Contractor Professional Liability Insurance: Reducing Risk On the Job Site

One mistake on a job site can cost your business thousands in legal fees and settlements. Contractor professional liability insurance protects you when clients claim you caused financial losses through design errors, negligence, or project delays.

At ISU Insurance Solutions Group, we help contractors understand what coverage actually matters for their specific risks. The right policy can be the difference between staying in business and facing bankruptcy.

Why Contractors Need Professional Liability Insurance

Client lawsuits over design errors, missed deadlines, or construction defects happen far more often than most contractors expect. Professional liability insurance covers design errors and construction negligence claims (also called errors and omissions or E&O), protecting your business when a client alleges you caused financial losses through negligence or breach of contract. Without this coverage, you’re personally liable for legal defense costs, settlements, and judgments-expenses that can easily reach tens of thousands of dollars even before a case goes to trial. Professional liability claims often exceed significant figures when design flaws trigger project delays or structural remediation. Construction professional liability specifically addresses design-driven exposures that general liability policies explicitly exclude, meaning your standard CGL won’t protect you when a client claims your engineering judgment or construction management decisions caused harm.

Why Design Errors Cost More Than You Think

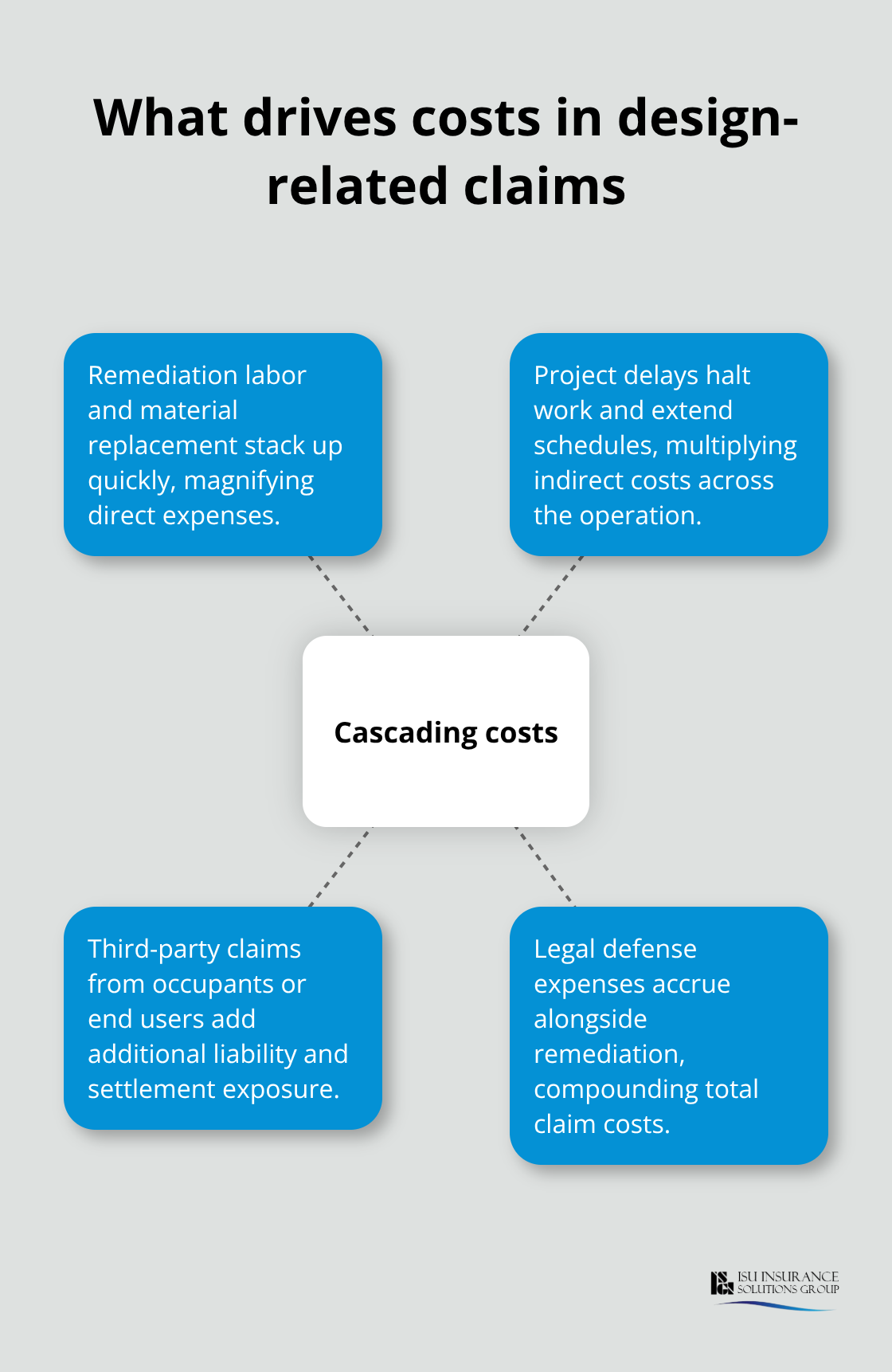

Design defects and construction negligence claims are expensive because they trigger cascading costs: remediation labor, material replacement, project delays, and third-party claims from end users or building occupants. A structural deficiency discovered mid-project halts work for weeks, multiplying indirect costs across your entire operation. Professional liability coverage funds these remediation expenses and pays legal defense costs, allowing you to focus on fixing the problem rather than depleting cash reserves. Contractors offering design-build services face the highest exposure because they control both design and execution, making them liable for errors in either phase. If you’re a general contractor managing design professionals or subcontractors, contractor protective professional indemnity (CPPI) coverage protects you from losses caused by their negligence, filling a critical gap when their insurance limits fall short.

Coverage Limits Matter More Than Price

Standard professional liability policies for contractors typically offer $1 million per occurrence and $2 million aggregate limits, but your actual exposure depends on project value and contract language. Owners increasingly require minimum professional liability limits as a condition of bidding, and failing to meet those thresholds disqualifies you before the work begins. Premiums rise with higher limits and fall with higher deductibles, so choosing a $2,500 or $5,000 deductible instead of $1,000 can reduce your annual cost significantly. The real actionable step is comparing quotes from multiple carriers-premium variation is substantial-and verifying that your chosen policy actually covers the services you provide, especially if you move into design-build or construction management roles where exposure expands.

What Happens When You Don’t Have the Right Coverage

A single claim without professional liability insurance can wipe out years of profit. Your general liability policy excludes professional services exposure, leaving you unprotected when clients claim you made design errors or failed to meet professional standards. Legal defense costs alone can reach $10,000 to $50,000 before settlement negotiations even begin, and that’s before you pay any judgment or settlement amount. Subcontractors with insufficient insurance limits create additional exposure for you as the general contractor-their mistakes become your financial responsibility if their coverage runs out. Without CPPI or owner’s protective professional indemnity (OPPI) coverage, you absorb the full cost of remediation when design professionals or subcontractors cause losses on your project.

Understanding your specific risk exposure and selecting appropriate limits sets the foundation for protecting your business. The next step is recognizing which claims actually occur on job sites and how they develop into costly disputes.

Common Claims and Real-World Scenarios

Structural Defects Create the Costliest Claims

Structural defects discovered during construction or after handover represent the most expensive professional liability claims contractors face. When a foundation settles unevenly, a roof framing calculation proves inadequate, or mechanical systems fail to meet code, remediation costs spiral fast. A mid-project discovery of structural deficiency halts work for weeks while engineers reassess the design, subcontractors mobilize for repairs, and project timelines slip. The contractor absorbs delay costs, material waste, and labor inefficiency while clients demand compensation for extended schedules and disrupted operations.

These claims frequently exceed $100,000 because they trigger simultaneous exposure: your remediation costs, third-party claims from building occupants or end users, and project delay damages. Design-build contractors face the highest frequency here because they control both design and execution, meaning they cannot deflect responsibility to a separate design firm. General contractors managing subcontractors also face significant exposure when a trade contractor’s negligence (poor workmanship, missed specifications, code violations) creates a deficiency that surfaces months later.

Your professional liability policy must explicitly cover remediation costs and project delay damages, not just legal defense. Many basic policies exclude these unless you specifically negotiate coverage. One structural claim can consume 20 to 30 percent of annual profit if you remain uninsured or underinsured.

Project Delays and Cost Overruns Trigger Secondary Claims

Project delays and cost overruns triggered by your design or management decisions create a second wave of claims that clients pursue aggressively. When a contractor’s construction sequencing error delays the critical path by six weeks, or a design change order driven by the contractor’s oversight doubles material costs, owners file claims for indirect damages: lost rent, financing costs, operational downtime, and delay penalties. These claims often exceed direct remediation costs because they capture the owner’s full financial exposure across the entire project timeline.

Owners calculate delay damages based on the project’s total duration and financial impact, which means a six-week delay on a $5 million project generates substantial claims. Your professional liability coverage must address these indirect costs, or you face the full exposure yourself.

Bodily Injury and Property Damage Disputes Complicate Coverage

Bodily injury and property damage disputes arising from construction defects add complexity because they blend professional liability with general liability exposure. If your design error or construction negligence causes a worker injury or damages adjacent property, both your CGL and professional liability policies may be triggered, and determining coverage boundaries becomes contentious. A structural deficiency that causes a worker fall, for example, creates dual liability: negligence in design or construction management (professional liability) plus negligence in site safety (general liability).

Carriers often dispute which policy responds first, delaying claim resolution and leaving you exposed if either policy has gaps or insufficient limits. A single incident can activate multiple coverage disputes simultaneously, which is why selecting appropriate limits and verifying policy language matters far more than shopping purely on premium. Understanding how claims develop across your entire insurance portfolio-not just professional liability alone-determines whether you recover or absorb the full cost.

Selecting Coverage That Matches Your Actual Risk

Audit Your Service Offerings and Exposures

Start with a complete inventory of every service your business performs, not just the primary work. Many contractors underestimate exposure because they offer multiple service lines-general contracting, construction management, design-build, or trade work-without recognizing that each carries different professional liability risk. Design-build work exposes you to professional liability insurance, making it riskier than general contracting alone. Construction management services trigger liability for project sequencing decisions, cost control, and schedule management, all of which create claim exposure distinct from trade work. A roofing contractor who occasionally provides design consultation faces exposure that pure installation work does not.

Document your service offerings in writing, then cross-reference them against your current policy language to verify what’s actually covered. Many contractors discover gaps only after a claim arises and their carrier denies coverage because the service wasn’t explicitly listed. Your professional liability limit should reflect your project values and contract requirements.

Match Your Coverage Limits to Project Value and Contract Demands

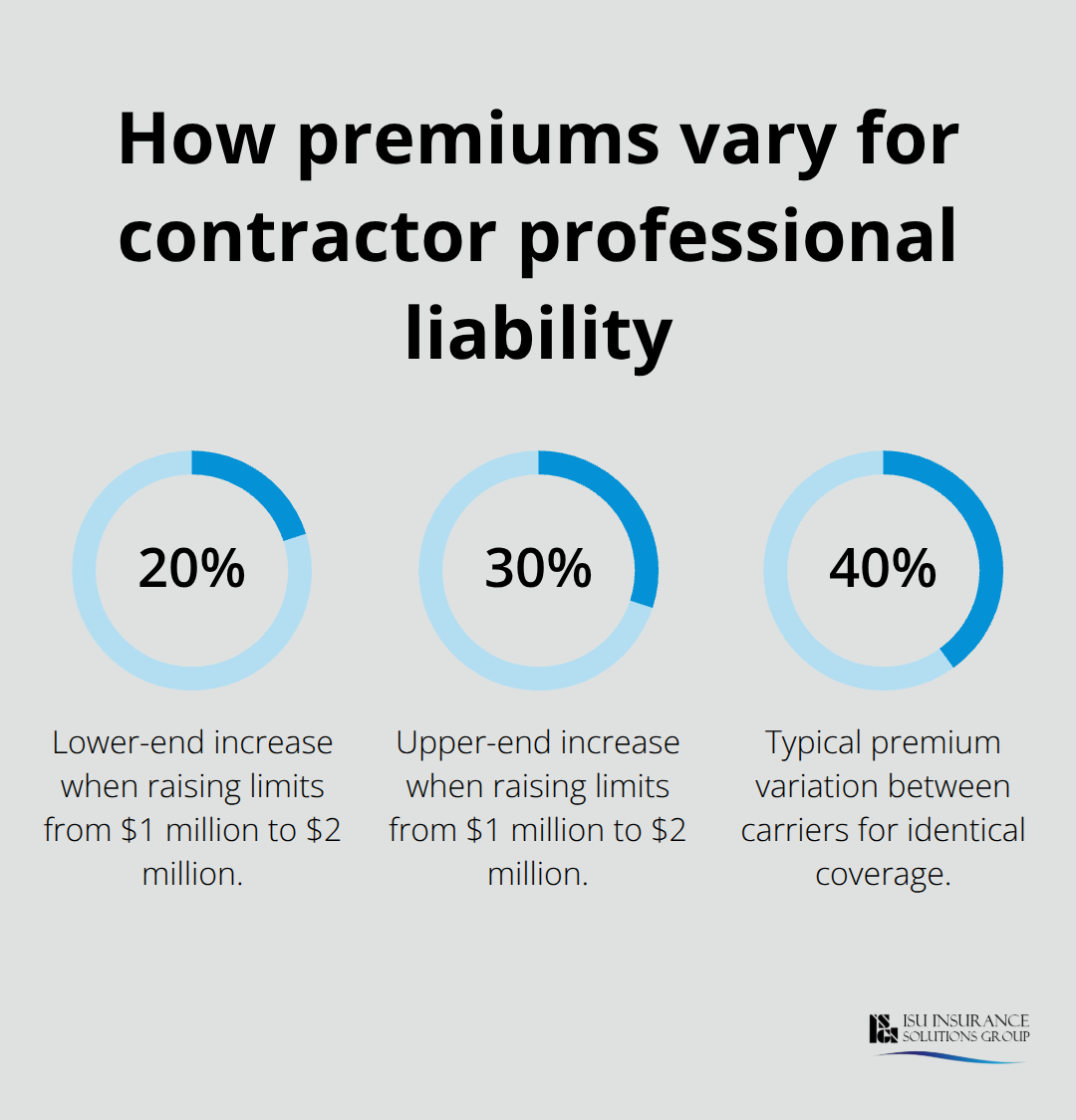

Standard $1 million per occurrence limits work for projects under $5 million, but larger projects or clients with strict insurance requirements demand higher limits. Review your client contracts for coverage requirements before renewal-many owners now mandate $2 million or $5 million limits as a condition of award, and quoting without those limits wastes your proposal effort. Increasing your limit from $1 million to $2 million typically costs 20 to 30 percent more in annual premium, but losing a project bid because you lack required coverage costs far more.

Get quotes from at least three carriers using identical coverage specifications-limits, deductibles, services, and project types-so you can compare apples to apples. Premium variation between carriers for identical coverage often exceeds 40 percent, meaning a $2,000 annual difference for the same protection is normal.

Choose Your Deductible Based on Claim Frequency

Your deductible choice directly impacts your cash flow. A $1,000 deductible costs significantly more than a $5,000 deductible, but the higher deductible means you pay more out of pocket on every claim. For contractors with strong safety records and low historical claims, a $5,000 deductible often makes sense because claims are infrequent enough that the premium savings outweigh occasional out-of-pocket costs. High-risk trades like electrical work or structural design should stick with lower deductibles because claim frequency justifies the extra premium.

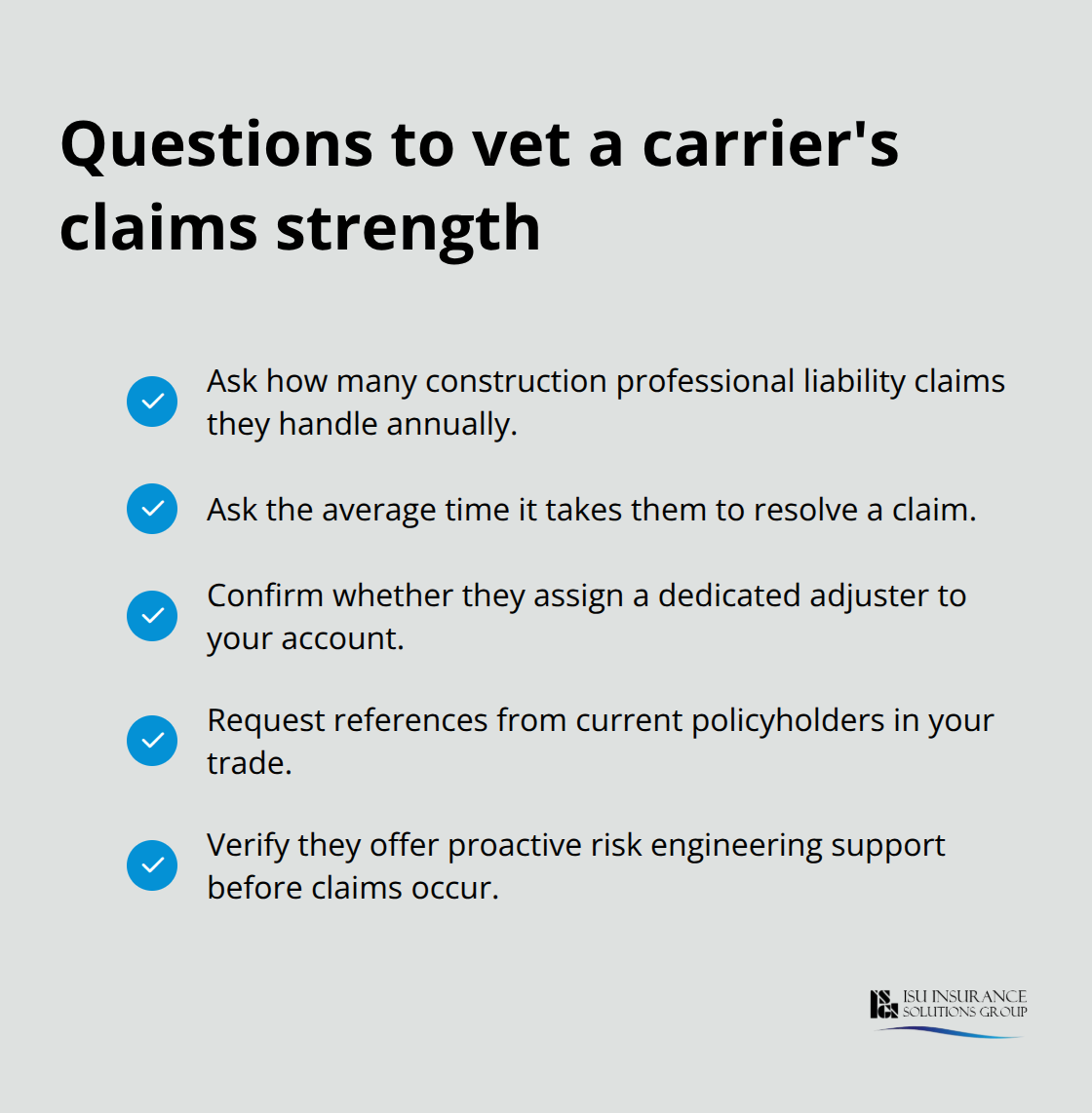

Evaluate Carrier Reputation and Claims Support

Carrier reputation and claims support determine whether you recover financially or absorb losses. When a claim arises, your carrier’s claims team either works efficiently to resolve it or creates additional friction that extends your exposure and legal costs. Carriers with in-house construction claims teams and dedicated adjusters familiar with construction defect disputes resolve claims faster and more fairly than carriers with generic claims operations.

Ask prospective carriers how many construction professional liability claims they handle annually, how long their average claim takes to resolve, and whether they assign a dedicated adjuster to your account. A carrier that handles 500 construction claims annually understands construction defects and delay damages better than one handling 50. Request references from current policyholders in your trade-ask them directly about claim experience and whether the carrier responded promptly and fairly when disputes arose.

Carriers rated A+ (Superior) by A.M. Best have stronger financial capacity to pay claims without delay or dispute, which matters more than you might think when claims exceed $100,000. Verify that your carrier offers risk engineering support before a claim occurs-some carriers provide safety consultations, document review, and loss prevention guidance that actually reduce claim frequency. This proactive support demonstrates a carrier committed to long-term partnership rather than one-off policy sales.

Establish Clear Notice Requirements with Your Carrier

When evaluating carriers, ask whether they require you to notify them of potential claims or potential loss situations before they develop into formal claims. Carriers that demand immediate notice of potential exposures allow them to engage early, often reducing severity by helping you address problems before they escalate. Delayed notice frequently triggers coverage disputes and claim denials, so a carrier with clear, reasonable notice requirements protects you better than one with aggressive timelines.

Final Thoughts

Contractor professional liability insurance protects your business from the financial devastation that follows a single design error, construction deficiency, or project delay claim. One structural defect claim consumes 20 to 30 percent of annual profit, while legal defense costs alone reach tens of thousands before settlement negotiations begin. Your general liability policy explicitly excludes professional services exposure, leaving you completely unprotected when clients allege negligence in design, construction management, or engineering judgment.

Audit your service offerings and match your coverage limits to your actual project values and client contract requirements. Standard $1 million limits work for smaller projects, but larger clients increasingly demand $2 million or $5 million limits as a condition of award-quoting without those limits wastes your proposal effort. Compare quotes from at least three carriers using identical specifications so you identify the 40 percent premium variation that typically exists between carriers for identical coverage.

Evaluate carrier reputation and claims support by asking how many construction claims they handle annually, whether they assign dedicated adjusters, and whether they offer proactive risk engineering before claims occur. We at ISU Insurance Solutions Group understand the specific risks contractors face across Washington and Oregon, and our local agents provide one-call multi-carrier quotes to help you secure appropriate contractor professional liability insurance at competitive rates. Reach out to discuss your coverage needs and verify that your current policy actually protects your business against the claims that matter most.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.