Understanding Auto Insurance Coverage Options for Every Driver

Most drivers pick auto insurance coverage options without really thinking it through. They either go with the bare minimum to save money or grab whatever their agent suggests.

At ISU Insurance Solutions Group, we’ve seen how the wrong choices cost drivers thousands in unexpected expenses. This guide walks you through each coverage type, how to match it to your situation, and the mistakes that could drain your wallet.

What Each Coverage Type Actually Covers

Liability coverage forms the foundation of every auto insurance policy, and it’s the only coverage legally required in California and most states. It splits into two parts: bodily injury liability covers medical expenses, lost wages, and legal defense if you injure someone in an accident you cause, while property damage liability pays for damage to their vehicle or property. The average bodily injury claim in 2024 reached $28,278 according to ISO and Verisk data, which shows why state minimums often fall dangerously short. If you cause a serious accident and your limits are $15,000 per person (California’s minimum), you become personally liable for anything above that amount. Try carrying at least $100,000 per person in bodily injury coverage if you have any assets to protect. Property damage claims average $6,770, so $50,000 limits provide reasonable protection without excessive cost.

Collision and Comprehensive Protection

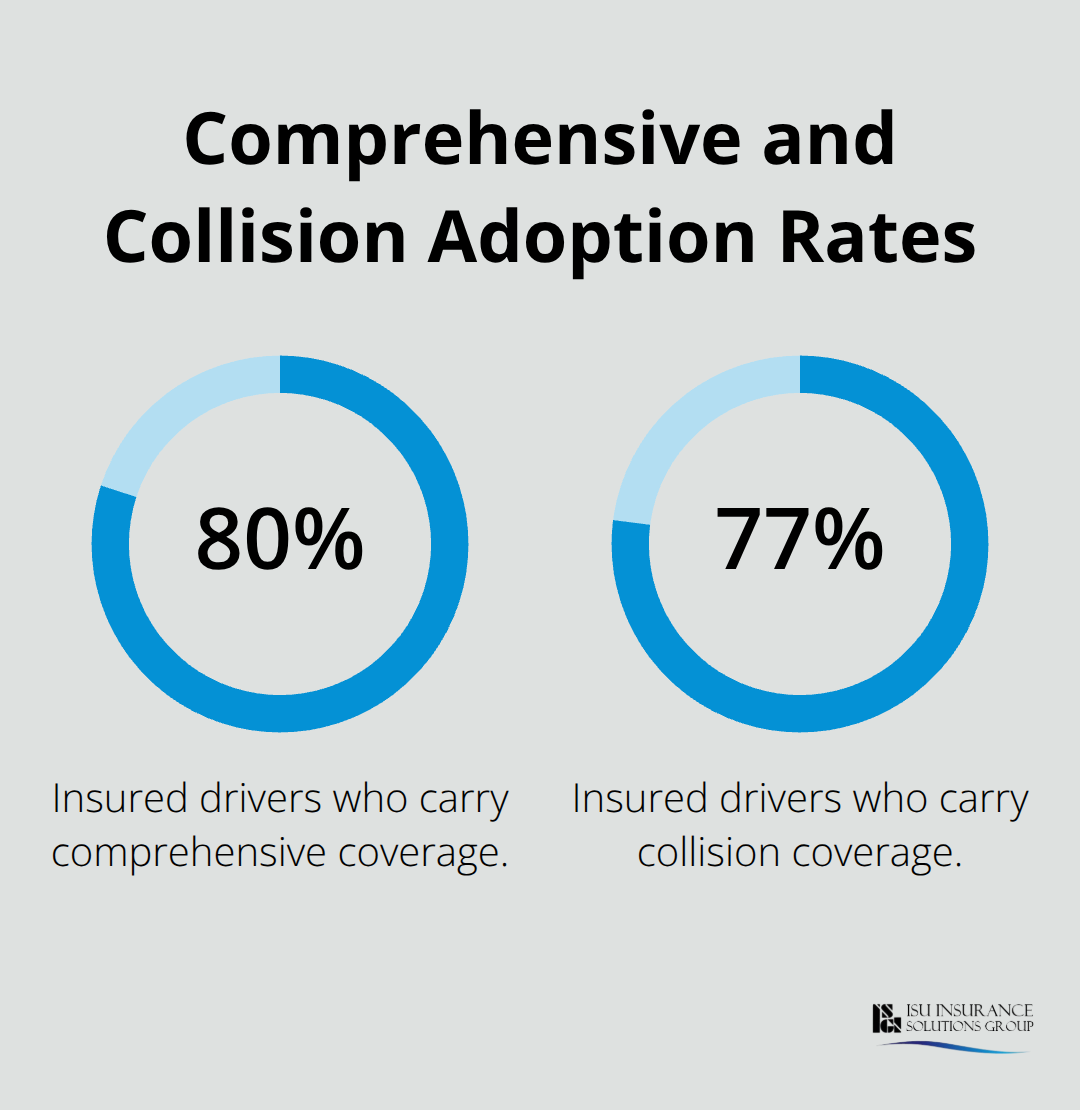

Collision coverage pays for damage to your vehicle when you hit another car or object, covering everything from fender benders to rollovers and pothole damage. In 2024, collision claims occurred at a frequency of 4.16% with average payments of $5,489 per claim, according to ISO data. The critical decision here is your deductible-raising it from $500 to $1,000 can cut your premium significantly, but only if you can afford that out-of-pocket expense when a claim happens. Comprehensive coverage protects against non-collision damage like theft, fire, weather, vandalism, and animal strikes, with 2024 claim frequency at 3.95% and average payments of $2,306. This coverage matters most if you live in areas prone to hail or wildfires, or if your vehicle is financed or leased since lenders require it. About 80% of insured drivers carry comprehensive coverage and 77% carry collision, showing most recognize their value beyond legal requirements.

The Protection Gap Uninsured Motorists Create

Uninsured and underinsured motorist coverage fills a critical gap that liability doesn’t address. If an uninsured driver hits you and causes $20,000 in injuries, their missing insurance means you’re stuck unless you have this coverage. This protection applies regardless of fault, covering your medical bills and lost wages when the other driver can’t pay. Underinsured motorist coverage kicks in when the at-fault driver’s liability limits are too low to cover your actual damages. Given that uninsured drivers remain common on roads and medical costs continue climbing, this coverage is essential rather than optional. Medical payments coverage works alongside these protections by covering your passengers’ medical expenses immediately after an accident, regardless of fault, which is particularly important if you frequently drive family members or friends.

Evaluating Your Coverage Needs

Your driving habits and risk factors determine which coverages make sense for your situation. A driver who commutes 50 miles daily on congested highways faces higher collision risk than someone who drives locally on quiet streets. Your vehicle’s age and value also matter-if you own a paid-off car worth $5,000, collision coverage with a $1,000 deductible costs more than the protection provides. Financed or leased vehicles require collision and comprehensive coverage regardless of your preference, since lenders protect their investment. The next step involves matching these coverage types to your specific circumstances and budget constraints.

Matching Your Coverage to Your Actual Risk

State Minimums Fall Short of Real Claim Costs

Your state’s minimum liability requirements represent a floor, not a finish line. California requires just $15,000 per person in bodily injury liability, but the 2024 average bodily injury claim reached $28,278-nearly double the state minimum. If you cause an accident and your limits fall short, the injured party can pursue your wages and assets for years. Louisiana residents face the highest insurance costs at 2.62% of median income, while Idaho drivers enjoy the lowest at 0.96%, reflecting how geography, traffic density, and repair costs dramatically shift your actual risk exposure.

How Your Driving Patterns Affect Your Risk

Your commute distance matters more than most drivers realize. Someone driving 50 miles daily on congested highways faces collision frequencies around 4.16% with average payments of $5,489, while local drivers experience substantially lower exposure.

If you finance or lease your vehicle, your lender mandates collision and comprehensive coverage regardless of state law, so those decisions are already made for you. The real choice lies in your liability limits and deductible strategy.

Try $100,000 per person in bodily injury coverage and $50,000 for property damage if you own any assets-this costs only slightly more than minimums but shields you from devastating personal liability.

Deductible Strategy Controls Your Premium

Your deductible selection directly controls your premium without sacrificing protection. Raising your collision deductible from $500 to $1,000 can reduce your premium by 15-30% depending on your vehicle and location, but only choose this if you can actually pay $1,000 out of pocket when a claim occurs. For comprehensive coverage, deductibles rarely exceed $500, and the 3.95% claim frequency with $2,306 average payments makes this protection essential in hail-prone or wildfire-risk areas.

Vehicle age and value determine whether collision and comprehensive make financial sense. If your paid-off car is worth $5,000, a $1,000 collision deductible with a $600 annual premium wastes money since you’re unlikely to file a claim.

Credit History and Usage-Based Programs Impact Your Rates

Credit history influences your rates significantly-drivers with poor credit pay substantially higher premiums, so monitoring your credit report and maintaining stable finances directly lowers your costs. Usage-based insurance programs reward low mileage and safe driving habits, but review the terms carefully since risky behavior can trigger surcharges that offset savings.

Shopping Multiple Carriers Reveals Dramatic Price Differences

Shopping quotes annually across multiple carriers reveals dramatic price differences. The same coverage can cost 40-60% more with one insurer versus another, and bundling auto with home insurance frequently cuts premiums by 10-25%. Your decision framework should weigh your actual driving exposure, your assets requiring protection, and your emergency fund capacity against the deductible you select-then compare quotes from at least three carriers to confirm you’re getting competitive rates for that coverage level.

Once you’ve identified the right coverage mix and deductible strategy for your situation, the next step involves understanding the common mistakes that derail drivers’ insurance decisions and how to avoid them.

Common Mistakes Drivers Make When Selecting Auto Insurance

The Dangerous Math of Minimum Coverage

Most drivers who choose minimum liability coverage convince themselves they’ll never cause a serious accident. Then reality hits. In 2024, the average bodily injury claim reached $28,278 according to ISO and Verisk data, but California’s minimum liability limit sits at just $15,000 per person. That $13,278 gap becomes your personal debt if you cause that accident. You can’t discharge it in bankruptcy, and wage garnishment can follow for years. Drivers who skip uninsured motorist coverage face an equally brutal discovery when an uninsured driver hits them-their own medical bills suddenly become their problem entirely. You saved $300 annually on premiums, then faced $50,000 in uncovered medical expenses or property damage. The math fails spectacularly.

Raising your bodily injury limit from $15,000 to $100,000 per person costs roughly $15-25 more per month. You’d need to avoid accidents for five years just to break even on the premium difference-and one serious accident erases decades of savings. Property damage minimums of $25,000 are equally inadequate in today’s repair environment, where hitting a newer vehicle can easily exceed $10,000 in damage.

Overlooking Required and Low-Cost Protections

Comprehensive and collision coverage get skipped too, particularly on financed vehicles where drivers don’t realize their lender requires these protections. If your vehicle is financed or leased, collision and comprehensive aren’t optional-your lender mandates them to protect their investment. Dropping these coverages violates your loan agreement and leaves you personally liable for vehicle damage, which defeats the entire purpose of having insurance.

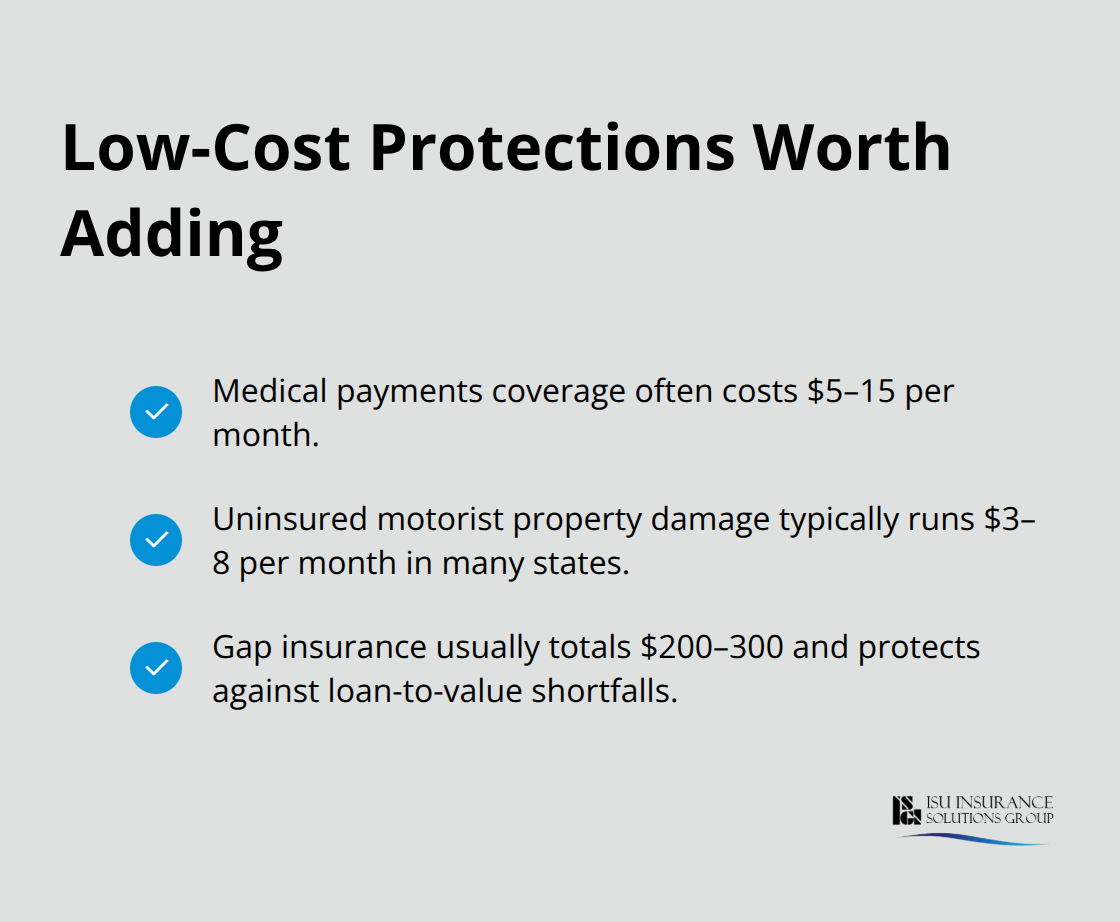

The second major mistake involves ignoring additional protections that cost almost nothing compared to their value. Medical payments coverage runs $5-15 monthly but covers your passengers’ medical expenses immediately after an accident, regardless of fault. Uninsured motorist property damage coverage, which pays for vehicle damage caused by uninsured drivers, costs $3-8 monthly in most states yet solves a genuine problem-uninsured drivers still exist on roads despite legal requirements.

Gap insurance matters significantly if you financed a vehicle, since it covers the difference between your loan payoff and your car’s actual cash value if it’s totaled. A driver financing a $35,000 vehicle with $32,000 remaining on the loan faces a $10,000 gap if the car is totaled and valued at $25,000-gap insurance costs roughly $200-300 total but prevents that exact scenario.

The Cost of Policy Neglect

Drivers who never review their policies miss rate changes, coverage gaps, and eligibility for discounts. Most drivers haven’t compared quotes in three or more years, which means they’re likely overpaying by 30-50% for identical coverage. Annual quote shopping across at least three carriers takes two hours and frequently reveals $400-800 in annual savings. Bundling auto with home insurance adds another 10-25% discount that many drivers simply never investigate. The pattern is clear: drivers make initial coverage decisions, then never revisit them, which means outdated assumptions and missed savings compound year after year.

Final Thoughts

Your auto insurance coverage options deserve serious attention because the wrong choices create financial exposure that lasts years. State minimums protect the other person, not you, and bodily injury claims averaging $28,278 in 2024 dwarf California’s $15,000 minimum. Carrying $100,000 per person in coverage costs roughly $15-25 monthly but shields your wages and assets from devastating liability.

Start reviewing your current policy by gathering your declarations page and comparing your liability limits against your actual assets. Check whether you’re paying for collision and comprehensive on a vehicle worth less than your deductible plus annual premiums combined, which wastes money. Then spend two hours shopping quotes from at least three carriers for identical coverage, which typically reveals 30-50% price differences for the same protection.

Contact ISU Insurance Solutions Group to review your current auto insurance coverage options and explore how competitive rates combined with personalized service can protect what matters most. Our local agents work hands-on with drivers to match coverage levels to their circumstances and budgets, then monitor your policy annually to capture rate changes and new discounts. Finding the right insurance partner means working with someone who listens to your driving habits and asset situation rather than pushing generic solutions.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.