Brewery Property Coverage Washington: Protecting Your Taproom and Tanks

Running a brewery in Washington means protecting assets that standard commercial insurance simply doesn’t cover. Fermentation tanks, brewing equipment, and thousands of dollars in inventory require specialized brewery property coverage in Washington.

At ISU Insurance Solutions Group, we work with breweries across Washington and Oregon to build protection plans that actually fit your operation. The risks you face-from equipment failures to fire hazards-demand more than generic policies.

Why Brewery Equipment Needs Different Protection

Washington breweries operate equipment that standard commercial policies simply refuse to cover or severely limit. Fermentation tanks, glycol cooling systems, canning lines, and pressure vessels represent hundreds of thousands of dollars in specialized assets that require dedicated protection. A glycol system failure at a mid-size facility triggers losses exceeding $100,000 when you account for spoilage, equipment repair, and lost production time. Standard property policies treat these as generic machinery, missing the reality that a single temperature control failure ruins entire batches of beer worth tens of thousands of dollars.

Equipment breakdown coverage specifically protects boilers, chillers, and refrigeration systems that are absolutely essential to brewing operations. Without this coverage, you face six-figure repair bills and production delays that stretch weeks or months. Washington’s craft beer industry contributes approximately $1.2 billion to the state’s economy, and that scale of operation demands insurance designed for manufacturing complexity, not retail simplicity. The Brewers Association reports that Washington has the second-largest hop acreage in the world and ranks fourth nationally for licensed breweries, meaning your inventory of raw materials and finished beer represents serious asset concentration.

Temperature Control Failures Cost More Than You Think

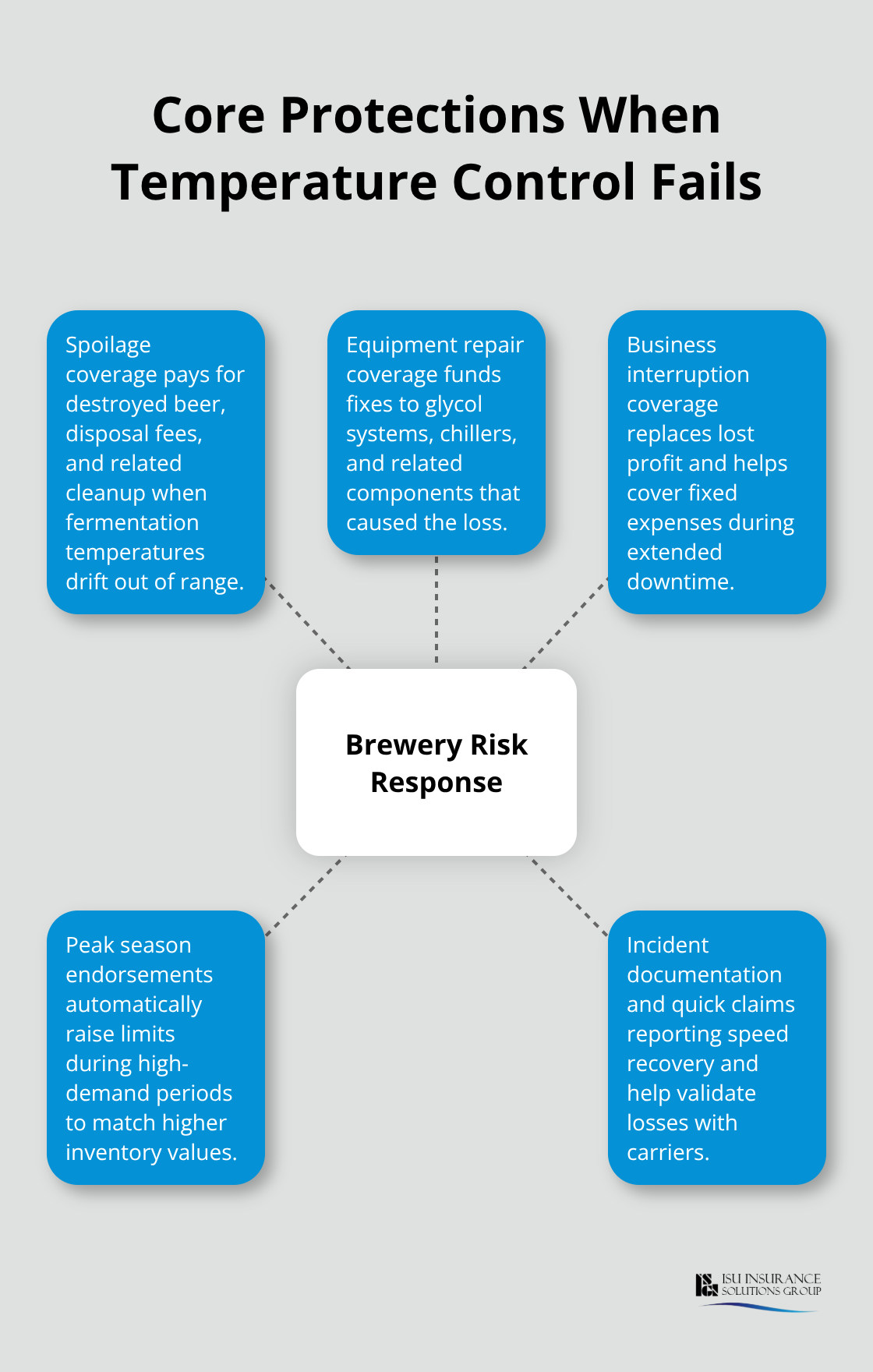

Glycol system failures represent the single most common and expensive claim in Washington breweries. These systems maintain fermentation temperatures within narrow ranges, and when they fail, you lose entire fermentation cycles instantly. Spoilage coverage that extends beyond standard property policies covers the cost of destroyed inventory, disposal fees, and lost production time while equipment repair occurs.

Replacement lead times for specialized tanks exceed 26 weeks, which makes business interruption coverage critical during extended downtime. Peak season endorsements adjust your coverage limits to reflect higher inventory values during peak demand periods, preventing underinsurance when you produce at capacity.

Regulatory Requirements Shape Your Coverage Obligations

Washington’s Liquor and Cannabis Board requires proof of Commercial General Liability insurance with minimum limits of $1,000,000 before you receive a license. The LCB also mandates liquor liability coverage specifically, which is a separate policy requirement from general liability. Local fire marshals impose additional requirements for facilities larger than 10,000 square feet, often requiring documented proof of adequate property and boiler coverage. Pierce County breweries face wastewater pollution-control requirements that affect environmental liability coverage needs.

These regulatory mandates are not optional suggestions-they are licensing prerequisites that directly influence which coverage types you must carry to remain compliant and operational. Your insurance decisions ultimately determine whether you can legally operate and whether you can recover from major losses. Understanding what regulators require helps you avoid coverage gaps that could cost your brewery its license or leave you unprotected after a catastrophic event. The next section examines the specific coverage types that protect your building, equipment, and inventory from the risks that actually threaten Washington breweries.

Building Real Protection Into Your Brewery Coverage

Foundation: Structure and Building Protection

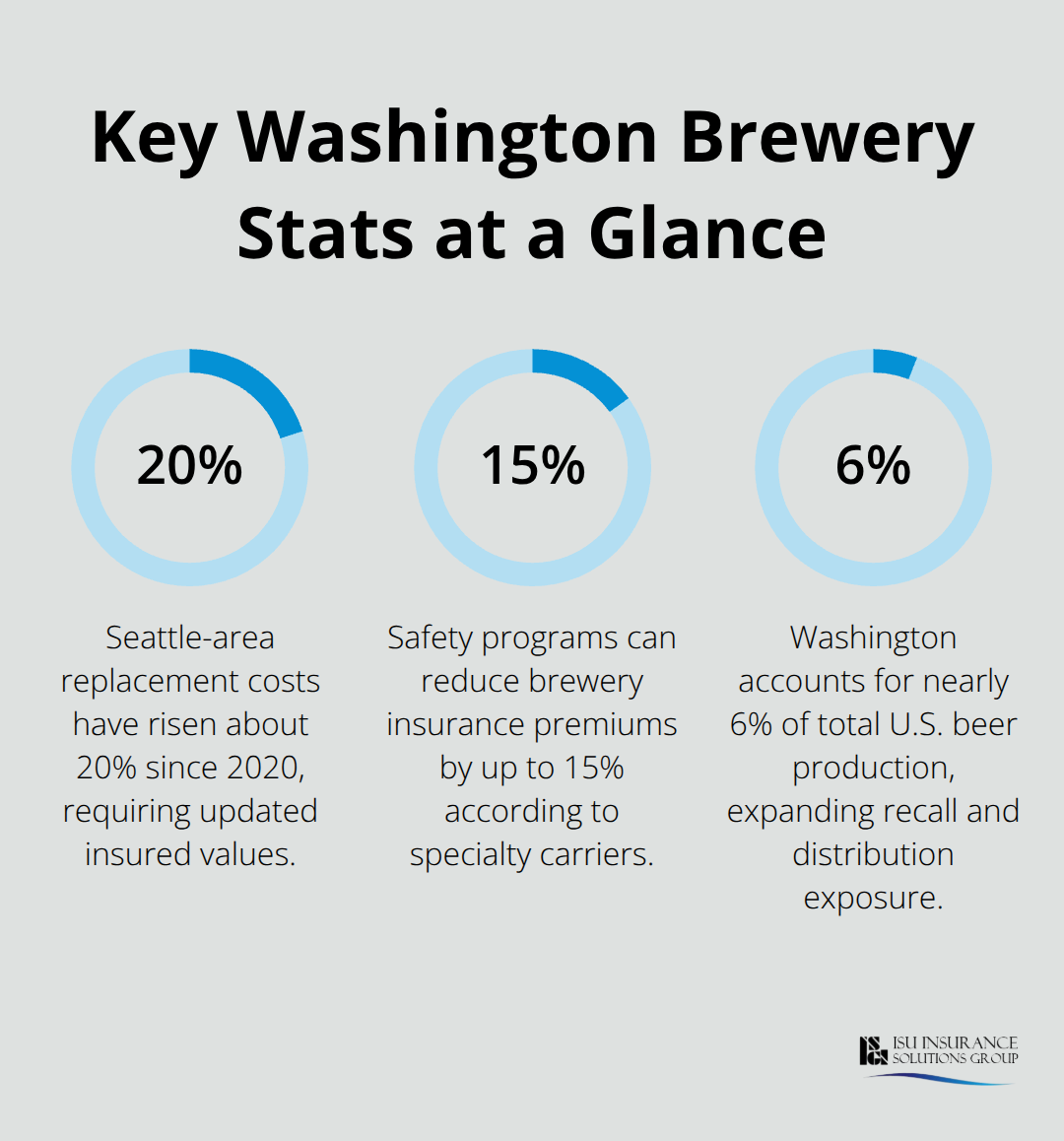

Your brewery’s physical assets demand coverage that goes far beyond standard commercial property policies. Building and structure protection forms the foundation, but it must account for replacement cost rather than depreciated book value. Seattle-area replacement costs have risen approximately 20% since 2020, which means your insured values need regular updates to reflect current construction expenses. A 15,000 square-foot brewery facility with concrete floors, specialized HVAC systems for temperature control, and reinforced structural supports for tank placement costs significantly more to rebuild than a generic commercial building. Fire marshals in Washington require documented proof of adequate property coverage for facilities exceeding 10,000 square feet, so your coverage limits directly determine licensing compliance.

Equipment Breakdown: Protecting Your Most Valuable Assets

Equipment breakdown coverage operates separately from standard property protection and covers the specific machinery that defines your operation. Boilers, pressure vessels, chillers, and canning lines represent the highest-value components in most breweries, and a single failure triggers six-figure repair costs plus weeks of production downtime. The Brewers Association data shows Washington ranks fourth nationally for licensed breweries, and that concentration of equipment-heavy operations means carriers understand the real costs of these failures. Spoilage protection extends coverage to inventory destroyed when temperature control systems fail, which is critical because fermentation tanks worth $50,000 can hold beer valued at $30,000 to $80,000 depending on batch size and production stage. Peak season endorsements automatically increase your equipment and inventory limits during high-production periods, preventing the common mistake of carrying insufficient coverage when you need it most.

Inventory Protection: Raw Materials and Finished Products

Inventory and product protection requires honest assessment of what you actually have stored at any given time. Raw materials including hops, malt, and yeast stored in climate-controlled areas need specific coverage because standard property policies often exclude spoilage unless you add explicit protection. Finished inventory in kegs, cans, and bottles represents liquid assets that require scheduled coverage detailing quantities and locations, especially if you distribute across multiple warehouses or retail partners. Product liability and recall coverage protects against contamination claims and covers government-mandated recall costs, which matters when you distribute across state lines. Washington accounts for nearly 6% of national beer production, and that multi-state distribution exposure means contamination in one batch could trigger recalls affecting retailers across five or more states.

Business Interruption: Protecting Revenue During Downtime

Business interruption coverage reimburses lost profits when covered perils halt production, which is essential during equipment repairs or facility damage when lead times for replacement tanks exceed 26 weeks. Many breweries underestimate how much revenue they lose during downtime, particularly when they supply restaurants and retail accounts on regular schedules that cannot be disrupted without damaging customer relationships. Production stoppages cost far more than just repair bills-they cost customer relationships and market share that take months to rebuild. Your coverage should reflect actual monthly revenue so that interruption payments cover both fixed expenses and lost profit margins during extended downtime.

The specific coverage types you select determine whether your brewery survives a major loss or faces financial devastation. Brewery insurance in Washington requires careful assessment of your unique operational risks, and working with carriers experienced in craft production ensures you capture exposures that generic policies miss. Beyond these core protections, additional exposures emerge when you operate a taproom, host events, or expand distribution-each creating liability risks that demand their own specialized coverage solutions.

Common Claims and How to Prevent Them

Fire and Explosion Risks in Brewing Facilities

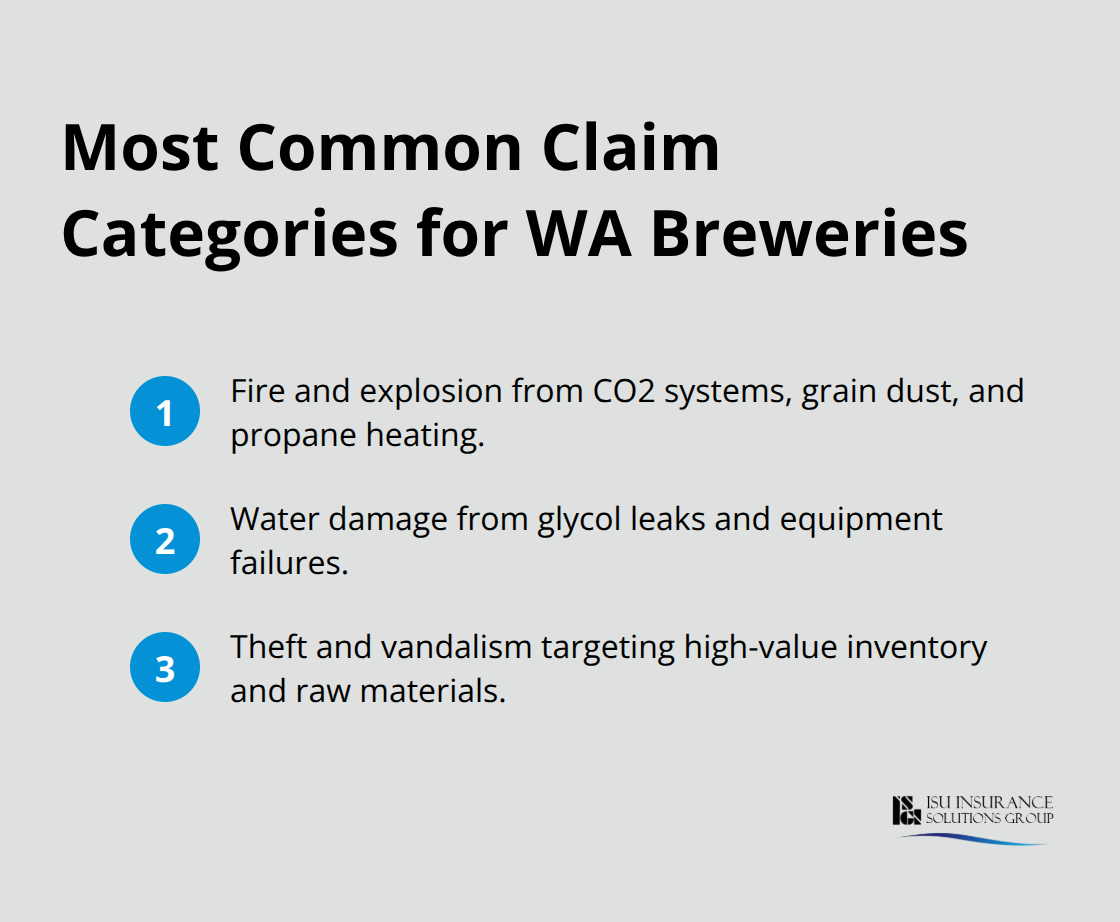

Fire and explosion risks in Washington breweries stem from specific operational hazards that most facility managers underestimate. CO2 systems pressurized to dangerous levels, grain dust accumulation in milling areas, and propane heating systems create genuine fire and explosion exposure that standard commercial policies treat as generic industrial risk. The Brewers Association reports Washington has over 475 craft breweries, and fire incidents at even one facility per year across the state demonstrate this is not theoretical concern.

A single propane system malfunction or electrical fault in fermentation areas can trigger catastrophic losses exceeding $500,000 when you account for building damage, equipment destruction, and inventory loss. Daily CO2 monitoring, regular boiler inspections documented in writing, and OSHA-style safety training reduce your premium costs by up to 15 percent according to carriers who specialize in brewery coverage. Fire marshals require proof of adequate property coverage for facilities exceeding 10,000 square feet, so your insurance limits directly determine whether your facility passes inspection and maintains operational licensing.

Water Damage from Equipment Failure

Water damage from equipment failure represents the second-largest claim category in Washington breweries, particularly from glycol system leaks that spread across production floors and destroy electrical systems, HVAC equipment, and inventory simultaneously. A mid-size facility experienced a glycol leak that triggered equipment breakdown, spoilage, and business interruption payments totaling over $150,000 because comprehensive coverage captured all three exposures.

Replacement lead times for specialized fermentation tanks exceed 26 weeks, which means business interruption coverage that extends through extended repair periods protects your revenue during months when you cannot produce. Temperature control failures demand immediate attention because even brief system malfunctions destroy fermentation cycles worth tens of thousands of dollars in raw materials and labor. Consider replacing aging water supply hoses with braided stainless steel alternatives, which have a longer lifespan and can help prevent costly water damage claims.

Theft and Vandalism Prevention Strategies

Theft and vandalism at brewery locations increased significantly post-2020, with break-ins targeting finished inventory in taproom storage areas and raw materials stored in accessible warehouse sections. Crime coverage addressing employee dishonesty and theft is often limited under standard property policies, which means standalone crime policies provide stronger protection for high-value inventory.

Implement daily inventory checks, secure raw material storage with keycard access, and install security cameras in high-value areas to reduce both loss frequency and insurance premiums. These controls demonstrate to carriers that you take asset protection seriously, which translates directly into lower renewal costs and faster claims resolution when incidents occur.

Final Thoughts

Protecting your Washington brewery requires specialized brewery property coverage that addresses temperature control failures, spoilage risks, equipment breakdown, and regulatory compliance simultaneously. The claims discussed throughout this guide reflect real losses that breweries face every year-fire and explosion risks from CO2 systems, water damage from glycol leaks, and theft of high-value inventory happen regularly across Washington’s 475+ craft breweries. The difference between financial recovery and operational collapse comes down to whether you carried the right coverage before the loss occurred.

Building comprehensive protection means starting with building and structure coverage based on replacement cost rather than depreciated value, adding equipment breakdown protection for your most critical machinery, and including inventory coverage that reflects both raw materials and finished products. Business interruption coverage protects your revenue during extended downtime when replacement lead times exceed 26 weeks, and peak season endorsements ensure you maintain adequate limits during high-production periods when your asset concentration peaks. Finding the right coverage requires working with carriers and agents who understand brewing operations specifically, since generic commercial insurance brokers lack the expertise to identify exposures unique to fermentation and temperature control.

We at ISU Insurance Solutions Group specialize in brewery and winery coverage through partnerships with multiple carriers and understand Pacific Northwest brewing operations thoroughly. Contact us for a brewery insurance quote that compares coverage options and competitive rates from carriers who actually understand your risks.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.