Craft Brewery Insurance Costs: Budgeting for Stability

Craft brewery insurance costs eat into your bottom line faster than you’d expect. Most brewery owners underestimate what they’ll actually pay until renewal time hits.

We at ISU Insurance Solutions Group help breweries understand their real insurance expenses and find ways to reduce them. This guide breaks down what drives your premiums and how to budget smarter.

What Actually Drives Your Brewery Insurance Premiums

Your insurance bill isn’t random. It’s built on concrete factors that underwriters measure and price into every quote.

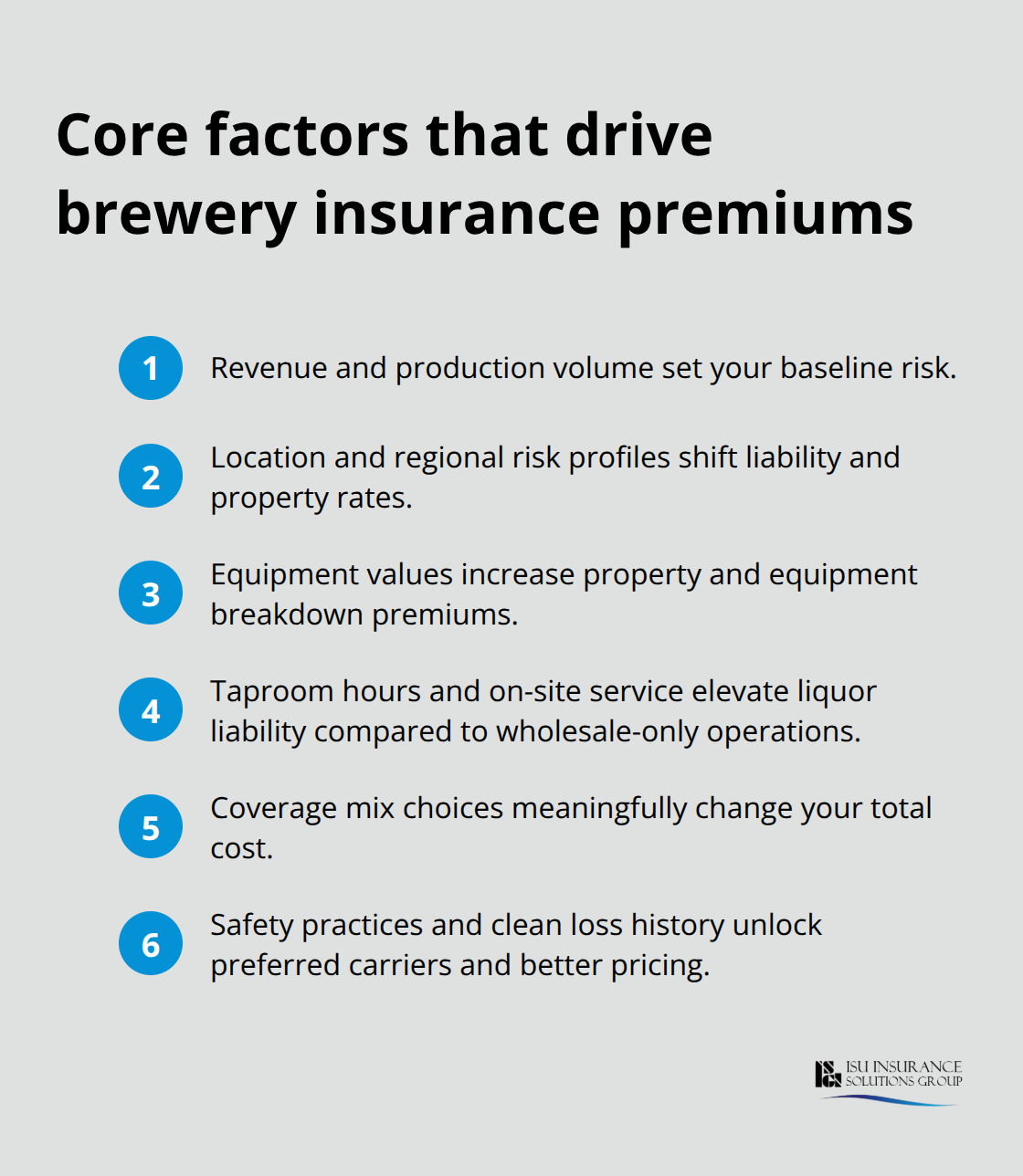

Revenue and Production Volume Set the Foundation

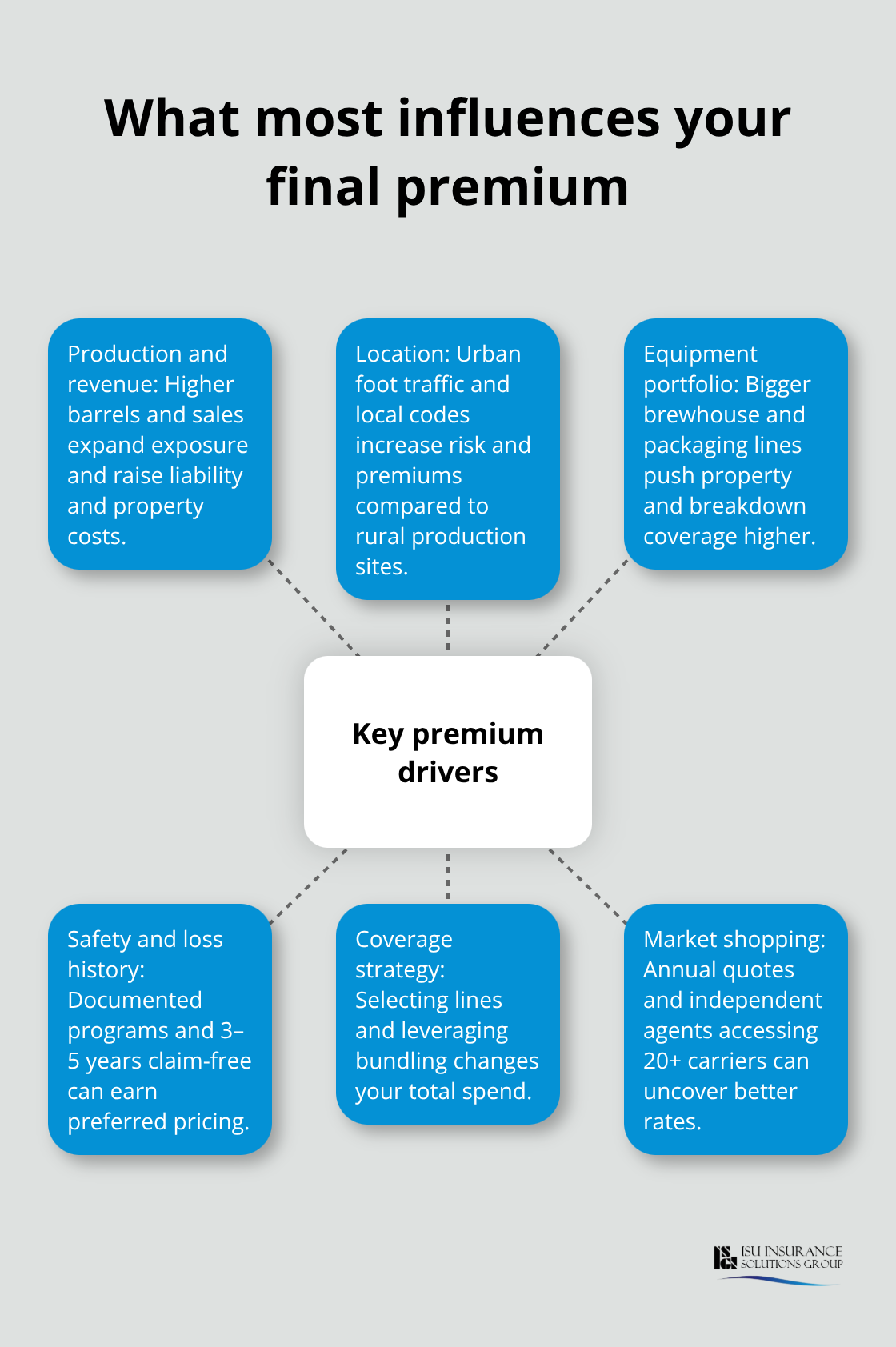

The biggest driver is your revenue and production volume. A brewery producing 500 barrels annually with $300,000 in revenue pays dramatically less than one hitting 5,000 barrels and $3 million. According to typical annual premium ranges, general liability alone runs $1,000 to $6,000 yearly, but that scales with your operation size. Liquor liability premiums average around $540 annually for smaller operations but climb past $10,000 for high-volume taproom businesses with extended hours.

A brewery doing $1 million in annual alcohol sales with a packed taproom pays substantially more than a production-focused facility selling mostly wholesale.

Location and Regional Risk Profiles Matter

Your location shapes your costs significantly. Oregon and Washington have different regulatory environments and risk profiles. A brewery in Portland faces different liability exposure than one in rural Eastern Oregon, affecting everything from slip-and-fall frequency to local code compliance costs. Urban taprooms with foot traffic and events pay higher premiums than quieter production facilities. Commercial property rates also shift by region and building type.

Equipment Value and Coverage Choices

Your equipment value directly impacts premiums. A $150,000 brewhouse system, $75,000 canning line, and supporting tanks create substantial property insurance costs. Equipment breakdown coverage, which protects against costly downtime when systems fail, ranges from $400 to $3,000 annually depending on your equipment portfolio and age.

The coverage mix you select determines roughly 40 to 50 percent of your total cost. General liability provides baseline protection against slip-and-fall claims and third-party injuries, but if you run a taproom, liquor liability becomes non-negotiable and often costs more than general liability itself. Workers’ compensation averages $45 monthly but varies by payroll size and state regulations. Product liability coverage, protecting against contamination or labeling errors, typically costs $500 to $2,000 annually but depends on your distribution reach. A brewery shipping direct-to-consumer across state lines faces higher product liability exposure than one selling only locally.

Real Costs Across Different Operation Sizes

A small 5-barrel operation with a modest taproom budgets roughly $5,000 to $8,000 annually for core coverage. A 50-barrel facility with aggressive wholesale distribution and events runs $12,000 to $18,000. The largest regional producers exceed $25,000 yearly. Those numbers reflect production volume, taproom hours, delivery radius, and equipment values.

ABV matters too. High-alcohol specialty beers or ready-to-drink products increase liability classification and premiums. A brewery making 12% ABV imperial stouts pays more than one focused on sessionable 5% lagers. Safety measures directly reduce what insurers charge. Documented equipment maintenance, staff TIPS training, slip-resistant flooring, security cameras, and clean loss history all unlock better rates. Three to five years without claims opens access to preferred carriers and discounts of 10 to 20 percent. Understanding these cost drivers positions you to identify where you can reduce premiums without sacrificing protection-which is exactly what the next section covers.

How to Cut Brewery Insurance Costs Without Cutting Coverage

Bundle Coverage Types for Immediate Savings

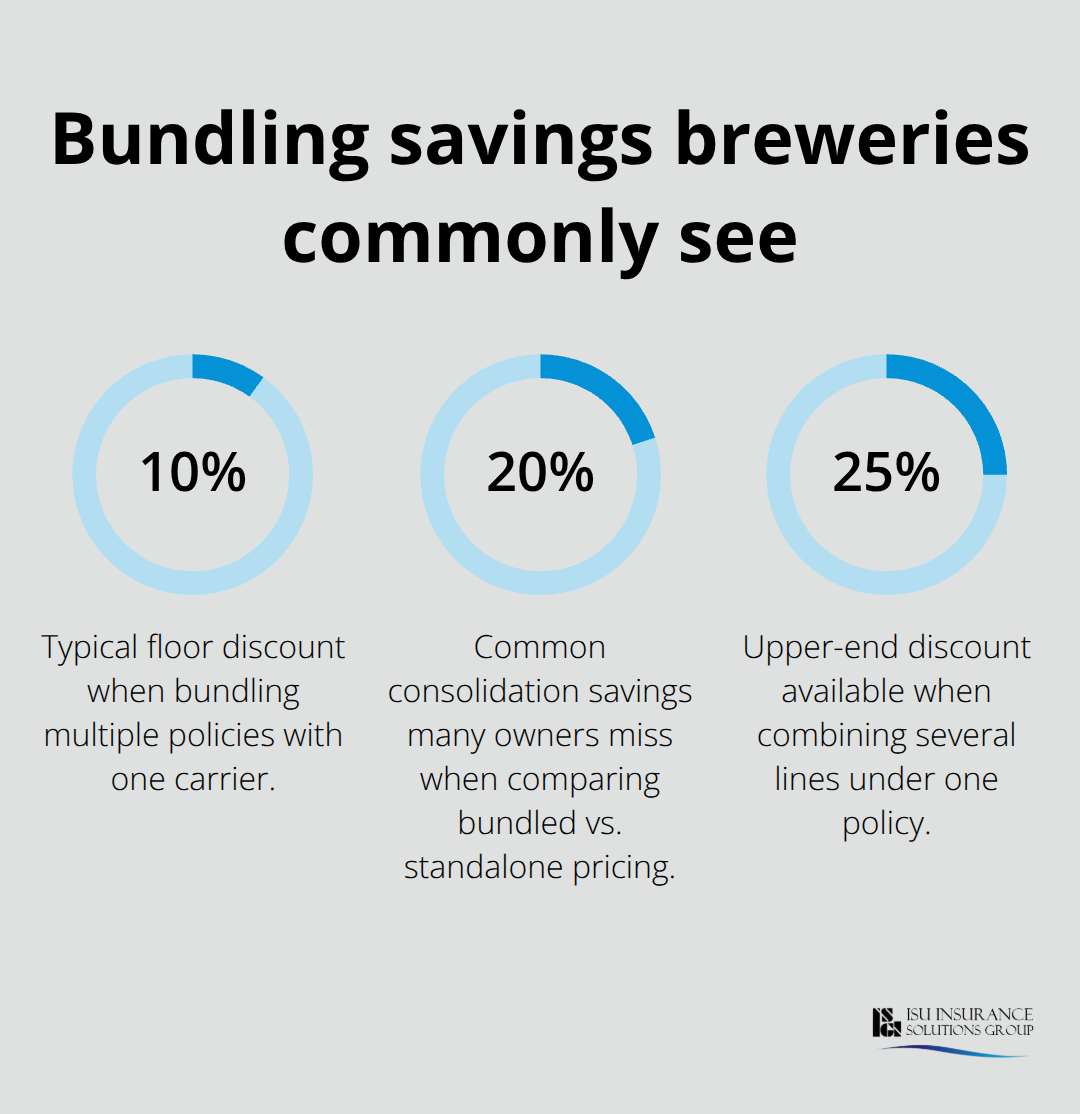

Bundling your coverage types cuts what you actually pay faster than any other strategy. Most insurers offer discounts ranging from 10 to 25 percent when you combine general liability, liquor liability, workers’ compensation, and property coverage under one policy. A brewery paying $1,200 for general liability and $540 for liquor liability separately might negotiate that down to $1,400 total through bundling.

The insurer gains stickier customer retention, and you get immediate savings. Underwriters prefer writing multiple lines for one risk they already understand.

When comparing quotes, request bundled pricing alongside individual line pricing so you see the actual discount. Many brewery owners focus only on the general liability quote and miss 15 to 20 percent savings available through consolidation.

Safety Programs Lower Your Risk Classification

Safety programs and loss prevention reduce your premiums because they lower claim frequency. Documented equipment maintenance logs, TIPS alcohol service training for all staff, slip-resistant mats, security camera footage, and clean loss history over three to five years unlock preferred carrier access and rate reductions of 10 to 20 percent. A brewery with zero claims over five years moves into a preferred underwriting class and qualifies for better pricing than one with even minor losses.

Install grain-dust controls, maintain CO2 monitoring systems, and enforce hot-work permits-these specific safety measures appeal to underwriters and get reflected in lower quotes. Your loss history matters most; three to five years without claims opens doors to preferred carriers and discounts that compound over time.

Compare Quotes Annually to Catch Rate Creep

Annual quote comparison matters because your renewal premium often creeps up even without claims. Getting three quotes annually takes four hours and frequently saves $2,000 to $5,000 on a $10,000 policy. Your production volume, equipment additions, safety improvements, or staffing changes shift your risk profile yearly, and new carriers price differently based on your current operations.

Work with an agent who understands brewery operations and can place your account across multiple carriers rather than one who defaults to your current insurer at renewal. An independent agency like ISU Insurance Solutions Group, serving Washington and Oregon since 1983, can access quotes from 20+ carriers in one call and identify where your specific operation qualifies for the best rates. Your risk profile changes constantly, and carriers that rejected you two years ago may now offer competitive pricing based on your improved safety record or lower production volume.

What Breweries Actually Pay for Insurance

Small 5-barrel operations with modest taprooms budget roughly $5,000 to $8,000 annually for core coverage combining general liability, liquor liability, workers’ compensation, and basic property protection. A 50-barrel facility running aggressive wholesale distribution and hosting events typically spends $12,000 to $18,000 yearly. Regional producers exceeding 100 barrels annually often exceed $25,000. These ranges reflect real-world pricing where production volume, taproom operating hours, delivery radius, equipment values, and loss history drive the final number. A brewery generating $300,000 in annual revenue with minimal on-site service pays substantially less than one hitting $3 million with a packed taproom running 12-hour days. General liability alone ranges from $1,000 to $6,000 annually depending on operation size, while liquor liability premiums average $540 for smaller operations but climb past $10,000 for high-volume taprooms with extended hours. Workers’ compensation averages $45 monthly but varies by payroll size and state regulations. Equipment breakdown coverage protecting against costly downtime ranges from $400 to $3,000 annually based on your equipment portfolio and age.

Cost Differences Between Washington and Oregon Markets

Washington and Oregon breweries face different premium structures due to regulatory environments and regional risk profiles. A Portland taproom-focused brewery pays higher premiums than a similar operation in rural Eastern Oregon because urban foot traffic increases slip-and-fall exposure and liquor liability risk. Washington’s regulatory framework differs from Oregon’s, affecting compliance costs and underwriter classifications. A brewery in the Seattle metro area typically pays 15 to 25 percent more for liquor liability than one operating in smaller Washington towns. Commercial property rates also shift by region and building type, with urban locations commanding higher premiums than rural production facilities. Oregon’s craft beer market shows strong wholesale distribution networks, which can lower per-barrel costs for distribution-focused breweries compared to those with heavy taproom exposure.

Local building codes, fire suppression requirements, and municipal regulations influence property insurance costs differently across these states. Agents familiar with brewery and distillery coverage understand how local factors affect your actual costs because regional underwriting preferences vary significantly.

Equipment Values and Safety History Shape Your Real Quote

Your equipment portfolio directly determines property and equipment breakdown costs. A brewery with a $150,000 brewhouse system, $75,000 canning line, and supporting fermentation tanks generates substantially higher property insurance premiums than one with basic brewing equipment. High-ABV specialty beers or ready-to-drink products increase liability classification and premiums compared to sessionable lager-focused breweries. Documented equipment maintenance logs, TIPS training completion for all staff, slip-resistant flooring, security camera installation, and three to five years without claims unlock preferred carrier access and rate reductions of 10 to 20 percent. A brewery with zero losses over five years moves into preferred underwriting classes and qualifies for significantly better pricing than one with even minor historical claims. Grain-dust controls, CO2 monitoring systems, and enforced hot-work permits appeal directly to underwriters and get reflected in lower quotes. Your loss history matters most because it demonstrates operational competence and risk management discipline. Carriers that rejected your account two years ago may now offer competitive pricing based on your improved safety record or production changes.

Final Thoughts

Craft brewery insurance costs don’t have to drain your profitability if you approach them strategically. Your premiums reflect your actual risk profile, and you control most of the factors that determine what you pay-production volume, location, equipment value, and safety practices all drive your costs. Bundling coverage types, maintaining clean loss history, and comparing quotes annually cut what you actually spend without reducing protection.

Small breweries budgeting $5,000 to $8,000 annually and larger operations spending $12,000 to $25,000 yearly share one common mistake: they renew with the same carrier without checking if better rates exist elsewhere. Your risk profile changes constantly as you add equipment, expand your taproom hours, or improve safety measures. Getting three quotes takes a few hours and frequently saves $2,000 to $5,000 on a $10,000 policy.

Working with an agent who understands brewery operations matters more than you might think. An independent agency accesses quotes from multiple carriers in one call rather than defaulting to your current insurer at renewal. ISU Insurance Solutions Group has served Washington and Oregon breweries since 1983, accessing 20+ carriers to find competitive rates tailored to your specific operation.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.