What Washington Brewery Insurance Quotes Really Cost for Craft Producers

Washington brewery insurance quotes vary wildly depending on your operation’s size, location, and equipment. We at ISU Insurance Solutions Group have seen premiums range from a few thousand dollars annually for small taprooms to six figures for larger production facilities.

Most breweries underestimate what coverage actually costs because they don’t understand which factors drive pricing. This guide breaks down the real numbers and shows you how to get competitive quotes without overpaying.

What Really Drives Your Brewery Insurance Quote

Revenue and Production Volume Set Your Baseline

Your annual revenue and production volume are the primary levers that insurers pull when pricing your policy. A brewery generating $500,000 in annual sales will pay substantially less than one hitting $5 million, because higher revenue means greater exposure to product liability, spoilage losses, and recall costs. Insurers also scrutinize your barrel-to-package ratios and the number of off-site festivals or events you attend annually. If you attend more than ten festivals per year, carriers expect you to carry $2 million to $5 million in general and liquor liability coverage, which directly inflates your premium.

Location and Regional Risk Factors

Location matters more than many brewers realize. Seattle-area facilities face higher property replacement costs because real estate values have climbed roughly 20 percent since 2020, driving up the insurable value of your building and equipment. A brewery in Spokane typically pays less for property coverage than an identical operation in the Seattle metro area. Washington’s craft beer landscape also creates concentrated risk-the state holds the second-largest concentration of hop acreage globally and ranks fourth in the nation for licensed breweries, according to the Brewers Association 2023 data. This density means local fire marshals and regulators are familiar with brewing risks and may demand specific coverage thresholds before issuing permits.

Equipment Breakdown and Operational Complexity

Your equipment footprint directly correlates to your premium. Boilers, chillers, canning lines, and glycol systems represent significant breakdown exposure. Brewery equipment breakdown coverage helps offset costs associated with spoilage, contamination, and product recall. That coverage illustrates why equipment breakdown protection isn’t optional-it’s essential. Breweries operating taprooms or tasting rooms face multiplied liability exposure because crowds, events, and alcohol service create slip-and-fall and intoxication risks that breweries-only operations don’t encounter. WA juries award premises-liability claims with medians exceeding $250,000, so many brokers recommend at least $2 million in combined single limits for public-facing operations.

Public-Facing Operations and Liquor Liability

If you run an on-premises restaurant or host weddings, your liquor liability costs can jump 3 to 4 times higher than wholesale-only coverage. The Washington Liquor and Cannabis Board requires separate liquor liability proof before licensing, and general liability policies often exclude alcohol-related incidents entirely, so you cannot skip this coverage. Small breweries typically pay $150 to $200 monthly for a $1 million/$2 million liability package, but that baseline shifts upward quickly with production scale, event frequency, or public access. Understanding these cost drivers helps you anticipate what your actual quote will look like and identify where you can negotiate or adjust coverage to fit your budget.

Getting Accurate Brewery Insurance Quotes

Prepare Your Operational Data Before Requesting Quotes

Requesting quotes without proper preparation wastes time and produces misleading numbers. Insurers need specific operational details to price your risk accurately, and vague answers lead to lowball quotes that don’t reflect reality when you actually bind coverage. Start by documenting your annual gross revenue for the past two years, your production volume in barrels, and your specific brewing setup-whether you operate a production facility only, a taproom with on-premises service, or both. Include the number of off-site events or festivals you attend annually, your employee count, and details on major equipment like boilers, chillers, and canning lines. If you serve alcohol on-site, specify whether you operate a full restaurant, limited food service, or tasting-room only. Insurers also scrutinize your building construction type, square footage, and whether you own or lease the space. Many brokers request three years of loss history if you’ve carried coverage before. The more granular your data, the tighter your quotes will be.

Compare Multiple Carriers to Spot Price Variations

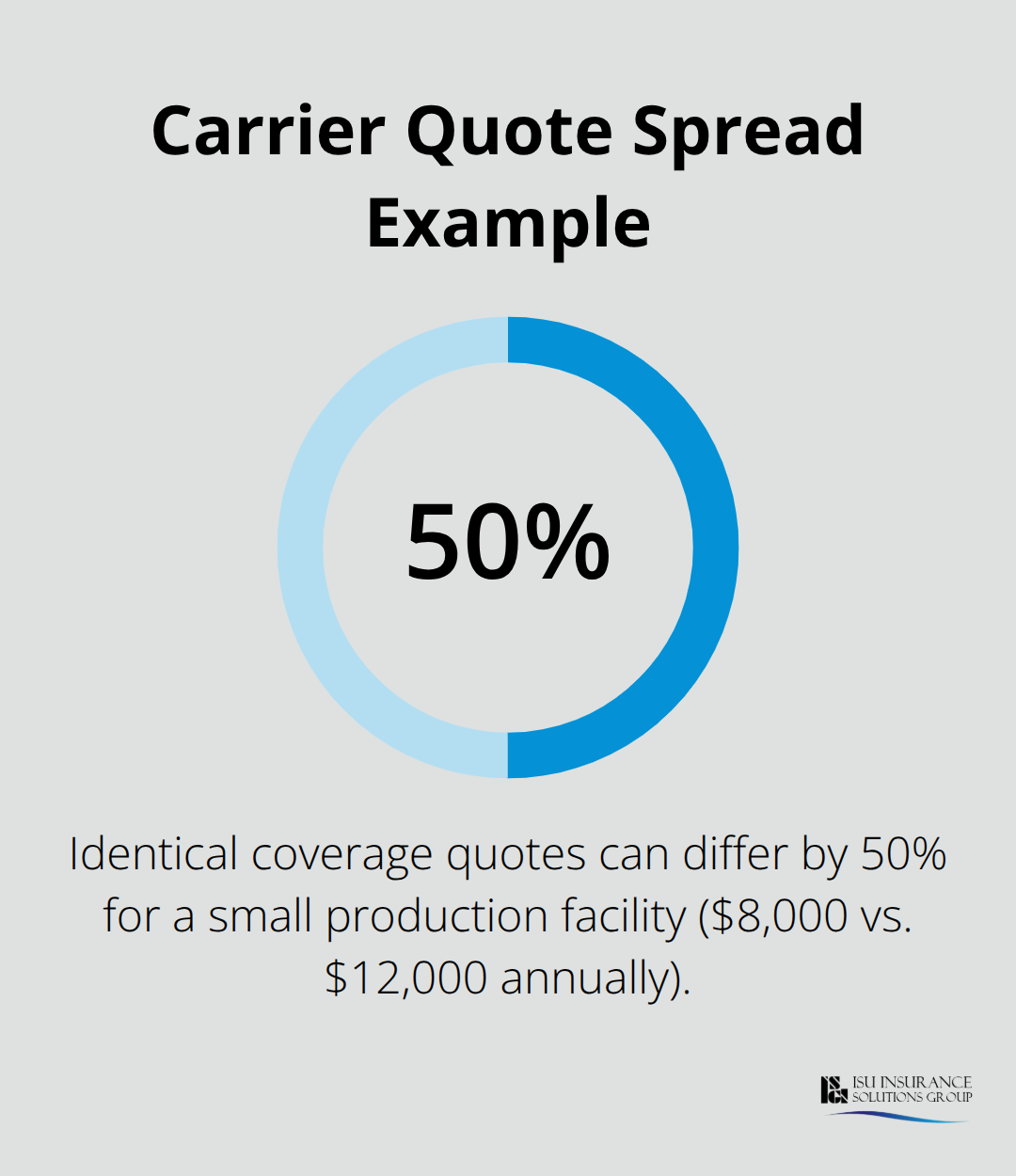

Comparing quotes from multiple carriers is non-negotiable because brewery premiums vary dramatically across insurers. One carrier might quote $8,000 annually for a small production facility while another quotes $12,000 for identical coverage-that’s a 50 percent spread.

Work with an independent agent who can access multiple carriers simultaneously rather than requesting quotes directly from insurers one at a time. An independent agency can pull quotes from 20+ carriers in a single process, saving you weeks of back-and-forth calls.

Identify Red Flags in Quote Pricing

When reviewing quotes, watch for red flags: if a quote seems unusually cheap, verify that it includes liquor liability, equipment breakdown, and spoilage coverage, because some carriers strip out expensive coverages to appear competitive on the base price. Check whether property limits reflect replacement cost rather than depreciated book value, especially in Seattle metro areas. Avoid agents who quote via email without a conversation about your operations-they’re likely using templates and missing critical exposures. A legitimate quote includes specific coverage limits, deductibles, exclusions, and a breakdown of premium by coverage type.

Evaluate Carrier Responsiveness and Support

Request certificates of insurance timelines during the quote process, because some carriers take weeks to issue them, which can delay your licensing. Ultimately, the lowest quote rarely represents the best value if it skips coverage you actually need or comes from a carrier slow to respond during claims. Speed of certificate issuance, references from similar breweries, and broker support for recalls and OSHA audits matter as much as the premium itself. Your next step involves understanding which specific coverage types protect your operation most effectively and where you can adjust limits to balance protection with cost.

Cost-Saving Strategies for Washington Breweries

Bundle Coverage Types for Substantial Savings

Bundling your coverage types into a single brewery-specific policy cuts your premium substantially compared to purchasing general liability, property, and equipment breakdown separately. Carriers offer integrated brewery packages that treat your operation as a cohesive risk rather than three disconnected exposures, which lets them apply volume discounts of 10 to 20 percent. A small production facility paying $12,000 annually for piecemeal coverage might drop to $9,600 to $10,200 with a bundled package. The savings compound when you add spoilage, equipment breakdown, and liquor liability to the same policy because the insurer eliminates duplicate administrative costs and applies a single deductible structure across coverages. This approach also eliminates coverage gaps that emerge when different insurers write different pieces of your risk. Verify that your bundled quote includes liquor liability with adequate limits for your on-premises operations, because some carriers bundle a weak liquor liability component to keep the base price attractive, then surprise you with limitations when you actually need the coverage.

Implement Safety Programs to Reduce Premiums

Safety programs and risk management practices directly reduce your premiums because insurers reward documented loss prevention. Breweries that install CO2 monitoring systems, maintain boiler inspection schedules, and train staff on safe keg handling and wort temperature control see premium reductions of 5 to 15 percent annually. A brewery in Yakima Valley that installed equipment breakdown coverage and spoilage protection avoided catastrophic loss when a glycol leak damaged equipment-the claim paid $145,000 in repairs and reimbursed lost product revenue during a three-week outage that would have otherwise decimated cash flow. Document your safety initiatives in writing and share them with your broker during renewal conversations, because insurers often don’t automatically apply discounts unless you explicitly highlight your risk-management investments.

Select Coverage Limits Based on Actual Exposure

Choosing the right coverage limits requires honest assessment of your actual exposure rather than guessing. A production-only brewery with no public access needs lower general liability limits than a taproom hosting ten events annually, so don’t pay for $2 million in liquor liability if you operate wholesale-only. Conversely, Seattle metro properties should carry property limits reflecting current replacement costs-real estate prices have risen roughly 20 percent since 2020, so your 2021 insurable values no longer match rebuild costs. Request a loss-control visit from your carrier’s engineers, who can walk your facility and recommend specific limits based on your equipment footprint and production setup. This consultation typically costs nothing and produces a detailed report that justifies your coverage choices to your accountant and board while identifying exposures you might otherwise miss.

Final Thoughts

Washington brewery insurance quotes reflect real operational costs that most producers underestimate until they request their first formal quote. Small taprooms pay $1,800 to $2,400 annually for basic coverage, while production facilities with public events and on-premises service climb toward $8,000 to $15,000 or higher depending on revenue and equipment complexity. The gap between these numbers tracks directly to your production volume, location, and whether you serve alcohol on-site.

Evaluating quotes effectively means moving beyond the premium number itself and comparing what each carrier actually covers. Does the quote include liquor liability with adequate limits for your taproom events, or did the carrier strip it out to appear competitive? Does property coverage reflect replacement cost in your Seattle or Spokane location, or does it use depreciated book value that won’t cover a rebuild? Request specific details on deductibles, exclusions, and coverage limits broken down by type, and ask each carrier how quickly they issue certificates of insurance, because delays can hold up your licensing.

Your next step involves connecting with an independent agent who understands Washington’s brewery landscape and can pull quotes from multiple carriers simultaneously. We at ISU Insurance Solutions Group work with 20+ carriers to deliver personalized brewery coverage tailored to your specific operation, and our agents can walk you through the real costs and help you bundle coverages for maximum savings. Contact us to request quotes and get clarity on what your brewery actually needs to protect your assets and stay compliant with state licensing requirements.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.