Washington Professional Liability Insurance: Local Risk Profiles

Professional liability claims are rising across Washington, with service professionals facing exposure they often underestimate. A single lawsuit can drain your business finances and reputation in ways general liability won’t cover.

We at ISU Insurance Solutions Group know that Washington professional liability insurance isn’t one-size-fits-all. Your coverage needs depend on your specific industry, client base, and local market conditions.

What Claims Actually Happen to Washington Professionals

Real Claims That Damage Real Practices

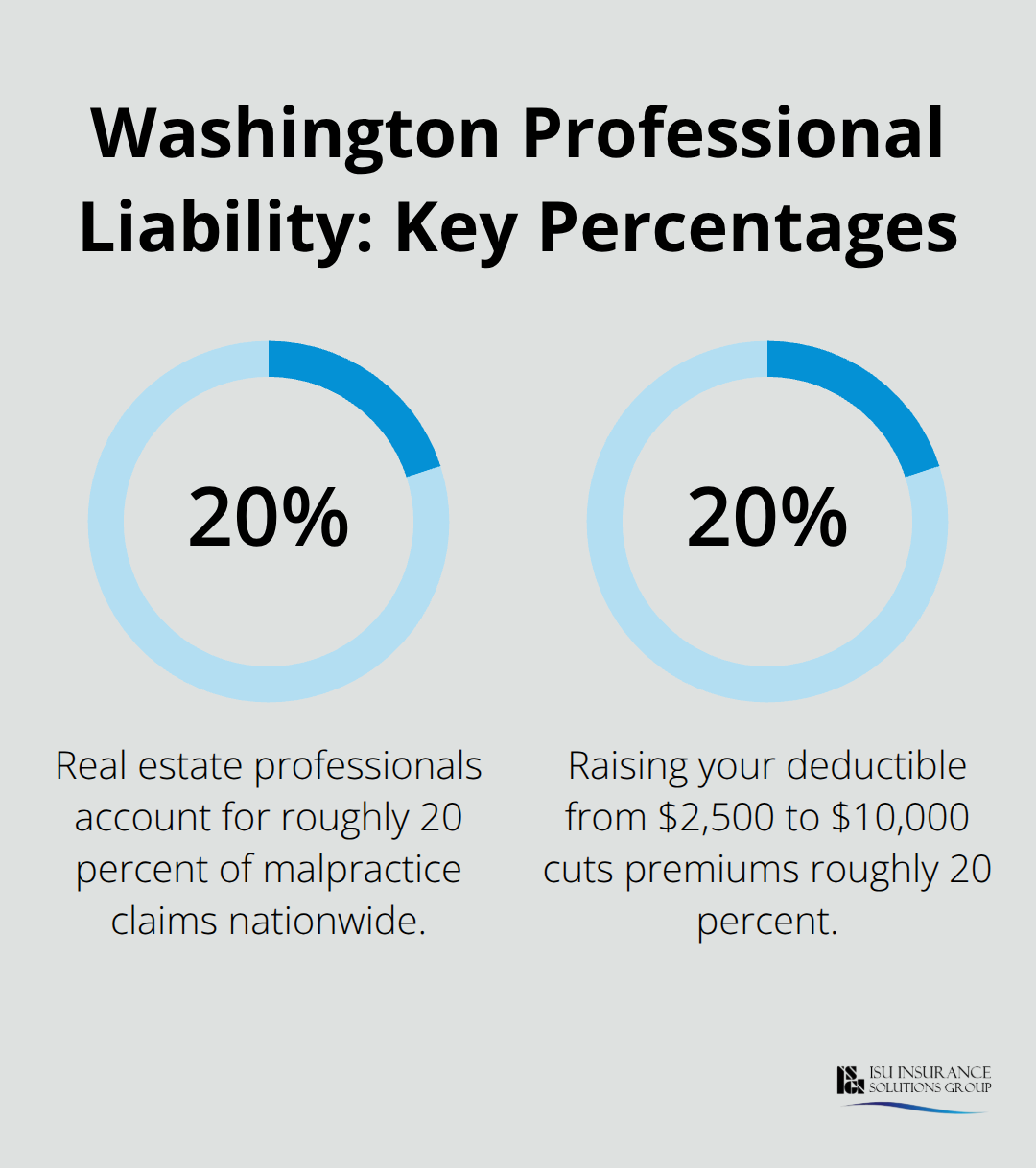

Healthcare providers, architects, consultants, and attorneys across Washington face concrete liability risks that go far beyond general business disputes. In 2021, healthcare providers in Washington reported 318 new malpractice claims with a median indemnity around $340,000, according to the Washington Office of the Insurance Commissioner. Real estate professionals account for roughly 20 percent of malpractice claims nationwide per the American Bar Association, with errors in title work, disclosure failures, and transaction mistakes creating expensive litigation. Technology and consulting firms encounter failure-to-perform claims regularly-a 2022 Spokane SaaS settlement totaled $425,000 plus $150,000 in defense costs, demonstrating that even software and service work carries substantial financial exposure. Attorneys defending professional liability claims in Washington absorb average defense costs around $87,338 before any settlement or judgment, which means a claim can financially damage your practice before liability is even determined.

How Washington’s Legal System Amplifies Exposure

Washington’s comparative negligence rules and consumer-friendly statutes like the Washington Consumer Protection Act allow courts to treble damages in certain cases, directly increasing settlement values and jury awards. This legal framework means settlements and verdicts in Washington tend to be higher than in states with stricter liability defenses. The state also has over 650,000 small businesses and about 1.4 million employees exposed to liability risk, creating a large, competitive professional marketplace where clients are quick to sue over perceived mistakes.

Coverage Requirements That Block Your Work

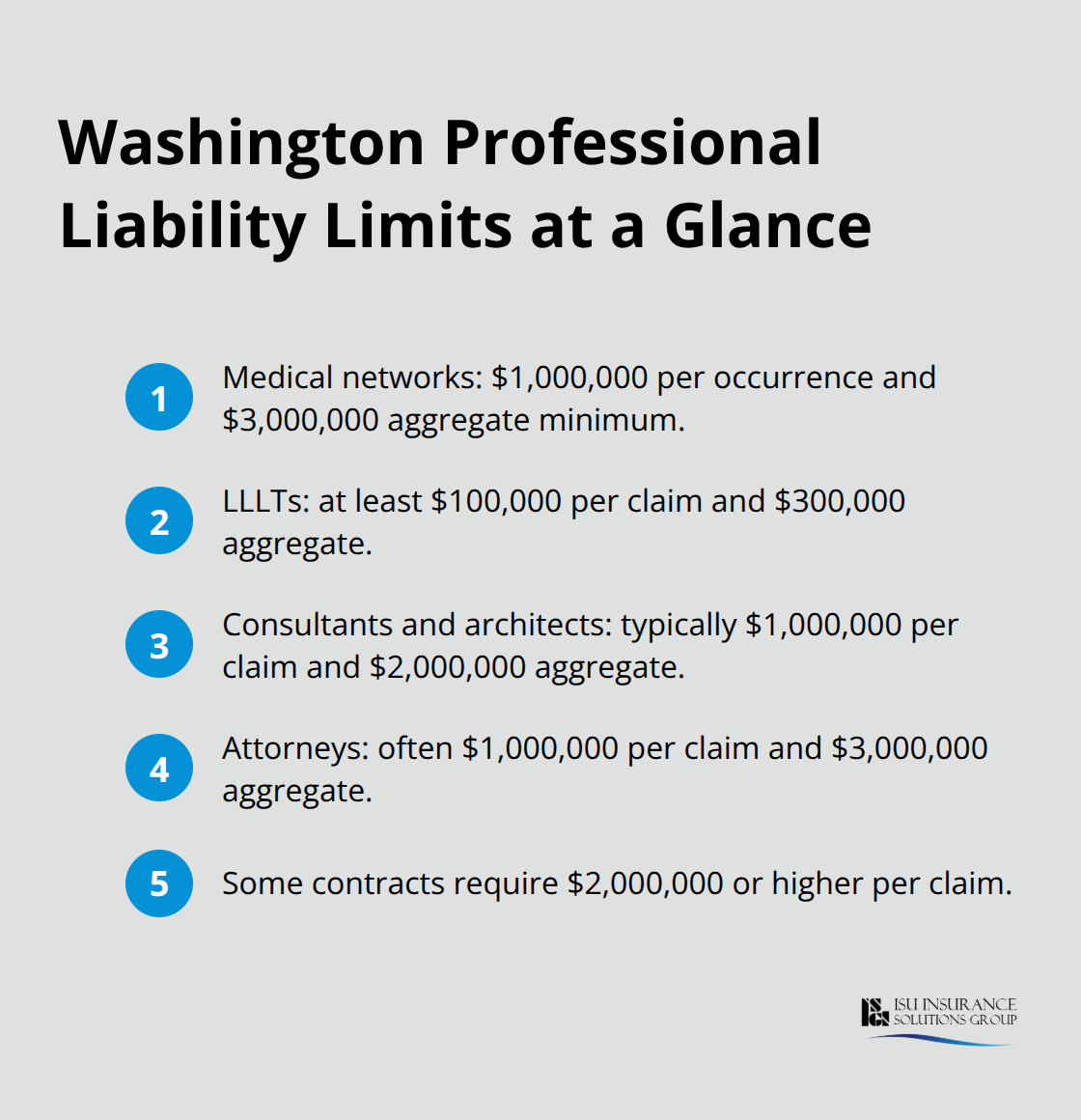

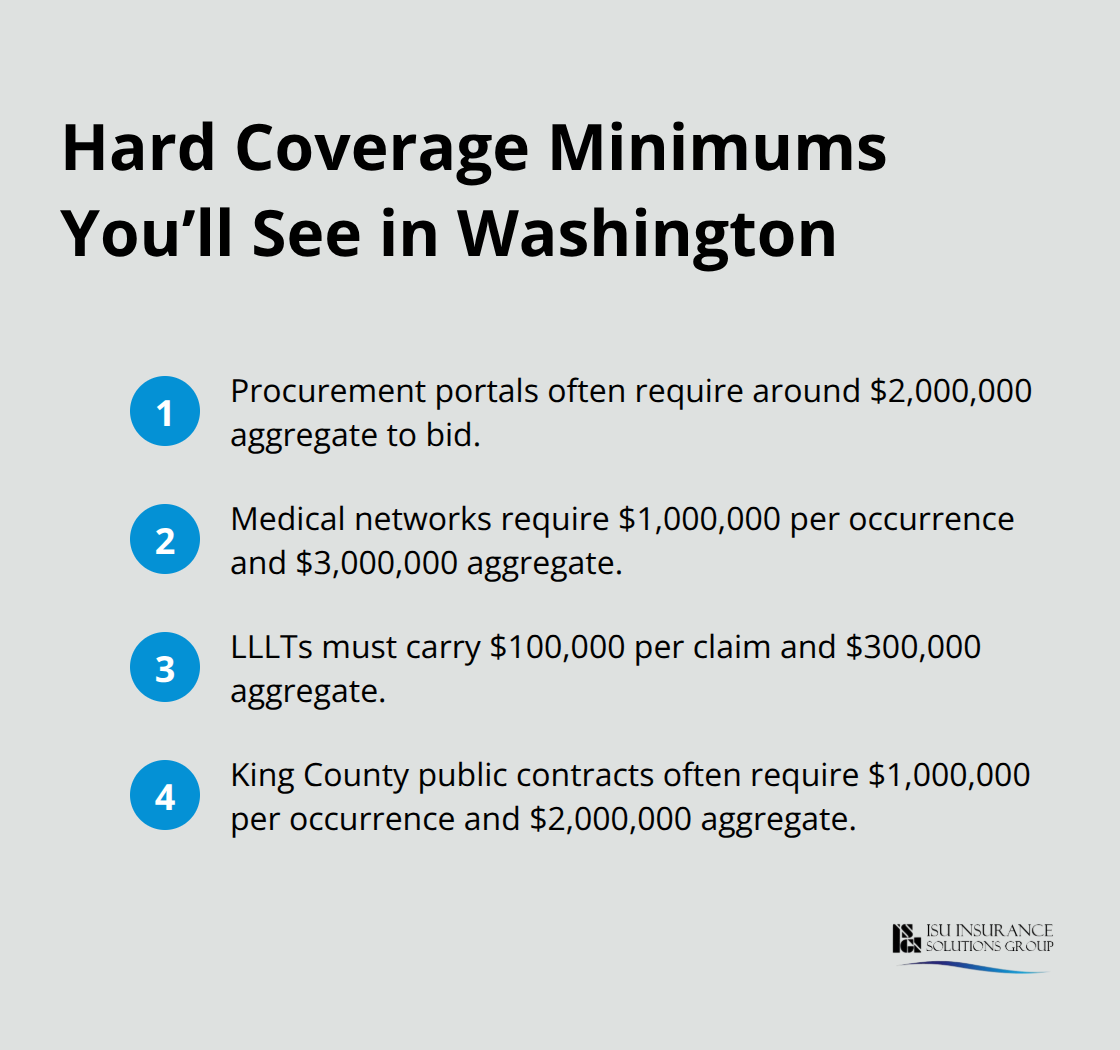

Procurement portals increasingly require proof of professional liability insurance with aggregate limits around $2 million before vendors can bid, which means lacking coverage blocks work opportunities. Medical professionals enrolling in insurance networks must carry at least $1,000,000 per occurrence and $3,000,000 annual aggregate to participate. Limited License Legal Technicians must maintain $100,000 per claim and $300,000 annual aggregate or face blocked client work.

These aren’t optional preferences-they’re hard requirements imposed by clients, networks, and regulatory bodies that directly affect your ability to operate and grow your practice in Washington. Understanding your specific coverage obligations is the first step toward protecting both your income and your professional standing.

How Washington’s Market and Rules Shape Your Coverage Needs

Regional Economic Clusters Drive Specialized Coverage

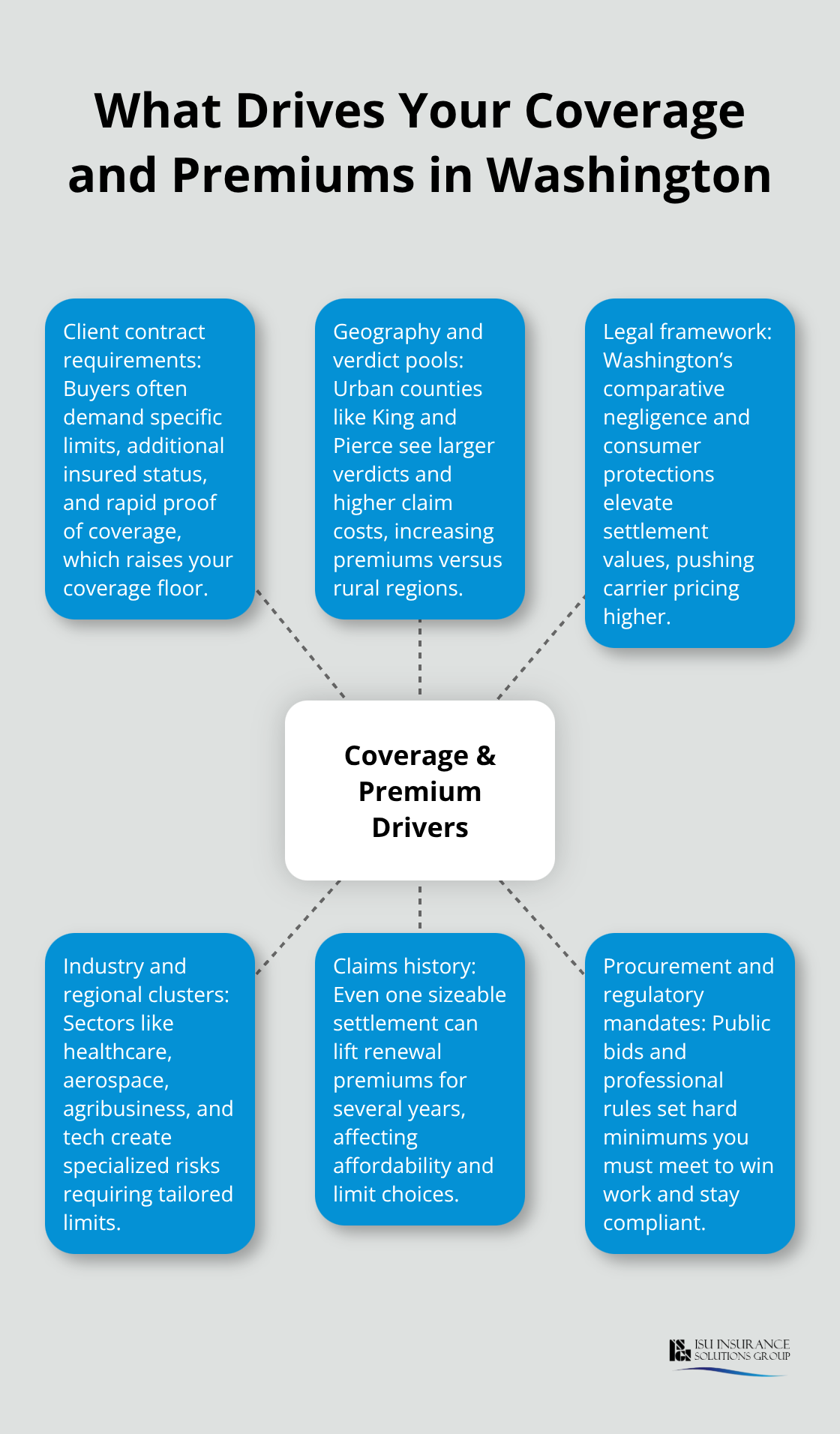

Washington’s economic clusters create vastly different professional liability exposures depending on where you operate and what you do. The Puget Sound aerospace sector, wine-region agribusiness, and Spokane’s growing healthcare hub each demand specialized coverage tailored to local risk patterns. King County procurement rules typically require $1,000,000 per occurrence and $2,000,000 aggregate for vendors bidding on public contracts, which means a consultant or architect working on county projects must meet these thresholds or lose the work entirely. Inland areas like Spokane and rural counties impose lower procurement minimums, but the exposure differences between regions are substantial.

How Geography Affects Your Premiums and Coverage Floor

If you serve clients across multiple regions, your highest requirement becomes your baseline coverage floor. Geography also drives premium costs directly: King County and Pierce County professionals typically pay 30 to 50 percent higher premiums than rural areas due to larger verdict pools and higher claim costs in urban centers. A five-attorney law firm in Seattle might pay $7,500 to $15,000 annually for $2,000,000 per occurrence and $4,000,000 aggregate coverage, while the same firm in Spokane could see premiums 30 to 40 percent lower. Washington’s pure comparative negligence system means courts assign fault proportionally, which increases settlement values because plaintiffs recover even when partially at fault. This legal framework pushes carriers to price policies higher in Washington than in states with stricter liability defenses, directly affecting what you pay for coverage.

Regulatory Boundaries That Determine Your Minimum Coverage

Regulatory requirements vary sharply by profession and create hard boundaries you cannot cross. Healthcare providers must report their insurance status and financial responsibility under RCW 7.70.150, and hospitals typically require physicians with admitting privileges to carry malpractice coverage. Architects must demonstrate E&O insurance for public contracts, and the Washington State Bar Association requires attorneys to report their insurance annually, though the WSBA does not independently verify coverage. Real estate professionals face no state mandate, but franchises and individual brokers frequently require E&O as a condition of employment. Technology firms increasingly face procurement demands for cyber-liability coverage bundled with professional liability, especially when handling client data or critical infrastructure.

Client Expectations Now Exceed Legal Minimums

Your specific regulatory obligations depend on your profession and client base, which is why a licensed Washington agent who understands your industry can identify gaps you might miss. Client expectations now routinely exceed legal minimums: many contracts specify minimum coverage limits, require the client to be named as additional insured, or demand proof of coverage within 24 hours of engagement. Dispute resolution in Washington increasingly favors mediation and settlement over litigation, but settlement negotiations still require proof of adequate coverage limits. Without documented insurance, clients assume you are uninsured or hiding risk, which damages trust and can cost you contracts before any claim arises.

These client-imposed requirements shape your actual coverage floor far more than state law does, making it essential to review your contracts and understand what your buyers and partners demand before you select a policy.

Sizing Coverage to Match Your Actual Exposure

List Your Services and Identify Your Highest-Risk Clients

Start by listing the specific services you provide and identifying your highest-risk client relationships. If you work across multiple sectors or geographies, your coverage floor is determined by your most demanding client, not your easiest one. A consultant serving both small startups and Fortune 500 companies must meet the Fortune 500 requirement, which typically means $1,000,000 per occurrence and $2,000,000 aggregate minimum. Real estate agents working with both residential buyers and commercial developers face the same dynamic: your largest transaction determines your baseline. Pull your last five client contracts and note every insurance requirement embedded in them-many professionals discover they’ve been operating under-insured because they never reviewed what clients actually demanded.

Medical professionals enrolling in insurance networks face non-negotiable minimums of $1,000,000 per occurrence and $3,000,000 annual aggregate, and hospitals often require higher limits for high-risk specialties like surgery or obstetrics. Your specific regulatory obligations depend on your profession and client base, which is why a licensed Washington agent who understands your industry can identify gaps you might miss.

Balance Your Deductible Against Cash Flow and Defense Costs

Your deductible choice matters more than most professionals realize. Increasing from $2,500 to $10,000 cuts premiums roughly 20 percent, but Seattle attorney rates hover around $367 per hour, meaning a $10,000 deductible absorbs 27 billable hours of defense costs before your carrier pays anything. If your cash flow cannot absorb a $10,000 hit immediately, the lower deductible saves money despite higher premiums. A five-attorney law firm in Seattle paying $7,500 to $15,000 annually for standard coverage faces a different risk calculation than a solo practitioner, and claims history reshapes everything: even one $250,000 settlement can lift renewal premiums 20 to 40 percent for three to five years.

Work with Local Agents Who Understand Washington’s Regional Differences

Choosing a local agent matters more than you might think because Washington’s regional differences are dramatic. King County and Pierce County premiums run 30 to 50 percent higher than inland areas due to verdict pools and claim costs, which means a consultant in Spokane should not expect to pay Seattle rates. A Woodinville-based independent agency like ISU Insurance Solutions Group has served Washington and Oregon since 1983 and partners with 20+ carriers, allowing you to access quotes from multiple insurers simultaneously and compare actual pricing instead of guessing.

Request identical coverage limits and deductibles across all quotes so actual rate differences become clear, then compare with quotes from at least two other carriers to verify competitiveness. Washington’s Office of the Insurance Commissioner publishes rate-change lookups by county and insurer, allowing you to benchmark what competing carriers have approved for similar businesses in your area.

Reduce Premiums Through Risk Management and Bundling

Documented risk management can yield 5 to 15 percent premium reductions: written safety protocols, quarterly jobsite inspections, subcontractor minimums, and incident reporting demonstrate underwriting discipline that carriers reward. Bundling professional liability with general liability, property, and commercial auto often yields 10 to 20 percent aggregate savings versus separate policies. When renewing, request your quote 60 to 90 days before expiration so you have time to negotiate or switch carriers without gaps.

Final Thoughts

Your coverage floor is determined by your most demanding client, not your easiest one. Medical professionals need $1,000,000 per occurrence and $3,000,000 aggregate to participate in networks, while attorneys and consultants bidding on King County projects face $1,000,000 per occurrence and $2,000,000 aggregate minimums. These aren’t optional-they’re hard requirements that block work if you fall short.

Geography shapes both your premiums and your coverage needs because King County and Pierce County professionals pay 30 to 50 percent higher premiums than inland areas due to larger verdict pools and higher claim costs in urban centers. Washington’s comparative negligence system means settlements tend to be larger than in other states, which carriers price into your policy. A five-attorney law firm in Seattle pays substantially more than the same firm in Spokane, reflecting these regional differences.

The practical next step is to pull your last five client contracts and identify every insurance requirement embedded in them. Then contact ISU Insurance Solutions Group to request quotes from multiple carriers simultaneously (we’ve served Washington and Oregon since 1983 and partner with 20+ insurers). A licensed local agent who understands your industry and region can identify gaps you might miss and help you avoid both overpaying and underinsuring your Washington professional liability insurance.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.