Commercial Vehicle Fleet Insurance: Protect Your Entire Fleet

Managing multiple vehicles across your business creates real exposure. One accident, one liability claim, or one uninsured incident can drain your budget fast.

Commercial vehicle fleet insurance consolidates coverage for all your vehicles under one policy, cutting through the complexity of managing separate policies. We at ISU Insurance Solutions Group help businesses like yours find fleet solutions that actually reduce costs while strengthening protection.

What Your Fleet Insurance Actually Covers

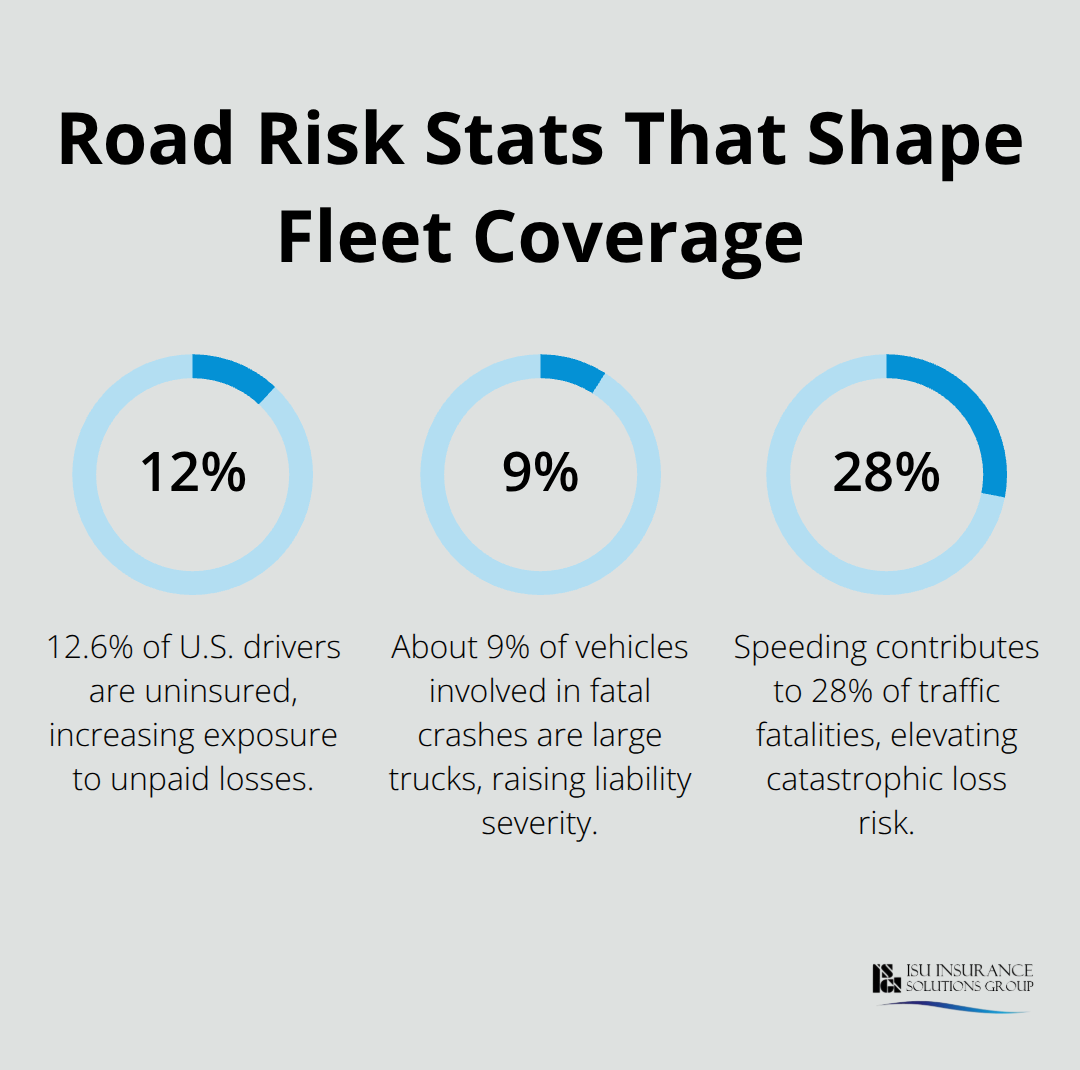

Fleet insurance protects your entire operation against the specific risks your vehicles face on the road. Bodily injury liability covers medical expenses and legal costs when your driver injures someone else, while property damage liability handles damage to other people’s vehicles or property. Physical damage coverage-split into collision and comprehensive-protects your own vehicles from accidents and non-collision events like theft or weather damage. Cargo coverage becomes essential if you transport goods, protecting freight from loss or damage during transit. Uninsured motorist coverage fills a critical gap: roughly 12.6% of drivers nationwide carry no insurance, so this protection shields you when an uninsured or underinsured driver causes an accident. Medical payments coverage handles your drivers’ medical bills regardless of fault, reducing litigation risk. Non-owned auto coverage extends protection when employees use personal vehicles for business purposes, a real exposure many fleet operators overlook.

How Fleet Policies Simplify Your Operations

Individual vehicle policies require you to manage separate renewals, claims, and coverage limits for each vehicle-an administrative burden that grows quickly as your fleet expands. Fleet policies consolidate everything under one policy, meaning one renewal date, one claims process, and uniform liability limits across all vehicles. This simplification matters: you avoid coverage gaps that emerge when individual policies have different limits or exclusions. Premiums typically run around $1,000 per vehicle annually, though your actual cost depends on vehicle type, driver records, mileage, and location. Larger fleets enjoy lower per-vehicle premiums due to volume, while smaller fleets with two to five vehicles still benefit from better rates than individual policies. You can add or remove vehicles anytime without rewriting the entire policy, giving you flexibility as your operations change. Most carriers require at least two vehicles to qualify for fleet coverage, making this option accessible to small and mid-sized operations.

Which Vehicles Qualify for Fleet Coverage

Fleet insurance covers light vehicles like pickup trucks and vans, heavy trucks including semi-tractors and box trucks, and mixed fleets combining different vehicle types under one policy. Specialized vehicles such as those carrying cargo, equipment, or hazardous materials qualify, though cargo coverage and higher liability limits may be necessary. Newer vehicles with advanced safety features often qualify for lower premiums due to better crash protection and theft deterrents. Older vehicles still qualify but typically cost more to insure due to reduced safety technology and higher repair expenses. Most carriers allow you to mix vehicle types within a single policy-delivery vans alongside heavy trucks-without requiring separate policies.

The key requirement is that all vehicles must serve business purposes; personal-use vehicles do not qualify for commercial fleet coverage.

Coverage Limits and Your Specific Needs

Your fleet’s risk profile determines which coverage limits you actually need. A delivery operation with light vehicles faces different exposure than a construction company with heavy equipment trucks or a logistics firm transporting high-value cargo. Review your coverage annually to verify that bodily injury, property damage, and uninsured motorist limits match your actual exposure. Consider hired and non-owned auto coverage if your team regularly uses rental vehicles or personal cars for business tasks. Tailor your policy using your safety data and driver records rather than accepting default insurer recommendations. This approach-selecting coverage that reflects your real operations-sets the foundation for managing your fleet’s total risk exposure.

How Fleet Insurance Cuts Your Operating Costs

Fleet insurance reduces your per-vehicle premium significantly compared to insuring each vehicle separately. On average, fleet insurance costs around $1,000 per vehicle annually, but this figure masks the real savings: larger fleets pay substantially lower per-vehicle rates due to volume discounts that individual policies simply cannot match. A five-vehicle fleet pays less per vehicle than a two-vehicle operation, and a twenty-vehicle fleet pays even less. Your actual premium depends on your specific risk profile-vehicle type, driver records, annual mileage, and location all factor in-but the consolidation itself creates immediate administrative savings.

One Policy Replaces the Administrative Burden

Instead of managing separate renewal dates, separate claims files, and separate coverage limits across multiple policies, you handle one renewal, one claims process, and uniform liability limits. Managing ten individual policies means ten opportunities for coverage gaps, ten different deductibles to track, and ten separate communications with insurers. One consolidated fleet policy eliminates that chaos. You can adjust coverage instantly as your fleet changes, adding or removing vehicles without rewriting entire policies. The bodily injury loss costs rose 9.2% from 2023 to 2024 according to the LexisNexis Risk Auto Insurance Trends Report, driven by uninsured motorists and medical cost inflation, making consolidated coverage and proper liability limits more important than ever.

Data-Driven Negotiations Lower Your Renewal Rates

When you consolidate your fleet, you also consolidate your negotiating power. Insurers recognize that managing one large account costs them less than managing multiple small accounts, and they price accordingly. You can share your fleet’s safety data-telematics information, maintenance logs, driver training records-with your carrier to demonstrate risk management and negotiate better renewal rates. This data-driven approach works: insurers reward fleets that show measurable safety improvements and compliance history.

Claims Processing Moves Faster With One Carrier

A single fleet policy means one claims department, one adjuster relationship, and one streamlined process when incidents occur. Compare this to managing claims across multiple carriers: you might wait for different adjusters, navigate conflicting coverage interpretations, and struggle to coordinate repairs across separate policies. With fleet insurance, your claims experience becomes predictable and faster. Most carriers offer 24/7 claims support and can coordinate repairs through established networks, minimizing vehicle downtime and keeping your operations running. You report the incident once, provide documentation once, and track one claim file rather than juggling multiple carriers’ systems. Every day a vehicle sits in the shop is revenue you do not generate, so faster claims processing means faster repairs and faster return to service.

Uniform Coverage Eliminates Liability Gaps

You also reduce your liability exposure significantly by consolidating coverage. When you maintain separate policies with different liability limits, you create gaps where a serious incident could exceed one policy’s coverage while leaving another policy underutilized. A consolidated fleet policy with uniform bodily injury and property damage limits across all vehicles means you have consistent protection regardless of which vehicle is involved in an accident. This uniform protection is especially critical given that large trucks account for about 9% of all vehicles involved in fatal crashes according to industry data. If your fleet includes heavy trucks, your liability exposure is substantial, and having adequate, consistent coverage across all vehicles protects your business from catastrophic losses. Speeding accounts for 28% of traffic fatalities, and 29% of speeding drivers in fatal crashes lacked valid licenses, according to the LexisNexis report.

These statistics highlight why maintaining strong coverage limits matters: one serious incident can generate litigation costs far exceeding your premium savings. A consolidated fleet policy with proper limits prevents that exposure from bankrupting your operation.

The real cost of fleet insurance extends beyond premiums-it includes the risk management strategies that lower your claims frequency and demonstrate safety leadership to insurers.

Finding the Right Fleet Insurer for Your Operation

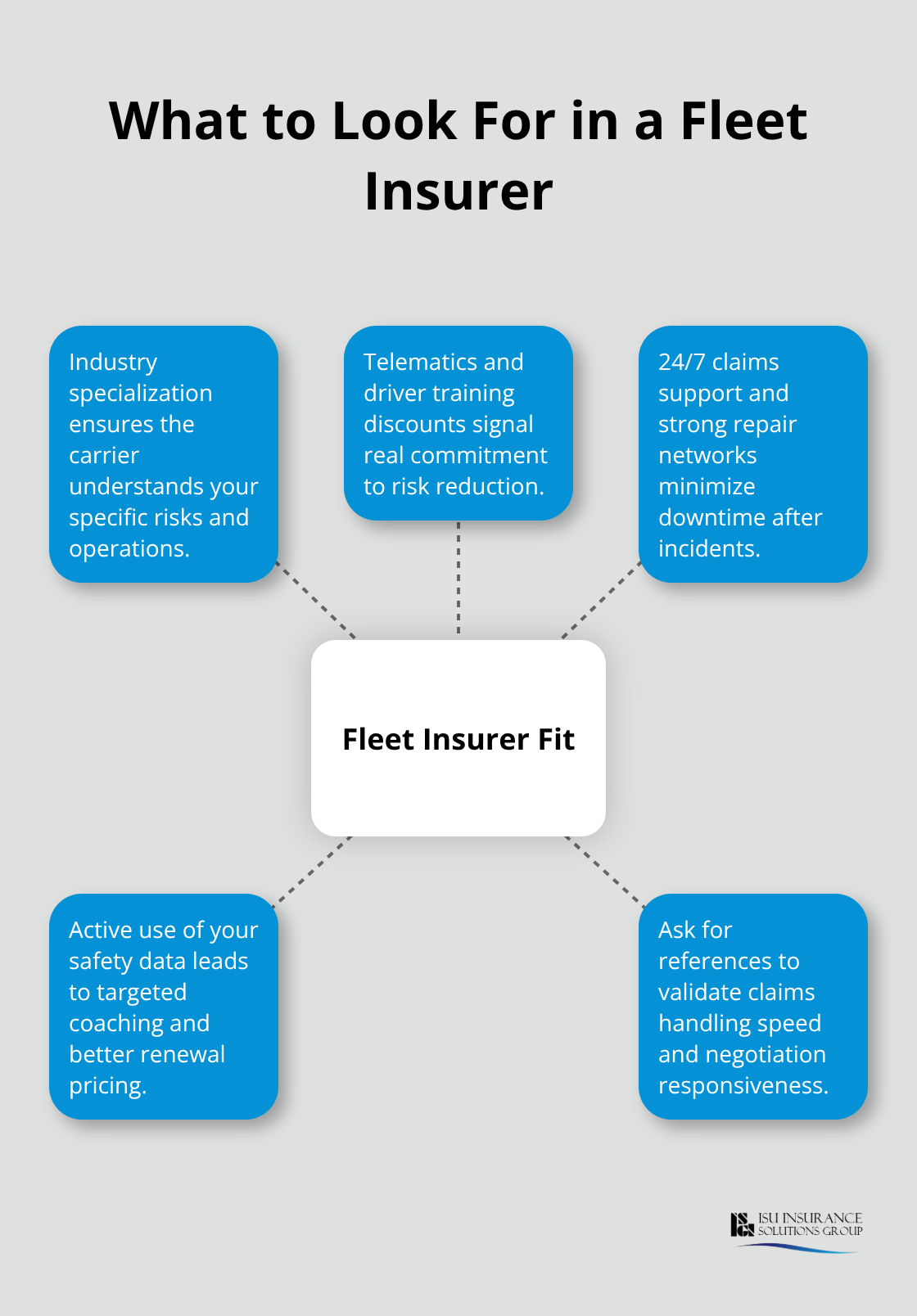

Selecting a fleet insurance carrier matters far more than chasing the lowest quote. Your insurer becomes a partner in managing your fleet’s risk, and the wrong choice costs you in claims delays, coverage gaps, and missed opportunities to reduce premiums through data-driven safety programs. Start by identifying carriers that specialize in commercial auto and understand your specific industry. A carrier experienced in construction fleets thinks differently about risk than one focused on delivery services or logistics operations. Ask potential insurers directly: what discounts do they offer for telematics adoption, driver training programs, and safety certifications? Carriers like Progressive offer 24/7 claims support and extensive truck repair networks, which matters when you need to minimize downtime. The real differentiator is whether your carrier will actively engage with your safety data. Some insurers simply collect telematics information and ignore it; the best ones use that data to identify high-risk drivers, reward safety improvements at renewal, and provide actionable coaching recommendations.

Request references from other fleet operators in your industry and ask specifically about claims handling speed and how the insurer responds to premium renewal negotiations backed by safety improvements.

Assess Your Coverage Limits Honestly

Coverage limits require honest assessment of your actual exposure rather than accepting insurer defaults. If your fleet includes heavy trucks, your bodily injury liability limit should reflect that large trucks represent a significant portion of vehicles in fatal crashes. A construction company with equipment trucks faces different cargo exposure than a delivery service with light vans. Pull your accident history from the past three years and calculate the highest single claim you have experienced, then add 30 percent as your minimum bodily injury limit.

Compare Quotes From Multiple Carriers

Compare quotes from at least three carriers, but do not treat price as the primary factor. A carrier offering 10 percent lower premiums but requiring a $2,500 deductible may cost you more after a claim than a carrier with slightly higher premiums and a $1,000 deductible. Request itemized quotes that break down liability, physical damage, cargo, and uninsured motorist coverage separately so you can see exactly what each carrier charges for each component. During the quoting process, disclose your complete fleet composition, annual mileage, driver ages, and claims history accurately. Misrepresenting information to get lower quotes creates coverage issues when you file a claim.

Identify Carriers That Reward Safety Data

Ask each carrier whether they allow you to implement telematics and what premium reductions they offer for documented safety improvements over time. Carriers that offer 5 to 15 percent discounts for telematics adoption and driver training programs demonstrate commitment to risk reduction rather than just collecting premiums. This approach separates insurers who view your fleet as a long-term partnership from those who simply want your premium dollars.

Evaluate Claims Handling Quality

Claims handling quality separates good carriers from great ones. Request the claims contact information and call that number yourself during business hours to verify response times. Ask whether the carrier has preferred repair shops in your service area and whether they offer rental vehicle coverage while yours is being repaired. A 24-hour First Notice of Loss process and same-day adjuster assignment can reduce your operational disruption significantly. Finally, verify that your carrier can handle FMCSA compliance filings such as MCS-90 and BMC-91X if your fleet operates commercial trucks, as this administrative support prevents costly compliance gaps.

Final Thoughts

Commercial vehicle fleet insurance protects your entire operation by consolidating coverage, reducing administrative burden, and lowering your per-vehicle costs compared to managing separate policies. The real value emerges when you pair your fleet policy with data-driven risk management: telematics monitoring, driver training programs, and maintenance discipline demonstrate safety leadership to insurers and create measurable premium reductions at renewal. Your fleet’s safety record becomes your negotiating advantage, and carriers reward fleets that show consistent improvements in driver behavior and incident prevention.

Starting with fleet insurance requires three concrete steps. First, audit your current coverage across all vehicles and identify gaps where separate policies leave you exposed. Second, gather your fleet data: vehicle types, annual mileage, driver records, and claims history from the past three years. Third, request quotes from multiple carriers that specialize in commercial auto and ask specifically about discounts for telematics, driver training, and safety certifications.

A consolidated fleet policy with uniform coverage limits eliminates liability gaps that could expose your business to catastrophic losses, while faster claims processing keeps your vehicles on the road and your revenue flowing. ISU Insurance Solutions Group serves Washington and Oregon businesses with commercial vehicle fleet insurance tailored to your fleet’s specific needs. Our independent agency partners with over 20 carriers to deliver multi-carrier quotes and hands-on local expertise that finds the right balance of coverage and cost for your operation.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.