Commercial Auto Insurance Quotes You Can Trust

Getting commercial auto insurance quotes shouldn’t feel like guessing what your business actually needs. Most fleet owners either overpay for coverage they don’t use or discover gaps when it’s too late.

We at ISU Insurance Solutions Group help business owners cut through the confusion and find quotes that match their real risks. This guide shows you exactly what to look for and how to compare options that actually protect your bottom line.

Why Your Commercial Auto Quote Matters More Than You Think

Most business owners treat commercial auto quotes as a necessary evil rather than a critical business decision. An inaccurate or incomplete quote creates immediate financial exposure. Bodily injury loss costs rose 9.2% from 2023 to 2024, driven by uninsured motorists, medical cost inflation, and speeding-related incidents. When you underestimate your coverage needs, you’re banking on never hitting that cost increase. One serious accident with an underinsured vehicle drains your operational budget faster than any premium increase ever would. The difference between a rushed quote and a properly researched one often determines whether your business survives a major claim or faces crippling liability exposure.

Hidden Financial Traps in Generic Quotes

Generic quotes miss critical details about how your specific business operates. A contractor moving equipment looks nothing like a delivery service, yet many quotes treat them identically. Vehicle repair and replacement costs have spiked dramatically-CPI for motor vehicle maintenance and repair rose 13% from January 2023 to January 2024 according to the Federal Reserve Bank of St. Louis. If your quote doesn’t account for your actual vehicle types, usage patterns, and driver experience levels, you’ll either overpay for unnecessary coverage or face gaps when claims happen.

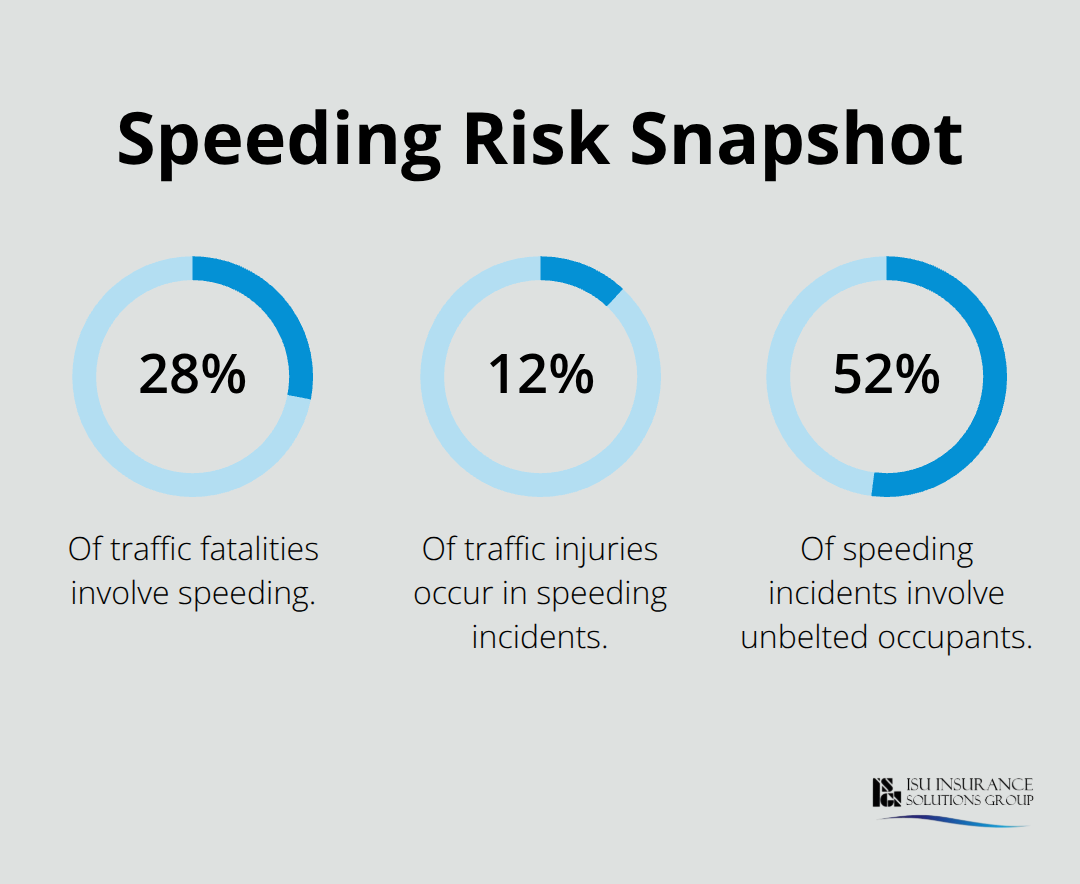

Speeding alone accounts for 28% of traffic fatalities and 12% of injuries, with 52% of speeding incidents involving unbelted occupants, per LexisNexis. Your fleet’s safety record and driver training directly impact your actual risk profile, yet many generic quotes ignore these factors entirely. The cost difference between a customized quote and a one-size-fits-all approach typically ranges from 15% to 30% in annual premiums-money that matters when cash flow is tight.

Comparison Shopping Reveals Real Savings Opportunities

Comparing multiple carrier quotes isn’t about finding the cheapest option; it’s about finding the right coverage at a defensible price. Progressive offers median monthly costs of $219 for business auto customers with clean records and $212 for contractors, though actual rates vary significantly by location, vehicle type, and claims history. When you gather quotes from three or more carriers, you immediately spot which insurers undervalue your business and which ones understand your industry.

Bundling commercial auto with property coverage typically saves around 12% on auto premiums alone, but not every carrier applies this discount equally. Snapshot ProView telematics programs yield approximately 9% average savings for new customers, while established safe-driving records save at least 5%. These discounts stack differently across carriers, which means your lowest quote from one insurer might be your highest from another once you layer in available savings.

Why Your Current Policy Information Matters

Your declarations page serves as a starting point for accurate quotes and demonstrates continuous coverage, which can save up to 25% on premiums. Without comparison shopping, you’re essentially paying whatever your first quote suggests. When you provide current policy information to multiple carriers, you enable them to assess your actual needs and apply relevant discounts. This transparency also reveals which carriers truly understand your industry and which ones apply a generic approach. The next section walks you through exactly what information you need to gather before requesting quotes.

What Actually Protects Your Fleet in a Commercial Auto Quote

The Foundation: Auto Liability and Medical Coverage

Auto liability coverage forms the foundation of every commercial auto quote, and many insurers recommend maintaining at least $1,000,000 per vehicle, with $500,000 as the minimum to avoid leaving your business exposed. Many business owners accept the minimum liability limits their state requires, which is a dangerous mistake-one serious accident involving an injured third party can generate costs far exceeding state minimums. Medical payments coverage sits alongside liability in your quote and pays medical expenses for you, employees, and passengers after an accident regardless of fault, up to your policy limits. This coverage matters because it accelerates claim resolution and prevents employees from suing your business directly.

Physical Damage Protection: Collision and Comprehensive

Collision coverage handles damage to your vehicles from impacts with other vehicles or objects, while comprehensive coverage protects against theft, vandalism, weather damage, and animal strikes. Both require deductibles, typically ranging from $500 to $2,500, and here’s where most business owners make poor decisions: they choose high deductibles to lower premiums without calculating their actual cash flow impact. A $2,500 deductible saves roughly 15-20% on premiums, but if you operate five vehicles and experience two collisions annually, you absorb $5,000 in out-of-pocket costs-money that could have been prevented with a $1,000 deductible and slightly higher premiums.

Protection Against Uninsured Drivers and Equipment

Uninsured and underinsured motorist coverage protects your drivers when at-fault drivers carry insufficient or no insurance, covering medical expenses and lost income for your team. High-risk industries like construction, plumbing, and delivery services face elevated exposure to uninsured motorists, making this coverage non-negotiable in your quote. Contractors and service providers should specifically request inland marine coverage protection for tools and equipment permanently mounted on vehicles, since standard commercial auto policies exclude loose tools.

Operational Support: Roadside Assistance and Beyond

Roadside assistance included in most quotes prevents costly downtime-24/7 towing, fuel delivery, and jumpstart services keep your fleet operational during emergencies. Your quote comparison should directly address which carriers offer these services without additional fees and which ones charge per incident. The deductible structure you select ultimately determines your risk tolerance and monthly cash burn, so resist the temptation to chase the lowest premium without stress-testing that deductible against your actual accident frequency and available reserves. Once you understand what protections matter most for your operation, commercial auto insurance agents can help you gather the specific information that carriers need to build accurate quotes tailored to your business.

Getting Accurate Commercial Auto Insurance Quotes

Compile Your Vehicle and Driver Information First

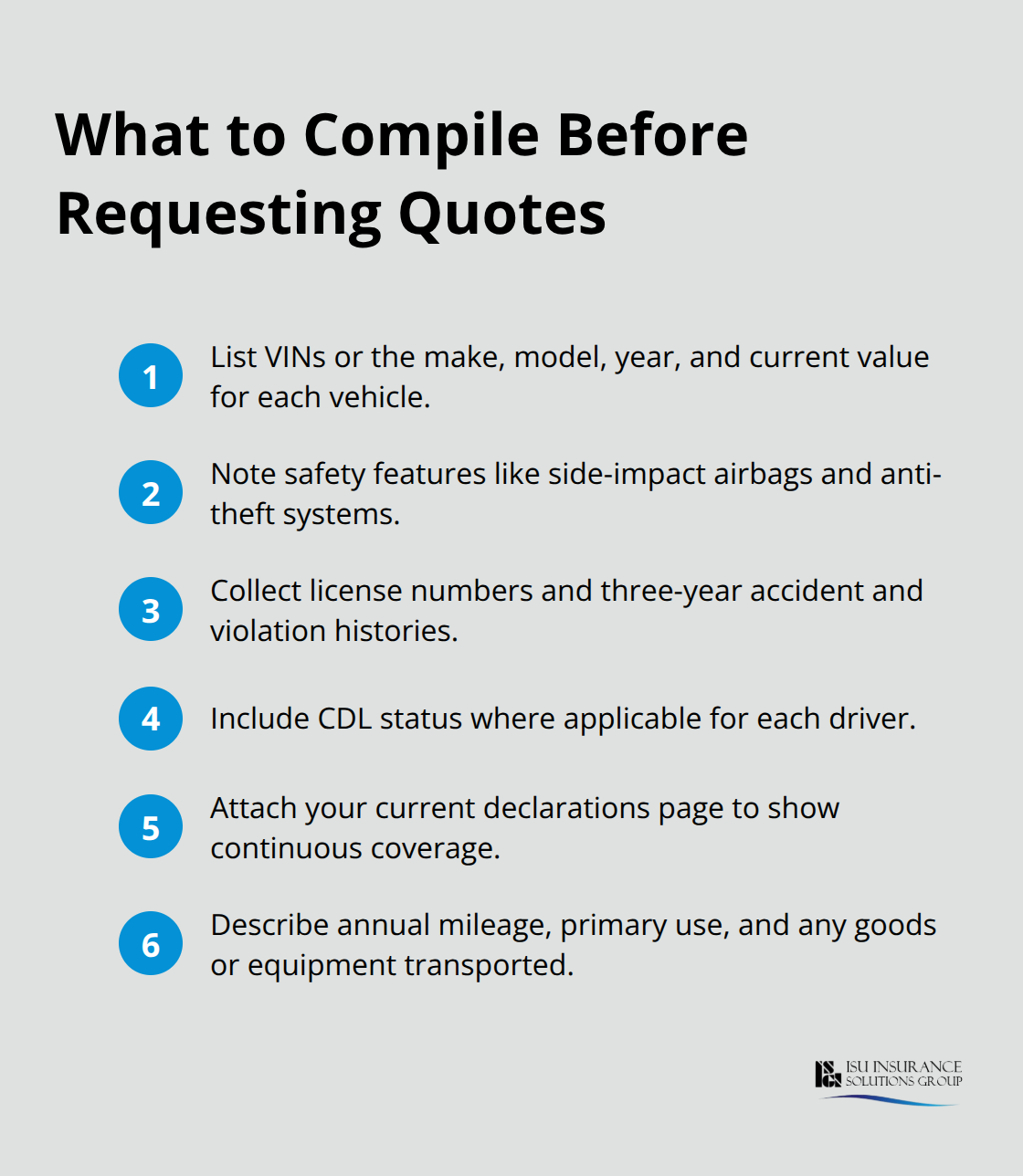

Start with your vehicle inventory and include specific details: VIN numbers for each vehicle, or at minimum the make, model, year, and current value. Safety features like side-impact airbags or anti-theft systems directly reduce premiums, so carriers won’t find these details independently. Next, document your drivers with precision-license numbers, three-year accident and violation histories, and CDL status if applicable. Progressive requires this driver-level detail to assess actual risk, and carriers that accept vague driver information typically underprice initially, then adjust rates upward at renewal once they obtain real records.

Gather your current declarations page from your existing policy, which demonstrates continuous coverage and qualifies you for discounts reaching up to 25% on premiums. This single document accelerates the quote process dramatically. Document how each vehicle operates: annual mileage, primary business use, whether employees drive personal vehicles for work, and any goods or equipment transported. A contractor hauling ladders faces different exposure than a salon owner using one vehicle for client visits, yet many business owners provide identical information across quotes.

Document Your Safety Practices and Risk Management

Compile your safety infrastructure-formal driver training programs, distracted driving policies, and fleet management systems. These reduce risk measurably and carriers reward them with discounts, but only if you mention them explicitly. Speeding-related crashes account for 29% of traffic fatalities, so carriers want to know what steps you take to prevent this exposure in your fleet. Your safety record and driver training directly impact your actual risk profile, yet many quotes ignore these factors entirely.

Work with Local Agents for Multi-Carrier Quotes

Local independent agents outperform online quote tools because they understand your specific industry and regional risk factors. An agent familiar with Washington and Oregon construction markets knows the local exposure landscape and can recommend coverage limits that actually reflect your risk rather than state minimums. More importantly, agents shop multiple carriers simultaneously rather than forcing you to visit each insurer’s website separately, collapsing what could take weeks into a single conversation.

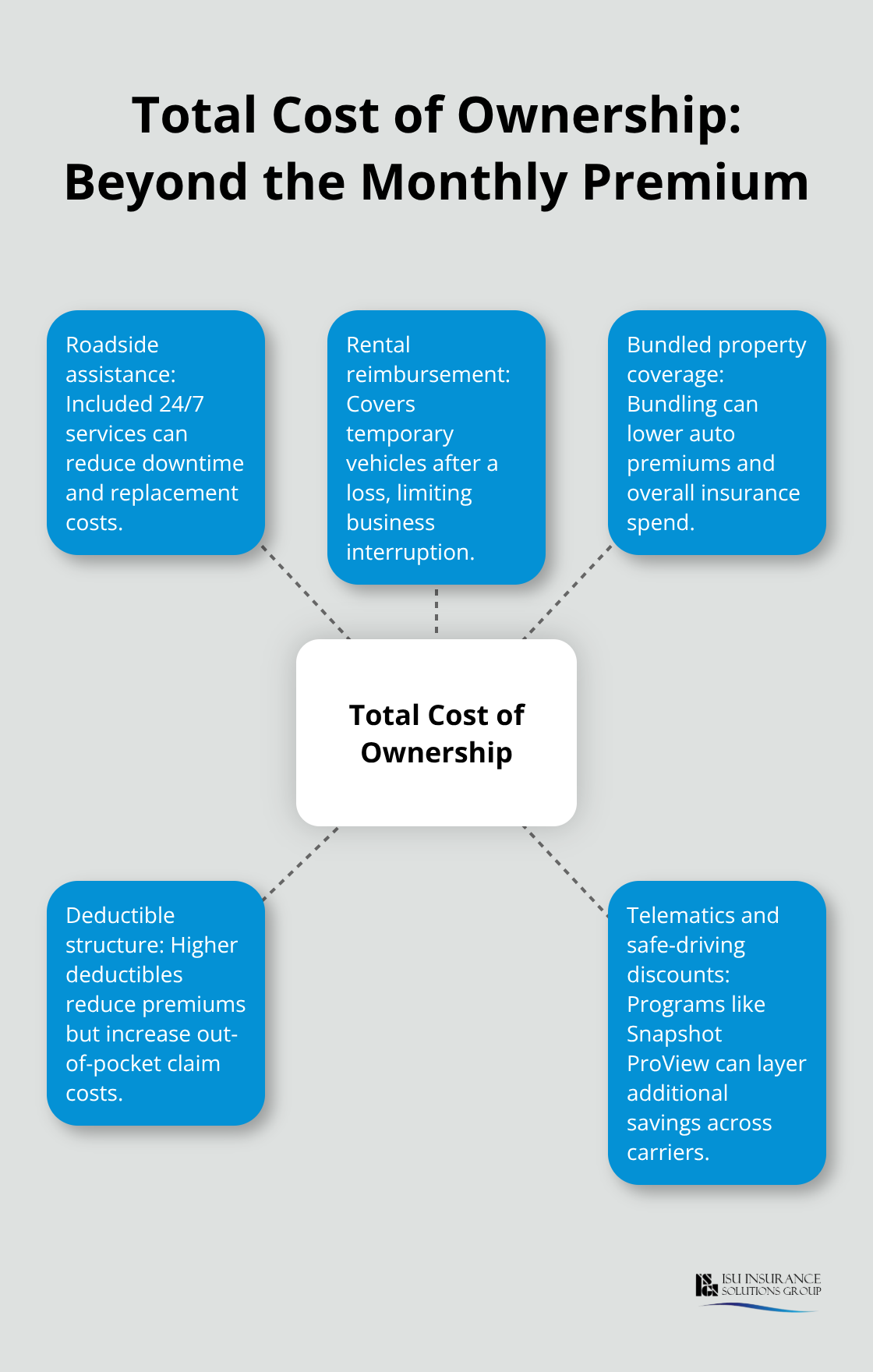

Insurance Solutions Group, a Woodinville-based independent agency serving Washington and Oregon since 1983, provides one-call multi-carrier quotes that compare options from 20+ carriers, eliminating the administrative burden entirely. When comparing quotes across carriers, focus on total cost of ownership, not just premium. A quote that costs $250 monthly but includes roadside assistance, rental reimbursement, and bundled property coverage often outperforms a $220 quote missing those components.

Compare Total Cost, Not Just Monthly Premium

Calculate what a $1,500 deductible actually costs you annually based on your historical claim frequency-if you file one collision claim every two years, a higher deductible saves less than the premium difference costs. Request quotes with identical coverage limits and deductibles across all carriers so you’re comparing actual pricing differences rather than coverage variations masking premium disparities. Progressive’s median rates of $219 monthly for business auto and $212 for contractors provide benchmarks, but your actual quote depends entirely on the specifics you provide and the accuracy of your driver records and vehicle information.

Final Thoughts

Evaluating commercial auto insurance quotes requires you to look beyond the monthly premium and assess total coverage value against your actual business operations. The quotes you gather should reflect your specific vehicle types, driver records, safety practices, and industry exposure rather than generic assumptions about how your business operates. A $219 monthly quote means nothing if it leaves gaps in coverage or includes deductibles that strain your cash flow after a claim.

Compare quotes with identical coverage limits and deductibles across multiple carriers, calculate the real cost of higher deductibles based on your historical claim frequency, and verify that bundled discounts and telematics savings apply equally across options. Gather your vehicle inventory, driver information, and current declarations page, then request commercial auto insurance quotes from multiple carriers simultaneously rather than visiting each insurer individually. This approach collapses weeks of administrative work into a single conversation and immediately reveals which carriers understand your industry.

Finding the right insurance partner means working with agents who understand your regional market and can access multiple carriers without forcing you to manage the comparison process yourself. ISU Insurance Solutions Group serves Washington and Oregon businesses with one-call multi-carrier quotes from 20+ carriers, eliminating the burden of shopping independently. Since 1983, we have helped contractors, delivery services, and other commercial operators find coverage built on accurate information and competitive pricing.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.