Auto Insurance Bundle Discounts: Save More on Your Policy

Most people don’t realize that auto insurance bundle discounts can cut their premiums by 15% to 25%. At ISU Insurance Solutions Group, we’ve helped countless customers lower their costs by combining policies strategically.

The right bundling approach depends on your specific situation and which carriers offer the best rates for your needs. This guide walks you through how bundling works and where you can find real savings.

How Bundling Actually Works

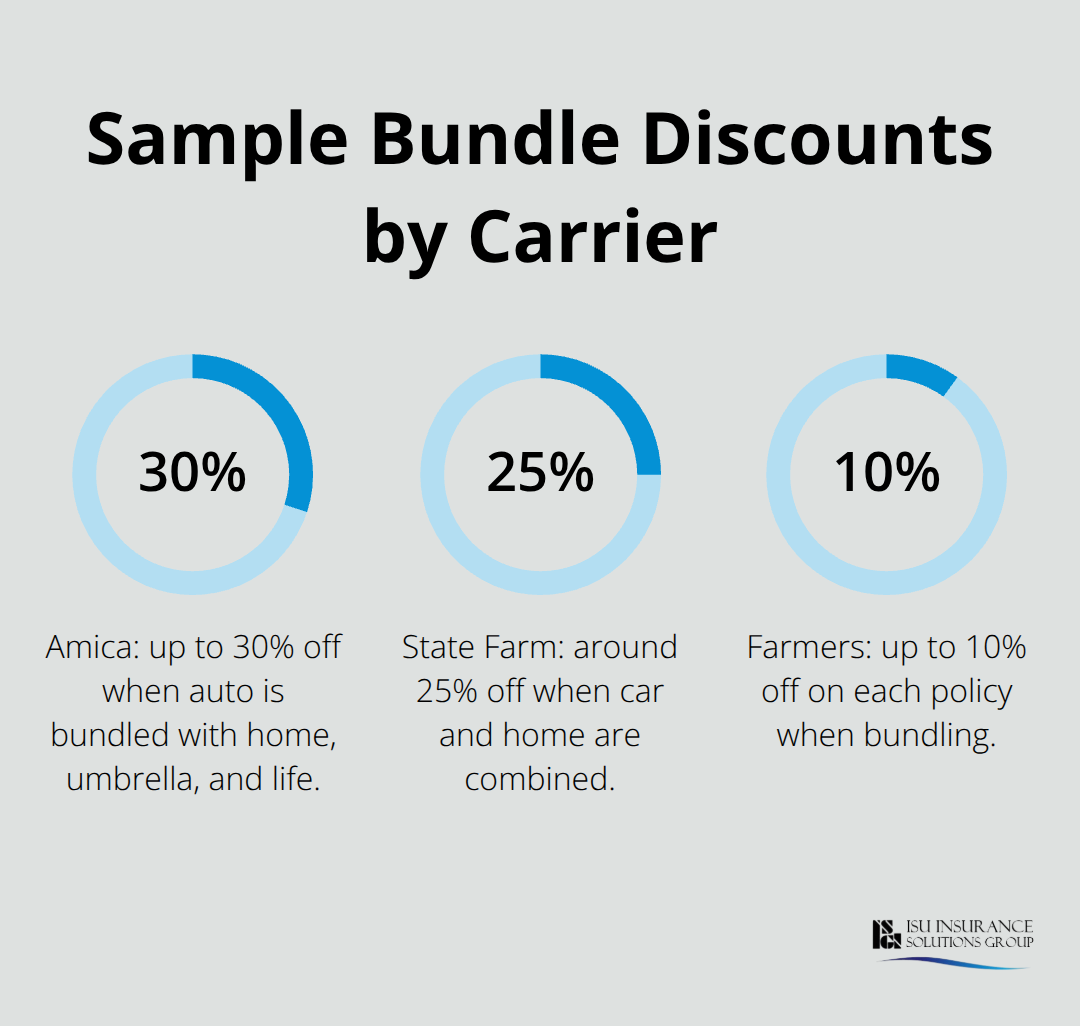

Bundling isn’t a mystery. When you combine auto insurance with another policy-typically home or renters-your carrier applies a multi-policy discount to your total premium. According to Mercury Insurance, bundling saves customers between 10% and 25% on average, though some carriers push higher. Amica offers up to 30% off auto when bundled with home, umbrella, and life insurance. State Farm averages around 25% off car and home combined.

Carriers offer these discounts for a straightforward reason: they want your entire insurance relationship. Managing one customer across multiple lines costs them less than acquiring and servicing separate customers, so they pass savings to you. The discount applies immediately when you add a second eligible policy, with no waiting period. If you currently have auto insurance with one company and home with another, you’re likely leaving money on the table. The gap between what you’re paying now and what a bundle could cost you is real money-potentially $950 per year or more, depending on your location and coverage selections, according to Liberty Mutual’s bundling data.

What Actually Gets Discounted

The discount applies to your total premium, not just one policy. If your auto policy costs $1,200 annually and home costs $1,000, a 20% bundle discount reduces your combined cost from $2,200 to $1,760. This matters because some people mistakenly think the discount applies only to the cheaper policy.

Beyond the percentage discount, bundling prevents coverage gaps that create real problems during claims. When both policies sit with the same carrier, deductibles, liability limits, and endorsements align automatically. During a weather event or accident, you won’t face conflicting interpretations from two different adjusters. One carrier coordinates the entire claim, which streamlines the process significantly. Some carriers sweeten the deal further. USAA, for military families, waives home deductibles for combat-related losses when both auto and home are bundled. Farmers Insurance adds accident forgiveness and rideshare coverage options to bundled policies. These aren’t minor add-ons-they represent genuine protection upgrades that cost extra if purchased separately.

Building Your Bundle Strategy

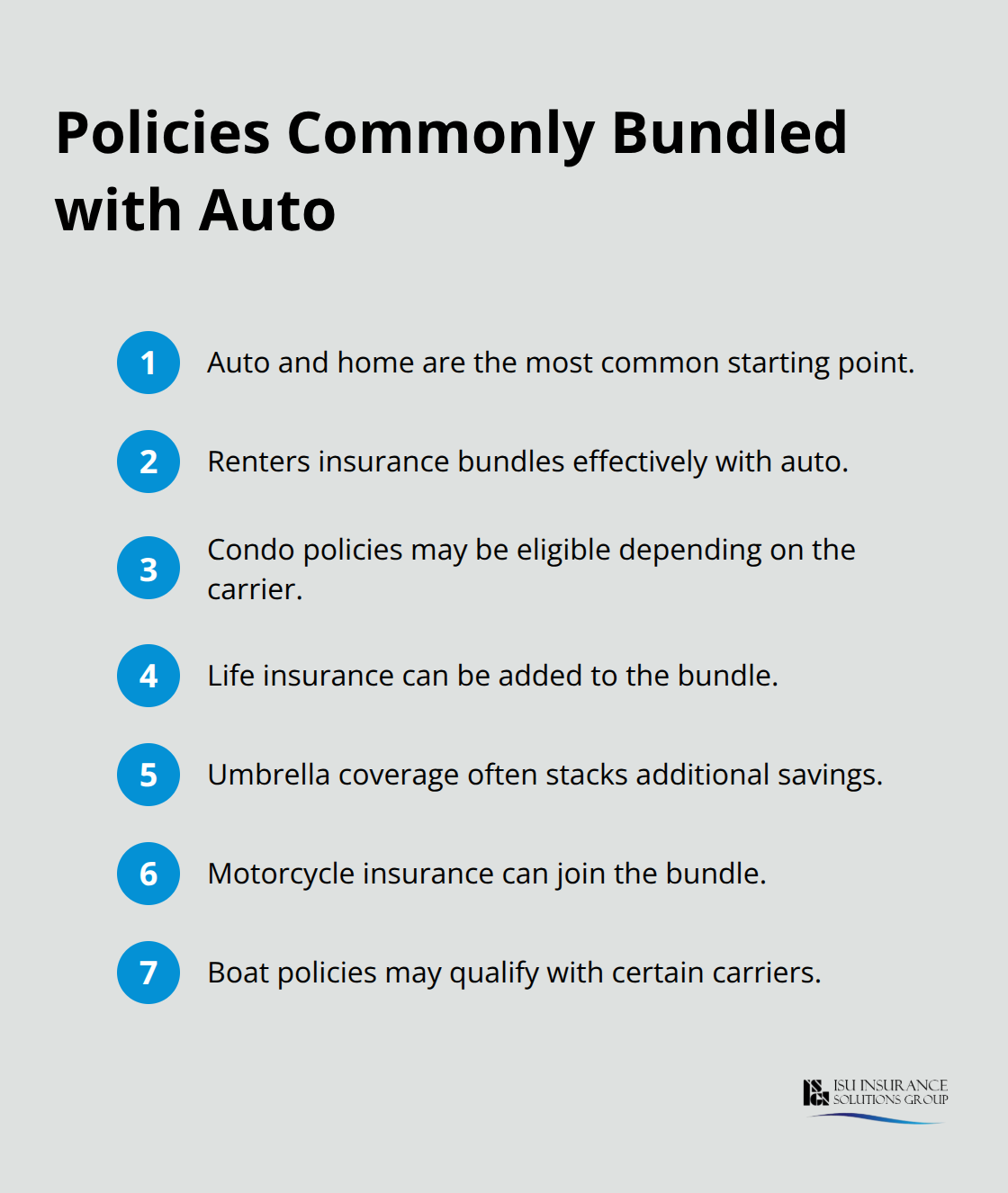

Start with listing what you actually need to insure. Most people begin with auto and home, but bundling extends to renters, condo, life, umbrella, motorcycle, and boat policies depending on your carrier. Liberty Mutual lets you add any eligible policy to an existing one and immediately receive the multi-policy discount.

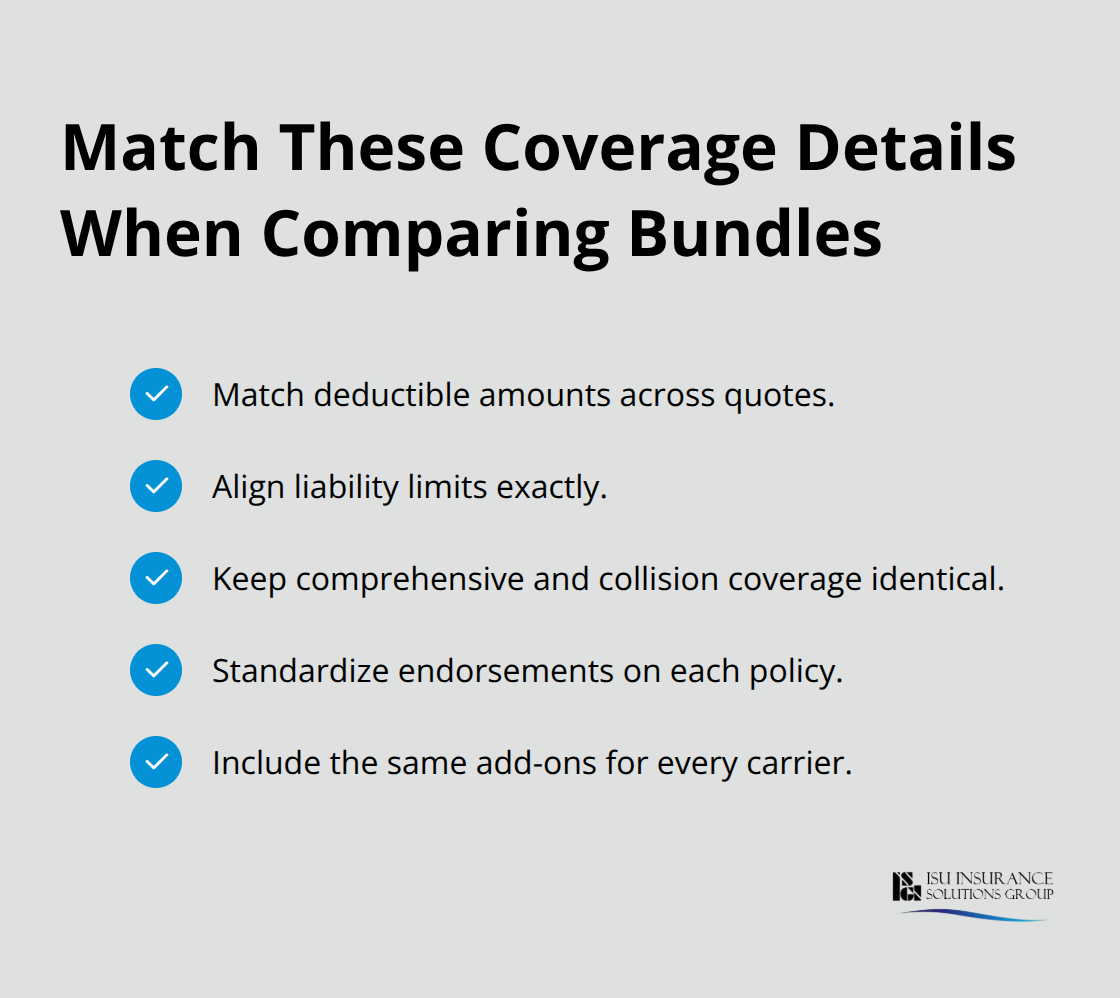

The critical step involves comparing quotes with identical coverage limits and deductibles across carriers. Don’t compare a $500-deductible home policy from one company against a $1,000-deductible policy from another-that’s not an apples-to-apples comparison. Align your policy start and end dates so renewals happen together, preventing gaps in coverage and simplifying your payment schedule. If you currently have separate policies, check when each renews before consolidating. Canceling mid-term triggers pro-rated refunds, but timing matters to avoid any lapse in coverage.

Getting the Right Quotes

An independent agent can pull quotes from multiple carriers simultaneously, saving you hours of phone calls. Not every carrier offers every discount or coverage type, so the cheapest auto option might not be the cheapest when bundled with home. An agent who works with multiple carriers (rather than just one) can show you which bundle actually saves you the most money for your specific situation and location.

Types of Policies You Can Bundle with Auto Insurance

Home and Homeowners Insurance

Home and homeowners insurance represents the most straightforward bundling choice, and for good reason. When you combine auto with homeowners coverage, carriers typically discount both policies. State Farm averages nearly 25% off car and home combined, while Amica pushes higher with up to 30% off when you add umbrella and life insurance to the home-auto foundation. The math works because your home is your largest asset and your car is your second-largest, so carriers view bundling these two as a complete risk picture.

If you rent instead of owning, renters insurance bundles just as effectively with auto. The discount applies identically, and renters policies cost significantly less than homeowners, so your total bundle premium drops faster. Condo owners should verify their carrier covers condo policies in bundle discounts, since some restrict bundling to traditional homeowners policies.

The practical advantage of bundling home or renters with auto goes beyond the percentage discount. Your renewal dates align, your deductibles coordinate, and claims involving both policies move faster because one adjuster handles everything rather than two carriers playing phone tag during a stressful situation.

Life Insurance and Umbrella Coverage

Life insurance and umbrella coverage take bundling further. Amica specifically offers substantial savings when you add life and umbrella to an auto-home bundle, recognizing that customers protecting their families comprehensively deserve meaningful discounts. Umbrella policies sit above your auto and home coverage, protecting you when liability claims exceed those underlying limits.

Most people underestimate how quickly a serious accident can exceed standard liability limits, so umbrella coverage matters more than it appears. When bundled, the umbrella discount stacks with your auto-home savings, and the carrier ensures your umbrella limits align perfectly with your underlying coverage.

Commercial Auto for Business Vehicle Owners

Business insurance for vehicle owners operates differently. If you use your vehicle for business purposes-rideshare, delivery, contractor work-standard personal auto policies exclude those uses entirely. Commercial auto insurance becomes necessary, and bundling commercial auto with your personal home policy still qualifies for multi-policy discounts at many carriers.

Farmers Insurance, for example, provides up to 10% off on each policy when bundling, making commercial auto bundling viable for self-employed individuals and small business owners who previously thought bundling wasn’t an option. The key is disclosing business use upfront. Failing to do so voids your coverage, leaving you uninsured during the activity that matters most.

An independent agent can help you identify which policies qualify for bundling at your carrier and whether commercial auto bundling makes financial sense for your situation. The next step involves comparing quotes across multiple carriers to see which bundle actually delivers the greatest savings for your specific coverage needs and location.

How to Actually Compare Bundle Quotes

Match Every Coverage Detail

Comparing bundle quotes across carriers fails when you pick the cheapest option without verifying that you’re comparing identical coverage. One quote might include a $500 home deductible while another uses $1,000. One auto policy might have $100,000 liability limits while another has $300,000. These aren’t the same products, and a $200-per-year savings on a policy with half the coverage isn’t actually savings-it’s a trap.

When you compare, match every coverage detail: deductible amounts, liability limits, comprehensive and collision coverage, endorsements, and any add-ons. This apples-to-apples approach takes more time upfront but prevents costly mistakes later.

Work with an Independent Agent for Multi-Carrier Quotes

The most efficient approach involves using an independent agent who works with multiple carriers simultaneously. Instead of spending three hours calling different companies, an agent pulls quotes from 10+ carriers in one session with identical coverage specifications. This matters because some carriers excel at auto rates while others dominate home pricing. State Farm might beat everyone on combined auto-home pricing, but Amica could offer better umbrella discounts when you add that third policy.

An independent agent shows you which combination actually saves the most money for your specific situation and location, not just which single policy is cheapest. A local agent can compare policies from multiple carriers to deliver personalized quotes that fit your actual needs and budget.

Coordinate Your Policy Renewal Dates

Timing your bundling decision requires strategic thinking about policy renewal dates. If your auto renews in March and home renews in August, bundling creates a coordination problem. You pay two separate premiums on two schedules, and you miss the benefit of aligned renewals.

Before switching carriers, check when each current policy renews. If you’re bundling policies currently with different companies, coordinate the start dates so both renew together going forward. This prevents coverage gaps when you cancel one policy before the other begins. Some carriers allow you to start a new policy mid-month to align renewal dates, which costs a few extra dollars in pro-rated premiums but eliminates months of administrative friction.

Conduct Annual Coverage Reviews

After bundling, review your coverage annually during renewal to confirm you still have adequate protection. Life changes-you buy a second vehicle, your home value increases, you purchase expensive equipment for work. Your bundle discount stays locked in, but your coverage needs may have shifted.

An independent agent can conduct a policy review in 20 minutes, identify gaps, and suggest adjustments without pressure to switch carriers. This annual check prevents the costly mistake of keeping outdated coverage just because you bundled years ago.

Final Thoughts

Auto insurance bundle discounts typically save you between 15% and 25% annually, though some carriers push higher with options reaching 30% when you add umbrella and life insurance. That translates to real money in your pocket-potentially $950 per year or more depending on your location and coverage selections. Beyond the percentage discount, bundling eliminates coverage gaps, aligns your deductibles and liability limits, and streamlines claims handling when accidents happen.

The right auto insurance bundle discounts depend entirely on your specific situation. Your carrier matters, your location matters, and which policies you actually need matters. State Farm averages around 25% off combined auto and home, while Amica reaches up to 30% when you add umbrella and life insurance to your bundle. Farmers Insurance provides up to 10% off each policy when bundling, and these aren’t theoretical numbers-they represent what real customers save when they consolidate their coverage strategically.

An independent agent accelerates this process significantly by pulling quotes from 10+ carriers simultaneously with identical coverage specifications. Rather than calling multiple companies yourself, an agent reveals which combination actually works best for your situation and location. Contact ISU Insurance Solutions Group to explore your bundle options and find the coverage combination that protects your family while lowering your total premium.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.