Professional Liability Insurance: For Businesses That Need Real Risk Coverage

One mistake we see constantly: business owners underestimate how quickly a single client complaint can turn into a lawsuit. Professional liability for businesses isn’t optional-it’s the difference between surviving a claim and facing financial ruin.

At ISU Insurance Solutions Group, we work with service providers, consultants, and professionals who understand that their reputation and finances need protection. The right coverage catches what general liability misses, covering negligence claims, defense costs, and errors that could otherwise drain your business.

Who Needs Professional Liability Insurance

High-Risk Professions Face the Most Exposure

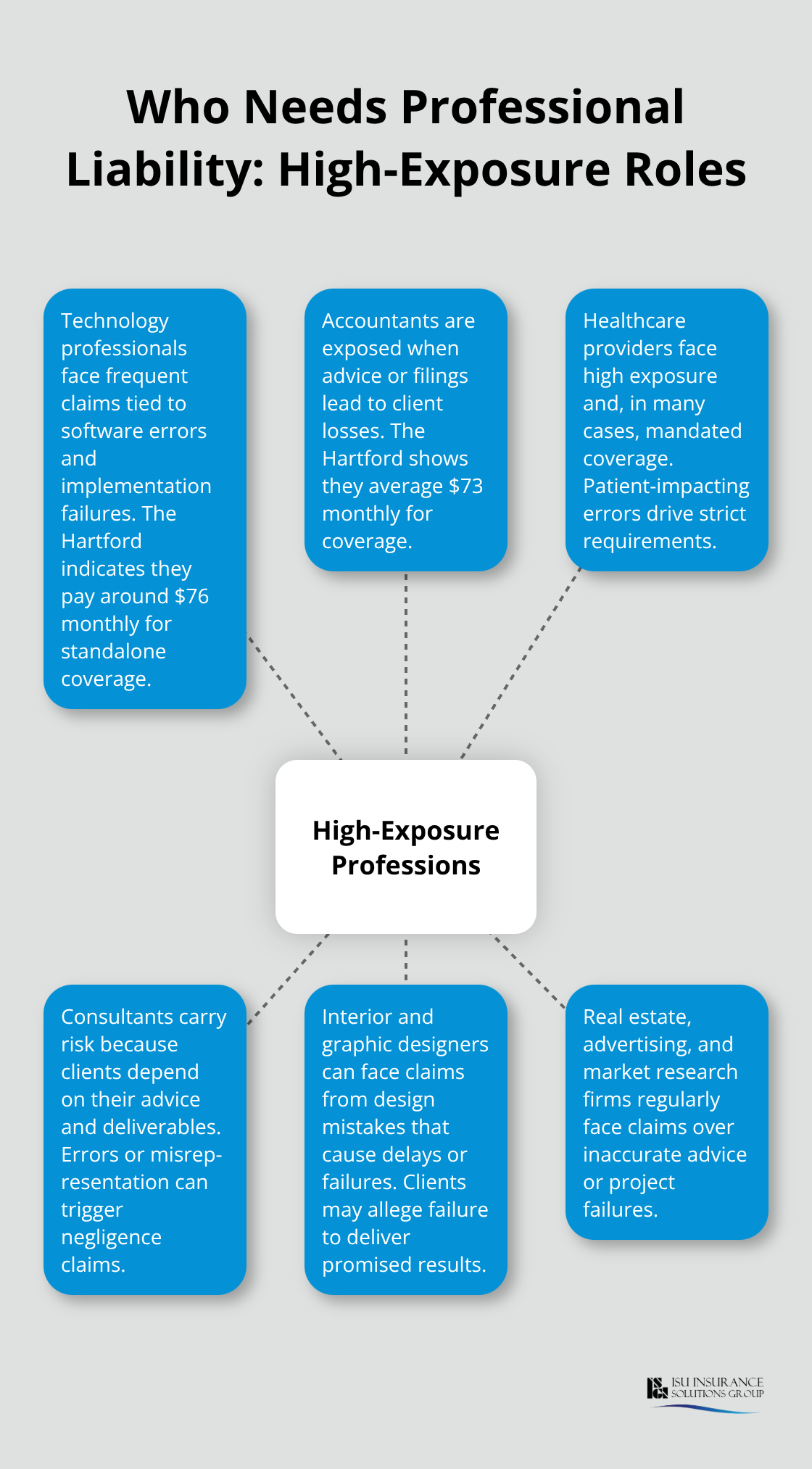

Accountants, consultants, interior designers, graphic designers, technology professionals, and healthcare providers face the highest exposure to professional liability claims. The Hartford’s pricing data reveals this reality: technology professionals pay around $76 monthly for standalone coverage, while accountants average $73 monthly. These price differences exist because certain professions generate more frequent claims. If your business involves giving advice, designing solutions, or providing services that clients depend on financially, you need this coverage.

Service-based businesses especially cannot afford to skip it-a single error in your work can trigger lawsuits alleging negligence, misrepresentation, or failure to deliver promised results. Many clients now require proof of professional liability insurance before signing contracts, making it a business requirement rather than an optional add-on. Real estate professionals, advertising agencies, and market research firms also face regular exposure to claims over inaccurate advice or project failures.

When Contracts and Regulations Demand Coverage

The cost varies significantly by industry, location, and your claims history, but ignoring the risk costs far more when a claim arrives. Healthcare professionals operate under additional pressure since some states and hospitals mandate professional liability coverage as a condition of practice. Technology firms handle increasing liability exposure as software errors, data breaches, or implementation failures can cost clients thousands or millions.

Financial services professionals, tax consultants, and bookkeepers face similar pressure because client losses from their errors are directly traceable and quantifiable. The Hartford’s data shows healthcare professionals face strict coverage requirements in many jurisdictions. Contractors and construction consultants need coverage for design flaws or project delays that harm clients financially.

The Real Cost of Operating Without Protection

If your contracts mention errors and omissions coverage or if state regulations apply to your profession, waiting until a claim arrives means operating without protection when you need it most. The decision isn’t whether your industry might face claims-it’s whether you can afford to pay defense costs, settlements, and judgments from your own pocket when a client sues. Understanding which professions face the highest exposure helps you assess your own risk level and determine what coverage limits make sense for your operation.

What Professional Liability Insurance Actually Covers

Financial Protection When Your Services Cause Client Losses

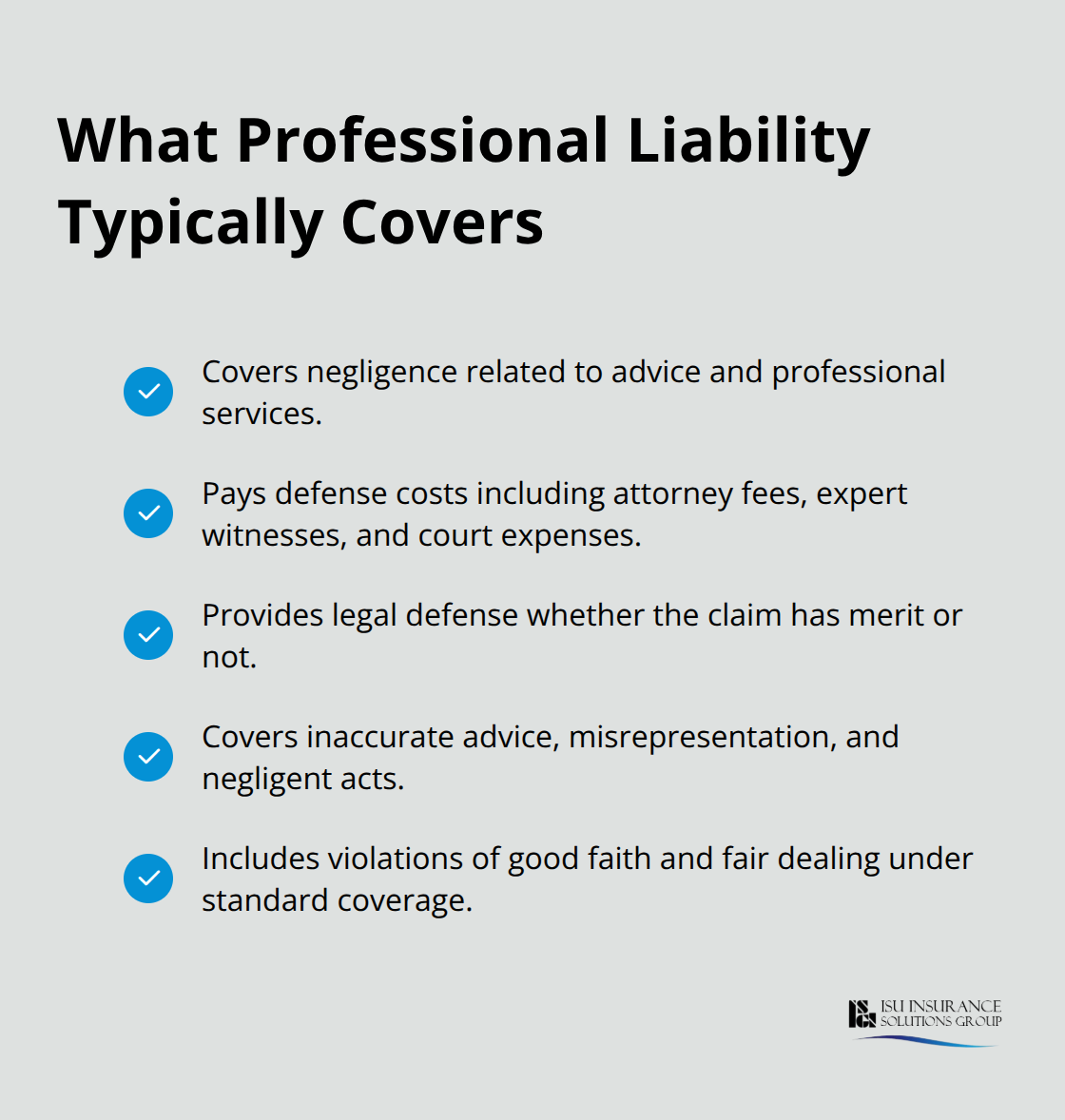

Professional liability covers claims of negligence related to advice and services. Accountants, consultants, and technology professionals regularly face claims for negligence, misrepresentation, or failure to deliver promised results-and this coverage pays what general liability won’t touch. When a client sues claiming your advice cost them money, your design caused project delays, or your implementation created losses, professional liability steps in to cover defense costs and settlements.

Defense costs alone-attorney fees, expert witnesses, court expenses-can exceed $50,000 before any settlement appears. The policy covers these expenses whether the claim has merit or not, meaning you get legal representation even when defending against baseless allegations. Claims for negligent acts, inaccurate advice, misrepresentation, and violations of good faith and fair dealing all fall under standard coverage.

Coverage Requirements in Contracts and Regulations

If a client contract requires this insurance, you must carry it. Operating without mandated coverage exposes you to contract breaches and potential penalties. The Hartford’s pricing reflects the real exposure across industries: architects and engineers pay around $239 monthly because their errors can trigger both professional liability claims and property damage claims requiring dual coverage.

Your policy likely includes a retroactive date, meaning incidents before that date aren’t covered, and an extended reporting period that allows claims filed shortly after cancellation to still be covered if they arose from work during the policy term. Many policies operate on a claims-made basis, meaning coverage triggers when a claim is filed during the active policy period, not when the error occurred. This distinction matters enormously-gaps in coverage leave past work completely unprotected.

What This Coverage Excludes

Professional liability doesn’t cover bodily injuries or property damage-those require general liability insurance. If a client trips on your office stairs, that’s general liability. If your advice causes them financial loss, that’s professional liability. Intentional dishonest acts, criminal conduct, and contractual liability beyond standard professional services typically get excluded from coverage.

The more your business grows and takes on complex projects, the more your coverage limits need to expand. A $250,000 limit that protected you in year one may leave you dangerously exposed by year three. As your operation scales, inadequate limits become your biggest vulnerability-and that’s where the next set of coverage gaps emerges.

Common Gaps in Coverage and How to Avoid Them

Coverage Limits That Actually Match Your Exposure

Most business owners pick coverage limits based on price rather than risk. You’ll see standalone professional liability policies starting around $250,000 in coverage, and many service providers lock into this amount without calculating what they actually need. The Hartford’s data shows architects and engineers pay roughly $239 monthly for coverage, a significant jump from the $73 accountants pay, because design errors create larger financial exposure. That price difference exists for a reason-your coverage limit should reflect the maximum financial loss a single client could face from your mistake, not the minimum amount your budget allows.

If you’re a consultant advising a mid-sized company and your recommendation costs them $500,000 in lost revenue, a $250,000 policy leaves you personally liable for half the damages. Technology professionals averaging $146 monthly typically face higher exposure than graphic designers because software failures impact entire business operations. When you request a quote, ask your agent to calculate coverage limits based on your largest client contracts, not your smallest ones.

Many policies operate on a claims-made basis with defense costs covered outside the policy limits-meaning the full amount of your liability coverage remains available for settlements. This structure protects you from the shrinking limit problem that forces you to either choose higher limits upfront or risk severe underinsurance when claims arrive. Your coverage should account for both defense costs and potential settlements, not just one or the other.

As your business grows and you take on larger contracts, your limits become obsolete almost immediately. A policy written three years ago at $500,000 won’t protect you if your current project engagements involve clients where errors could trigger million-dollar claims.

Industry-Specific Exclusions Create Hidden Vulnerabilities

Your professional liability policy covers negligence and errors in services you explicitly list on the application, but services you didn’t mention often get excluded entirely. If you’re a consultant who started offering bookkeeping services alongside your main consulting work, and you never updated your policy, bookkeeping claims likely won’t be covered. Contractors face exclusions for design services separate from construction, creating dangerous gaps when you provide design recommendations alongside build work.

Healthcare professionals discover that certain treatment modalities or specialized services require separate professional liability riders. The Hartford’s pricing reflects these exclusions-your rate depends partly on exactly which services your policy covers. When you grow your business or add new service lines, you need to notify your carrier immediately. Waiting until you land a major project in a new service area means operating unprotected in that area.

Some carriers simply decline to cover certain services, forcing you to find specialized providers or operate without coverage. Real estate professionals learned this lesson painfully when property management services weren’t covered under their sales-focused policies. Your policy documents spell out covered services clearly, but most business owners never read them thoroughly enough to catch exclusions.

Staying Protected as Your Business Evolves

Request a coverage summary from your agent that explicitly lists what is and isn’t covered, then have them confirm in writing that all your current services appear in that covered list. As you expand into adjacent services, treat this as a quarterly review item to prevent coverage disasters. This simple practice catches service gaps before they become expensive problems.

Final Thoughts

Professional liability for businesses isn’t a luxury add-on or something you handle after a claim arrives. It’s the financial foundation that separates manageable risk from catastrophic loss. When a client sues over negligence, misrepresentation, or errors in your services, your policy covers defense costs and settlements that would otherwise come directly from your business bank account.

Your business generates revenue by providing services or advice that clients depend on, and that dependency creates exposure. The Hartford’s pricing data shows technology professionals pay $146 monthly while accountants pay $73 monthly, reflecting real differences in claim frequency and severity across industries. These aren’t arbitrary numbers-they represent the actual cost of risk in each profession, and your coverage limits should match your actual exposure, not your budget constraints.

Start by reviewing your current contracts to identify which ones mention errors and omissions coverage or professional liability requirements. Check whether your state or industry regulations mandate this insurance, then calculate what a worst-case claim would cost-not the smallest possible error, but the largest financial loss a single client could face from your mistake. Contact ISU Insurance Solutions Group to evaluate your current coverage or get a quote for professional liability insurance tailored to your business.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.