Security Guard Bonds: Why They Matter for Local Businesses

A dishonest employee can cost your business thousands of dollars in a single incident. Security guard bonds protect you from these financial losses and give you legal coverage when things go wrong.

At ISU Insurance Solutions Group, we’ve seen too many local business owners skip this protection because they don’t understand what it covers. This guide breaks down why security guard bonds matter and how they work for your business.

What Security Guard Bonds Actually Cover

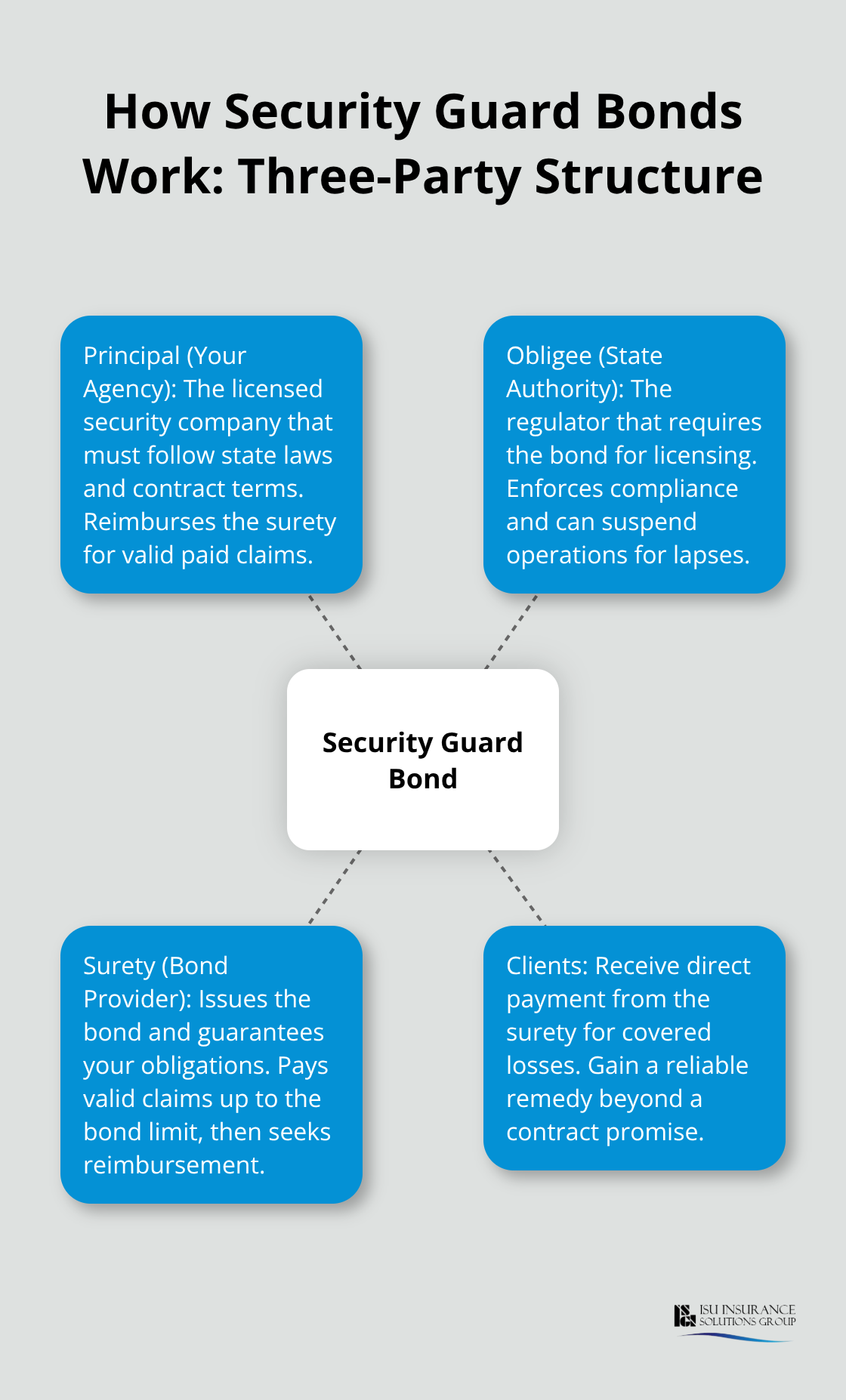

The Three-Party Structure

A security guard bond involves three parties: your security agency (the principal), the state licensing authority (the obligee), and the surety company (the bond provider). The surety guarantees that your agency will comply with state laws and fulfill its obligations to clients. If your business violates licensing requirements or an employee acts dishonestly, the surety pays valid claims up to the bond limit, and your agency reimburses that amount.

State Requirements in Washington and Oregon

Washington and Oregon both require security guard agencies to post bonds as a condition of licensing, though the specific amounts differ by state and whether guards are armed or unarmed. Oregon mandates bonding through its Department of Public Safety Standards and Training. For local businesses in Washington and Oregon, this distinction matters because licensing authorities actively monitor compliance, and a lapsed or inadequate bond can suspend your operating license immediately.

What the Bond Actually Protects

The real protection comes from what happens when something goes wrong. If a guard steals from a client, assaults someone, or violates licensing rules, the harmed party files a claim against your bond. The surety pays the claim directly, protecting the victim and your business from the full financial hit. You then repay the surety the claim amount. This structure holds your agency accountable while giving clients a concrete remedy if misconduct occurs.

Cost and Credit Impact

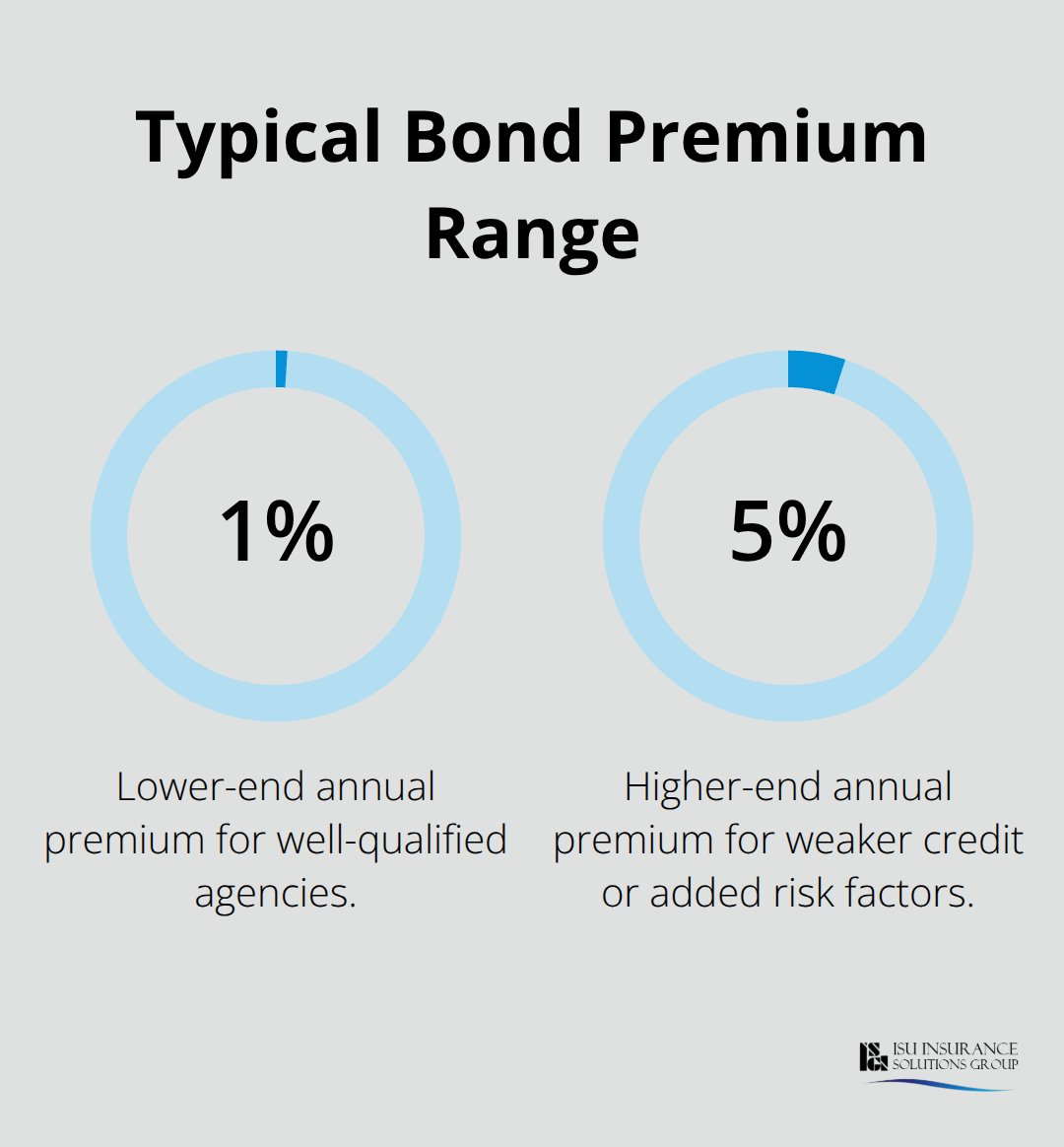

The cost is modest for most operations-premiums typically run 1 to 5 percent of the bond amount annually, so a $10,000 bond might cost $100 to $500 per year depending on your credit and business financials. Stronger personal and business credit scores lower your premium significantly. Many agencies obtain bonds online in minutes with instant email delivery of documents, so administrative burden stays minimal.

Bonds Versus Insurance

Unlike insurance, which covers accidents and unforeseen events, bonds guarantee compliance with specific legal and contractual obligations. This distinction shapes how you approach risk management and regulatory responsibility. Understanding this difference helps you recognize that bonds serve a fundamentally different purpose than traditional business insurance, which means you may need both to fully protect your operation.

How Bonds Actually Protect Your Bottom Line

Direct Payment When Theft Strikes

A security guard bond transforms a potential financial disaster into a manageable claim. When an employee steals cash, equipment, or client data, the victim files a claim against your bond. The surety pays the claim directly up to the bond limit, which means your business avoids the full financial hit. You then reimburse the surety, but the structure protects you in the immediate moment when cash flow matters most. This direct payment mechanism is why bonds exist-they create accountability that goes beyond a written contract or a promise. Without a bond, you remain personally liable for every dollar, and collecting from an employee who committed theft is often impossible. With a bond, the surety absorbs the claim and handles recovery, freeing you to focus on running your operation instead of pursuing legal action.

Compliance Guarantees That Shield You from Lawsuits

The second protection is equally practical: your bond guarantees compliance with state licensing laws when your guards cause harm. If a guard uses excessive force during an arrest or fails to prevent a security breach that results in injury or property damage, clients sue your agency. When a claim shows that you violated licensing requirements-such as failing to properly train a guard or operating without adequate supervision-the bond covers it. This matters because licensing violations are common triggers in security lawsuits. Clients in Washington and Oregon specifically expect bonded agencies because state licensing authorities require it; operating without a valid bond is grounds for immediate suspension.

Why Claims Specialists Beat Legal Fees

For small operations, this compliance guarantee is worth far more than the 1 to 5 percent annual premium you pay. Local business owners who face a claim find that having a bond in place means the surety’s claims specialists handle the dispute rather than forcing the owner to hire an attorney and negotiate directly. That cost difference alone-paying $200 to $500 annually for a bond versus spending $5,000 to $15,000 on legal fees-makes the decision obvious for any serious operator. The surety absorbs not just the financial claim but also the administrative burden of resolution, which protects your time and your reputation during a crisis.

The Competitive Edge Bonds Provide

Agencies that maintain bonds signal to clients that they take accountability seriously. Clients know that if something goes wrong, they have a direct financial remedy backed by a surety company, not just a promise from a small business owner. This confidence translates into contract wins and client retention, especially for larger accounts that require bonded providers as a condition of engagement. The bond becomes part of your marketing advantage in a competitive market where trust determines who gets hired.

Common Misconceptions About Security Guard Bonds

The Real Cost of Bond Protection

Small business owners reject bonds before they even investigate the actual price. A $10,000 bond for a local security agency costs between $100 and $500 per year, depending on your credit score and business financials. That amounts to less than $50 per month for most operations. A single theft claim-guards stealing client cash, equipment, or data-costs businesses $5,000 to $25,000 per incident. The math is straightforward: your annual bond premium protects against losses that dwarf the cost many times over.

Your credit score matters more than your company size. Strong personal and business credit qualifies you for the lower end of the premium range. Weaker credit results in higher rates, but the cost remains manageable for any operation serious about compliance. Many agencies pay their annual bond premium in one invoice and move forward; the administrative burden stays minimal because bonding happens online with instant document delivery.

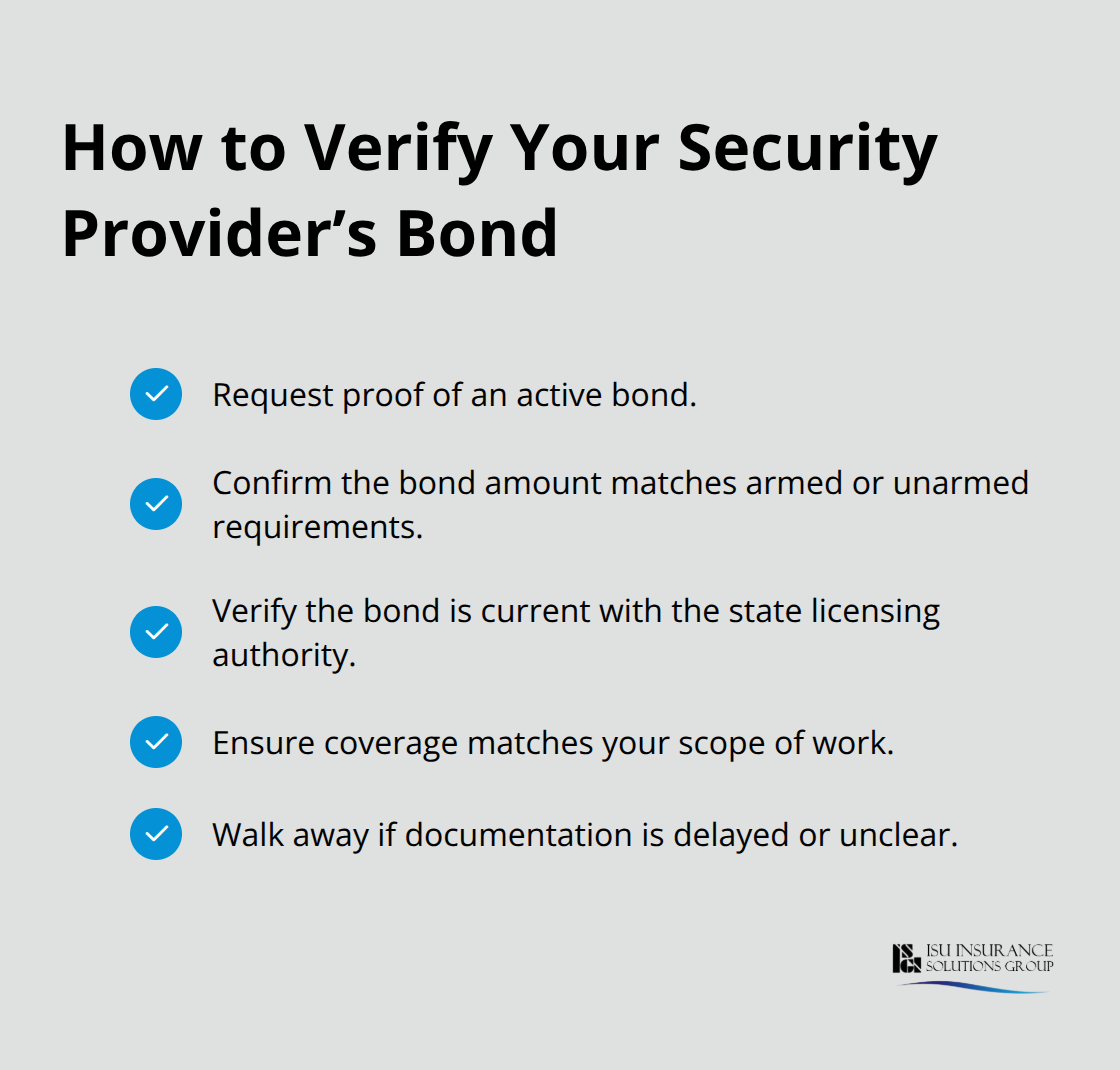

Assuming Your Security Provider Carries Bond Coverage

The second misconception proves far more dangerous: business owners assume that hiring a security guard company automatically provides bond protection. This assumption is false. Some security service providers operate without bonds or with inadequate bond amounts, exposing their clients to unprotected liability. Washington and Oregon licensing authorities require bonds, but compliance varies across providers.

You must verify that your security provider maintains an active bond in the correct amount for armed or unarmed guards. Ask for proof of bonding before signing a contract. A provider who hesitates to show documentation should raise immediate red flags. The bond protects you only when it actually exists and covers the right scope of work.

Why Bonds Matter Across All Business Types

The third misconception-that bonds only matter for high-risk industries-misses the practical reality. Bonds matter wherever employees handle cash, keys, or access to client property. A security guard working at a retail store, office building, or warehouse has direct access to valuable assets. One dishonest employee costs your business tens of thousands of dollars. The bond isn’t about industry classification; it’s about protecting yourself against employee dishonesty, which happens across all sectors.

If you operate a security guard agency in Washington or Oregon, licensing authorities mandate bonding regardless of whether you consider your work high-risk. If you hire security guards, you should demand bonded providers because state regulators require it for solid reasons. The protection is practical, affordable, and legally necessary for any operation handling client assets or property.

Final Thoughts

Security guard bonds protect your operation from financial disaster and satisfy state licensing requirements in Washington and Oregon. A single incident involving employee theft or misconduct costs $5,000 to $25,000 or more, but your bond covers that loss immediately and protects your cash flow when you need it most. Beyond the financial shield, bonds signal to clients that you operate with accountability and comply with state regulations, which translates into contract wins and client retention for larger accounts.

Determine your specific bonding needs by identifying whether your guards are armed or unarmed, as this affects bond amounts and premium costs. If you hire security services, verify that your provider maintains an active bond in the correct amount before signing any contract and ask for proof of bonding to confirm the coverage matches your scope of work. The cost remains minimal-typically $100 to $500 annually-compared to the protection you gain from security guard bonds.

We at ISU Insurance Solutions Group work with multiple carriers to find competitive rates tailored to your operation and understand Pacific Northwest licensing requirements specific to your state. Contact us to discuss your bonding needs and receive a quote that fits your budget.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.