Personal Auto Insurance Oregon: What Drivers Should Know

Oregon drivers face a complex insurance landscape with state-mandated requirements and optional coverage choices that directly impact protection and costs. Getting personal auto insurance in Oregon right means understanding both what’s legally required and what makes financial sense for your situation.

We at ISU Insurance Solutions Group help drivers navigate these decisions by breaking down coverage types, rate factors, and practical strategies for finding affordable policies. This guide walks you through everything you need to know to make informed choices about your auto insurance.

Oregon Auto Insurance Requirements and Coverage Types

State-Mandated Minimum Coverage

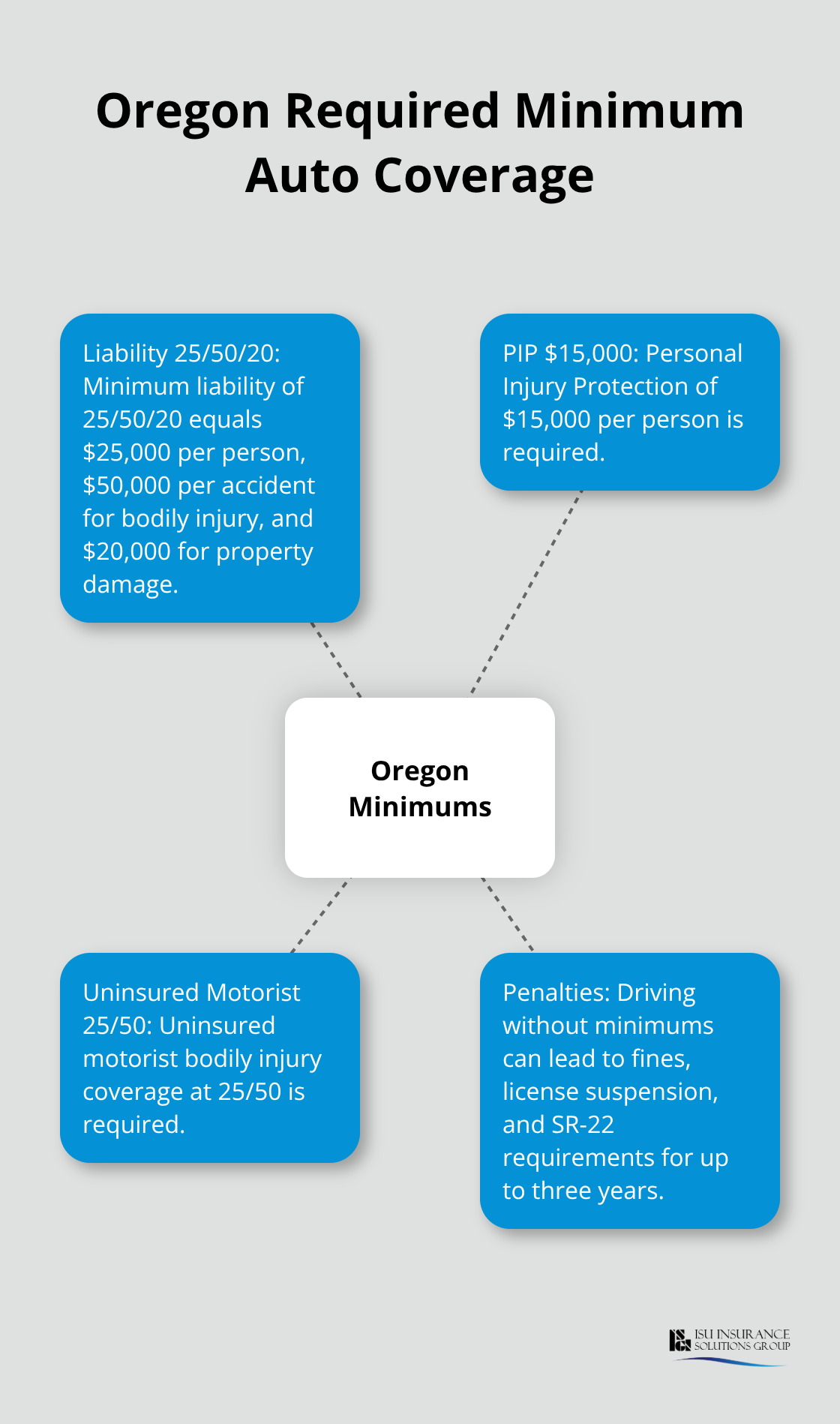

Oregon law mandates that every driver carry minimum liability coverage of 25/50/20, meaning $25,000 per person and $50,000 per accident for bodily injury, plus $20,000 for property damage. You also need $15,000 in Personal Injury Protection per person and uninsured motorist coverage at 25/50. Driving without these minimums is illegal and can result in fines, license suspension, and SR-22 requirements lasting up to three years.

State minimums are genuinely inadequate for real-world protection. A single serious accident can easily exceed these limits, leaving you personally liable for medical bills, lost wages, and vehicle repairs. Higher limits like 100/300/100 or 250/500/250 cost only modestly more than minimums while providing substantially better protection. According to data from Quadrant Information Services, the difference between minimum and full coverage in Oregon averages roughly $1,280 annually, but that gap narrows significantly when you compare minimum coverage to higher liability limits alone.

Physical Damage Coverage for Your Vehicle

Comprehensive and collision coverage protects your own vehicle rather than others, which is why lenders require these when you finance or lease a car. Comprehensive covers theft, weather, vandalism, and animal strikes, while collision handles accidents with other vehicles or objects. These aren’t legally required if you own your car outright, but skipping them is financially risky.

The real decision involves your deductible: raising it from $250 to $500 or $1,000 substantially lowers your premium, but you pay that amount out-of-pocket when you file a claim. This trade-off works well if you have emergency savings to cover a higher deductible, but it creates real financial strain if an accident happens and you lack those reserves.

Protection Against Uninsured Drivers

Uninsured motorist coverage protects you if an uninsured or hit-and-run driver causes an accident. Given that uninsured drivers pose a genuine risk on Oregon roads, this coverage deserves serious consideration even though it’s optional. Uninsured motorist property damage is also optional but worth evaluating, especially if you drive a vehicle where repair costs might exceed your deductible anyway.

These optional coverages matter because they fill gaps that state minimums leave wide open. Once you understand what Oregon requires and what optional protections actually serve your situation, the next step involves recognizing which factors most heavily influence what you’ll actually pay for that coverage.

What Drives Your Auto Insurance Rates in Oregon

Your Driving Record Sets the Foundation

Your driving record is the single most powerful factor determining what you pay for auto insurance in Oregon, and the impact is severe. A single at-fault accident raises your premium by roughly 49%, according to data from Quadrant Information Services, while a speeding ticket adds about 24%. A DUI conviction increases rates by 54% to 86% compared to a clean record. Insurers review your driving history from the past three years, pulling records from the Oregon DMV and other states, so one bad decision affects your wallet for years.

Defensive driving saves money far more effectively than any discount or policy adjustment ever will. If you’ve already accumulated violations, an approved defensive driving course can help offset rate increases and demonstrates commitment to safer driving.

Credit Score Creates Massive Rate Gaps

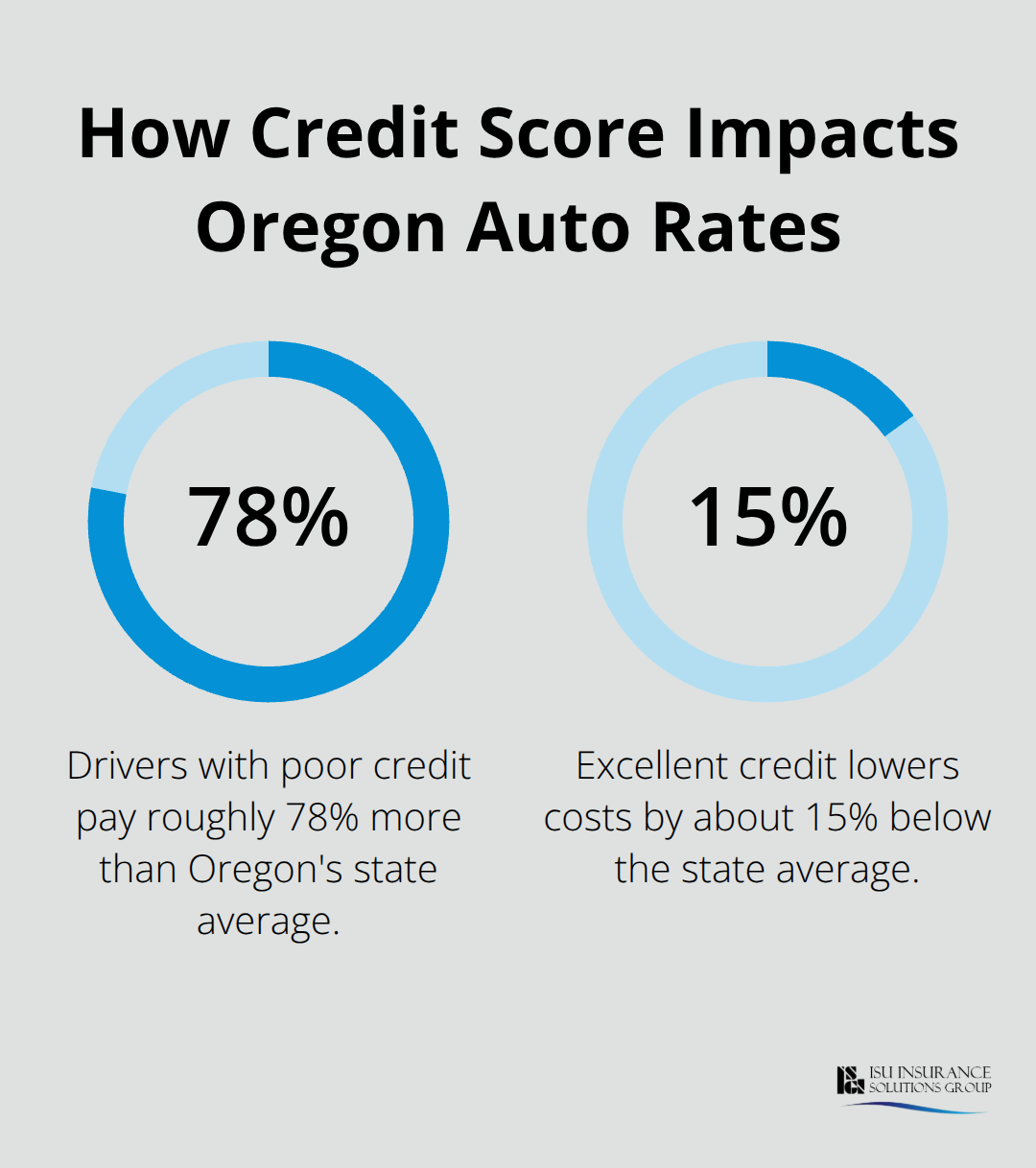

Credit score matters almost as much as your driving record, and the gap between poor and excellent credit is staggering. Drivers with poor credit pay roughly 78% more than Oregon’s state average, while excellent credit lowers costs by about 15% below average.

This means a driver with poor credit might pay $303 monthly while someone with excellent credit on the same policy pays $139-a difference of $1,968 annually.

Improving your credit score produces measurable savings over time. Even modest improvements in your credit profile can lower your monthly payments substantially, making this one of the few rate factors you can actively control.

Vehicle Type and Age Shape Your Costs

Vehicle type significantly influences rates; a BMW 330i costs around $2,548 per year for full coverage while a Toyota Prius runs about $2,148, and a Honda Odyssey roughly $1,883. Age creates dramatic rate variations too-a 25-year-old pays approximately $2,723 annually for full coverage while a 60-year-old pays roughly $1,906 for identical protection.

Young drivers face the harshest penalty; an 18-year-old on their own policy pays around $6,100 per year, making a parent’s policy substantially cheaper until you can demonstrate a clean driving record. These factors interact constantly, meaning your exact situation determines your exact rate.

Taking Control of What You Can Change

If you’re shopping for coverage and have multiple factors working against you (young age, recent ticket, lower credit score), focus on what you can control. Maintaining a clean driving record going forward and raising your deductible to lower premiums are concrete actions that produce measurable savings.

Understanding these rate drivers prepares you to shop strategically. The next step involves knowing where to find the most competitive quotes and which discounts actually move the needle on your final bill.

Finding the Best Rates Without Wasting Time

Compare Quotes Across Multiple Carriers

Shopping for auto insurance in Oregon means obtaining quotes from multiple carriers because rates vary wildly between insurers for identical coverage. Progressive offers Oregon’s most affordable rates for full coverage, while Country Financial averages about $172 monthly for the same protection. That difference makes quote comparison genuinely worth your effort. For minimum liability coverage, Travelers posts the lowest rates at roughly $56 per month compared to Country Financial at about $92-another significant gap that justifies spending 30 minutes to gather quotes from at least three carriers before you decide.

Leverage Discounts That Actually Save Money

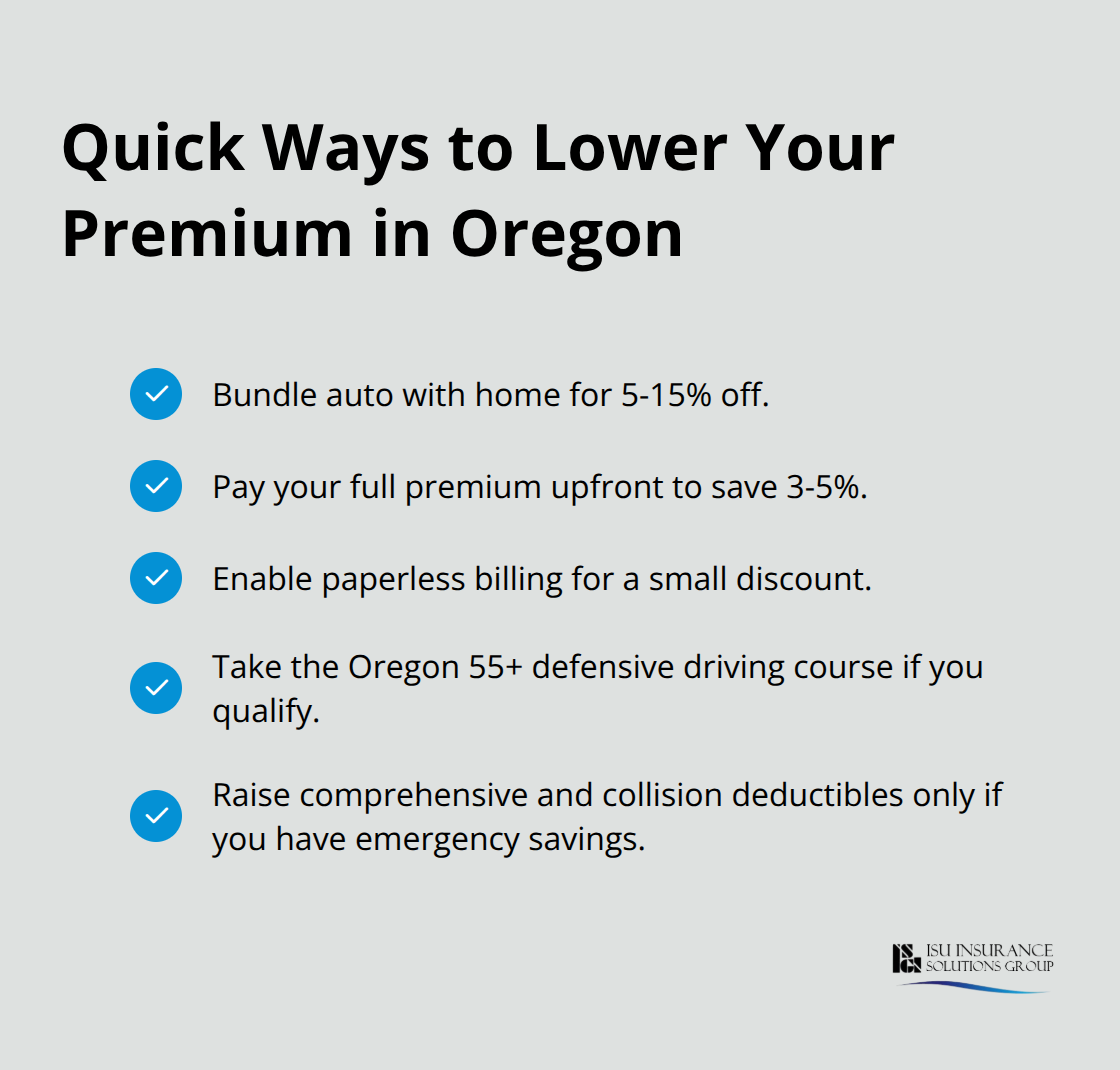

Your credit score and driving record lock in your base rate, but discounts and deductible choices create the second layer of savings. Bundling auto with home insurance typically reduces your auto premium by 5-15%, while paying your full premium upfront rather than monthly often saves another 3-5%. Paperless billing discounts exist across most carriers, and Oregon offers a specific 55+ defensive driving discount worth pursuing if you qualify. Raising your collision and comprehensive deductible from $250 to $500 cuts premiums noticeably, though this strategy only works if you have emergency savings to cover that deductible after an accident.

Adjust Your Deductible Strategy

The deductible you select directly impacts what you pay each month and what you owe when you file a claim. Higher deductibles reduce your premium substantially, but they create real financial strain if an accident happens and you lack emergency reserves. Try a $500 or $1,000 deductible only if you can actually afford to pay that amount out-of-pocket without hardship.

Monitor Rates and Re-Shop Annually

Rate changes happen constantly, and Oregon drivers should re-shop their coverage annually or after major life changes like moving, getting married, or purchasing a vehicle, since your current insurer’s renewal quote may no longer be competitive. Travelers tends to offer smaller rate increases after at-fault accidents compared to other major Oregon carriers, which matters if you’re rebuilding from a recent claim. Checking rates once per year takes minimal time and frequently uncovers savings you wouldn’t find otherwise.

Final Thoughts

Personal auto insurance in Oregon requires you to balance legal minimums with realistic protection for your situation. State-mandated coverage of 25/50/20 liability, $15,000 PIP, and 25/50 uninsured motorist protection keeps you legal, but these limits leave you exposed to substantial out-of-pocket costs after a serious accident. Higher liability limits like 100/300/100 cost only modestly more while protecting your assets far better, and raising your deductible from $250 to $500 or $1,000 meaningfully reduces your monthly premium if you have emergency savings to cover that amount.

Your driving record and credit score determine your base rate more than any other factor. A clean driving record saves you thousands annually compared to someone with recent violations, while excellent credit cuts costs roughly 15% below Oregon’s average. Comparing quotes from at least three carriers typically reveals rate differences exceeding $100 monthly for identical coverage, making this effort genuinely worthwhile, and bundling auto with home insurance, paying your premium upfront, and pursuing available discounts add another layer of savings without reducing your protection.

Rate changes happen constantly, so reviewing your coverage annually or after major life changes prevents you from overpaying. We at ISU Insurance Solutions Group help Oregon drivers navigate personal auto insurance decisions with personalized quotes from multiple carriers and hands-on guidance tailored to your specific situation. Contact us today to compare your options and secure the right policy for your circumstances.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.