Professional Liability for Consultants: Reducing Risk in Consulting

Consultants face a growing number of liability claims each year, from missed deadlines to data breaches. Professional liability for consultants isn’t optional-it’s a business necessity that protects your reputation and finances.

At ISU Insurance Solutions Group, we’ve seen firsthand how the right coverage and risk management practices separate thriving consulting firms from those struggling with claims. This guide walks you through the risks you face and how to address them.

What Professional Liability Actually Covers

Professional liability insurance covers claims arising from errors, mistakes, or negligence in the delivery of professional services. It covers legal defense costs, settlements, and judgments when a client alleges you failed to deliver promised services, gave negligent advice, or made errors in your work. This isn’t about property damage or bodily injury-those fall under general liability. Professional liability specifically addresses claims that your professional work caused the client financial loss. The coverage applies to errors and omissions you made during service delivery, breach of confidentiality if you accidentally disclosed client data, and negligence where your work fell below accepted industry standards. Most professional liability policies are claims-made, meaning they cover claims reported during the policy period, not when the work was performed. This distinction matters because if you switch insurers or retire, you’ll need tail coverage to protect against claims filed after your policy ends.

Why General Liability Leaves You Exposed

Your general liability policy won’t cover professional liability claims. General liability covers third-party bodily injury, property damage, and advertising injury-someone slips in your office, you damage a client’s equipment during a meeting, or you make a false advertising claim. When a client sues because your advice cost them money or your deliverable was incomplete, general liability rejects the claim. Consultants often mistakenly believe their general liability covers professional work, then face significant legal bills out of pocket. The gap is real and expensive. E&O claims show that missed scope and ambiguous engagements remain top drivers of disputes, with clients claiming they didn’t receive what was promised. Without professional liability coverage, you’re personally liable for every dollar of defense costs and any settlement or judgment.

The Claims That Actually Happen

Consultants face concrete claim scenarios regularly. A management consultant provides strategic recommendations that a client follows, resulting in operational losses-the client sues for negligent advice. An IT consultant implements software that fails to meet performance specifications, delaying the client’s project launch and costing them revenue. A financial consultant makes calculation errors in a proposal, leading to incorrect pricing and client losses. A contractor hires a technical consultant who fails to flag a major implementation risk, and the project fails catastrophically. Fee disputes escalate into claims when clients claim they were misled about costs or deliverables. Data breaches happen when consultants store client information insecurely, triggering breach notification costs, forensic investigations, and regulatory fines. These aren’t hypothetical-they’re the claims that land on desks every day, and they cost tens of thousands in legal defense alone, before any settlement.

How Claims-Made Policies Affect Your Protection

Claims-made policies create a critical timing issue that many consultants overlook. The policy covers claims reported during the active policy period, not claims arising from work performed years earlier. If you complete a project in 2025 but the client doesn’t sue until 2027, your 2025 policy won’t cover that claim unless you’ve purchased tail coverage. Tail coverage (also called run-off coverage) extends your protection after you leave the business or switch insurers, typically covering claims filed within a set period after the policy ends. Without tail coverage, you face a dangerous gap where old claims arrive with no active policy to defend you. This makes continuity planning essential for any consultant who plans to retire or change insurance providers.

What You Need to Know Before the Next Step

Professional liability insurance addresses the financial and legal fallout from client disputes, but it works best alongside strong risk management practices. The right coverage protects your finances, but clear contracts, detailed documentation, and quality control processes prevent claims from happening in the first place. Understanding what professional liability covers-and what it doesn’t-helps you make informed decisions about the coverage limits and deductibles that fit your consulting practice. The next section walks you through the specific risks you should address before a claim arrives at your door.

Specific Risks That Drive Consultant Claims

Errors and Omissions Create the Biggest Exposure

Errors and omissions in client projects remain the leading source of professional liability claims, and they happen more often than most consultants expect. A missed deadline, incomplete deliverable, or incorrect calculation triggers a lawsuit even when you intended to do good work. Industry claims trends in 2025 show that missed scope and ambiguous engagements rank as top drivers of E&O claims. This means the problem isn’t always about your competence-it’s about mismatched expectations between you and your client.

When you tell a client you’ll deliver something by Friday but they understood you meant the following Friday, that gap becomes a claim. When you implement a software solution but the client expected it to solve a different problem, they sue. The solution isn’t to work harder; it’s to write everything down. Your contract or statement of work must detail every deliverable, timeline, and specification. If the scope changes mid-project, document it in writing and update your fee estimate. Issue a change order that both you and the client sign. This single practice eliminates most scope-related disputes because no ambiguity exists about what was promised.

Data Breaches and Confidentiality Violations

Breach of confidentiality and data protection create a different but equally serious exposure. Consultants routinely handle sensitive client information-financial records, proprietary strategies, employee data, customer lists. A data breach costs tens of thousands of dollars in forensic investigation, breach notification, legal fees, and regulatory fines, and that’s before any client lawsuit.

If you store client data, review your technology provider’s security protocols and the liability insurance they carry to protect your business from breaches cascading from third-party systems. Practical cyber hygiene includes installing antivirus software on all systems, applying security patches promptly, using complex passwords, educating staff about phishing, and routinely backing up files on a separate server. These steps reduce your exposure significantly and demonstrate due diligence if a breach occurs.

Fee Disputes Escalate Into Claims

Fee disputes escalate into E&O claims more often than consultants realize. When clients claim they were misled about costs or deliverables, they sue. Prevent this by specifying payment terms and due dates clearly in every contract, requiring partial upfront payments, and documenting the value you deliver. Even if you provide additional work outside the agreed scope, issue an invoice for it-even if the amount is zero-to create a paper trail that proves you recognized the extra work and its value. This documentation protects you when disputes arise and demonstrates transparency throughout the engagement.

Understanding these three risk categories-scope ambiguity, data protection, and fee disputes-positions you to implement the preventive controls that stop claims before they start. The next section shows you exactly how to build those controls into your consulting practice.

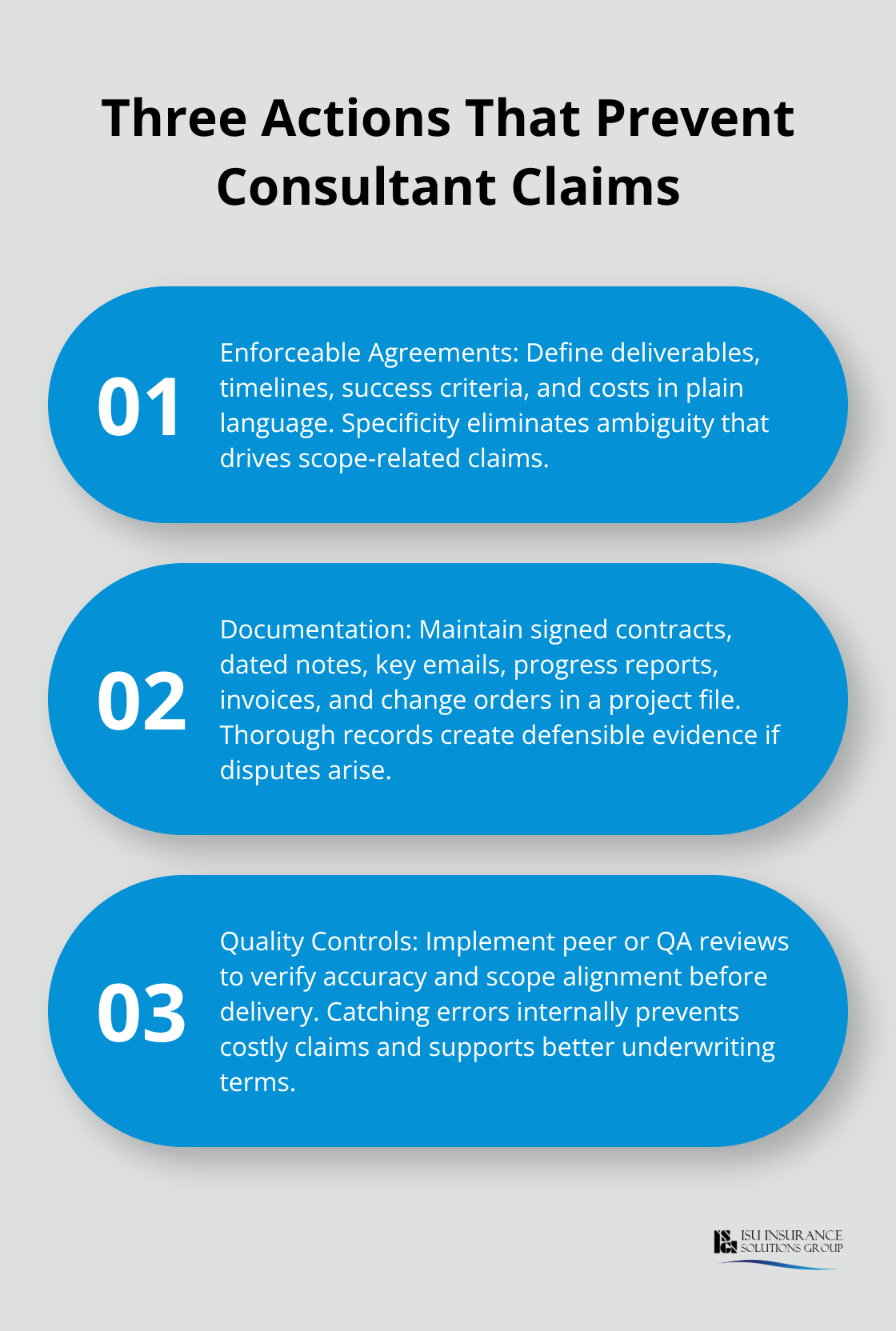

How to Stop Claims Before They Start

The gap between what you promise and what clients expect is where most liability claims originate. Closing that gap requires three concrete actions: write enforceable agreements that spell out exactly what you’ll deliver, maintain documentation that proves you delivered it, and implement quality checks that catch errors before clients see them. These practices work together to prevent claims from happening in the first place, and when disputes do arise, they give you a defensible record.

Contracts That Actually Prevent Disputes

Your engagement letter or statement of work is your most powerful liability tool. It must specify every deliverable, timeline, success criteria, and cost. Vague language like “we’ll improve your processes” or “we’ll provide strategic recommendations” guarantees future disputes. Instead, write “we will deliver a 50-page process improvement report by March 15th that includes current-state analysis, recommendations ranked by implementation cost, and a 12-month implementation roadmap.”

This specificity eliminates the ambiguity that triggers claims.

Include a section on scope changes that explicitly states any work outside the original agreement will be documented in a written change order and billed separately. This prevents scope creep, which is a major claim driver. Have an attorney draft your standard contract template covering service scope, deliverables, timelines, payment terms, limitation of liability, and indemnification clauses. This upfront investment pays dividends by protecting you across dozens of engagements. Require clients to sign the engagement letter before you start work, and keep a copy in your project file.

Documentation That Defends You

Project documentation transforms vague memories into concrete evidence. Create a project file for every engagement containing the signed engagement letter, all email correspondence with the client, meeting notes dated and summarized in writing, progress reports sent to the client, invoices showing work performed, and any change orders or scope amendments. If a dispute arises two years later, this file proves what you promised, what you delivered, and when you communicated issues to the client.

Progress reports sent monthly or at key milestones serve double duty: they keep clients informed and create a timestamped record of your work. Include in these reports what was completed, what’s pending, any obstacles encountered, and how you’re addressing them. When you flag risks or limitations in your recommendations, document that communication in writing. A consultant who warns a client that a recommendation carries implementation risk (and documents that warning) has strong protection against a failure-to-advise claim.

Quality Control Before the Client Sees It

Implement a review process where work is checked before delivery. For deliverables like reports, proposals, or implementation plans, assign a second person to review for accuracy, completeness, and alignment with the engagement scope. For technical work, have someone other than the primary consultant validate that the solution meets specifications. This catches errors before they become claims and demonstrates due diligence if a claim occurs.

Small firms can use peer review; larger firms might assign a quality assurance role. The investment in review time is minimal compared to the cost of defending a claim. When errors are caught internally and corrected before client delivery, no claim ever materializes. Industry claims trends show that consultants with documented quality controls and governance processes experience better underwriting terms and lower claim frequency than those without these safeguards.

Final Thoughts

Professional liability for consultants protects your business when disputes happen despite your best efforts, absorbing legal defense costs, settlements, and judgments that would otherwise drain your reserves. The risks are real-scope ambiguity, data breaches, fee disputes, and missed deadlines create claims that cost tens of thousands in legal defense alone. But these risks become manageable when you combine clear contracts that specify exactly what you’ll deliver, documentation that proves you delivered it, and quality controls that catch errors before clients see them.

Clients increasingly require professional liability insurance as a contractual condition before engagement, and underwriters now favor consulting firms with documented risk controls and governance processes. Start by reviewing your current policy to confirm it matches your services and client requirements, then strengthen your risk controls through written engagement letters, detailed project files, and a review process for deliverables. Claims trends show that consultants with strong documentation practices experience better coverage terms and lower claim frequency than those without these safeguards.

ISU Insurance Solutions Group has served Washington and Oregon businesses since 1983, helping consultants assess their specific risks and secure appropriate coverage tailored to their practice. Our agents work with multiple carriers to find competitive rates and comprehensive protection for your consulting business. Contact us today to review your coverage and ensure your business is protected.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.