Restaurant Liability Insurance: Guarding Your Kitchen and Guests

A single foodborne illness outbreak or slip-and-fall accident can cost a restaurant tens of thousands of dollars in legal fees and settlements. Restaurant liability insurance protects your business from these financial disasters.

At ISU Insurance Solutions Group, we’ve seen how the right coverage gives restaurant owners peace of mind to focus on what they do best: serving customers. This guide walks you through what you need to know about liability protection for your restaurant.

What Restaurant Liability Insurance Actually Covers

Foodborne Illness and Food Contamination

Foodborne illness claims represent one of the costliest exposures for restaurants. When a customer contracts food poisoning from your establishment, liability insurance covers medical expenses, legal defense costs, and settlements-sometimes reaching six figures. Product liability coverage within general liability protects against claims when contaminated or defective food injures customers. Food contamination endorsements go further by covering health department closure costs, lost income during shutdown, and remediation expenses when authorities shut you down due to a foodborne outbreak.

Slip-and-Fall Accidents

Slip-and-fall accidents happen constantly in restaurants, and they rank among the four most expensive claim types according to 2021–2024 claims data. General liability insurance pays for customer medical bills, legal fees, and court settlements when someone slips on a wet floor or trips on restaurant property. Property damage liability covers situations where a customer or their belongings suffer damage on your premises-broken glasses, damaged phones, or injuries from falling objects.

Third-Party Injuries and Property Damage

Third-party injury claims extend beyond customers to include delivery personnel, vendors, and contractors injured at your location. Water damage, fire, and vandalism rank among the most frequent restaurant insurance claims, and liability coverage addresses injuries or property damage resulting from these events. If a kitchen fire spreads and damages a neighboring business or injures someone, your liability policy covers those third-party losses. Equipment breakdown claims spike in restaurants, and while property insurance covers repair costs, liability coverage addresses injuries occurring during equipment failure.

Additional Liability Exposures

Assault and battery claims from confrontations with staff or customers also fall under liability protection, covering medical expenses and legal defense. Commercial property insurance bundled with liability through a Business Owner’s Policy provides the most efficient protection, combining both exposures into one plan.

Understanding what liability insurance covers helps you identify gaps in your protection. The next section explains why restaurants cannot afford to operate without this coverage and what legal and financial consequences emerge when liability protection falls short.

Why Your Restaurant Needs Liability Coverage

Legal Requirements and Operational Mandates

Most states don’t legally mandate general liability insurance for restaurants, but landlords, lenders, and health departments require proof of coverage before you operate. Lease agreements almost always include insurance requirements, and violating them gives landlords grounds to evict you. If you have a commercial mortgage, your lender won’t fund the loan without evidence of adequate liability protection. Health permits in many jurisdictions now include insurance verification as part of the approval process. These aren’t suggestions-they’re conditions of operation.

The True Cost of Going Uninsured

A single slip-and-fall lawsuit costs between $15,000 and $45,000 on average. Food poisoning claims routinely exceed $100,000 once medical expenses, legal defense, and jury awards combine. The U.S. Bureau of Labor Statistics reports 2.8 million nonfatal workplace injuries and illnesses across private industry in 2022, and restaurants account for a disproportionate share due to high-heat equipment, slippery floors, and repetitive motion.

Without liability coverage, you face personal liability for these costs. Creditors pursue your personal assets, bank accounts, and future earnings. One major incident eliminates years of profit and forces closure.

How Liability Coverage Protects Your Business

Liability coverage transforms this equation entirely. Your insurance carrier handles legal defense, negotiates settlements, and pays claims up to your policy limits-protecting both your business and personal finances from catastrophic loss. This protection (combined with proper risk management) allows you to operate with confidence rather than constant fear of financial ruin.

The financial stakes explain why compliance matters so much. Restaurant owners who understand their exposure typically move quickly to secure appropriate coverage. The next section walks you through how to evaluate your specific risks and select the right liability limits for your operation.

Selecting the Right Liability Limits for Your Restaurant

Match Coverage Limits to Your Restaurant’s Scale

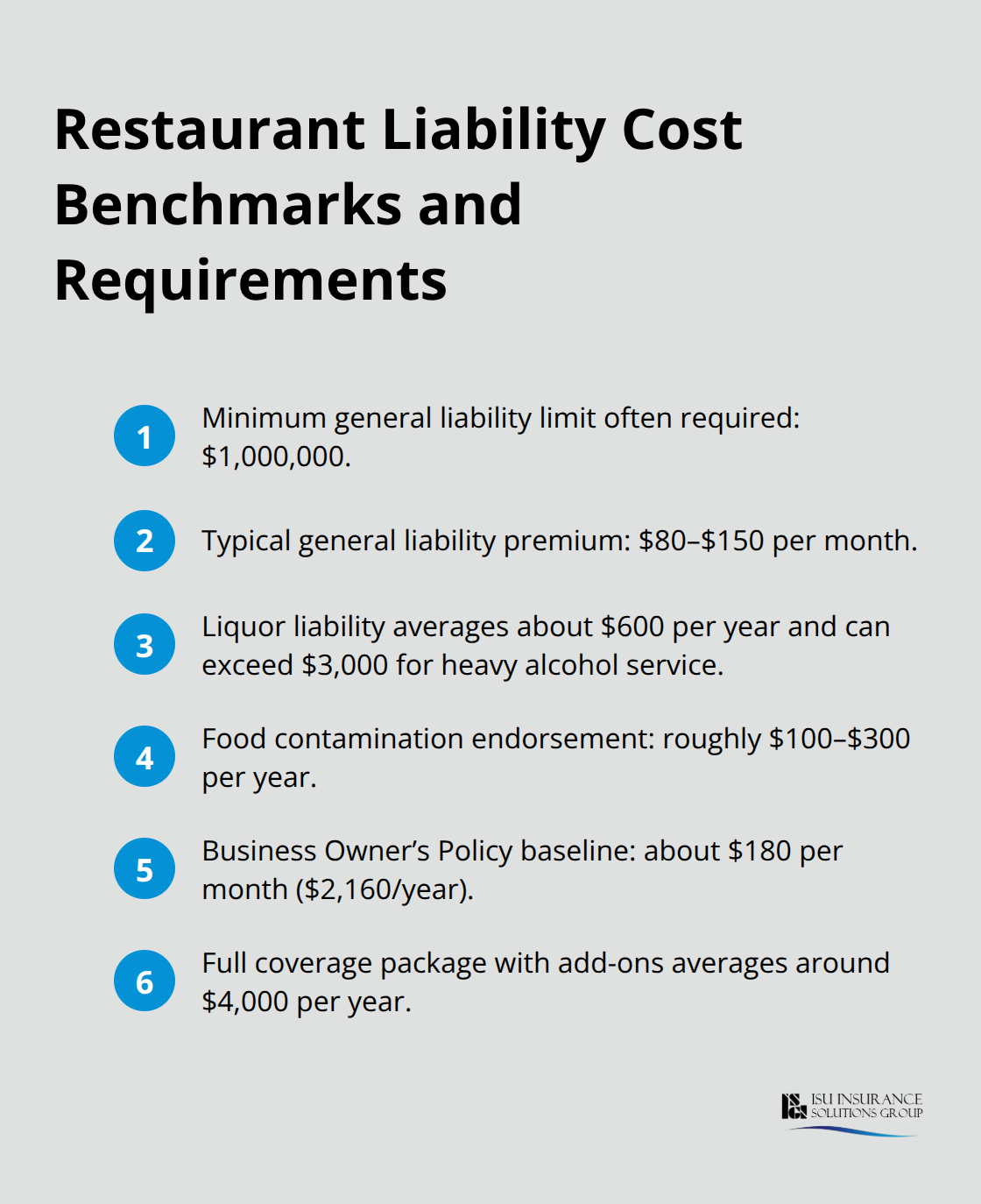

Restaurant size and revenue directly determine your liability exposure and necessary coverage limits. A small café with $300,000 in annual revenue faces different risks than a fine-dining establishment generating $2 million yearly. General liability insurance for restaurants depends on factors such as the coverage limits and deductible you choose and the size of your business. Most landlords and lenders require minimum limits of $1 million in general liability coverage, which typically costs between $80 and $150 monthly for basic coverage.

If you serve alcohol, liquor liability insurance becomes mandatory-this coverage averages $600 annually but can exceed $3,000 for venues with extensive alcohol service, since intoxicated patron claims drive significantly higher settlements. Food contamination endorsements add roughly $100 to $300 annually but protect against six-figure closure costs when health authorities shut you down.

Account for Your Restaurant Type and Asset Value

The 2021–2024 NEXT insurance data shows that fine-dining establishments suffer nearly double the average loss compared to casual restaurants, meaning a steakhouse with open flames and high equipment value needs substantially higher limits than a pizza shop. Calculate your total asset value-building, kitchen equipment, furniture, and inventory-then add your annual revenue to determine appropriate property and business interruption limits.

A Business Owner’s Policy bundling general liability and commercial property typically costs $180 monthly ($2,160 annually) as a baseline, with total restaurant coverage packages including workers’ compensation and liquor liability running around $4,000 per year on average.

Test Different Deductibles and Limits Through Quotes

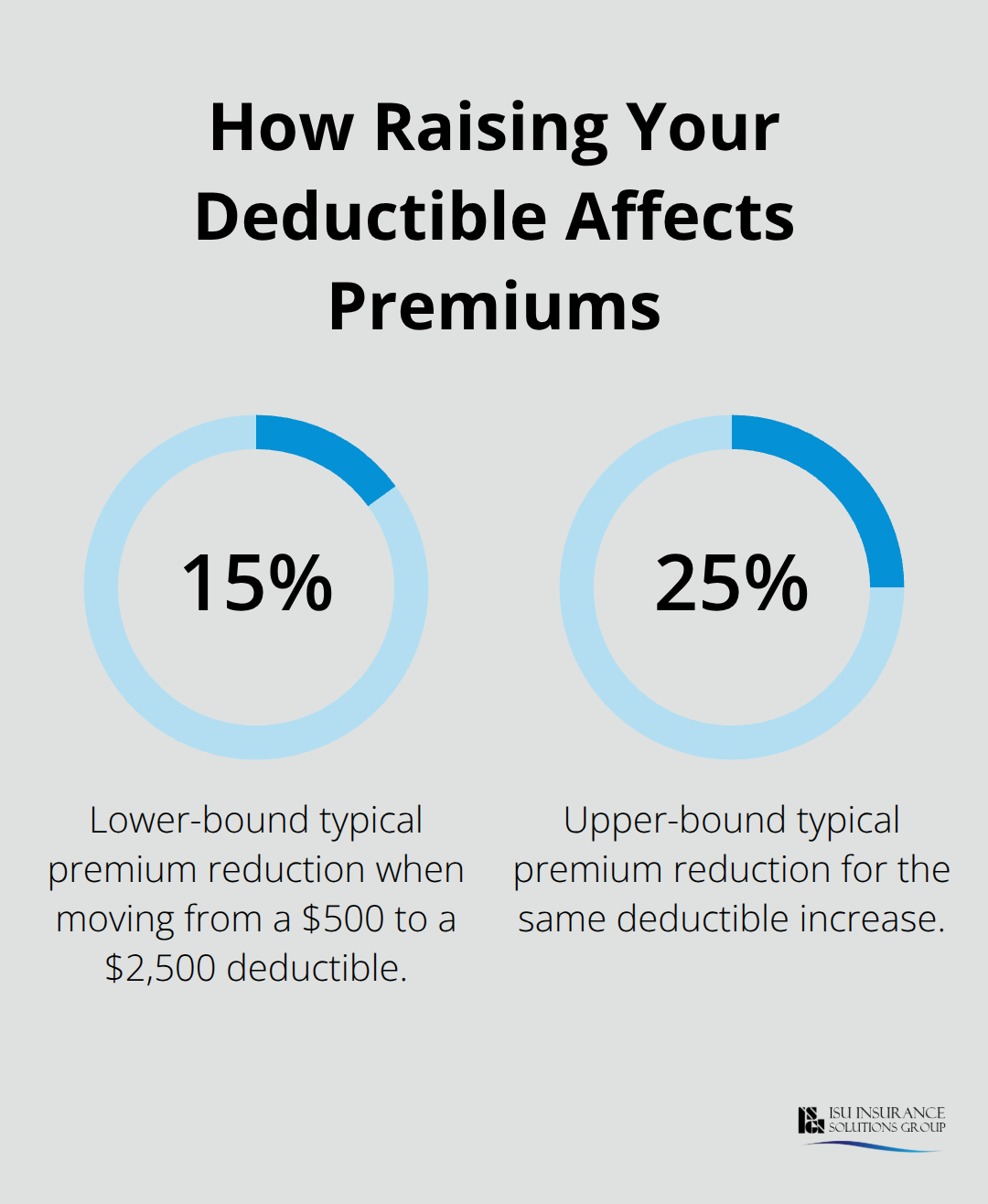

Comparing actual quotes from multiple carriers reveals dramatic price differences for identical coverage. Online quote tools deliver estimates within 10 minutes, allowing you to test different deductibles and limits without commitment. Raising your deductible from $500 to $2,500 typically reduces your premium by 15–25%, but only if you maintain emergency reserves to cover that higher out-of-pocket cost when claims occur.

Policy limits matter far more than monthly premiums-choosing $500,000 in coverage to save $20 monthly exposes you to catastrophic personal liability if a major incident occurs.

Factor in Regional and Location-Specific Risks

Regional claim patterns shape your coverage decisions: equipment breakdown claims spike in Pennsylvania, water damage peaks December through February across most regions, and wind damage dominates in Mississippi. If your restaurant operates in a flood-prone area or high-crime neighborhood, standard policies contain exclusions that require additional endorsements or separate policies to address those specific risks.

As an independent agency serving Washington and Oregon since 1983, ISU Insurance Solutions Group works with 20+ carriers to deliver multi-carrier quotes that identify the best value for your specific restaurant type and location, avoiding the trap of choosing coverage based solely on price rather than actual protection adequacy.

Final Thoughts

Restaurant liability insurance protects your business from financial collapse after slip-and-fall claims ($15,000–$45,000), foodborne illness cases (exceeding $100,000), and third-party injuries that would otherwise drain your personal assets. Landlords, lenders, and health departments all require proof of coverage before you operate, making this protection non-negotiable for compliance and peace of mind. Without it, a single incident eliminates years of profit and forces closure.

Your next step is obtaining quotes from multiple carriers to understand what appropriate coverage costs for your specific restaurant. Online tools deliver estimates within 10 minutes, and comparing quotes reveals dramatic price differences for identical protection-test different deductibles and limits to find the balance between affordable premiums and adequate coverage. Account for your restaurant type, asset value, annual revenue, and whether you serve alcohol, since each factor shapes your actual exposure and necessary limits.

We at ISU Insurance Solutions Group have guided Washington and Oregon restaurants through this process since 1983, partnering with 20+ carriers to deliver multi-carrier quotes that identify genuine value rather than just the cheapest option. Contact us for a personalized quote that matches your restaurant’s specific needs and protects both your business and personal finances.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.