance covers medical expenses and legal defense, but the real issue is that one serious injury lawsuit can exceed your policy limits. A customer suffering permanent injury from a fall or severe burn can pursue settlements well above $1 million, which is why successful restaurants layer umbrella policies on top of their standard coverage. This additional protection costs surprisingly little compared to the financial catastrophe of an uncovered judgment.

Employee Claims Extend Beyond Workers Compensation

Employee injuries and related claims pose ongoing financial exposure. Burns, cuts, sprains, and repetitive stress injuries occur regularly in kitchens. Workers compensation covers medical costs and lost wages, but employment practices liability insurance addresses a separate risk entirely. Claims for discrimination, harassment, or wrongful termination can cost $50,000 to $150,000 in legal defense alone, even when the restaurant ultimately prevails. Many operators skip EPLI coverage thinking it’s unnecessary, then face devastating legal costs when a terminated employee claims discrimination. The coverage costs far less than a single employment lawsuit, making it a practical investment for any restaurant with staff.

Understanding these specific risks helps you move beyond generic insurance policies toward coverage that actually protects your operation. The next section walks you through how to select the right policy structure for your restaurant’s unique situation.

Matching Your Restaurant’s Specific Needs to the Right Policy

Document Your Restaurant’s Actual Operations

Selecting restaurant insurance requires moving past generic quotes and building coverage around your actual operation. A 40-seat casual bistro with five employees and $400,000 in annual revenue needs fundamentally different protection than a 120-seat fine dining establishment with 25 staff members and $1.2 million in sales. Your property values differ, your liability exposure varies dramatically, and your employee-related risks scale with headcount.

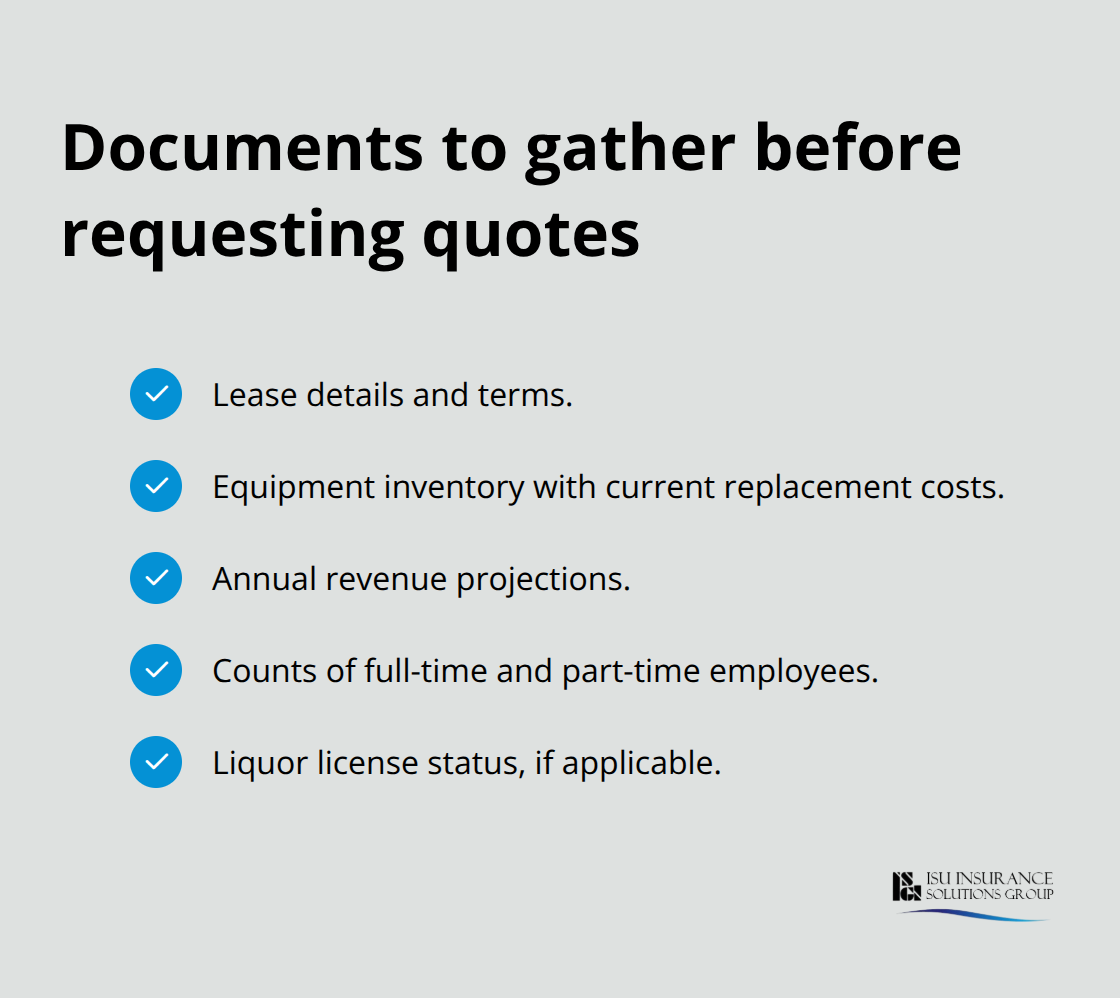

Start by documenting your restaurant’s specifics before talking to any agent. Gather your lease details, current equipment inventory with replacement costs, annual revenue projections, number of full-time and part-time employees, and your liquor license status if applicable. This information determines which coverage limits make sense and which deductibles you can actually afford.

A $5,000 deductible sounds cheaper until a fire damages your kitchen and you must write that check while waiting for reimbursement. Many restaurant owners choose $1,000 deductibles because they can absorb that cost without destroying cash flow, even though monthly premiums cost slightly more.

Set Coverage Limits That Match Your Actual Exposure

Coverage limits should reflect your real exposure, not industry minimums. General liability limits of $1 million work for small neighborhood cafés, but mid-sized restaurants frequently need $2 million in coverage. The difference in premium cost between $1 million and $2 million limits often runs only $200 to $400 annually, making the upgrade practical insurance.

Your property coverage limit must match your actual equipment and inventory value-not what you wish you paid for your kitchen. Photograph and document everything in your restaurant, then obtain replacement cost estimates from your equipment suppliers. This creates an accurate inventory that prevents disputes when you file a claim. When comparing policies, ignore the headline premium and focus on what’s actually covered. One carrier’s standard property policy might include food spoilage coverage while another charges extra for it. One general liability policy might cover liquor liability incidents up to a certain limit while another excludes them entirely.

Read Policy Language, Not Just Summary Sheets

Read the actual policy language, not just the summary sheet. The details reveal what separates adequate protection from dangerous gaps. One policy structure might bundle equipment breakdown coverage with a short waiting period before reimbursement kicks in, while another policy requires you to purchase it separately at higher cost.

An agent who specializes in restaurants understands these nuances far better than someone selling generic commercial policies. That expertise prevents you from discovering coverage gaps after a loss occurs. A restaurant-focused agent knows which carriers handle liquor liability claims efficiently, recognizes that your property coverage needs to account for seasonal inventory fluctuations, and understands how equipment breakdown coverage actually works in practice.

Work with Agents Who Understand Restaurant Operations

Working with an agent who specializes in restaurants matters far more than shopping purely on price. At ISU Insurance Solutions Group, we work with 20+ carriers across Washington and Oregon, which means we can show you multiple policy structures for the same protection level so you understand exactly what differences exist between them. This multi-carrier approach reveals options that single-carrier agents cannot offer.

Your agent should ask detailed questions about your specific operation-not just your revenue and employee count. Questions about your menu (do you deep fry?), your kitchen layout, your equipment age, and your claims history all shape which carriers will offer competitive rates and which will decline your business. An agent with restaurant expertise recognizes that a 15-year-old commercial oven presents different risk than brand-new equipment, and that knowledge influences both pricing and coverage recommendations.

Final Thoughts

Restaurant insurance coverage tailored to your operation protects far more than your equipment and inventory-it protects your ability to recover and rebuild after unexpected events. Your restaurant faces unique risks based on your menu, location, equipment, staffing levels, and customer base, so generic policies miss the distinctions that matter most. A pizza place with a wood-fired oven faces different fire exposure than a sandwich shop, and a fine dining establishment with 30 staff members needs different employment practices coverage than a casual café with five employees.

Start by gathering your restaurant’s documentation: your lease, equipment inventory with replacement costs, annual revenue, employee count, and liquor license status if applicable. Then contact an agent who specializes in restaurant operations rather than someone selling generic commercial policies, because that expertise prevents costly coverage mistakes and reveals options that single-carrier agents cannot offer. The difference between adequate protection and dangerous gaps often comes down to the detailed questions an agent asks about your menu, kitchen layout, equipment age, and claims history.

At ISU Insurance Solutions Group, we’ve been protecting Pacific Northwest businesses since 1983, and restaurants represent a significant part of our practice. We work with 20+ carriers across Washington and Oregon, which means we show you multiple policy structures so you understand exactly what separates one option from another. Contact us today to discuss your specific needs and get quotes that reflect your real exposure.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.