Small Business Professional Liability: What It Covers for Startups

One mistake in your service delivery can cost your startup thousands in legal fees and settlements. Small business professional liability insurance protects you from these financial disasters.

At ISU Insurance Solutions Group, we’ve seen startups lose clients and credibility after a single claim. The right coverage gives you peace of mind and shows your clients you take responsibility seriously.

What Professional Liability Actually Covers

How Professional Liability Protects Your Startup

Professional liability insurance protects your startup when clients claim your work caused them financial harm. This coverage pays for legal defense costs from the moment a claim arrives, regardless of whether you’re ultimately found at fault. According to The Hartford, E&O specifically covers mistakes in the products or services you deliver-think a bookkeeping error that costs a client thousands, web development work that tanks their sales, or incorrect tax filings that trigger an audit. The policy typically covers lawyer fees, court costs, expert witness testimony, settlements, and judgments. Many policies include a right-and-duty-to-defend provision, meaning your insurer takes over the legal defense rather than leaving you to manage it alone.

Why Legal Defense Costs Matter

Even winning a lawsuit can drain significant legal fees before any judgment is reached. For IT consultants, software developers, management consultants, accountants, and designers-professions The Hartford identifies as most needing this coverage-a single mistake can trigger client litigation that would otherwise force you to pay out of pocket. This financial exposure makes professional liability coverage essential for service-based startups.

Understanding Claims-Made Policies and Tail Coverage

Most professional liability policies operate on a claims-made basis, which means coverage applies only if the policy is active when the claim is filed, not when the work was performed. This distinction is critical: if you cancel coverage and a client sues six months later over work you did last year, you have no protection unless you purchased tail coverage beforehand. Your coverage limits matter too-standard policies offer $1 million per occurrence and $2 million aggregate, though you can purchase higher limits if larger clients demand it.

Cost and Coverage Variations by Industry

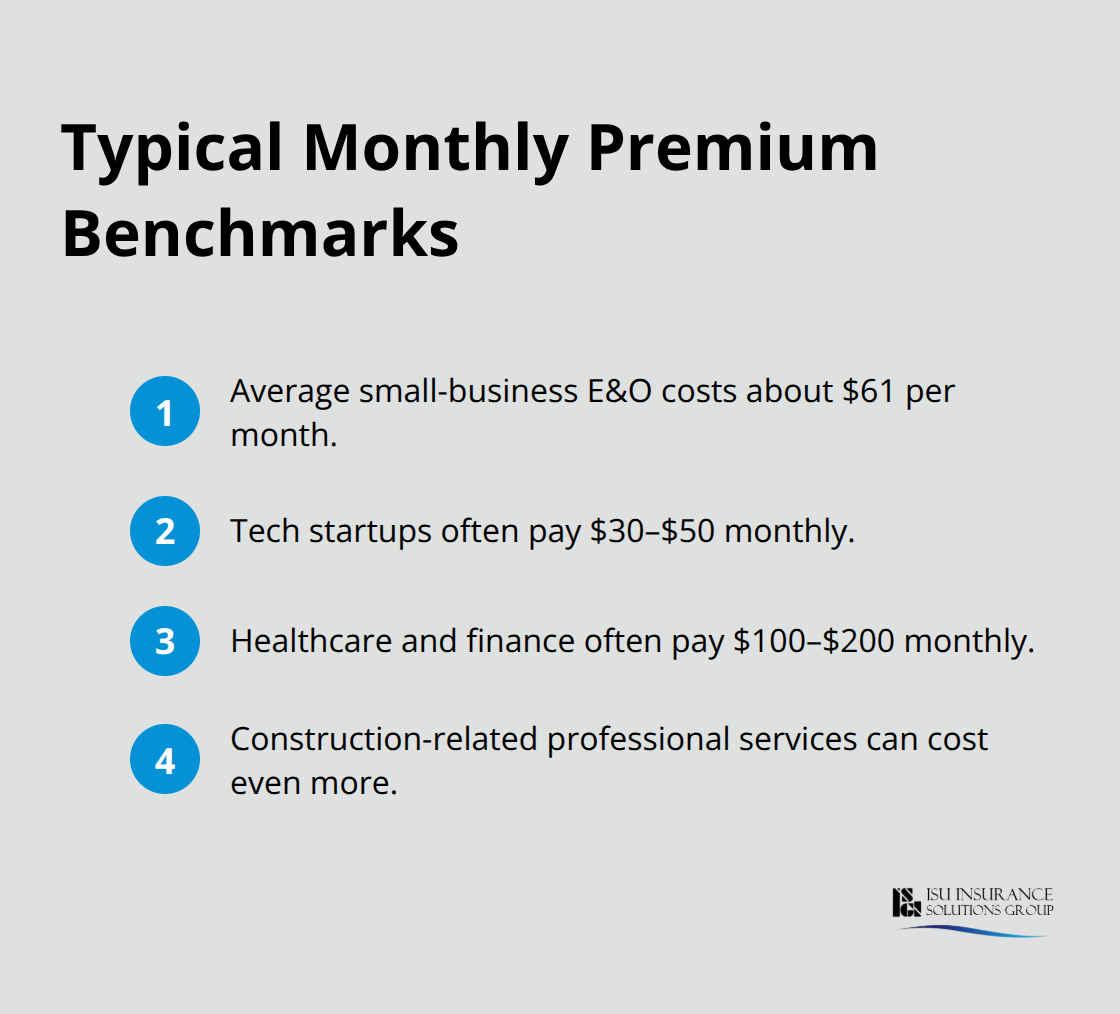

Professional liability insurance costs vary significantly by industry and risk profile. According to Insureon data, professional liability insurance averages around $61 per month. A tech startup might pay $30 to $50 monthly, while a healthcare or finance startup could face $100 to $200 monthly due to higher regulatory risk. The policy excludes illegal acts and intentional wrongdoing, so it won’t cover fraud or deliberate misconduct.

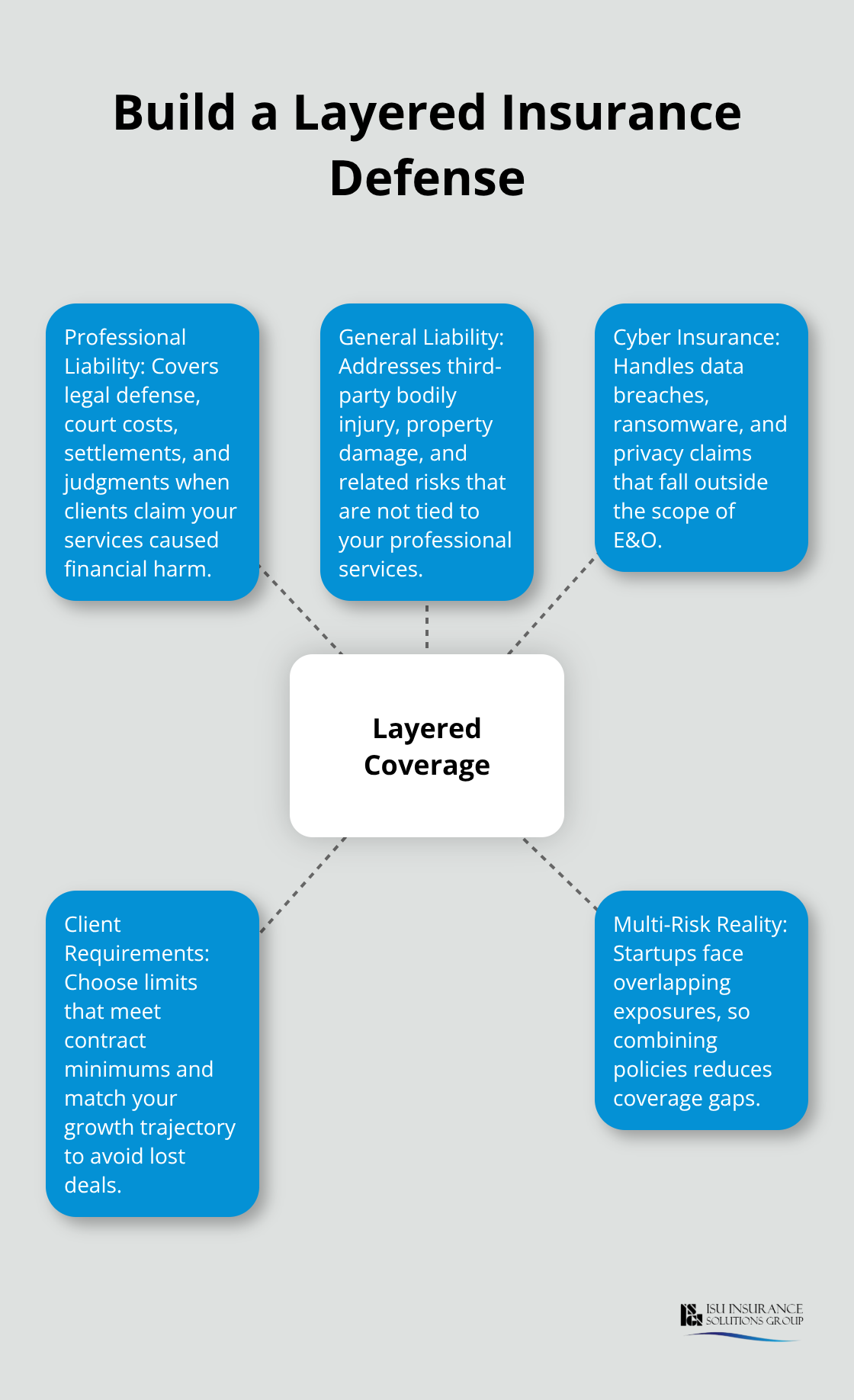

Layering Professional Liability with Other Coverages

Professional liability works best alongside other coverages like general liability and cyber insurance, creating a layered defense against different types of claims. This combination addresses the reality that startups face multiple risk exposures simultaneously. As you assess your specific industry risks and determine what coverage limits your clients will require, the next step involves selecting a policy that aligns with your business model and growth trajectory.

Why Your Startup Needs Professional Liability Coverage

Larger Clients Won’t Work Without It

Mid-market and enterprise clients demand professional liability coverage before they sign contracts with you. They’ll request a certificate of insurance showing your coverage limits, and this requirement isn’t negotiable. Many clients require minimum coverage of $1 million per occurrence, while others demand $2 million. Without proof of coverage, you lose deals before your first pitch. Professional liability insurance is now standard for consultants, accountants, IT professionals, designers, and software developers. Your competitors already carry it, so clients expect you to have it too. If you operate without coverage and a client demands it mid-negotiation, you either walk away from revenue or scramble to purchase a policy at higher rates. Securing coverage before your first pitch keeps you competitive and ready to close deals.

Lawsuits Arrive Regardless of Your Intentions

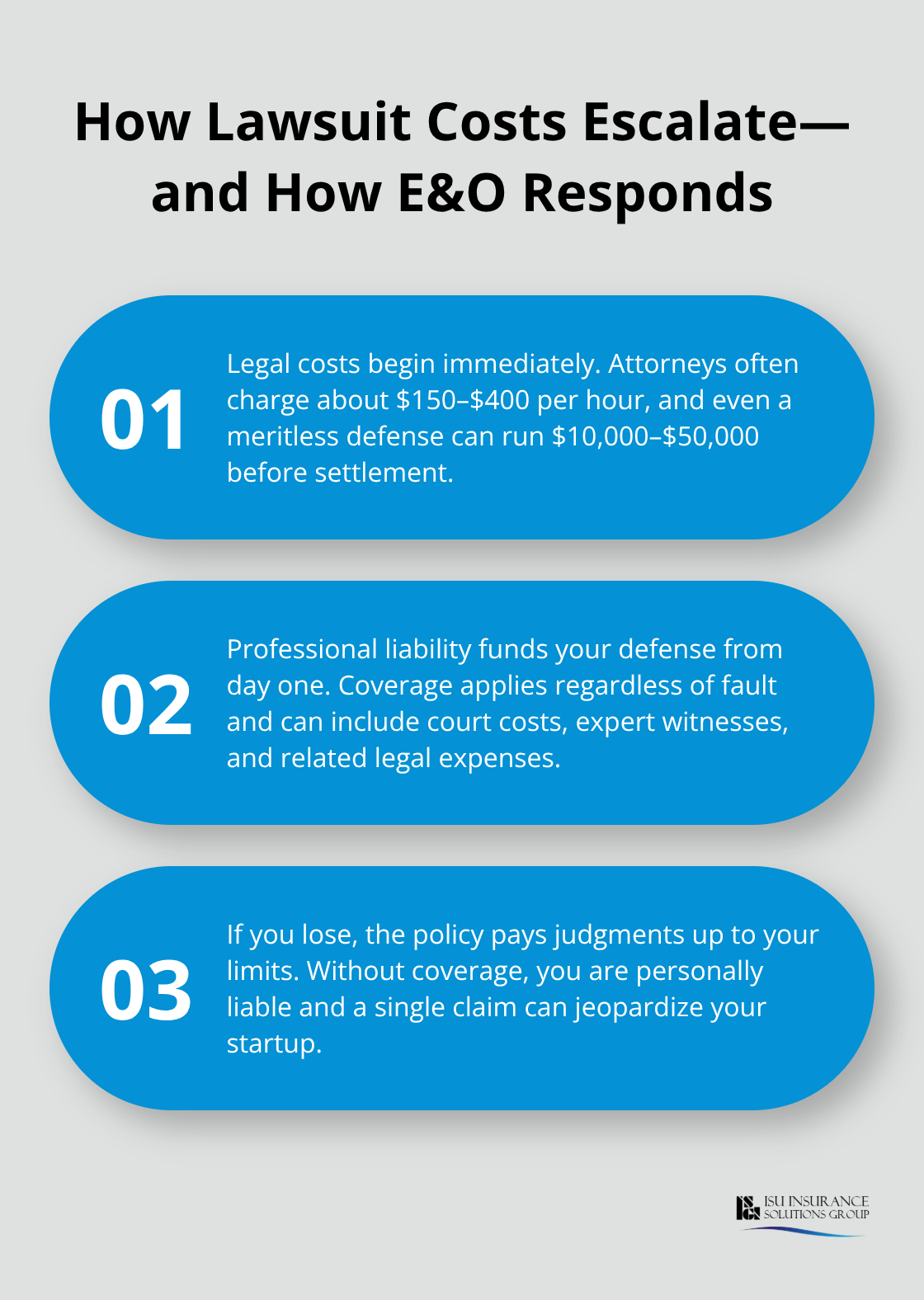

A bookkeeping error that costs a client $50,000 triggers litigation whether you made an honest mistake or acted deliberately. Insureon data from 40,000 small business policies shows that professional liability claims arrive constantly across service industries. Your legal defense costs start immediately-lawyers charge $150 to $400 per hour, and defending even a meritless claim runs $10,000 to $50,000 before settlement. Professional liability insurance covers these costs from day one, regardless of fault. If you lose and owe damages, the policy pays the judgment up to your coverage limits. Without it, you remain personally liable for every dollar.

A single claim can bankrupt a young startup or force you to liquidate personal assets.

Your Insurer Takes Over the Legal Battle

The right-and-duty-to-defend provision in most professional liability policies means your insurer takes over the legal defense rather than leaving you to manage lawyers and court filings while running your business. This matters because defending yourself while building your company is impossible. You focus on operations while your insurer handles the legal strategy, court appearances, and settlement negotiations. This separation protects your time and mental energy during a stressful period.

Professional Liability Protects Your Reputation

Professional liability coverage signals to clients that you’ve insured against risk, which demonstrates professionalism and accountability. Clients see that you take responsibility seriously and have the financial backing to make them whole if something goes wrong. This trust translates into stronger client relationships and repeat business. Your startup’s reputation depends on delivering results, and this coverage protects both your finances and your ability to continue operating after a claim surfaces. As you assess your specific industry risks and determine what coverage limits your clients will require, the next step involves selecting a policy that aligns with your business model and growth trajectory.

Which Coverage Limits Do You Actually Need

Your industry determines your baseline coverage limits more than anything else. A software developer facing a $500,000 client loss needs different protection than an accountant handling million-dollar tax strategies. Start by examining your largest client contracts-most will specify minimum coverage requirements, typically $1 million per occurrence and $2 million aggregate. This isn’t arbitrary; clients set these numbers based on their potential exposure if your work fails. If your biggest prospect demands $2 million in coverage and you only carry $1 million, you lose the deal.

Insureon data from 40,000 small business policies shows that technology startups average $30 to $50 monthly for professional liability, while healthcare and finance startups face $100 to $200 monthly because their error exposure runs higher. Construction-related professional services cost even more due to regulatory complexity.

Your coverage limits and deductibles directly affect your premium-higher limits cost more, but underinsuring yourself creates gaps that could bankrupt you. Try limits that match your actual client demands plus a safety margin, not the minimum that sounds affordable.

Comparing Quotes from Multiple Carriers

Never accept a single quote as your baseline. The Hartford, Liberty Mutual, and Acuity all price professional liability differently based on their underwriting criteria and risk tolerance. One carrier might charge $75 monthly for your IT consulting startup while another quotes $120 for identical coverage. Request quotes from at least three carriers to identify genuine pricing variations. Online platforms can streamline this process and often deliver quotes within hours, but verify that each quote covers the same limits, deductibles, and retroactive dates before comparing prices.

Understanding Deductibles and Their Impact

Deductibles matter significantly-increasing your deductible from $500 to $1,000 can reduce your premium, but only if you can actually afford that deductible during a claim. Most startups overlook this detail and choose the lowest premium without calculating whether they could handle the deductible if litigation arrived next month. A $1,000 deductible sounds manageable until you face a real claim and discover your cash reserves can’t cover it while you wait for settlement.

State Requirements and Location Factors

Your state requirements also affect pricing; some states mandate specific coverage minimums for licensed professions, while others allow flexibility. Location influences rates too-operating in Washington or Oregon may cost differently than other states due to local claims patterns and regulatory environments. If you operate across multiple states, verify that your policy covers all jurisdictions where you conduct business.

Tail Coverage and Policy Transitions

As you evaluate quotes, verify that tail coverage options exist if you ever need to transition carriers, since claims-made policies leave you exposed after cancellation without it. Tail coverage (also called extended reporting period coverage) protects you if a client sues after your policy ends for work you performed while insured. The cost typically runs 150 to 300 percent of your annual premium, but it’s far cheaper than facing an uninsured claim years later.

Final Thoughts

Professional liability insurance protects your startup from financial ruin when clients claim your work caused them harm. Your clients demand it, larger prospects require it in contracts, and a single mistake can cost more than you’ll earn in your first year. Small business professional liability covers legal fees immediately, shifts defense responsibility to your insurer, and pays settlements or judgments up to your policy limits-without it, you remain personally liable for every dollar.

We at ISU Insurance Solutions Group have guided startups and established businesses through this process since 1983. As a Woodinville-based independent agency serving Washington and Oregon, we partner with 20+ carriers to deliver personalized quotes and competitive rates tailored to your specific industry and risk profile. Contact ISU Insurance Solutions Group for a one-call multi-carrier quote and hands-on guidance through the entire process.

Request quotes from multiple carriers to compare pricing and terms, verify that coverage limits match your client requirements, and confirm that tail coverage options exist for future transitions. Most startups secure a policy within days and start operations with protection in place, and the cost averages $61 monthly-a small investment compared to the financial exposure you face without it.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.