Professional Liability for Lawyers: Safeguarding Legal Practice

One missed deadline. One overlooked clause. One client dispute-and your law firm faces a claim that could cost thousands in legal fees and damage your reputation.

Professional liability for lawyers isn’t just a safety net. It’s a business necessity. At ISU Insurance Solutions Group, we’ve seen firsthand how quickly a single error can spiral into a costly lawsuit that threatens your practice.

This guide walks you through what coverage protects you, which claims hit law firms hardest, and how to build defenses that actually work.

What Professional Liability Insurance Covers for Lawyers

Professional liability insurance protects you from the financial devastation that follows when clients claim you’ve made costly errors. This isn’t about minor slip-ups-it’s about the real financial losses clients suffer when something goes wrong in your legal work. When a client loses money because you missed a statute of limitations, failed to file a document on time, or overlooked a critical clause, they sue. Your professional liability policy pays for your defense, settlements, and judgments. The policy covers defense costs separately from damages, which matters enormously-your legal fees can reach tens of thousands of dollars before a case even settles. If you face a lawsuit for negligence, errors in legal research, or breaching your duty to the client, the insurer funds your defense team and any resulting judgment or settlement up to your policy limits.

Errors and Omissions That Trigger Claims

Your professional liability policy covers the financial losses clients suffer from your professional mistakes. A missed deadline on a settlement, a misjudged statute of limitations, or an error in a trademark filing-each one can trigger a malpractice claim. The policy applies whether you made the error yourself or an employee under your supervision made it. This distinction matters when you evaluate whether your current coverage extends to all attorneys and staff in your firm, including part-time or contract lawyers who handle client matters. Defense costs alone in these cases often exceed $50,000 because disputes require extensive document review and expert testimony.

Breach of Fiduciary Duty and Conflicts of Interest

Breach of fiduciary duty claims hit harder than most lawyers expect because they involve more than just professional mistakes. When you fail to disclose a conflict of interest, mishandle client funds, or act without proper client authorization, you’ve crossed into territory where clients demand significant compensation. These claims often involve allegations that you put your interests ahead of the client’s, and courts take that seriously. Your professional liability policy covers the financial losses the client suffered as a result-not the reputational damage, but the actual money they lost.

Defense Costs and Coverage Limits

Your insurer funds your defense team and any resulting judgment or settlement up to your policy limits. Defense costs apply separately from damages, which means your legal fees don’t reduce the amount available for settlements or judgments. This separation proves critical when you face complex litigation that demands expert witnesses and extensive discovery. Most professional liability policies are claims-made, meaning coverage applies to claims filed during the policy period, not when the error occurred. Understanding your retroactive date and policy limits helps you assess whether your current coverage matches your practice’s actual exposure. The next section examines which claims hit law firms hardest and why certain practice areas face elevated risk.

What Actually Triggers Malpractice Claims Against Lawyers

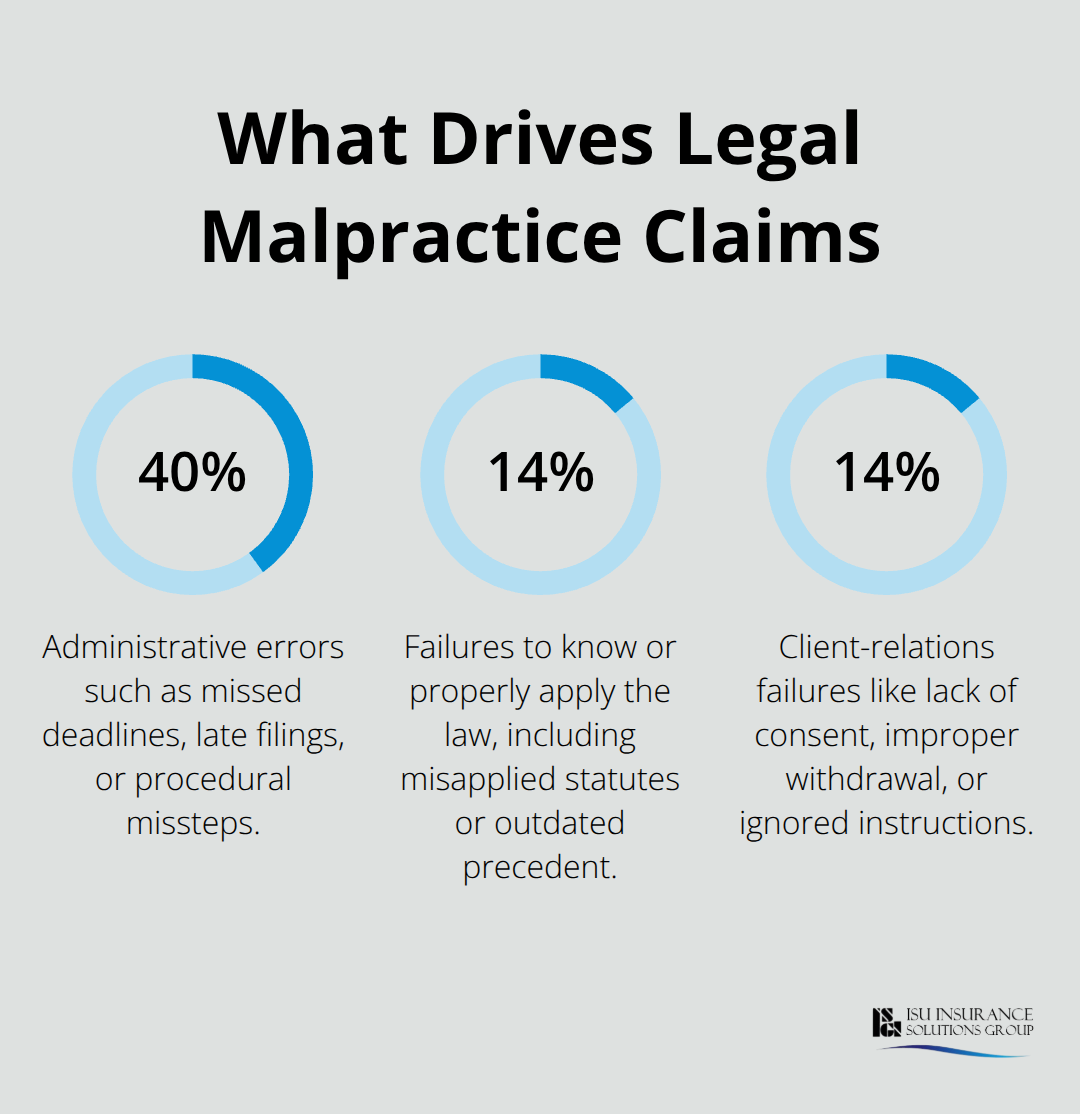

Administrative Errors Lead the Pack

Administrative errors dominate the malpractice landscape far more than most lawyers realize. Nearly 40 percent of legal malpractice claims stem from administrative mistakes-missing filing deadlines, failing to file documents on time, or overlooking procedural requirements that courts demand. A missed statute of limitations deadline doesn’t just lose the case; it exposes you to a direct malpractice claim because the client’s remedy died with the deadline. Real estate attorneys discovered this hard truth after the 2008 recession when claim frequency spiked due to rushed transactions and document errors.

Personal injury attorneys face the highest litigation risk overall, making them statistically the most likely to face malpractice suits. These practice areas share a common thread: tight deadlines, high client expectations, and significant financial stakes that clients notice immediately when something goes wrong.

Gaps in Legal Knowledge and Application

The second major category involves failing to know or properly apply the law, accounting for roughly 14 percent of claims. This isn’t about complex legal strategy disagreements-it’s about fundamental errors in legal knowledge that any competent attorney should catch. A lawyer who misapplies a statute, misses a critical case precedent, or applies outdated law leaves a clear trail of negligence that clients and courts easily identify.

Communication Breakdowns and Conflicts

Client-relations failures-including failure to obtain proper consent, improper withdrawal, or ignoring client instructions-comprise about 14 percent of malpractice claims. Clients tolerate strategy disagreements far better than they tolerate silence. Extended periods without updates, missed calls, or vague explanations about case progress breed resentment and suspicion that their attorney has abandoned them.

Conflicts of interest and inadequate legal research each create substantial exposure because they involve breaches of trust that courts view as serious departures from standard practice. These failures (whether rooted in oversight or negligence) trigger claims that damage both your finances and your reputation.

Building Your Defense Strategy

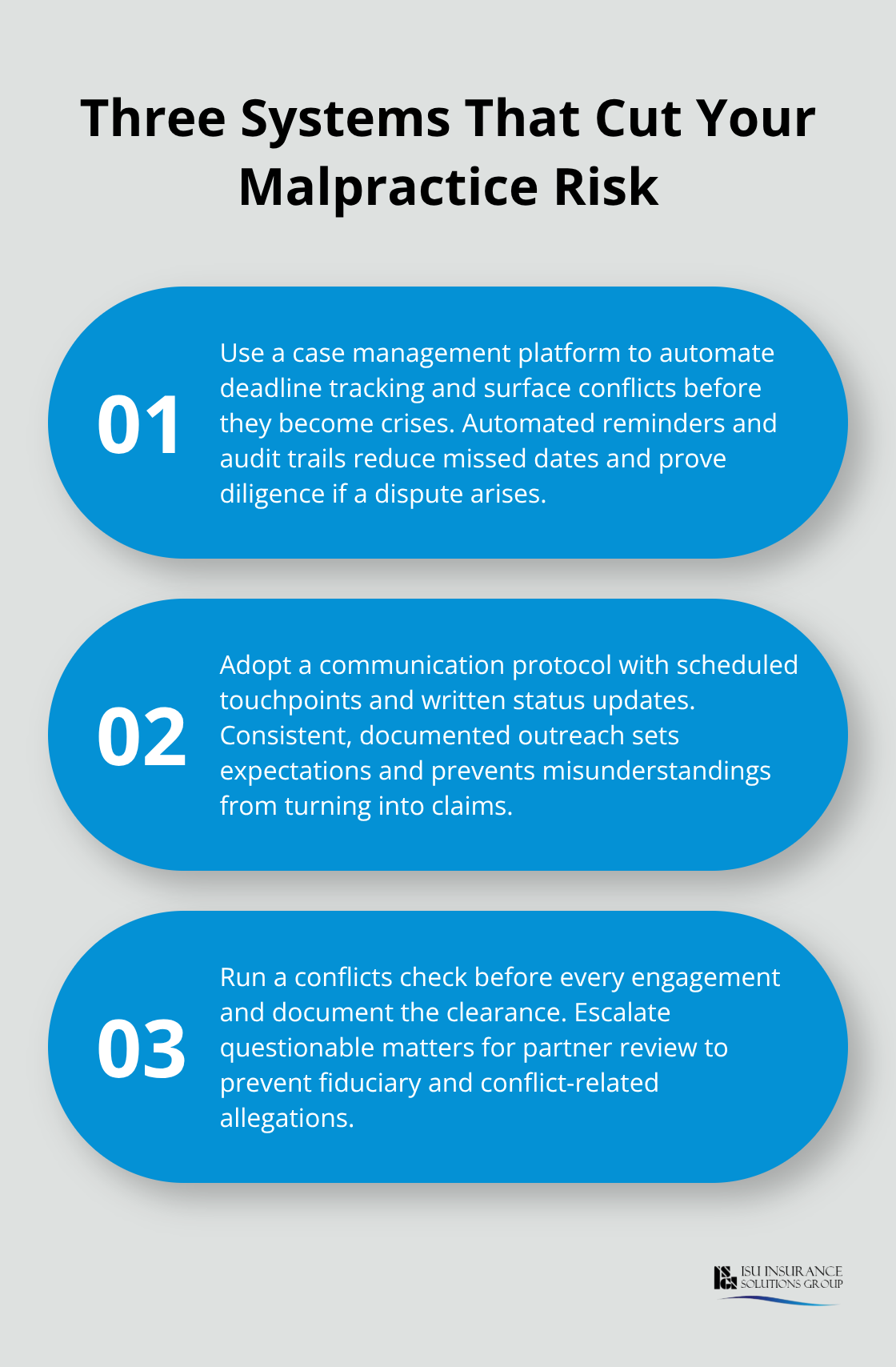

Three systems directly address the three biggest claim drivers in the legal profession. Implement a case management system that flags deadlines automatically, create a communication protocol that touches base with clients at scheduled intervals, and maintain a conflicts checking process that runs before you accept any engagement. These safeguards transform how your firm operates and significantly reduce exposure to the claims that hit hardest.

The next section examines how to reduce professional liability risks through stronger systems and proactive risk management.

Stop Relying on Memory: Build Systems That Catch Errors Before Claims Happen

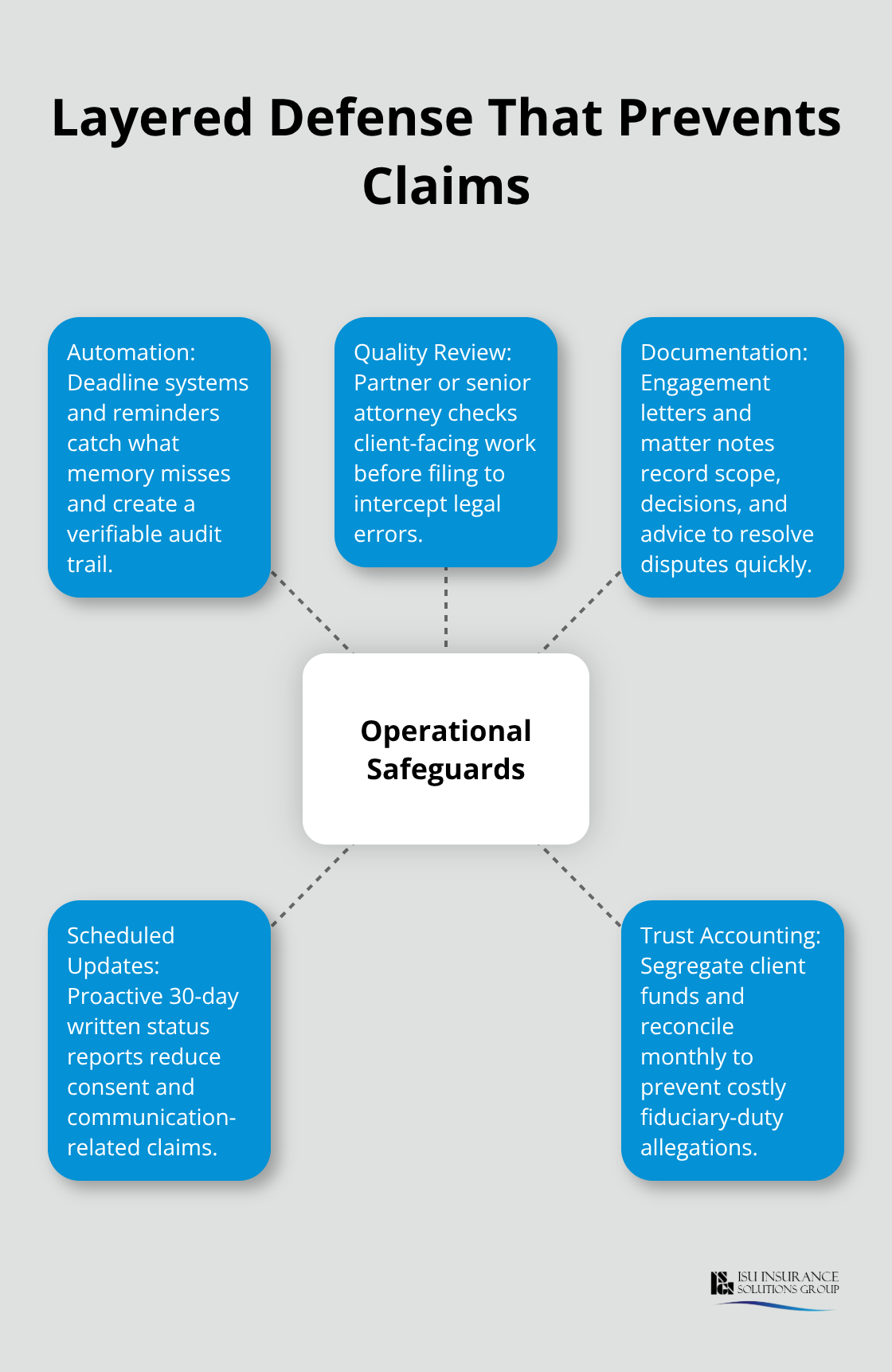

The firms that avoid malpractice claims don’t have smarter lawyers-they have better systems. Case management software that flags deadlines automatically prevents the administrative errors that trigger nearly 40 percent of malpractice claims. A firm using practice management tools like Clio, MyCase, or TimeSolv catches missed deadlines through automated alerts rather than relying on attorney memory or handwritten calendars. These systems integrate deadline tracking with client communication logs, creating an audit trail that demonstrates you acted with reasonable care if a dispute arises.

Automate Deadline Tracking to Eliminate Your Biggest Exposure

When you implement automated deadline reminders set 30 days, 14 days, and 3 days before critical dates, you eliminate the most expensive category of claims outright. Real estate and personal injury practices benefit most because these areas involve hard statutory deadlines that courts won’t extend. Your case management system becomes the backbone of your defense strategy-it catches what human memory misses and creates documentation that protects you if a claim surfaces later.

Review Work Product Before It Leaves Your Office

The second defense layer involves quality reviews built into your workflow-not annual audits, but real-time checks before documents go out. Assign a partner or senior attorney to review all client-facing work product before filing, and document that review. This catches the legal research errors and application mistakes that account for 14 percent of claims. When you establish this review requirement as a firm standard, you transform quality control from an afterthought into a systematic barrier against negligence.

Train Staff on Your Actual Procedures, Not Generic Topics

Staff training matters, but only if it targets the actual failure points in your firm. Generic ethics CLEs don’t prevent the specific errors your practice faces. Instead, train staff on the exact procedures your firm uses: how conflicts checking works, when to escalate client concerns, and what constitutes proper client authorization before settling a matter. Your insurer may offer ethics CLEs at 5 hours per attorney as part of your professional liability coverage-check whether your policy includes this benefit.

Document Everything and Communicate in Writing

Clear client communication and detailed documentation form the third pillar of your defense strategy. Establish a written engagement letter that specifies scope, fees, timeline, and what you will and won’t do for the client. When clients have written expectations, disputes over strategy don’t transform into malpractice claims. Document every significant conversation, court appearance, and case development in your matter file with dates and summaries. If a client later claims you never told them about a deadline or settlement offer, your file proves otherwise.

Communication breakdowns and failure to obtain proper consent comprise 14 percent of malpractice claims-problems that disappear when you send written status updates every 30 days without waiting for clients to ask. Schedule these updates automatically through your case management system so they go out regardless of case activity. Mishandling client funds or retainers creates fiduciary duty claims that rank among the most costly, so implement a trust accounting procedure that separates client funds from operating accounts and reconciles monthly.

Combine Systems to Address Your Highest-Risk Exposures

When you combine automated deadline systems, documented quality reviews, systematic client communication, and proper trust accounting, you address the specific triggers that hit law firms hardest and create evidence of reasonable care that protects you even if a claim arises. These three layers-automation, review, and documentation-work together to eliminate the administrative errors, legal research failures, and communication gaps that dominate malpractice litigation.

Final Thoughts

Professional liability for lawyers protects your practice when claims arrive, but only if your coverage matches your actual exposure. Evaluate your current limits against the size and complexity of matters you handle, confirm that your policy extends to all attorneys and staff (including part-time or contract lawyers), and verify your retroactive date so you understand what incidents your policy covers. If you handle personal injury or real estate work, your risk profile demands higher limits because these practice areas face the litigation frequency that transforms single errors into costly lawsuits.

The systems you’ve built-automated deadline tracking, documented quality reviews, and scheduled client communication-work alongside your professional liability policy to create a complete defense strategy. Defense costs alone exceed $50,000 before any settlement payment, which is why the combination of strong operational safeguards and adequate insurance coverage protects both your finances and your reputation. Start today by reviewing whether your current coverage aligns with your practice’s actual risks.

We at ISU Insurance Solutions Group work with law firms throughout Washington and Oregon to secure professional liability coverage that matches their specific practice exposures. Our agents understand the vulnerabilities that different practice areas face and help you determine appropriate limits and policy terms. Contact us for a quote and let’s build coverage that protects what you’ve built.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.