Business Vehicle Insurance Washington: Tailored Coverage for Local Firms

Running a fleet in Washington means navigating state-specific insurance rules that most business owners find confusing. Business vehicle insurance in Washington isn’t one-size-fits-all, and gaps in coverage can cost you thousands when accidents happen.

At ISU Insurance Solutions Group, we’ve helped hundreds of local firms find the right protection without overpaying. This guide walks you through what you actually need, where you can save money, and how to avoid the mistakes we see businesses make every day.

What Washington Businesses Actually Need to Cover

State Minimums Fall Short of Real Protection

Washington state requires a minimum of $25,000 bodily injury per person, $50,000 per accident, and $10,000 property damage for commercial vehicles. That baseline is the legal floor, not a safety net. For contractors, delivery services, and food trucks operating in Washington, these minimums leave significant exposure. A single accident involving multiple people or property damage to a commercial building can exceed these limits within minutes. Most businesses find that jumping to $100,000/$300,000/$50,000 costs only marginally more but eliminates genuine financial risk.

Vehicle Type and Usage Drive Coverage Needs

Your vehicle type and how you use it determine whether you need more than state minimums. A plumber with a single service van has different exposure than a landscaper running multiple trucks with trailers. Heavy trucks over 26,000 pounds gross vehicle weight rating face federal requirements that push minimums to $750,000 combined single limits or higher, depending on cargo type and interstate operations. Food trucks and mobile services need to think beyond liability-attached equipment, spoilage coverage, and product liability gaps exist in standard policies. Contractors hauling equipment face loading and unloading exposure that most don’t anticipate until something breaks during transport.

Personal Auto Policies Create Dangerous Gaps

The biggest mistake we see is assuming personal auto insurance works for business use. It doesn’t. A plumber who drives a personal truck to job sites, a real estate agent shuttling clients, or a consultant making client visits all need commercial coverage. Personal policies exclude business use and will deny claims outright if work activity is discovered. Small operators often skip uninsured motorist coverage because it’s optional in Washington, then face medical bills and vehicle damage when hit by an uninsured driver.

Additional Coverages Protect Against Hidden Losses

Collision and comprehensive coverage gets skipped too, leaving businesses vulnerable to theft, weather, and accident repair costs they can’t absorb. For fleets in the Seattle metro area, comprehensive coverage protects against theft and vandalism more than it does for rural operations. Medical payments coverage costs almost nothing but covers employee injuries regardless of fault, which matters when you’re liable for accident costs.

Static Policies Create Risk as Businesses Evolve

Coverage gaps compound because business owners often fail to review policies annually. As your business grows, your fleet changes, your routes shift, and your risk profile evolves-but the policy stays static. That’s when undercovered losses happen. The next section walks you through the specific coverage options that address these gaps and how to structure them for your operation.

Liability, Collision, and Uninsured Motorist Coverage Explained

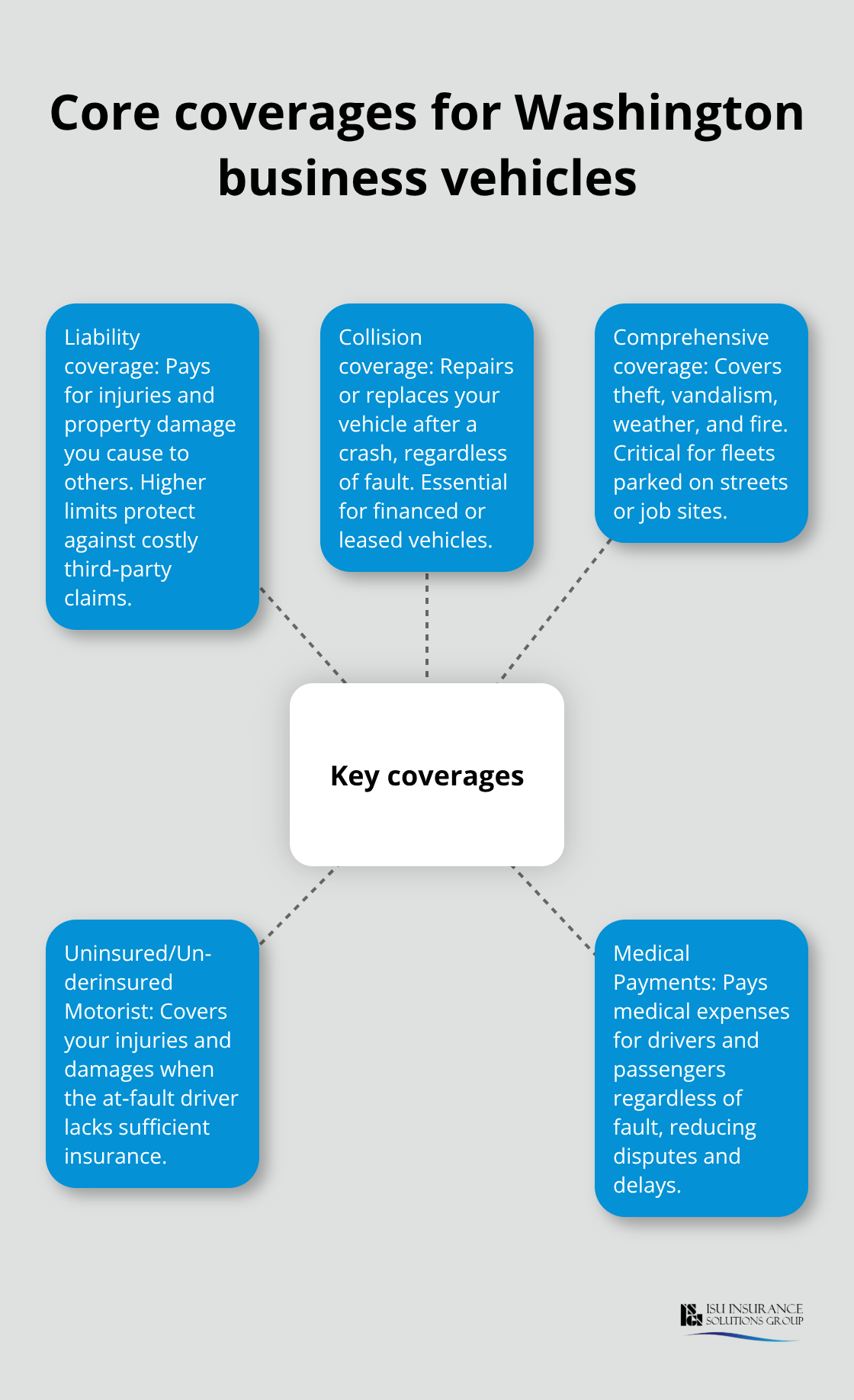

Liability Coverage Protects Your Business from Third-Party Claims

Liability coverage protects your business when your vehicle injures someone or damages their property. Washington requires combined single limit liability coverage in the amount of one million dollars for rideshare operations during prearranged rides. A contractor backing into a storefront, a delivery driver hitting a parked car, or a food truck colliding with another vehicle can easily exceed these limits in seconds. Try jumping to at least $100,000/$300,000/$50,000 for most Washington operations. For heavy trucks over 26,000 pounds or interstate operations, federal requirements mandate $750,000 combined single limits or higher depending on cargo type. The cost difference between state minimums and $100,000/$300,000 coverage typically runs $20–$50 monthly for most fleets, which is negligible compared to the financial exposure you eliminate.

Contractors, landscapers, and delivery services operating in Seattle, Tacoma, Bellevue, or surrounding areas face higher claim frequency due to urban congestion, so adequate liability limits become non-negotiable for these operations.

Collision and Comprehensive Coverage Protect Your Fleet Assets

Collision and comprehensive coverage protect your own vehicles rather than third parties. Collision pays repair or replacement costs after an accident regardless of fault, while comprehensive covers theft, vandalism, weather, and fire. Many Washington business owners skip these because they assume vehicles remain supervised at all times, but that assumption fails quickly. A contractor’s van parked at a job site overnight, a food truck in a busy Seattle neighborhood, or service vehicles left unattended during appointments all face real theft and vandalism risk. For fleets financed or leased, collision and comprehensive are typically mandatory. These coverages cost more upfront but prevent a single loss from derailing your operation or forcing you to absorb thousands in unexpected repair bills.

Uninsured Motorist Coverage Fills a Critical Gap

Uninsured and underinsured motorist coverage protects your business when another driver causes an accident but lacks sufficient insurance to cover your damages. Washington doesn’t require this coverage, but skipping it leaves your business exposed to uncompensated losses. An uninsured driver hitting one of your vehicles can trigger medical bills, repair costs, and lost productivity that your liability coverage alone won’t cover (liability only protects third parties, not your own losses). This coverage activates when the at-fault driver has no insurance or carries limits below what you need to recover fully.

Medical Payments Coverage Prevents Employee Disputes

Medical payments coverage covers employee and passenger medical expenses after an accident regardless of fault, costing roughly $15–$30 monthly per vehicle but eliminating out-of-pocket medical bills that employees might otherwise pursue through litigation. For fleets with multiple drivers or regular passenger transport, this coverage prevents small accidents from becoming employment disputes or wage claims. When an employee gets injured in a company vehicle, medical payments coverage handles their immediate medical needs without forcing them to file a personal injury claim against your business.

Structuring Coverage for Your Washington Operation

The right combination of these coverages depends on your vehicle type, routes, and business model. A single service vehicle operating locally within the Seattle metro needs different protection than a contractor fleet hauling equipment across Washington or a food truck operating multiple locations. Your coverage structure should reflect your actual exposure, not just legal minimums. As your fleet grows or your routes expand, your coverage needs shift-which is why annual policy reviews matter more than most business owners realize.

How to Lower Your Washington Business Vehicle Insurance Costs Without Cutting Coverage

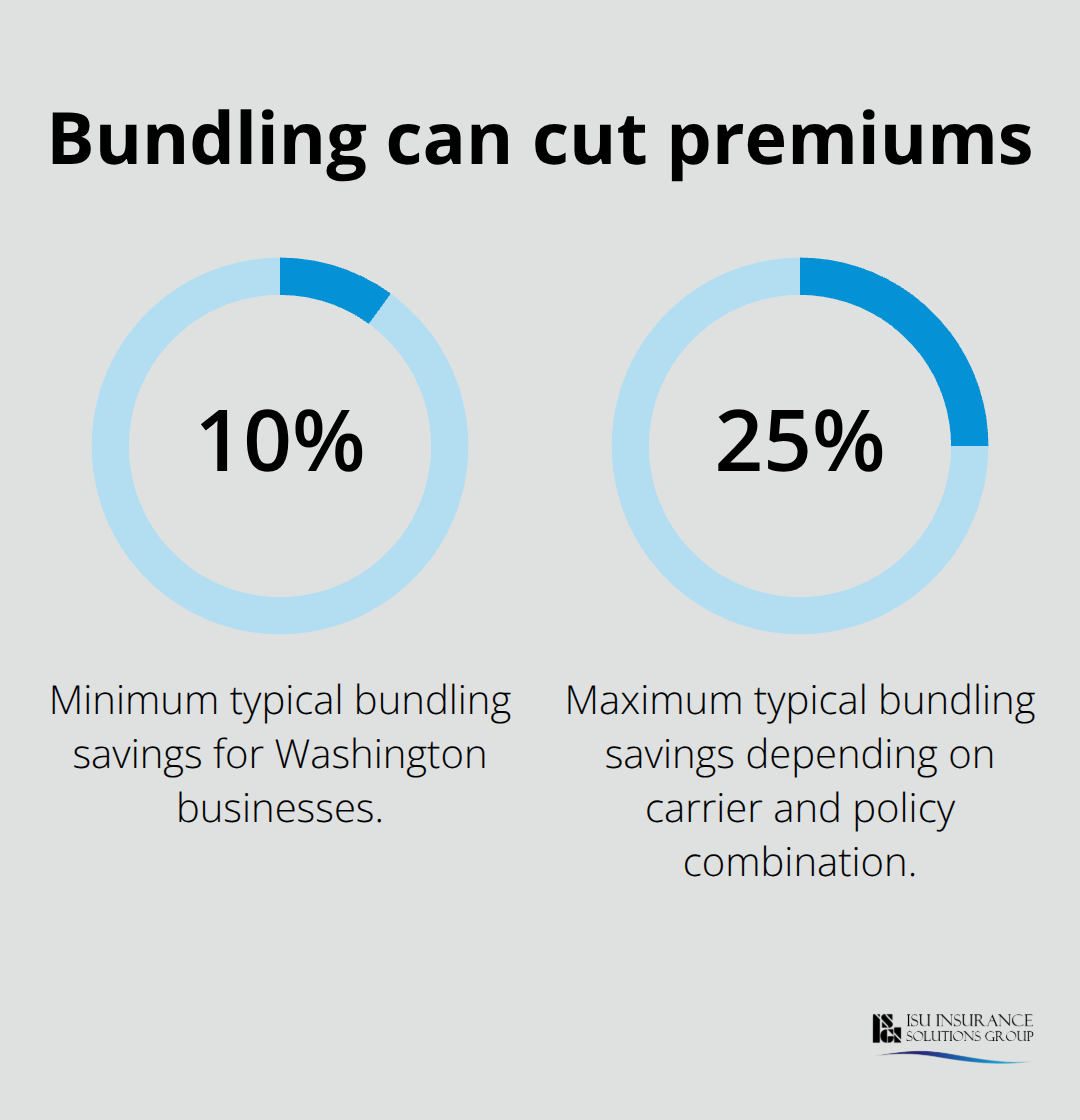

Bundle Policies to Unlock Substantial Discounts

Bundling commercial auto with property, general liability, or workers’ compensation coverage cuts your premium by 10 to 25 percent, depending on your carrier and which policies you combine. Most Washington business owners treat insurance policies as separate purchases, missing the discount tier that bundling unlocks. A contractor carrying general liability and commercial auto separately pays more than one who combines them under the same insurer.

The savings compound when you add property coverage for job site equipment or office space.

Different insurers reward bundling differently. Some carriers offer deeper discounts for adding workers’ compensation to an auto policy, while others prioritize bundling auto with property. A single phone call to compare multi-policy quotes across carriers beats shopping policies individually, which most business owners never do. Food truck operators who bundle auto, general liability, and property coverage often see combined annual premiums drop by $800 to $2,000 compared to purchasing each policy from different insurers.

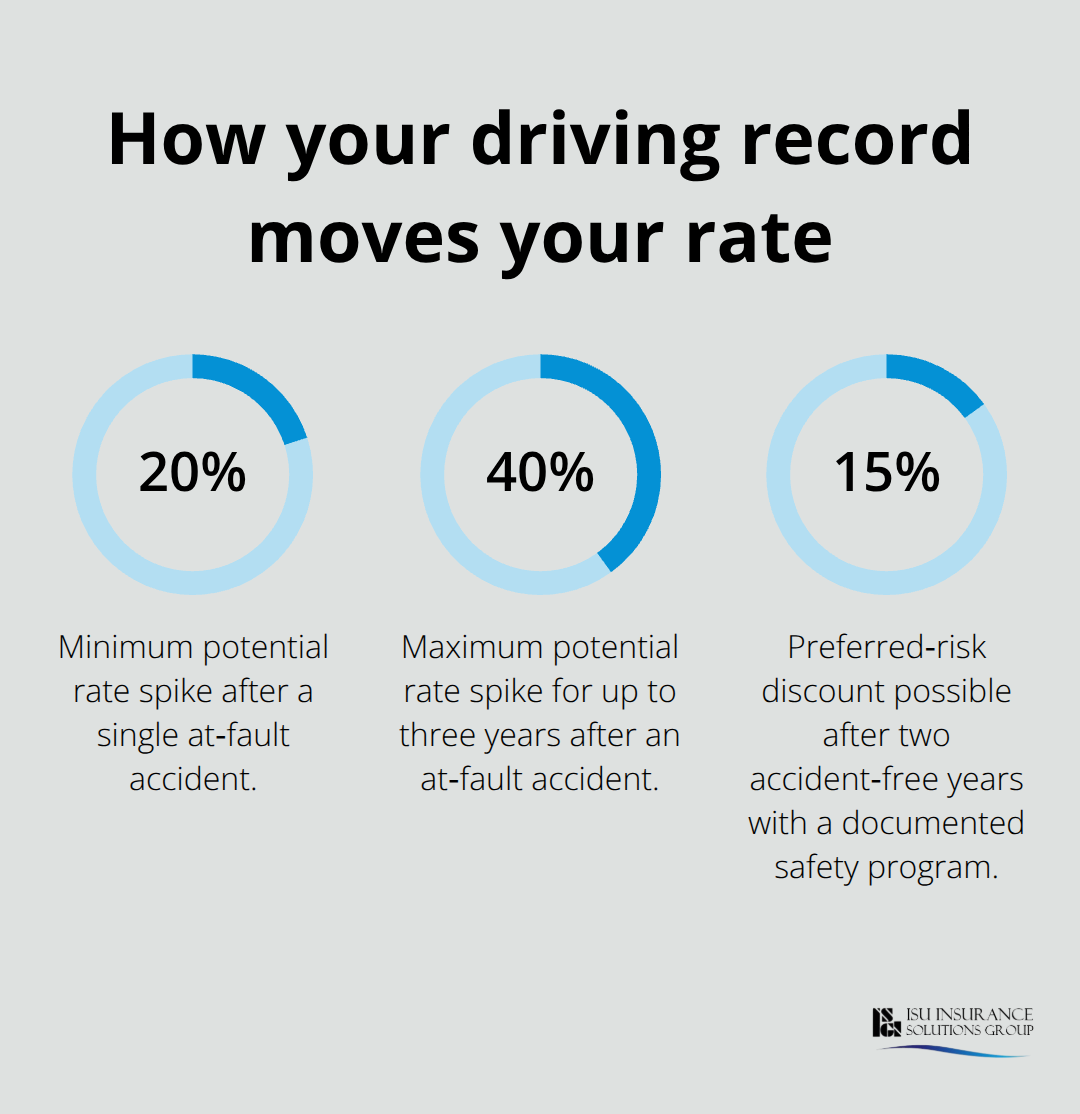

Maintain Clean Driving Records to Control Rates

Your driving and safety record directly controls premium rates more than any other factor. A single at-fault accident can spike your rates 20 to 40 percent for three years, making loss prevention worth far more than the discounts you chase. Contractors with documented safety programs and zero accidents over two years qualify for preferred-risk discounts that drop premiums 15 to 20 percent.

Specific actions reduce accident frequency enough that insurers reward you with lower rates on renewal. Install dash cameras on service vehicles, implement a formal vehicle maintenance schedule, and require safety training for all drivers. These measures demonstrate commitment to loss prevention and translate directly into rate reductions at renewal time.

Adjust Coverage When Your Fleet or Routes Change

Reviewing your policy annually instead of renewing automatically catches coverage gaps and allows you to adjust limits as your fleet changes. A landscaper who added two new trucks last year but never updated the policy leaves those vehicles potentially undercovered or overinsured depending on their value and use. When you review coverage annually, you also catch changes in your routes or service areas that affect your risk profile-local Seattle metro deliveries cost less to insure than regional routes spanning Spokane or Vancouver.

Carriers often offer rate reductions for policy renewals when you maintain clean records, so your renewal premium at year two or three can drop below year one if no claims occur. Your coverage structure should evolve with your business, not remain static while your operation grows.

Final Thoughts

Business vehicle insurance in Washington requires more than checking a box and hoping for the best. The coverage gaps we’ve outlined-from inadequate liability limits to missing collision protection-compound over time and hit hardest when you can’t afford them. State minimums exist to satisfy legal requirements, not to protect your business from real financial exposure. Your fleet, your routes, and your specific operation demand coverage tailored to what you actually face on Washington roads.

Getting the right protection means working with someone who understands Pacific Northwest business operations and knows how to structure coverage across multiple carriers. Generic quotes from national platforms miss the nuances that matter for contractors, food trucks, landscapers, and service fleets operating in Seattle, Tacoma, Spokane, or anywhere else in Washington. Your policy should reflect your actual risk, not a template built for businesses in other states with different conditions and requirements.

The next step is straightforward: reach out for a personalized quote that reflects your fleet, your routes, and your actual exposure. Visit ISU Insurance Solutions Group to connect with a local agent who can walk you through your options and show you where you stand exposed. A quick conversation now prevents expensive mistakes later.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.