IT Professionals Liability Insurance: Coverage You Need

One mistake in your IT infrastructure can cost thousands in client lawsuits, regulatory fines, and recovery expenses. IT professionals liability insurance protects you when things go wrong-whether it’s a failed system deployment, data breach, or missed compliance requirement.

At ISU Insurance Solutions Group, we help IT professionals understand exactly what coverage they need. This guide walks you through what’s covered, why protection matters, and how to choose the right policy for your business.

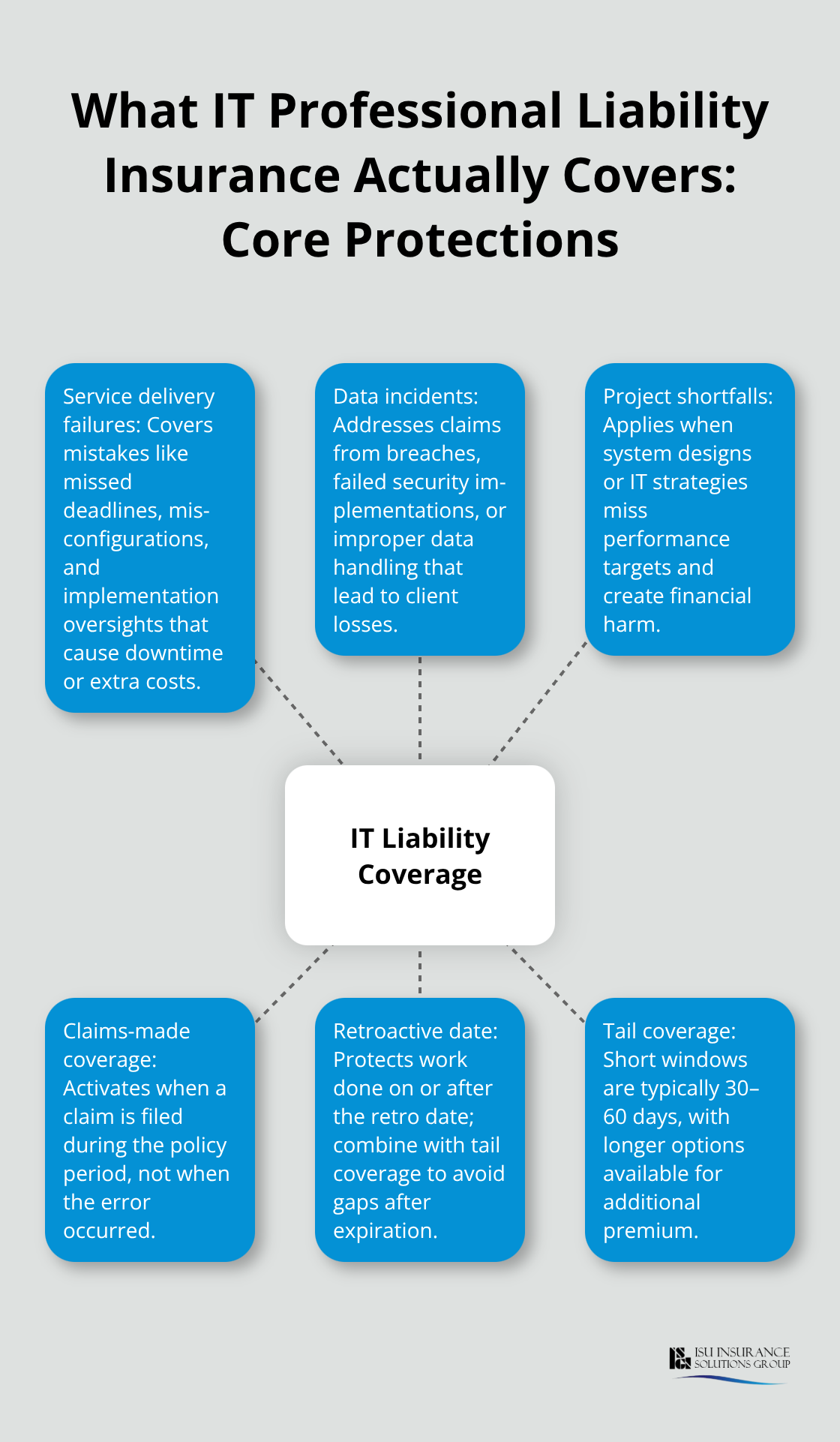

What IT Professional Liability Insurance Actually Covers

IT professional liability insurance protects you against three categories of claims that damage your business most: service delivery failures, data incidents, and project shortfalls. The Hartford data shows technology professionals pay around $146 per month on average for this coverage, reflecting the real risk exposure in IT work.

Most policies operate on a claims-made basis, meaning coverage triggers when a client files a claim during your policy period, not when the error occurred. This matters because you need a retroactive date-typically the policy start date or earlier-to cover work you’ve already completed. Without it, past projects have no protection, which is why many IT consultants add extended reporting periods lasting 30 to 60 days (or longer for additional cost) after policy expiration.

Service Delivery Errors That Cost You

Missed deadlines, system misconfigurations, and implementation oversights generate the most common claims in IT professional liability. A software implementation that causes client downtime or requires expensive change orders triggers a claim for defense costs and settlements. Your policy covers attorney fees, expert witnesses, and court expenses-costs that easily exceed $50,000 before any judgment. Poor documentation compounds these claims; if you cannot prove you delivered what was promised or followed industry standards, your defense becomes harder. Coverage limits matter here: The Hartford offers options ranging from $250,000 to $2,000,000 per claim, and you should choose the right limit based on your typical project value and client contract requirements. Architects and engineers, who face similar liability exposure, average around $140–$240 per month for professional liability, suggesting IT consultants handling infrastructure work should lean toward higher limits rather than lower ones.

When Projects Fail and Clients Lose Money

System design flaws that fail to meet performance projections or IT strategy recommendations that produce financial losses fall under most professional liability policies. A failed security implementation or incompatible software deployment that disrupts revenue is exactly what this insurance handles. The difference between general liability and professional liability matters here: general liability covers bodily injury and property damage, while professional liability covers the financial losses from your professional mistakes. Professional liability costs scale with the complexity and client impact of your work. The moment a client sends a written complaint or hints at legal action, you must notify your insurer immediately. Delays in notification can jeopardize your claim, and insurers assign a claims adjuster to manage your defense once they accept coverage.

Coverage Triggers and Policy Mechanics

Your policy’s retroactive date determines which past work qualifies for protection. Claims filed during your active policy period receive coverage if the work occurred on or after that retroactive date. Extended reporting periods (also called tail coverage) allow you to report claims after your policy expires, typically for 30 to 60 days, though you can purchase longer periods for additional premium. This protection matters when you leave the industry, sell your practice, or switch carriers-without tail coverage, claims filed after expiration have no protection. The Hartford and other carriers structure these options to fit different business transitions, so you should discuss your specific situation with an agent to avoid coverage gaps.

Why Your IT Business Faces Real Liability Exposure

The Financial Reality of IT Service Failures

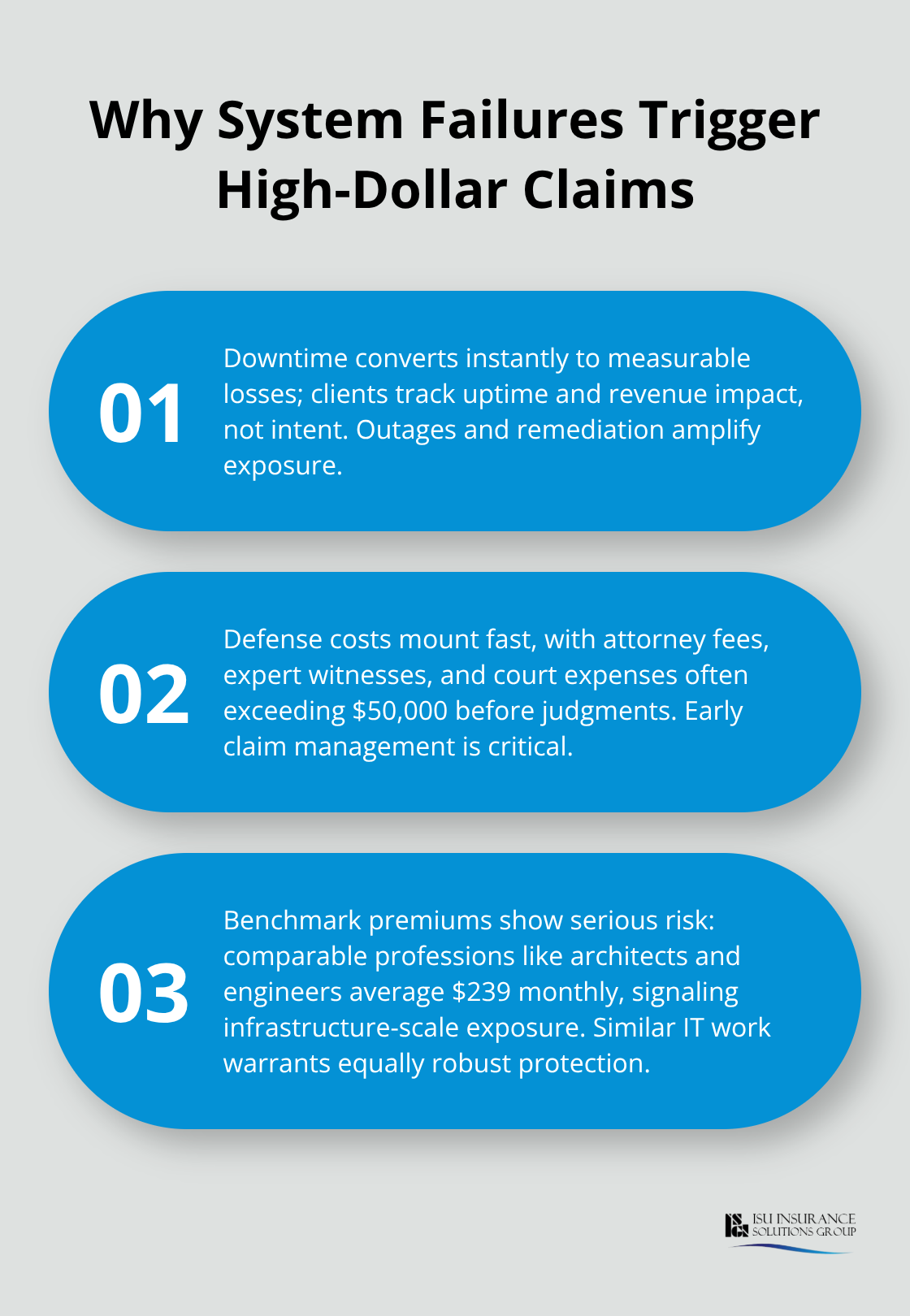

IT work creates multiple pathways to financial disaster that general liability cannot address. The Hartford data shows technology professionals pay around $146 per month for this coverage, reflecting genuine operational risk. When a client’s system fails and they lose revenue, when your implementation causes compliance violations, or when a security gap exposes their data, they will pursue you for damages. These are not hypothetical scenarios-they happen regularly enough that the insurance industry has priced them into standard coverage. Your professional liability policy exists because the financial impact of a single failed project often exceeds what most IT consultants can absorb alone. A missed deadline that costs a client $100,000 in lost productivity becomes your legal battle, and defense costs alone can reach $50,000 before any settlement.

System Failures Drive the Largest Claims

System failures and downtime claims dominate the liability landscape because clients measure IT performance in dollars and uptime percentages, not intentions. When your implementation causes network outages, disrupts revenue-generating operations, or requires expensive remediation, the client calculates their losses and their legal team calculates your exposure.

A software implementation that causes client downtime or requires expensive change orders triggers a claim for defense costs and settlements. Your policy covers attorney fees, expert witnesses, and court expenses-costs that easily exceed $50,000 before any judgment. The Hartford reports that architects and engineers (professionals with similar service-delivery risk) pay $239 monthly on average, suggesting that IT infrastructure work justifies equally serious protection.

Regulatory Fines and Compliance Violations Add Hidden Risk

Regulatory fines and compliance violations add another layer of risk that many IT consultants underestimate. A failed security audit, improper data handling, or missed compliance requirement during your work can trigger both client lawsuits and regulatory penalties. Your professional liability policy covers the defense costs and settlements from these disputes, but only if you have adequate limits and proper retroactive dating. Coverage limits matter enormously here-The Hartford offers $250,000 to $2,000,000 per claim options, and you should choose based on your typical project scope and client contract terms, not just what feels affordable. Many IT consultants operating in regulated industries or handling sensitive client data should seriously consider limits at the $1,000,000 level or higher.

Taking Action When Disputes Emerge

The moment any client dispute becomes a written complaint, you must notify your insurer immediately. Delays in notification jeopardize your entire claim, and insurers assign claims adjusters specifically to manage your defense and protect your interests once coverage is triggered. Your policy’s retroactive date determines which past work qualifies for protection-claims filed during your active policy period receive coverage if the work occurred on or after that retroactive date. Extended reporting periods (also called tail coverage) allow you to report claims after your policy expires, typically for 30 to 60 days, though you can purchase longer periods for additional premium. This protection matters when you leave the industry, sell your practice, or switch carriers-without tail coverage, claims filed after expiration have no protection.

Understanding your exposure is the first step, but selecting the right coverage limits and policy structure requires careful evaluation of your specific business operations and client relationships.

Selecting Coverage Limits That Match Your Actual Exposure

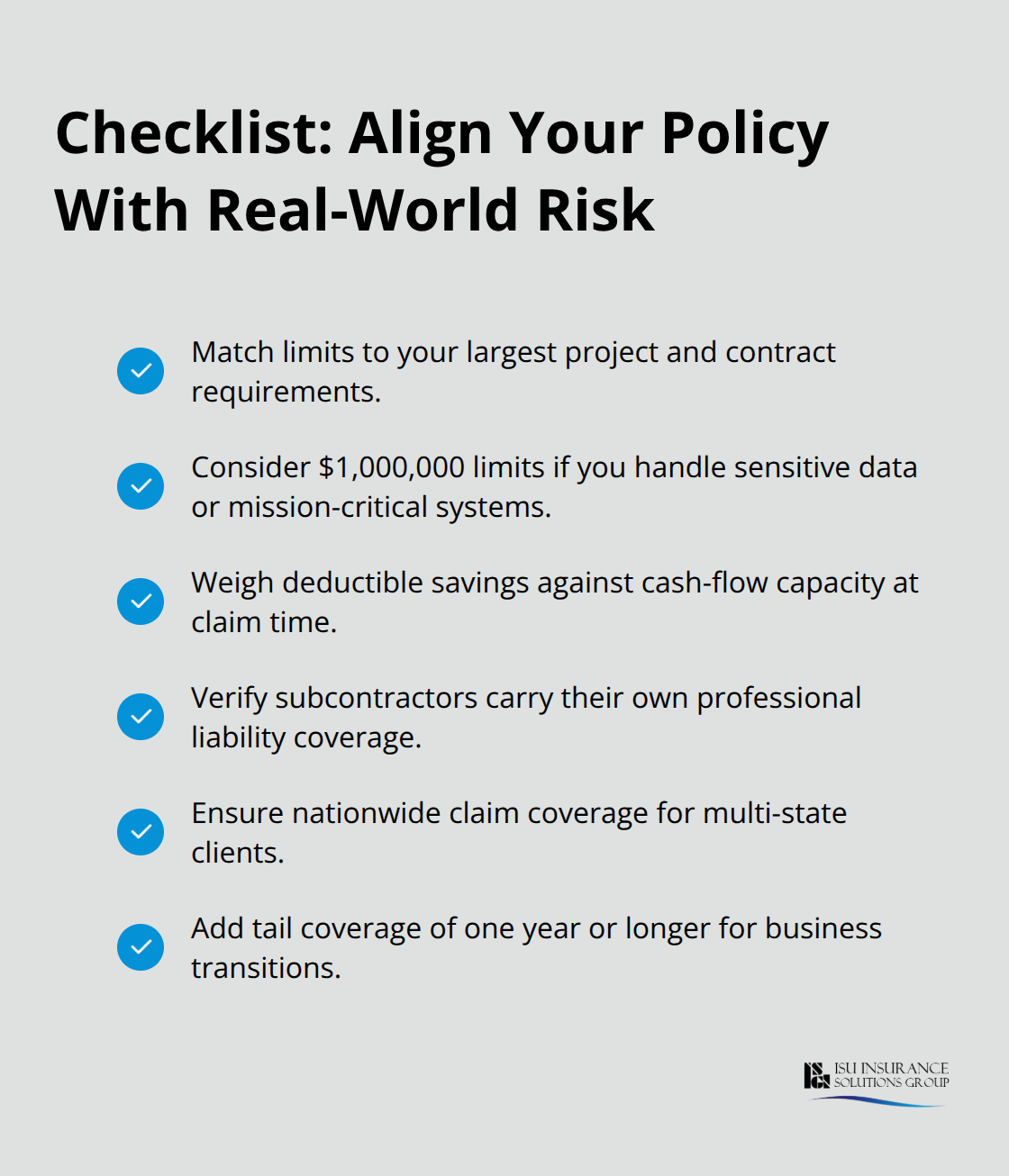

Choosing the right professional liability policy starts with matching your coverage limits to the financial stakes of your work, not to what feels comfortable. The Hartford offers per-claim limits ranging from $250,000 to $2,000,000, and this range exists because IT consultants operate across vastly different risk profiles. If you manage infrastructure for mid-market companies, handle sensitive client data, or implement mission-critical systems, a $250,000 limit is dangerously low. A single failed deployment that costs a client $500,000 in lost productivity exposes you to a judgment far beyond your policy’s protection.

Match Coverage Limits to Your Project Value

General IT professionals average professional liability coverage premiums starting at $50 monthly according to industry data. The premium difference between a $500,000 limit and a $1,000,000 limit is often 20 to 30 percent, yet that extra coverage prevents catastrophic personal liability if a claim exceeds your initial limit. Start by reviewing your largest client contracts and identify the financial exposure each project represents. If your typical engagement generates $100,000 in client revenue, your coverage should protect against losses at least double that amount.

Set Your Deductible Based on Cash Flow Reality

Your deductible selection directly impacts your monthly premium. Choosing a $5,000 deductible instead of $1,000 can reduce your monthly cost by 15 to 25 percent, but this strategy only works if you can genuinely absorb that out-of-pocket expense when a claim arrives. Many IT consultants underestimate how quickly legal defense costs accumulate before any settlement discussion occurs. Attorney fees, expert witnesses, and court expenses easily exceed $50,000 in the first few months of a dispute, meaning your deductible should not force you into financial stress during the claims process.

Account for Business Size and Subcontractor Risk

Your business size and employee count significantly affect both your premium and your coverage needs. The Hartford notes that more employees increase premiums because more people can make mistakes that trigger claims. A solo consultant operating from home faces different exposure than a 20-person IT services firm managing enterprise clients. If you employ subcontractors, confirm whether your policy covers their work or whether they need separate professional liability insurance. Most policies require subcontractors to carry their own coverage rather than extending protection under your policy, which creates a critical gap if you fail to verify their insurance status before assigning them client work.

Expand Coverage for Multi-State Operations

State-specific legal costs and regulatory requirements shape your coverage decisions. If you operate in multiple states or serve clients across different jurisdictions, confirm that your policy covers nationwide claims and includes provisions for varying state compliance standards. The Hartford offers options for customizing limits and terms based on your specific risk profile, so contact an agent to discuss your particular service offerings and client base rather than selecting standard limits off a rate card. When you transition your business, sell your practice, or switch insurance carriers, extended reporting periods become essential. A 30-day tail coverage period is minimal and leaves you vulnerable to claims filed just beyond that window. Purchasing tail coverage for one year or longer costs additional premium but provides genuine protection when business changes occur.

Final Thoughts

IT professional liability insurance protects your business from the financial devastation that follows a single failed project, missed deadline, or compliance violation. Your coverage needs depend on your project scope, client base, and the financial stakes of your work-a $250,000 limit works for solo consultants handling small implementations, but IT professionals managing enterprise systems or handling sensitive data should seriously consider $1,000,000 or higher. Your deductible selection matters equally, as choosing a $5,000 deductible saves premium money only if you can absorb that cost when a claim arrives without jeopardizing your business operations.

An online quote takes less than an hour and reveals exactly what your IT professionals liability insurance costs based on your specific risk profile. You’ll need basic information about your business structure, employee count, annual revenue, and the types of services you deliver, and most carriers offer online quotes that let you customize coverage limits and deductibles before committing to anything. Extended reporting periods deserve serious attention during the quote process-if you plan to transition your business, sell your practice, or change carriers, tail coverage lasting one year or longer prevents claims filed after policy expiration from leaving you unprotected.

An independent agent changes the entire process by accessing multiple insurers and finding the combination of coverage, limits, and price that actually fits your business. Contact ISU Insurance Solutions Group today to discuss your IT professional liability insurance needs and receive quotes that reflect your real business risk.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.