Oregon Commercial Auto Insurance: Rates, Coverage, and Options

Oregon commercial auto insurance isn’t one-size-fits-all. Your business faces unique risks, and your coverage should reflect that.

We at ISU Insurance Solutions Group help Oregon business owners navigate rates, coverage options, and policy selection. This guide walks you through what affects your premiums, which protections matter most, and how to find competitive quotes that fit your operation.

What Drives Your Oregon Commercial Auto Premium

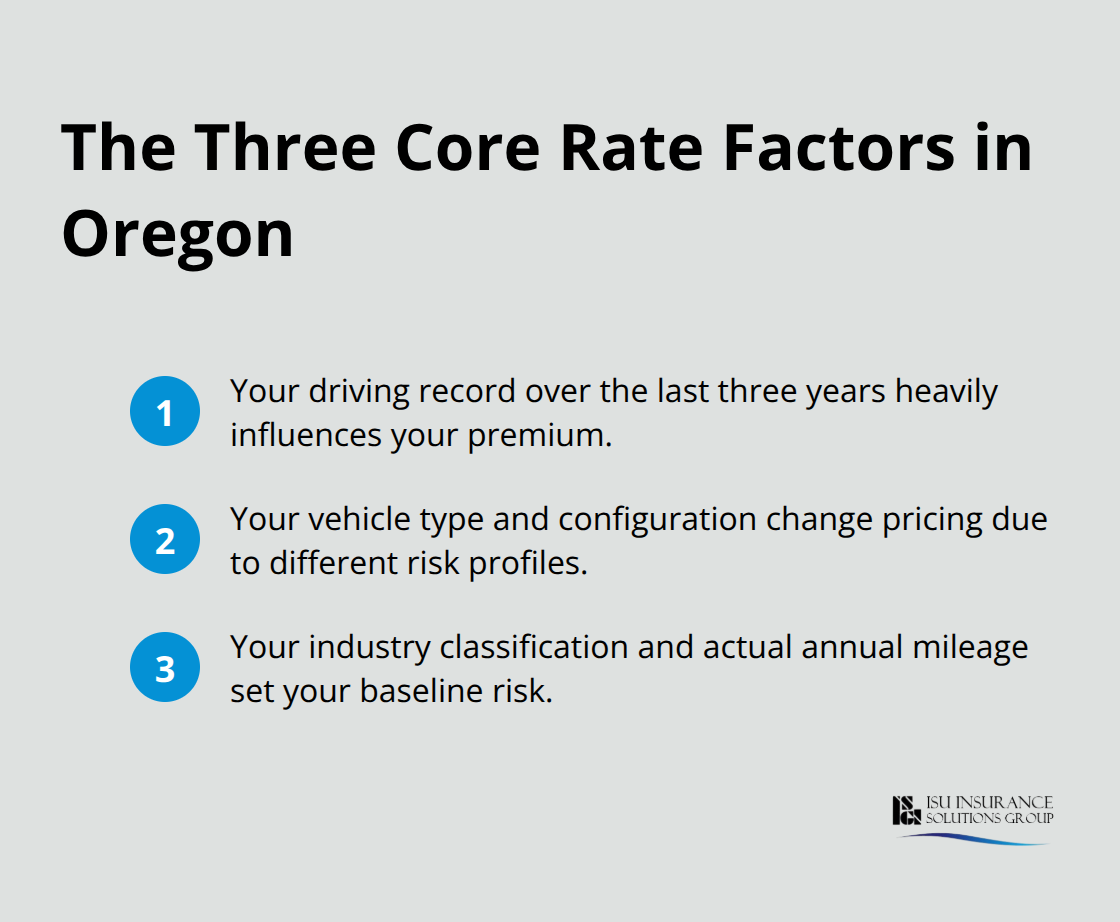

The Three Core Rate Factors

Your premium isn’t arbitrary. Oregon insurers examine three core factors that directly determine what you pay each month. Your driving record over the past three years carries real weight-a single at-fault accident or moving violation can push rates up 15–25%, while a clean history qualifies you for preferred pricing. Traffic violations hit harder than most business owners expect; a reckless driving citation can add $50–$100 monthly to your policy. Maintain zero incidents for three consecutive years and you’ll position yourself for renewal discounts that compound over time.

Vehicle type matters enormously. A light cargo van typically costs $225–$275 per month with full coverage in Oregon, but switching to a dual rear-wheel pickup truck can add $40–$50 monthly because insurers view them as higher-risk for towing-related claims. Semis and utility trailers trigger FMCSA requirements that demand additional liability coverage, pushing premiums substantially higher.

Your industry classification and actual annual mileage determine baseline risk assessment. Construction contractors face rates between $325–$425 per vehicle monthly for general work, while higher-risk trades like structural work or excavation run $450–$600 or more. A contractor who operates within a 50-mile local radius saves roughly 10–15% compared to one covering a 200-mile territory, so verify your actual routes when quoting-insurers penalize overstated service areas.

New Business Surcharges and Geographic Pressures

New ventures face a 20–35% surcharge in their first three years, which gradually fades after maintaining a clean loss history. This front-loaded cost reflects insurer caution around unproven track records. Beyond these three anchors, Oregon’s specific geography adds pressure. Portland’s elevated theft rates for catalytic converters and tools push comprehensive coverage costs higher than rural areas like Bend.

Nationwide, commercial auto premiums rose 7–15% in 2026 due to social inflation (rising litigation costs) and vehicle repair expenses, including calibration of modern camera and sensor systems. Oregon tracks this national trend closely.

Strategies to Lower Your Costs

If you operate seasonally-say, a snow plow service-switch idle vehicles to comprehensive-only coverage during off-months and cut costs by 20–30%. Telematics enrollment proves worth pursuing aggressively; usage-based programs can reduce premiums by up to 30% for safe driving behavior. Install GPS trackers or AI dashcams to demonstrate risk reduction to insurers and directly lower your annual cost.

Bundle commercial auto with general liability or workers’ compensation to typically yield 5–15% total discounts and simplify claims handling across multiple policies. Mini-fleet pricing applies at just 2–3 vehicles, offering roughly 10–15% volume discounts. Hidden fees often surprise business owners-broker fees run 5–10%, installment charges add another 5–10%, and per-endorsement fees range from $25–$100 each. Request an itemized quote breakdown upfront to avoid surprises at renewal.

With these rate drivers in mind, the next step involves understanding which coverage types actually protect your operation and which ones your Oregon business truly needs.

What Coverage Actually Protects Your Oregon Business

Oregon’s Mandatory Minimums vs. Real-World Exposure

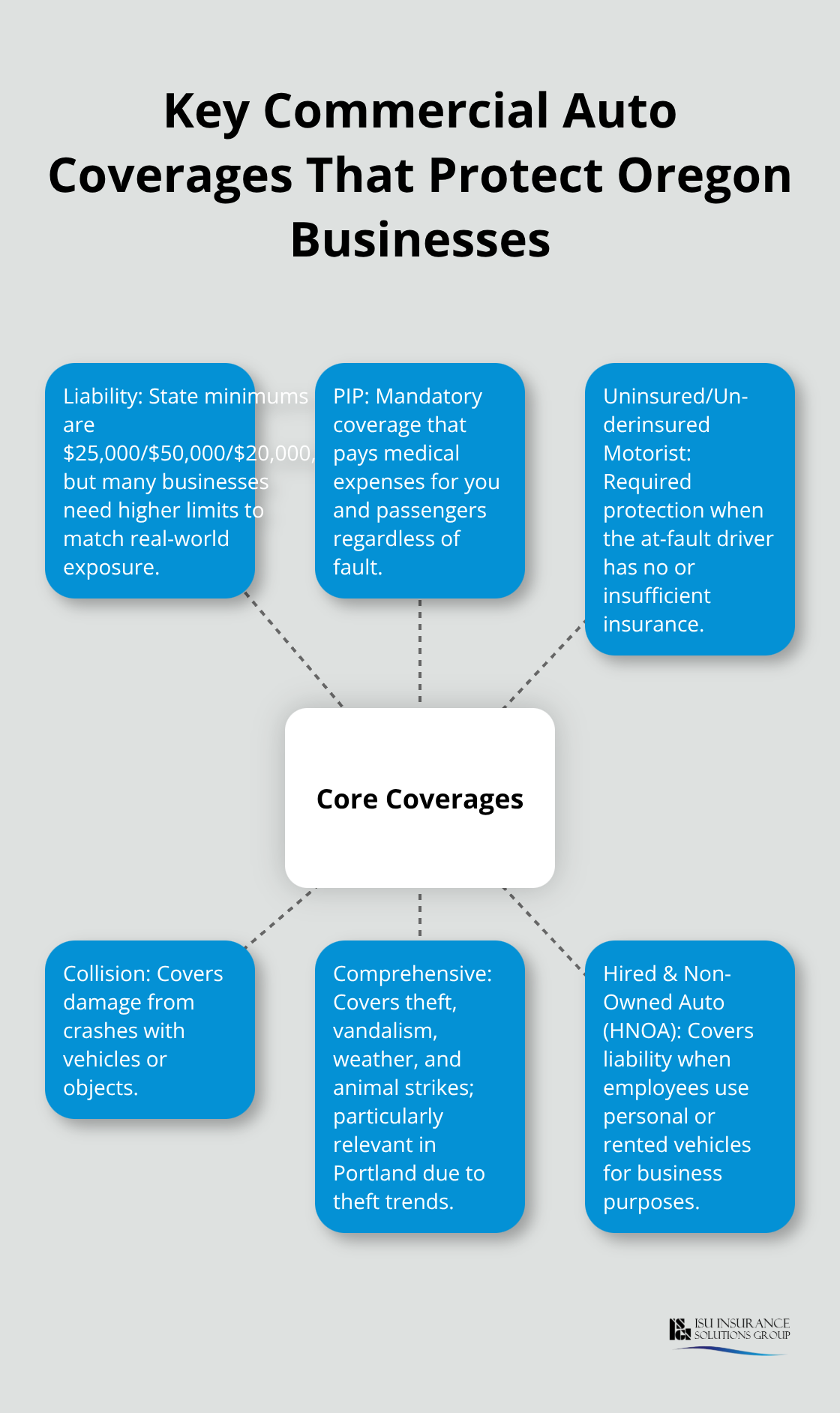

Oregon law mandates minimum liability limits of $25,000 per person and $50,000 per accident for bodily injury, plus $20,000 for property damage. Most Oregon businesses should ignore these minimums entirely. A single serious accident involving an employee driving a company vehicle generates medical bills, lost wages, and legal fees that far exceed state minimums. Construction contractors regularly face claims exceeding $100,000, so carrying $100,000 per person and $300,000 per accident protects your actual exposure rather than leaving your business vulnerable.

Personal injury protection (PIP) coverage is mandatory and covers medical expenses for you and passengers regardless of fault. This protection matters more than it initially appears when an employee injury claim lands on your desk. Uninsured and underinsured motorist coverage is also required, protecting your team when another driver lacks adequate insurance. Roughly one in eight Oregon drivers operates uninsured, meaning your employees face real risk on the road.

Physical Damage and Specialized Protections

Physical damage coverage splits into collision and comprehensive. Collision covers accidents with other vehicles or objects; comprehensive handles theft, vandalism, weather, and animal strikes. In Portland and surrounding urban areas, comprehensive claims spike due to catalytic converter theft and tool theft from vehicles, so this coverage isn’t optional if you park overnight in the metro area. Try a $500 deductible rather than $1,000 if your vehicles sit exposed; the monthly premium difference is typically $15–$25 but saves substantial out-of-pocket costs when claims occur.

Towing and labor coverage costs roughly $10–$20 monthly and covers roadside assistance after breakdowns or accidents. For contractors carrying tools or materials, this endorsement prevents a disabled vehicle from becoming an expensive towing bill. Loading and unloading coverage protects against liability when cargo is being loaded or unloaded from your vehicle. For seasonal operations like snow plowing, switching to comprehensive-only during off-months cuts costs while maintaining theft and weather protection.

Closing Coverage Gaps That Personal Policies Miss

Hidden coverage gaps create real problems. If your team occasionally uses personal vehicles for work tasks, hired and non-owned auto (HNOA) coverage fills the gap that personal auto policies deliberately exclude. HNOA covers accidents involving employee-owned or rented vehicles used for business purposes but does not cover damage to business-owned vehicles, so this is supplemental protection, not a replacement.

Medical payments coverage, separate from PIP, reimburses medical expenses for employees and passengers regardless of fault and typically costs $5–$10 monthly for meaningful limits. Bobtail coverage applies if your business operates tractors without trailers during non-work hours, ensuring coverage during periods when standard commercial policies may not apply.

Getting Quotes That Actually Compare

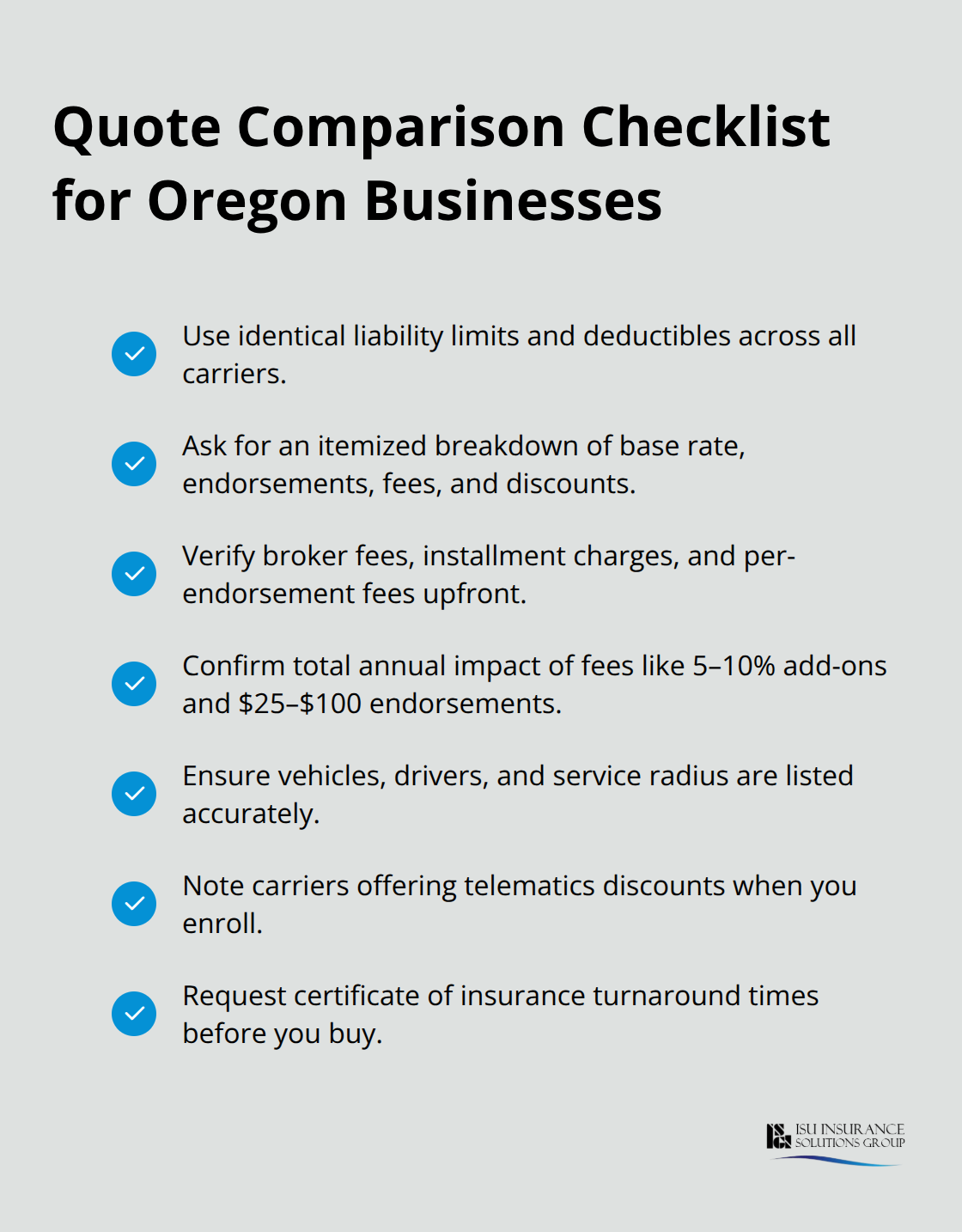

When evaluating quotes from multiple carriers, request identical coverage limits and deductibles across all quotes so actual rate differences become visible rather than buried in coverage variations. Oregon-based businesses often benefit from working with local agents who understand regional risks like Portland’s theft patterns and can recommend appropriate coverage without overselling unnecessary add-ons. These agents help you navigate the next critical step: comparing multiple quotes and selecting the policy that truly fits your operation’s needs and budget.

Comparing Quotes and Finding the Right Policy

Pull Multiple Quotes in One Conversation

Requesting quotes from multiple carriers is non-negotiable if you want competitive rates, but most Oregon business owners approach this backward. Don’t call five different insurers separately and spend three hours repeating your business details each time. Instead, contact one independent agent who represents 10+ carriers and can pull quotes from all of them in a single conversation. An agent working with multiple insurers like Progressive, State Farm, or regional carriers shows you rate differences immediately without forcing you to wait for callbacks.

When you request quotes, specify identical coverage limits across all carriers-use $100,000 per person and $300,000 per accident for liability if you’re a contractor, or $50,000 per person and $100,000 per accident if you run a smaller service business. This consistency lets you see which insurer actually offers the lowest premium rather than hiding price differences under different coverage tiers. Request an itemized breakdown showing base rate, endorsements, fees, and discounts applied. Broker fees (5–10%), installment charges (5–10%), and per-endorsement fees ($25–$100 each) often add $200–$400 annually, so catching these upfront prevents sticker shock at renewal.

Match Your Industry to the Right Carrier

Your industry and vehicle type dramatically shift which carrier offers the best rate. Construction contractors typically find better pricing from carriers that specialize in trades, while service-based businesses like cleaning or landscaping may get lower quotes from standard commercial auto carriers. A contractor operating a dual rear-wheel truck with a trailer will pay roughly $40–$50 more monthly than someone with a light cargo van, so some carriers price this spread more aggressively than others.

Local agents in Oregon understand these nuances and know which carriers price favorably for your specific operation rather than quoting you a one-size-fits-all rate. An experienced agent asks about your actual service radius, vehicle condition, safety equipment, and loss history, then matches you with carriers most likely to offer competitive pricing for your exact risk profile. Telematics enrollment matters during the quoting process-mention if you’re willing to install GPS tracking or dashcam technology, since some carriers offer 15–30% discounts for enrollment, making their higher base rate irrelevant.

Timing and Claims Service Matter

Request quotes in early spring or fall before renewal deadlines arrive, since carriers fill their books strategically and may offer better rates during slower periods. Once you have three to five competing quotes in hand, evaluate not just the monthly premium but also the carrier’s claims process, local repair networks, and how quickly they issue certificates of insurance. Some Oregon carriers issue certificates within 24 hours after purchase, while others take five business days-a factor that matters if you need coverage activated immediately for a new contract or client requirement.

Final Thoughts

Oregon commercial auto insurance protects your business from liability exposure that personal policies deliberately exclude. The three core rate factors-your driving record, vehicle type, and industry classification-determine what you pay monthly, but telematics enrollment cuts premiums by up to 30%, bundling policies yields 5–15% discounts, and mini-fleet pricing applies at just 2–3 vehicles. New business surcharges fade after three years of clean loss history, so your first renewal brings meaningful savings if you maintain a strong claims record.

Coverage requirements matter more than Oregon’s legal minimums suggest. State law mandates $25,000 per person and $50,000 per accident for bodily injury, but construction contractors and service businesses regularly face claims exceeding $100,000. Carrying $100,000 per person and $300,000 per accident reflects actual exposure rather than leaving your operation vulnerable, and physical damage coverage plus uninsured motorist protection close gaps that personal policies miss entirely.

We at ISU Insurance Solutions Group serve Oregon businesses with one-call multi-carrier quotes and hands-on local agents who understand Pacific Northwest risks. Contact an independent agent today to compare rates from 20+ carriers and find Oregon commercial auto insurance coverage that actually protects your operation without overpaying for unnecessary add-ons.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.