Security Guard Coverage Options: Tailored Plans for Your Security Team

Security guard coverage options aren’t one-size-fits-all. Your team faces unique risks that standard business insurance simply doesn’t address.

At ISU Insurance Solutions Group, we’ve helped hundreds of security firms find the right protection. This guide breaks down the coverage types that actually matter for your operation.

What Coverage Types Actually Protect Your Security Operation

General Liability: The Foundation That Isn’t Enough

General liability coverage forms the foundation of any security firm’s insurance strategy, but it’s not enough on its own. This coverage protects your company when a guard faces accusations of excessive force, false arrest, or property damage during operations. Assault and battery lawsuits represent the most common liability claim against security personnel. A guard restrains a disruptive client appropriately, yet the client files a lawsuit claiming excessive force. General liability typically covers legal defense costs and settlements up to your policy limits, which range from $1 million to $2 million for most security operations. Standard business policies exclude security-specific risks, making a specialized program essential. Start with at least $1 million in general liability limits for firms with fewer than 20 employees, then scale upward as your headcount and contract values increase.

Workers Compensation: A Legal Requirement With Real Costs

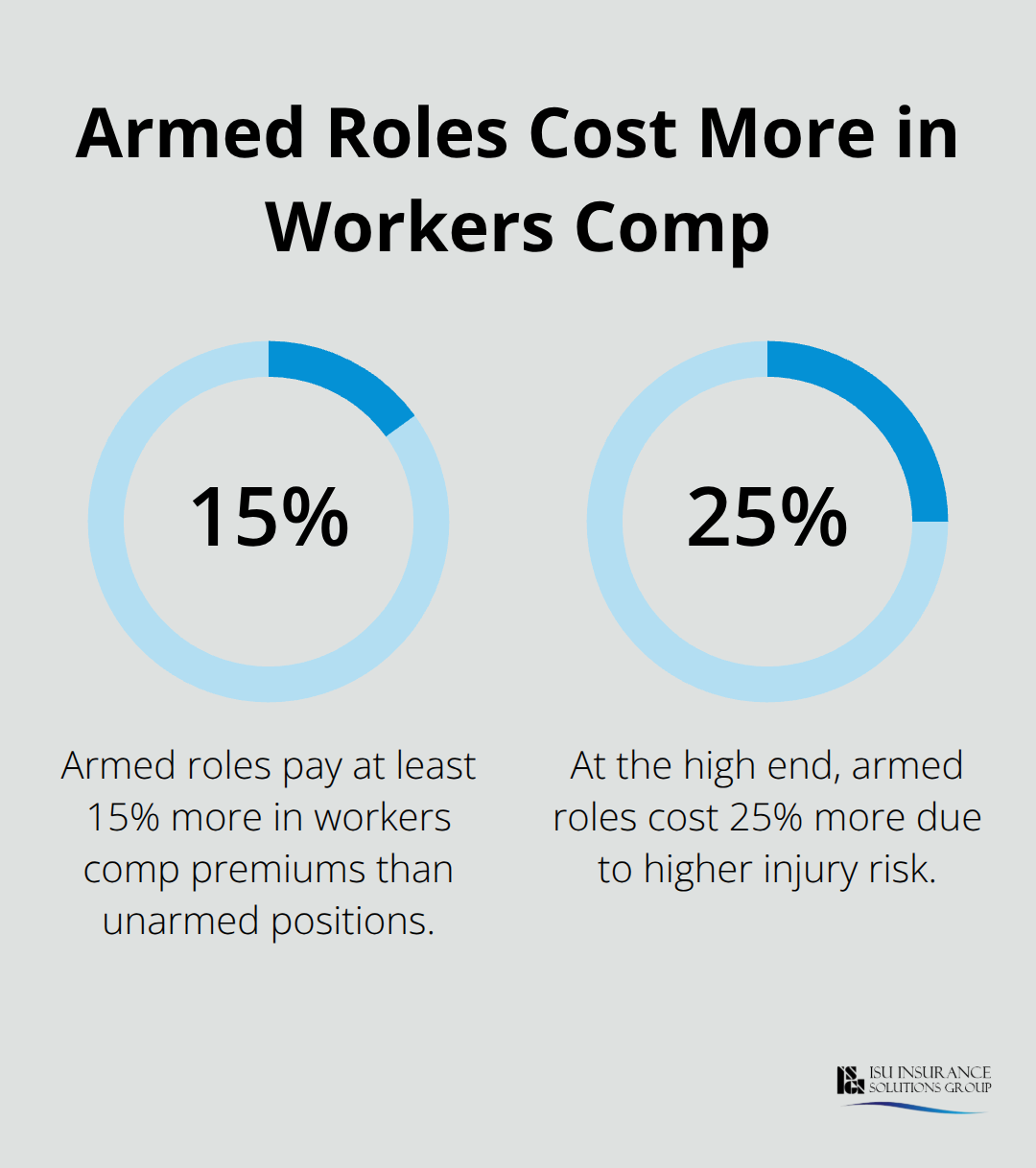

Workers compensation covers medical expenses and lost wages when guards sustain injuries on the job. Security work carries genuine physical hazards-guards suffer sprains, fractures, and lacerations during confrontations or while patrolling properties with uneven terrain. State law mandates workers compensation in all 50 states for businesses with employees, and violations result in substantial fines and potential criminal liability for owners. Your premium depends on payroll, job classification, and claims history. Armed security roles typically cost 15 to 25 percent more in workers comp premiums than unarmed positions because the injury risk profile differs significantly.

Professional Liability: Protecting Against Failed Duties

Professional liability covers legal costs when a security guard is sued for a mistake or oversight that causes financial harm. A guard fails to secure a perimeter and theft occurs, or a guard misses a threat that results in client injury-professional liability covers the resulting claim. This coverage matters for contract security firms because clients increasingly demand it as a contractual requirement. Most security contracts now include language requiring minimum coverage of $500,000 to $1 million in professional liability. Claims under this coverage include failure to perform duties, reporting inaccuracies, and breach of client confidentiality. A single incident can bankrupt a small security operation without this protection in place.

Scaling Coverage to Match Your Operation

The coverage limits you select should reflect your operation’s size, the number of guards you employ, and the types of contracts you pursue. A firm with five unarmed guards patrolling office buildings faces different exposure than a firm with twenty armed personnel protecting high-value assets. Your professional liability limits should align with what clients contractually require and what your annual revenue can support. General liability limits should account for the maximum potential loss from a single incident-consider the worst-case scenario for your typical contract. Armed operations require higher limits across all categories because the injury and liability exposure increases substantially.

Your coverage structure directly influences which contracts you can bid on and which clients will hire you. Clients in regulated industries (healthcare, finance, government) often mandate specific minimum limits before they’ll sign an agreement. The right coverage combination removes barriers to winning larger contracts and protects your firm from the financial devastation that follows a major claim.

What Coverage Limits Actually Work for Your Security Operation

Understanding Your Real Coverage Needs

The coverage limits you select determine which contracts you can pursue and how much financial protection your firm actually has when a claim arrives. Most security firms operate with insufficient limits because they don’t understand how claims develop in their specific market. A $1 million general liability limit sounds substantial until you face a lawsuit where a guard’s actions result in a permanent injury claim worth $2.5 million-your firm then covers the gap personally. The right approach starts with understanding what your actual clients demand, not what insurance brokers suggest as standard. Contact your top five existing clients and review their insurance requirements in writing. Most will specify minimum limits of $1 million to $2 million in general liability and $500,000 to $1 million in professional liability.

Setting Limits for Armed Operations

Armed security operations should carry $2 million in general liability and $1 million in professional liability as a baseline because the injury exposure increases substantially when guards carry weapons. Third-party bodily injury claims represent your highest exposure category-a guard’s actions injure a bystander, client employee, or the person being detained, and that person sues your company. These claims routinely exceed $500,000 in medical costs and lost wages alone, before accounting for pain and suffering or punitive damages. Your limits should reflect the worst realistic scenario in your market. A security firm protecting retail locations faces different exposure than one providing executive protection or armed asset protection services. Retail security typically involves lower-severity claims averaging $100,000 to $300,000, while executive protection claims can reach $5 million when serious injury occurs.

Analyzing Claims Data for Your Market

Review claims data from your state’s workers compensation board to understand what injuries actually happen in security work. Armed security personnel sustain higher injury rates than unarmed guards-data shows armed guards experience injury claims 20 to 35 percent more frequently, which directly impacts both your workers compensation costs and your professional liability exposure. This information shapes the coverage limits that actually protect your operation rather than leaving you exposed to catastrophic loss.

Specialized Coverage Requirements for Armed Guards

Specialized coverage for armed operations requires separate attention because standard policies often exclude or severely limit coverage for armed guard activities. Your policy must explicitly cover armed personnel, including the use of force decisions and weapons-related incidents. Many carriers impose higher deductibles and require additional training documentation before covering armed operations. Assault and battery coverage becomes critical for armed guards because the injury exposure increases dramatically. A guard makes a lawful arrest but uses more force than necessary, and the detainee sues claiming excessive force-this claim falls outside standard general liability unless your policy includes assault and battery endorsement. Professional liability for armed operations should address both the decision to use force and the consequences when force decisions result in client harm or property damage. Your policy should cover legal defense costs even if the claim is ultimately dismissed, because defending against an excessive force allegation costs $50,000 to $150,000 in attorney fees alone.

Evaluating Armed Coverage Costs and Protection

Coverage limits for armed operations typically run 25 to 40 percent higher in annual premium than comparable unarmed operations, but this cost reflects the genuine increase in liability exposure. Request quotes that specifically itemize armed versus unarmed coverage costs so you understand exactly what the additional risk premium represents. When evaluating coverage options, ask carriers whether they cover both the guard and your company in an assault and battery claim, because some policies protect only the company while leaving individual guards exposed. This matters because guards increasingly face personal lawsuits, and your firm’s reputation suffers if guards lack individual coverage. Working with a broker who specializes in security operations and can access multiple carriers (rather than accepting a single insurer’s standard program) positions your firm to identify the coverage structure that actually matches your operation’s risk profile and contract requirements.

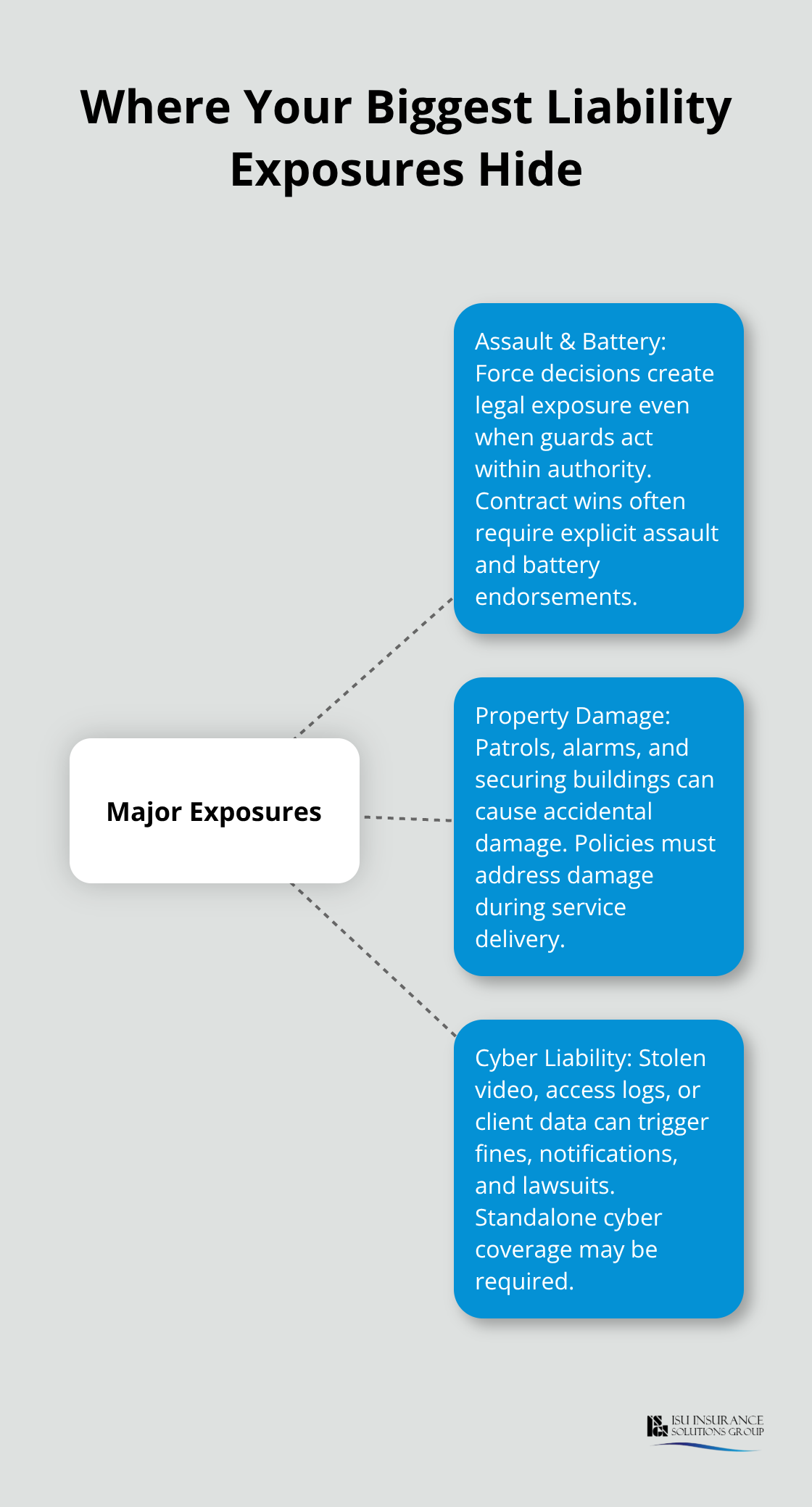

Where Your Biggest Liability Exposures Actually Hide

Assault and Battery Claims: The Armed Guard Reality

Assault and battery claims dominate security industry litigation, but they represent only part of your exposure picture. Armed guards face the highest risk-data shows assault and battery lawsuits against armed security personnel occur at higher rates than against unarmed guards, primarily because force decisions create legal vulnerability even when guards act within their authority. A guard lawfully detains someone for trespassing but applies pressure that causes injury, and the detainee files suit claiming excessive force. Your general liability policy must explicitly cover assault and battery through endorsement, because standard policies frequently exclude or limit coverage for these claims. Many carriers require documented training in de-escalation and force limitations before covering armed operations at all. Armed security contracts now routinely demand proof of assault and battery coverage before signing, making this endorsement non-negotiable if you want to win those contracts.

Property Damage During Security Operations

Property damage during security operations represents your second-largest exposure category. A guard’s vehicle damages client property during patrol, or a guard accidentally triggers an alarm system while securing a building, or guards move equipment and cause structural damage. These incidents happen frequently enough that clients specifically ask about property damage liability limits during contract negotiations. Your general liability should cover both accidental property damage caused by your guards and damage to client property while under your care. The coverage gap most security firms miss: property damage caused during the act of securing a location. A guard installs temporary barriers and damages flooring, or uses force to secure a door and damages the frame-these claims fall outside coverage unless your policy explicitly addresses property damage during security service delivery. Request quotes that itemize property damage coverage separately so you understand exactly what’s protected and what’s excluded.

Cyber Liability for Surveillance and Client Data

Cyber liability for digital surveillance systems ranks third in importance but gets overlooked by most security firms. Security companies now store client video footage, access logs, visitor records, and sometimes financial data-all attractive targets for ransomware attacks and data breaches. A breach exposes client confidential information, and your firm faces regulatory fines, notification costs, forensic investigation expenses, and client lawsuits claiming negligence in data protection. Cyber liability insurance covers breach response costs, regulatory fines, business interruption losses, and legal defense against claims that you failed to protect client data adequately. The exposure increases dramatically if you operate cloud-based surveillance systems or store data on networked servers rather than isolated systems. Your professional liability policy may not cover cyber incidents because they’re increasingly excluded from standard coverage-you need a standalone cyber liability endorsement or separate cyber policy. Most security firms carrying fewer than 50 employees face annual cyber premiums ranging from $1,500 to $3,500, depending on the volume of client data stored and your security infrastructure.

Calculating Your Cyber Coverage Needs

Start by inventorying exactly what client data your firm stores, where it’s stored, and what security controls protect it. This inventory directly determines your cyber liability premium and tells you which coverage limits actually matter for your operation. Armed security firms handling client financial information or storing surveillance footage for regulated clients in healthcare or finance should carry minimum cyber liability coverage of $250,000 to $500,000 because regulatory fines in those industries can reach $100,000 or more per breach.

Final Thoughts

Security guard coverage options require a strategic approach that matches your firm’s actual risk profile, not industry defaults. General liability, workers compensation, and professional liability form your essential foundation, but the specific limits and endorsements you select determine whether your firm survives a major claim or faces financial devastation. Armed operations demand higher limits across all categories because the injury and liability exposure increases substantially, while cyber liability protection has shifted from optional to necessary as security firms store more client data and operate cloud-based surveillance systems.

The coverage limits that work for a five-person unarmed patrol firm won’t protect a twenty-person armed operation protecting high-value assets. Your clients’ contractual requirements, your state’s regulatory environment, and your specific service delivery model all shape which security guard coverage options actually matter for your operation. A broker who understands security industry risks and can access multiple carriers positions your firm to identify coverage structures that remove barriers to winning larger contracts while protecting against catastrophic loss.

We at ISU Insurance Solutions Group have worked with security firms across Washington and Oregon since 1983 to build coverage that adapts as your operation grows. Contact us to review your current coverage gaps and identify which endorsements and limits your firm genuinely needs to operate with confidence.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.