Craft Brewery General Liability Essentials for Small Breweries

Craft breweries face real liability risks that most owners underestimate. From contaminated products to accidents during tastings, one claim can threaten your entire operation.

We at ISU Insurance Solutions Group work with breweries across the Pacific Northwest, and we’ve seen how the right general liability coverage makes the difference between a manageable incident and a business-ending lawsuit. This guide walks you through what protection you actually need.

Coverage Gaps That Put Craft Breweries at Risk

Your general liability policy has limits. Understanding where those limits fail protects your brewery from catastrophic exposure. Most owners assume GL covers everything-it doesn’t. The gap between what you think you’re protected against and what your policy actually covers is where claims become devastating.

Contaminated Beer and Product Defects Slip Through Standard Coverage

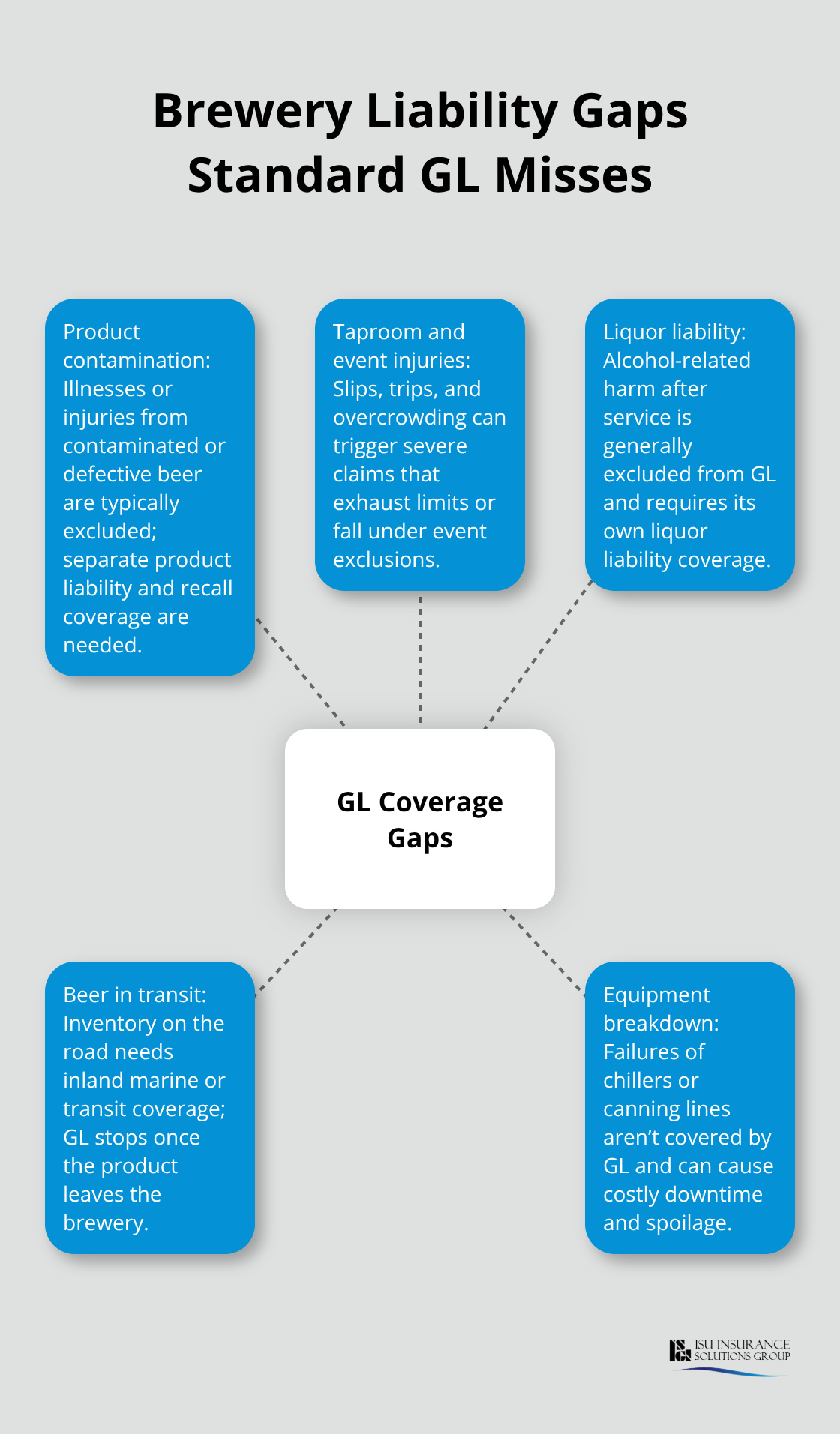

Contaminated beer creates liability that general liability policies routinely exclude. If a customer gets sick from a spoiled batch or discovers foreign material in a can, they will sue. Your standard GL policy won’t cover it because product liability insurance protects against claims arising from injuries or illnesses caused by contaminated or defective beer, but this coverage is separate from standard GL. A single product recall-whether from mold, bacterial contamination, or packaging errors-forces you to absorb disposal costs, customer notifications, and replacement inventory out of pocket.

The Beer Institute reports that over 350,000 kegs are stolen annually, costing roughly $50 million in losses across the industry. While keg theft represents a different exposure, it shows how much breweries lose when they lack comprehensive coverage. Without specific product recall coverage or spoilage protection, you pay for something that could have been insured.

Taproom and Event Injuries Reach Your GL Limits Fast

Your tasting room is a liability magnet. Slippery floors from spilled beer, tangled electrical cords near seating areas, and crowded events create conditions for serious injuries. A customer who trips over equipment and breaks a leg will have a claim that reaches your GL limits quickly. Medical expenses alone for a severe injury exceed $100,000 before legal costs enter the picture.

Events multiply your exposure. If you host weddings, fundraisers, or private parties, your standard GL policy may exclude large gatherings or require special event endorsements that you don’t have. NFPA occupancy guidelines determine how many people your space can safely hold, but many breweries ignore this and pack in crowds without adjusting their insurance. An injury during an overcrowded event gives your insurer grounds to deny the claim entirely, leaving you liable for the full amount. Liquor liability is a separate coverage that GL doesn’t touch-if alcohol is served and someone leaves your event intoxicated and causes harm, GL won’t defend you.

Equipment and Inventory in Transit Lack Protection

Once your beer leaves the brewery, GL coverage stops protecting it. Transit to distributors, retailers, or festivals requires inland marine or transit coverage-something most standard policies don’t include. A delivery truck hit by another vehicle destroys your inventory with no recovery available. Kegs damaged during loading represent a total loss you absorb alone.

Equipment breakdown during production creates another gap. A glycol chiller or canning line costs six figures to replace. Equipment failure without breakdown coverage means you absorb the entire replacement cost plus lost production time. Property damage liability during your own operations covers damage you cause to someone else’s property, but only up to your limits. Damage to a distributor’s facility or a retailer’s equipment caused by your delivery process can quickly exceed standard limits and leave you personally responsible.

These gaps explain why choosing the right coverage requires more than a standard GL policy. The next section walks you through what your brewery actually needs to stay protected.

What Craft Breweries Need in General Liability Coverage

Coverage Limits That Match Your Actual Exposure

A standard GL policy with $1,000,000 in coverage sounds adequate until a serious injury happens. For breweries in Washington and Oregon, that limit evaporates quickly when medical bills, legal defense costs, and court awards stack up. A customer who suffers a spinal injury from a fall in your tasting room will generate $200,000 to $500,000 in immediate medical expenses before litigation costs arrive.

If your GL limit sits at $1,000,000, one major claim consumes half your coverage with nothing left for additional incidents or punitive damages.

Breweries that operate taprooms or host events should carry a minimum of $2,000,000 in GL coverage, with $1,000,000 per occurrence and $2,000,000 aggregate. Breweries that host frequent events, weddings, or large gatherings should push toward $3,000,000 to $5,000,000 in total limits. Your actual number depends on how many people you pack into your space and how often.

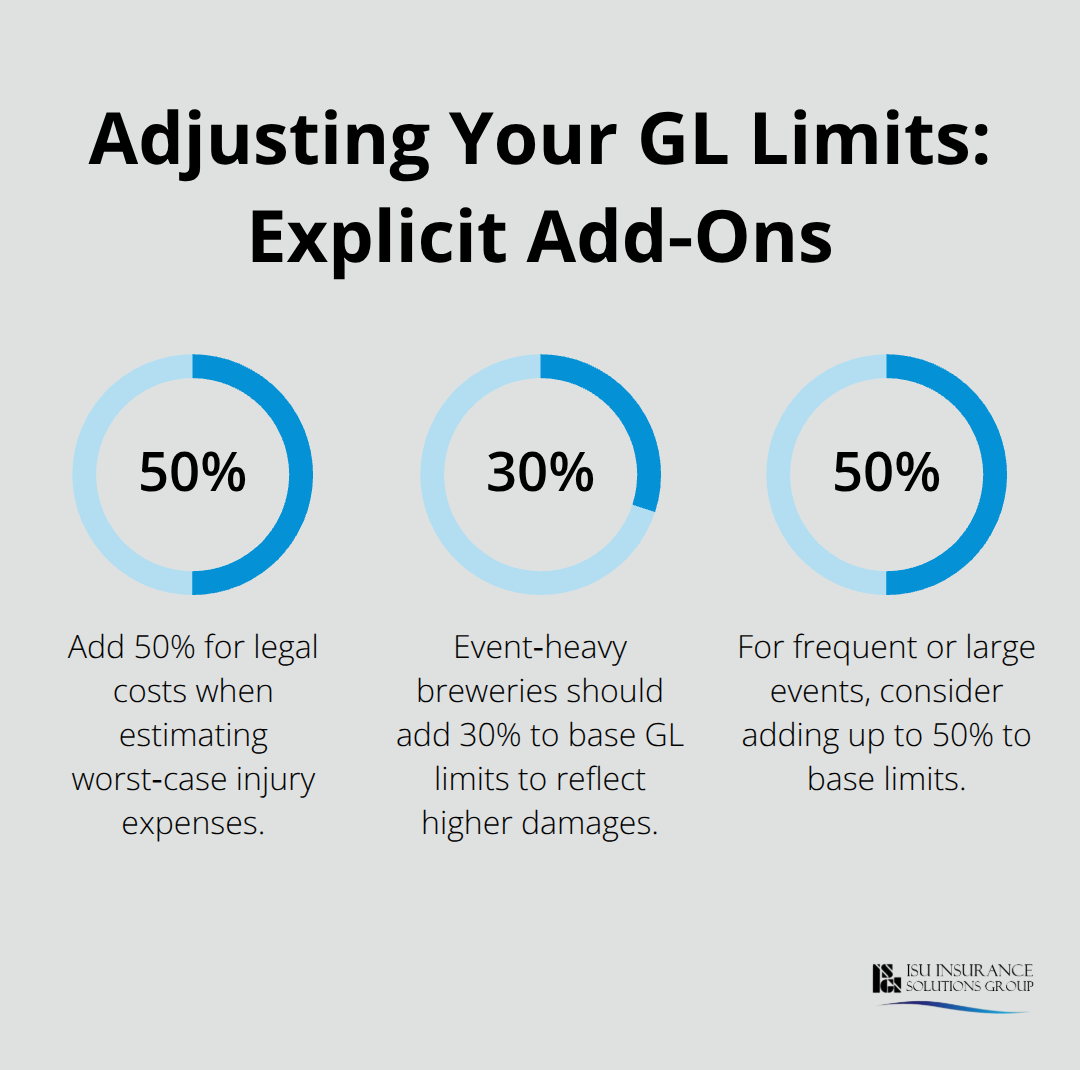

Calculate potential medical costs for your worst-case injury scenario-spinal cord damage, traumatic brain injury, or permanent disability-then add 50 percent for legal costs. That figure tells you what your limit should be. In Washington, regulators require Commercial General Liability insurance with minimum limits of $1,000,000 before you receive a license.

Event and Tour Coverage That Actually Protects You

Events and tours require specific protection that standard GL policies routinely exclude or severely limit. Your policy likely contains language that caps coverage during large gatherings or excludes events altogether. If you host a wedding with 150 guests and someone gets hurt, your insurer can deny the claim based on occupancy limits or event-related exclusions buried in the fine print.

A special events endorsement or separate special events policy explicitly covers the types of gatherings you run. This endorsement must list your brewery as the primary insured and include liquor liability protection if alcohol flows during the event. Without this protection, you absorb the full cost of any injury claim that occurs during your events.

Equipment and Inventory Protection Beyond Standard GL

Brewery-specific endorsements for equipment and inventory protect against equipment breakdown and spoilage losses that GL ignores. A glycol chiller failure during fermentation costs $150,000 to replace plus thousands in lost product. Equipment breakdown coverage reimburses replacement costs and covers extra expenses to keep production moving.

Spoilage and contamination coverage protects your inventory if temperature swings, power outages, or contamination destroy a batch. These endorsements transform your GL policy from a liability-only tool into a comprehensive protection plan that actually reflects how breweries operate and where they lose money. The right combination of coverages means you recover from equipment failures and contamination incidents instead of absorbing losses that threaten your operation.

Your GL policy forms the foundation of your brewery’s protection, but it only works when you pair it with the right endorsements and limits. The next section shows you how to evaluate carriers and policies to find coverage that actually matches your brewery’s specific risks.

How to Choose the Right Carrier and Policy

Match Coverage Limits to Your Production and Distribution Scale

Start with your production volume and distribution footprint. A brewery producing 500 barrels annually with sales limited to a three-county area faces different exposures than one producing 5,000 barrels and shipping across multiple states. Your GL limits should scale with your reach. A smaller operation with taproom-only sales needs $1,000,000 to $2,000,000 in coverage, while breweries distributing regionally should carry at least $1 million per incident with consideration for higher limits if events are frequent.

Calculate your actual risk with real numbers. Document how many people visit your facility monthly, how many events you host annually, and whether your distribution involves third-party logistics. Write these numbers down. Most brewery owners guess at their exposure rather than measuring it, which leads to underinsurance.

Your GL limit must account for worst-case medical scenarios specific to your operation. A customer who suffers a spinal cord injury from a fall in your tasting room could generate $300,000 to $1,000,000 in lifetime medical costs. Add legal defense expenses of $150,000 to $250,000, and your $1,000,000 limit disappears entirely. Breweries that host events should add 30 to 50 percent to their base limit because event claims tend toward higher damages.

If you operate in Washington, state licensing requirements mandate $1,000,000 minimum GL coverage before you receive approval. Oregon has similar expectations, though enforcement varies by county. Check your specific jurisdiction’s requirements before finalizing your limits.

Select Carriers With Actual Brewery Experience

The carrier you choose matters enormously because not all insurers understand brewery-specific risks equally. Many standard commercial carriers treat breweries like generic manufacturing operations and miss the nuances of taproom liability, equipment breakdown, and product contamination. You need a carrier with actual brewery experience who understands that a canning line failure isn’t just equipment damage-it’s lost production time, spoiled inventory, and potential customer defaults.

Travelers offers IndustryEdge craft brewery insurance specifically designed for food and beverage manufacturers, with specialized knowledge of equipment breakdown and spoilage coverage. Philadelphia Insurance, Nationwide, and Auto-Owners also serve brewery clients, though their depth of brewery expertise varies. An independent agency can quote multiple carriers in a single conversation, which saves you weeks of phone calls and ensures you compare apples to apples.

Demand Transparency on Policy Exclusions and Endorsements

When comparing carriers, demand transparency on what each policy excludes. Most GL policies contain standard exclusions for product liability, liquor liability, and equipment breakdown-you already know this. What matters is whether the carrier offers affordable endorsements to fill those gaps or forces you to purchase separate policies at inflated rates. A carrier charging $500 to add spoilage coverage through an endorsement is far superior to one requiring a $2,000 separate policy.

Ask each carrier specifically whether their standard GL excludes events and whether event coverage requires an endorsement or separate policy. Ask whether equipment breakdown, spoilage, and contamination coverage are available as add-ons. Ask whether liquor liability coverage is available through the same policy or requires a separate quote. Request sample policy language showing exactly what’s covered and what’s excluded-don’t accept summaries or verbal explanations.

Read the exclusions section carefully, not the summary. Exclusions buried in subsections often contradict what sales materials promise. A policy that claims to cover product liability but excludes contamination discovered more than 30 days after purchase creates a gap that destroys your protection in real claims.

Align Coverage Structure to Your Actual Operations

Your distribution method directly impacts which endorsements you need. If you distribute through wholesalers only, your transit exposure is lower than if you deliver directly to retailers or consumers. Direct distribution requires inland marine or transit coverage to protect beer in transit and during loading. If you operate a taproom with events, special events liability becomes non-negotiable. If you operate a production facility only with no taproom, your event exposure disappears but your equipment breakdown exposure increases.

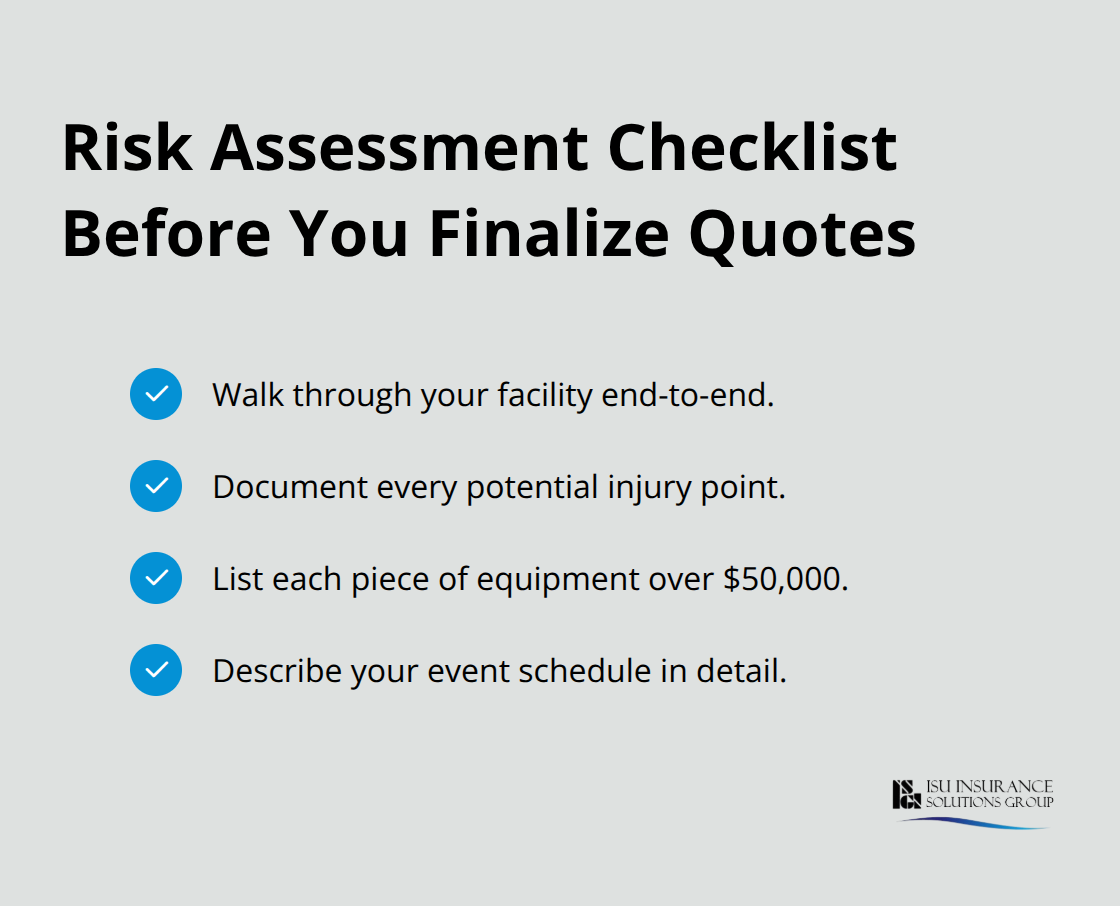

Match your coverage structure to how your brewery actually operates, not how you think it operates. Many owners purchase coverage based on assumptions, then discover gaps when claims arise. A detailed risk assessment before you finalize any quote protects you from this mistake-walk through your facility, document every potential injury point, list every piece of equipment over $50,000, and describe your event schedule in detail.

That assessment becomes the foundation for your coverage decisions and ensures you don’t purchase unnecessary coverage while missing critical gaps.

Final Thoughts

Craft brewery general liability coverage only protects your business when it matches your actual operations. Standard GL policies leave breweries exposed because they fail to account for taproom injuries, equipment failures, and product recalls. Adding the right endorsements and limits transforms your policy from a liability-only document into genuine protection that pays claims when they matter most.

An independent agent with brewery experience can quote multiple carriers in one conversation and compare exclusions side by side. You shouldn’t spend weeks calling carriers individually or guessing at coverage limits. A knowledgeable agent eliminates that burden and ensures you purchase adequate coverage without paying for unnecessary add-ons.

Contact ISU Insurance Solutions Group to discuss your brewery’s specific coverage needs and receive a multi-carrier quote that compares options side by side. Our local agents understand Pacific Northwest brewery operations and the liability exposures you face. Your brewery’s survival depends on having the right protection in place today.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.